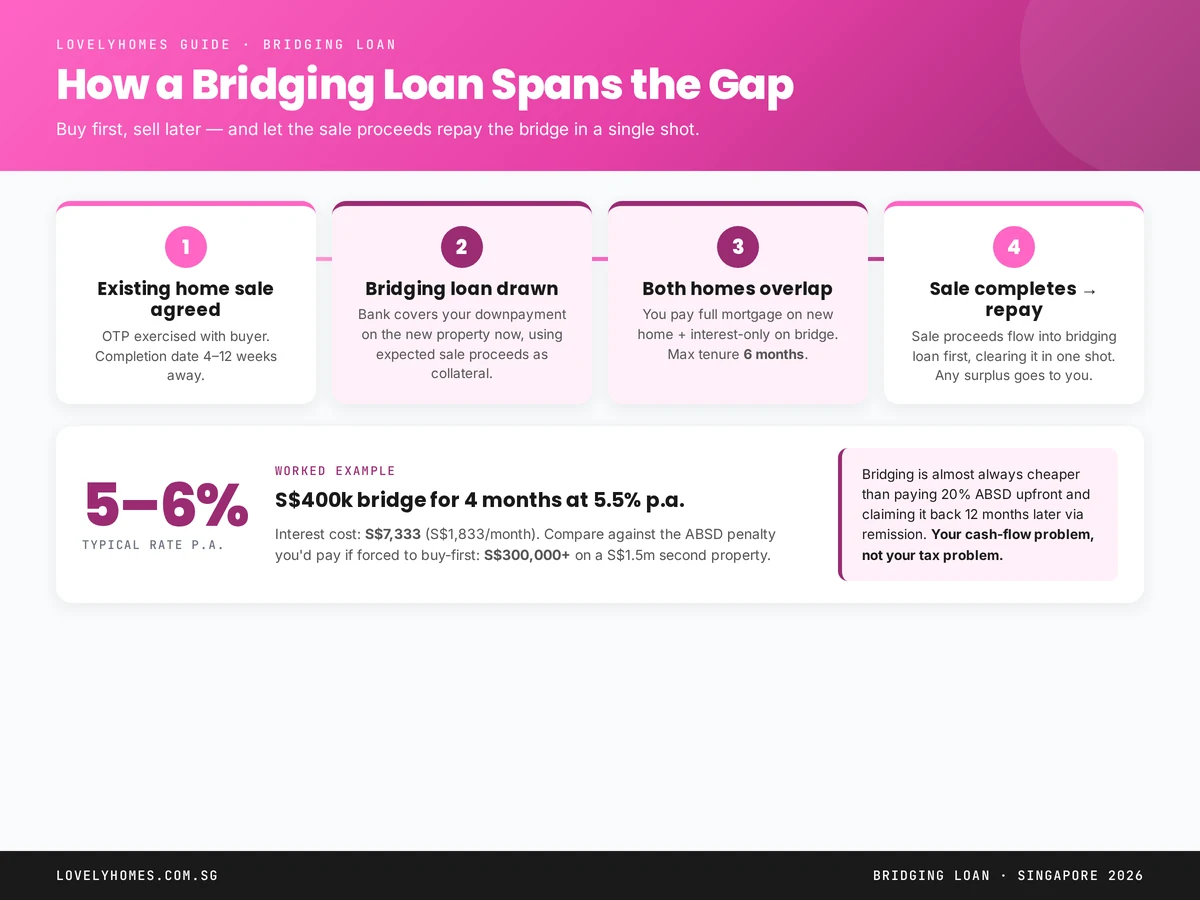

Singapore Executive Condo (EC) Buying Guide 2026: Eligibility, Prices, MOP and the New 10-Year Rules Explained

Quick Answer — Singapore Executive Condo (EC) at a glance

- EC household income ceiling: S$16,000/month (unchanged in 2026)

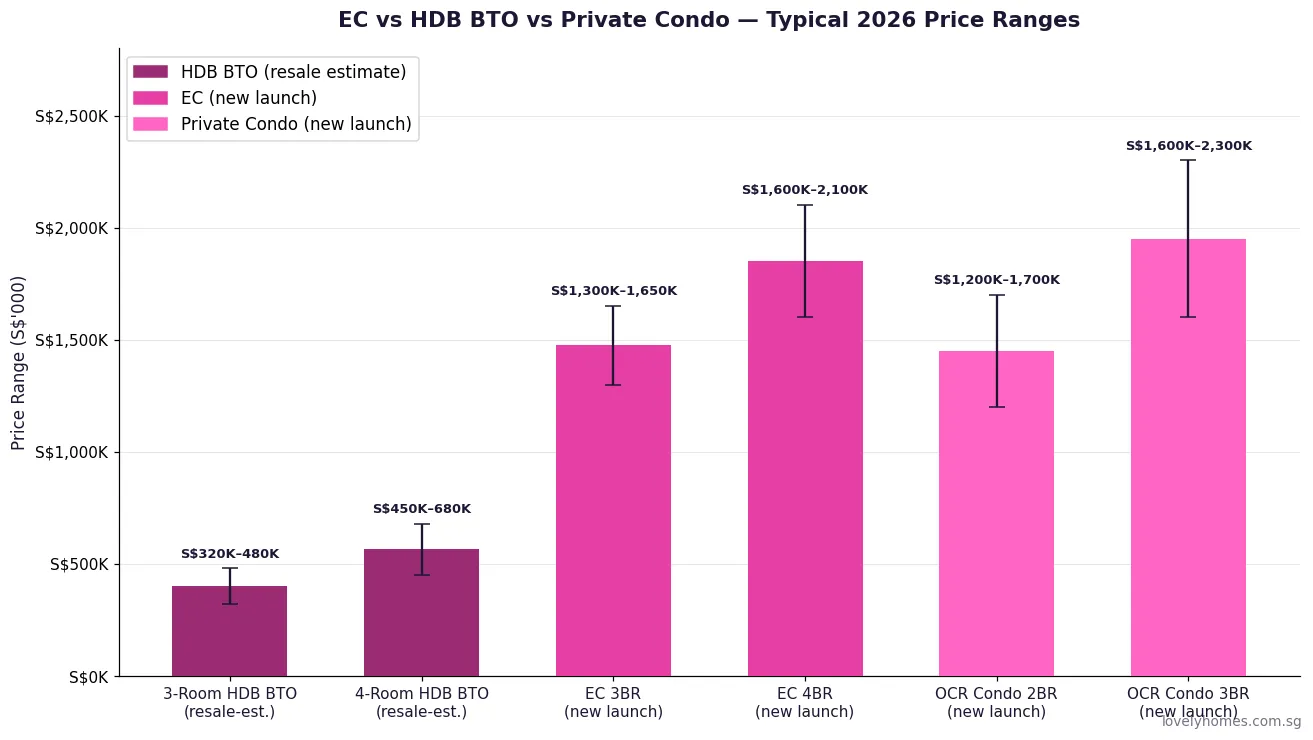

- EC prices in 2026: roughly S$1.3M–S$2.2M for new launches, depending on unit size

- At least one Singapore Citizen applicant required; co-applicant can be SC or PR

- New EC sites from 8 May 2026: 10-year MOP and 15-year wait to full privatisation

- Existing launched ECs retain the older 5-year MOP and 10-year privatisation timeline

- ECs occupy the unique “sandwich class” position — priced above HDB BTO but below private condos

- CPF Housing Grant of up to S$30,000 (Proximity Housing Grant) available for eligible EC buyers

- Foreigners and companies cannot buy ECs during the initial launch period from developers

An Executive Condominium — universally abbreviated to EC in Singapore — is a hybrid housing type administered by the Housing & Development Board (HDB) but developed and sold by private property developers. ECs were introduced in 1995 to serve the “sandwich class” of Singaporeans who earn above the HDB BTO income ceiling of S$14,000/month but find private condominiums financially out of reach. In 2026, ECs remain one of Singapore’s most compelling property purchases for eligible buyers: they offer condominium-standard facilities (swimming pool, gym, function room, landscaped grounds, 24-hour security) at prices roughly 15–25% below comparable private condominiums, with the bonus of becoming fully private after a defined holding period. This guide covers every aspect of buying an EC in Singapore in 2026 — eligibility, pricing, the new 10-year MOP and 15-year privatisation rules, CPF usage, financing, and a worked financial example.

What Makes an EC Different from an HDB BTO and a Private Condo?

Understanding where an EC sits in Singapore’s housing ecosystem is the starting point for any prospective buyer. HDB Build-To-Order (BTO) flats are owned by the government, subject to significant resale restrictions, carry an income ceiling of S$14,000/month, and cannot be sold on the open market for five years from the date of key collection. At the other extreme, fully private condominiums have no income ceiling, no nationality restriction (subject to ABSD rates), and no minimum occupation period — but typically cost S$1.4M–S$3M+ for a new launch in 2026.

ECs sit between these two. During the initial restricted period, ECs operate under HDB rules — they must be sold by the developer at launch to eligible SC/PR applicants, buyers must meet the income ceiling, and a Minimum Occupation Period applies. Once privatised, an EC becomes indistinguishable from any other private condo in the eyes of the law. This trajectory — from subsidised hybrid to fully private asset — is what makes ECs uniquely attractive as a long-term investment vehicle, particularly for first-time buyers who can benefit from CPF grants while locking in capital appreciation over 10–15 years.

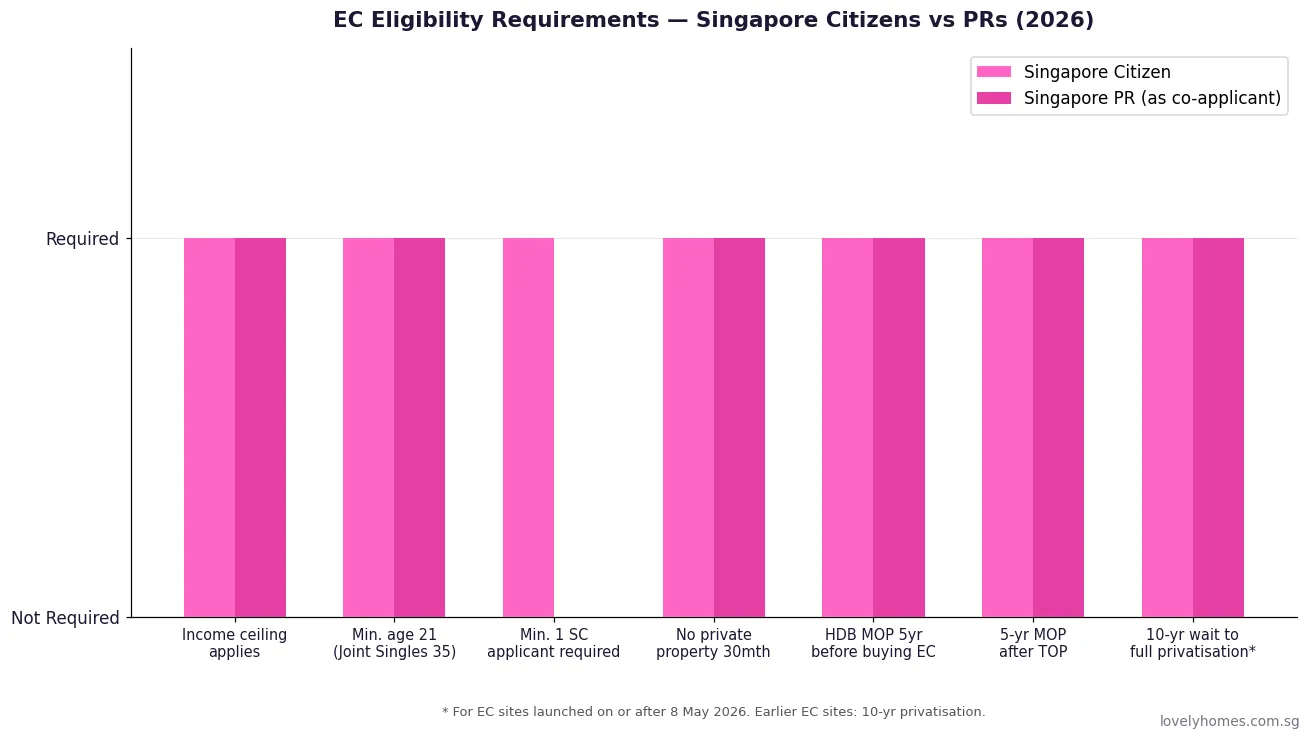

EC Eligibility — Who Can Buy?

EC eligibility is more restrictive than private condo eligibility and must be carefully assessed before any application. All of the following conditions must be met simultaneously.

Citizenship: At least one applicant in the application must be a Singapore Citizen. Co-applicants can be Singapore Citizens or Singapore Permanent Residents. Foreigners are categorically ineligible to purchase ECs during the initial launch period from the developer. Only after 10 years from the date the EC obtained its Temporary Occupation Permit (TOP) may foreigners purchase ECs on the open market.

Household income ceiling: The combined gross monthly household income of all applicants and any occupants listed in the application must not exceed S$16,000. This ceiling has not changed in Budget 2026. Gross income includes all sources — base salary, allowances, bonuses averaged over 12 months, self-employment income, rental income, and foreign income if the applicant is assessed for Singapore tax. Exceeding the ceiling by even S$1 at the time of application results in automatic disqualification, and HDB verifies income through IRAS tax assessments and CPF contribution records.

Age: All applicants must be at least 21 years old. Under the Joint Singles Scheme (JSS), two or more unmarried Singapore Citizens may jointly apply for an EC, but each must be at least 35 years old.

Private property cooling-off period: Applicants must not have disposed of any private residential property (locally or overseas) within 30 months before the EC application date. If you sold a private property on 1 January 2024, you cannot apply for an EC until 1 July 2026.

HDB ownership history: If you or any applicant has previously owned an HDB flat, the Minimum Occupation Period of that flat must be fully served before you may apply for an EC. Additionally, if you currently own or are listed as an occupant of an HDB flat, you must dispose of that HDB flat within six months of taking possession of the EC.

EC Pricing in 2026 — What to Expect

New EC launches in 2026 are priced in the S$1,300–S$2,200 per square foot (psf) range, reflecting rising land costs. Upcoming EC sites at Jalan Loyang Besar (Pasir Ris) and Tampines Street 95 are expected to launch at around S$1,700 psf when they come to market, which translates to absolute prices of approximately S$1.4M for a 3-bedroom unit and S$1.8–S$2.0M for a 4-bedroom unit.

Currently available ECs illustrate the pricing landscape. Novo Place — a 504-unit development by Hoi Hup Realty and Sunway Developments — was released at indicative prices starting from S$1.298M for a 2-bedroom unit up to S$1.779M for a 4-bedroom-plus-study. Aurelle of Tampines is another active launch in 2026, reflecting the continued concentration of EC supply in the north-east corridor near good MRT connectivity.

| EC Development | Location | Year of TOP (est.) | Price Range (new launch) | Units |

|---|---|---|---|---|

| Aurelle of Tampines | Tampines Ave 11 | ~2029 | S$1.35M–S$2.0M | 760 |

| Novo Place | Tengah Garden Walk | ~2029 | S$1.30M–S$1.78M | 504 |

| Lumina Grand | Bukit Batok West Ave 5 | ~2028 | S$1.31M–S$1.65M (est.) | 495 |

| Altura | Bukit Batok West Ave 8 | ~2028 | S$1.30M–S$1.65M (est.) | 360 |

| Jalan Loyang Besar (upcoming) | Pasir Ris | ~2030 | ~S$1.40M–S$2.0M (projected) | TBC |

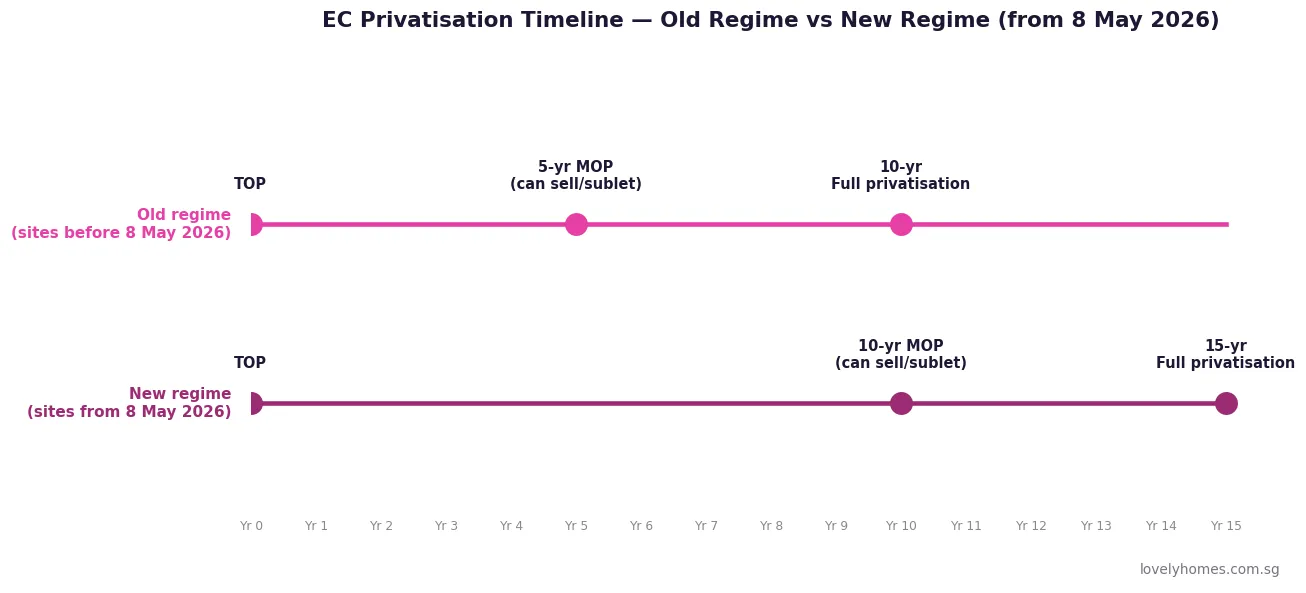

The New 10-Year MOP and 15-Year Privatisation Rules (From 8 May 2026)

On 8 May 2026, the Singapore Government announced a significant tightening of EC holding period rules for EC sites awarded on or after that date. Understanding the distinction between old-regime ECs (already launched) and new-regime ECs (future GLS site awards) is essential for any EC buyer in 2026.

Old regime (Aurelle of Tampines, Novo Place, Lumina Grand, Altura, and all ECs launched before 8 May 2026): The familiar 5-year MOP applies from TOP. After the MOP, the EC may be sold on the open market to Singapore Citizens or PRs. After 10 years from TOP, the EC is fully privatised and may be sold to foreigners and entities — subject to ABSD.

New regime (EC sites awarded from 8 May 2026 onwards): The MOP extends to 10 years from TOP. Full privatisation — when the unit may be transacted with foreigners and entities — does not occur until 15 years from TOP. This significantly extends the illiquidity period and reduces the short-to-medium-term capital gain that characterized earlier EC purchases. The Government’s stated rationale is to ensure ECs genuinely serve the long-term housing needs of eligible Singaporeans rather than shorter-cycle investment objectives.

The practical implication for buyers in 2026: the four currently launched ECs (Aurelle, Novo Place, Lumina Grand, Altura) are old-regime projects and retain the more liquid 5-year MOP and 10-year privatisation timeline. New EC sites awarded after 8 May 2026 will carry the extended restrictions. Buyers who prioritise resale flexibility should prioritise current launches over future GLS-derived ECs.

Financing an EC — CPF, Bank Loans and TDSR

ECs are financed through bank loans (HDB concessionary loans are not available for ECs). The bank will assess the application under the Total Debt Servicing Ratio (TDSR) framework administered by the Monetary Authority of Singapore (MAS), capping total monthly debt repayments at 55% of gross monthly income. The maximum loan-to-value (LTV) ratio for an EC bank loan is 75% of the purchase price or valuation (whichever is lower), so buyers must have at least 25% in cash and/or CPF.

CPF Ordinary Account (OA) savings may be used for the downpayment (subject to the Valuation Limit and Withdrawal Limit), monthly mortgage instalments, and stamp duties on the EC purchase. However, CPF usage for ECs is governed by the same accrued interest rules as HDB loans — when you sell the EC, you must return to your CPF account the principal withdrawn plus 2.5% per annum accrued interest. This is not a penalty but a refund to your own retirement account, and it reduces the net cash proceeds from any eventual sale.

Buyers who currently own an HDB flat and are eligible to purchase an EC simultaneously (e.g., within the six-month disposal window) must be careful about ABSD exposure: if they have not yet sold their HDB when they execute the EC Sales and Purchase Agreement, they will technically hold two residential properties and may attract ABSD at 20% (SC second property) on the EC purchase price. Planning the HDB sale to precede the EC SPA execution by at least one day is the standard approach.

Worked Example: Mr and Mrs Lim — Buying Aurelle of Tampines EC

Mr Lim (SC) and Mrs Lim (SC) are a married couple in their mid-30s. Mr Lim earns S$9,500/month and Mrs Lim earns S$5,800/month — combined S$15,300/month, comfortably below the S$16,000 income ceiling. They currently live in Mrs Lim’s parents’ HDB flat and have no prior private property ownership. They are applying for a 4-bedroom unit at Aurelle of Tampines at S$1,780,000.

Eligibility checks:

- Income: S$15,300/month — below S$16,000 ceiling ✓

- Citizenship: both SC ✓

- Age: both 34 and 36 — above 21 ✓

- Private property cooling-off: neither has owned private property ✓

- HDB ownership: neither owns an HDB flat in their own names ✓

Purchase costs:

- Purchase price: S$1,780,000

- Buyer’s Stamp Duty (BSD): S$1,780,000 × BSD schedule = S$4,600 (first S$180,000 × 1%) + S$27,600 (next S$360,000 × 2%) + S$36,000 (next S$360,000 × 3%) + S$39,200 (next S$880,000 × 4%) = S$56,600 (standard BSD calculation: (180,000×1%)+(360,000×2%)+(360,000×3%)+(880,000×4%) = 1,800+7,200+10,800+35,200 = S$55,000)

- Additional Buyer’s Stamp Duty (ABSD): S$0 — SC buying first residential property ✓

- Legal fees (EC S&P): approximately S$3,500

- Total acquisition cost: approximately S$1,783,500 + S$55,000 BSD + S$3,500 legal = S$1,841,500

Financing:

- Downpayment (25%): S$445,000 — funded from CPF OA + cash savings

- Bank loan (75%): S$1,335,000 at 3.2% fixed over 25 years = approx S$6,420/month

- TDSR check: S$6,420 ÷ S$15,300 = 42.0% — well within 55% TDSR ✓

- MSR note: MSR (Mortgage Servicing Ratio) of 30% applies only to HDB loans, not to EC bank loans

Grant eligibility: The Lims do not qualify for the CPF Housing Grant (available only for HDB BTO buyers) or the Enhanced Housing Grant (EHG). However, if one set of parents lives within 4km of Aurelle of Tampines, the Proximity Housing Grant (PHG) of S$10,000 (living near parents) or S$20,000 (living with parents) may apply — reducing the effective purchase price.

Projected holding value: Assuming Aurelle of Tampines follows a typical EC appreciation trajectory, comparable ECs that TOPed around 2019–2020 and privatised around 2029–2030 have demonstrated 35–50% resale premium over launch price during the privatisation window. This is speculative — past EC performance does not guarantee future returns — but the long-term track record of ECs converting to fully private assets in strong MRT-connected locations has been broadly positive.

Why ECs Matter: The Sandwich Class Opportunity

ECs were specifically designed by the Ministry of National Development (MND) to address Singapore’s “sandwich class” dilemma — households too affluent for subsidised HDB housing but not wealthy enough to comfortably absorb private condo prices without significant financial strain. In 2026, this remains the precise demographic challenge: private condo prices have risen substantially since 2020, the income ceiling for HDB BTO remains S$14,000/month, and the S$14,001–S$16,000 income band represents hundreds of thousands of eligible Singaporean households.

For buyers who qualify, an EC in a well-located development is arguably the most efficient use of S$1.3–S$2.0M in Singapore’s property market — providing private facilities and capital appreciation without the full ABSD burden on a second purchase or the income-test barriers of HDB. The caveat is the holding period: buyers must be prepared for the unit to remain illiquid (under old-regime rules) for 5 years and (under new-regime rules) for 10 years before they can sell. EC buying is fundamentally a medium-to-long-term commitment, not a short-cycle trade.

What Might Come Next — EC Policy Outlook

The 8 May 2026 announcement extending the MOP to 10 years and privatisation to 15 years for new EC sites signals that the Government intends to reinforce EC’s owner-occupation objective and reduce speculative pressure. It is plausible that income ceilings may be reviewed upward if private condo prices continue to rise faster than household income growth — a precedent exists from the 2021 rise in the HDB BTO income ceiling from S$12,000 to S$14,000 and the parallel EC ceiling rise from S$14,000 to S$16,000. Future EC GLS allocations will likely continue to be concentrated in MRT-connected OCR towns such as Tengah, Tampines, Pasir Ris, and the north corridor, aligning with long-term infrastructure investment in these areas.

Summary: EC vs HDB BTO vs Private Condo

| Feature | HDB BTO | Executive Condo (EC) | Private Condo |

|---|---|---|---|

| Income ceiling | S$14,000/mth | S$16,000/mth | None |

| Eligibility | SC/PR (various schemes) | Min. 1 SC; SC/PR only | Open (with ABSD for foreigners) |

| MOP (new launch) | 5 years | 5 yrs (old) / 10 yrs (new*) | None |

| Full privatisation | N/A | 10 yrs (old) / 15 yrs (new*) | Already private |

| CPF Housing Grant | Up to S$120,000 (EHG) | PHG up to S$30,000 | None |

| HDB loan available? | Yes (2.6%) | No — bank only | No — bank only |

| Typical 2026 price | S$300K–S$700K (resale) | S$1.3M–S$2.2M | S$1.4M–S$3.5M+ |

| Foreign buyer eligible? | No | After 10 yrs TOP (old) / 15 yrs (new*) | Yes (60% ABSD for foreigners) |

* For EC GLS sites awarded from 8 May 2026 onwards.

Frequently Asked Questions

Can a Singapore Permanent Resident buy a new EC?

A PR cannot buy a new EC as the sole or principal applicant. At least one Singapore Citizen must be part of the application. A PR may be a co-applicant alongside a SC spouse under the Public Scheme, or an EC may be purchased under a family nucleus that includes at least one SC. After the EC is fully privatised (10 years under old-regime rules, 15 years under new-regime rules), PRs and foreigners may purchase ECs on the open market. On the open market, a PR purchasing a fully privatised EC is subject to PR ABSD rates (5% for first residential property, 30% for second+).

What is the difference between the 5-year MOP and the 10-year MOP?

The Minimum Occupation Period (MOP) is the period during which the EC cannot be sold on the open market. Under the old regime (ECs launched before 8 May 2026), the MOP is 5 years from the date the EC obtained its TOP. After 5 years, the EC may be sold to Singapore Citizens or PRs on the open market. After 10 years from TOP, it becomes fully private (saleable to foreigners). Under the new regime (EC GLS sites awarded from 8 May 2026), the MOP extends to 10 years from TOP, and full privatisation occurs only at 15 years. During the MOP period, the EC cannot be sublet in its entirety (individual rooms may be sublet with HDB approval), and the owner must occupy the unit as their primary residence.

Can I use my CPF to pay for an EC?

Yes. CPF Ordinary Account (OA) savings may be used for the downpayment (subject to the Valuation Limit — VL — which is the lower of purchase price or valuation), monthly mortgage instalments, legal fees, and stamp duties. When CPF OA is used, the CPF Act requires you to refund the principal amount withdrawn plus 2.5% per annum accrued interest when you sell the EC. This refund goes back into your CPF OA (and, where applicable, Special or Retirement Account up to the prevailing Full Retirement Sum). The accrued interest is not a penalty — it is your own retirement savings with its minimum guaranteed return. Buyers should model this refund when calculating net sale proceeds from a future EC sale.

Does ABSD apply when buying an EC?

Yes, the same ABSD schedule that applies to private condominiums applies to ECs. Singapore Citizens buying their first residential property pay 0% ABSD — this is the most favourable scenario and why many EC buyers time their HDB disposal to precede the EC purchase. Singapore Citizens buying a second residential property pay 20% ABSD on the EC’s purchase price. If a buyer still holds their HDB flat when they execute the EC Sales and Purchase Agreement, the HDB flat counts as a first property, making the EC the second — triggering 20% ABSD. HDB provides a conditional ABSD remission for married SC couples who sell their HDB flat within six months of purchasing the private property (including EC). Always consult an IRAS-registered solicitor to verify your ABSD status before signing.

What happens to my HDB flat if I buy an EC?

If you currently own an HDB flat and wish to purchase an EC, you must dispose of your HDB flat within six months of taking possession of the EC (i.e., within six months of key collection). Selling before key collection is the cleanest approach to avoid ABSD exposure. If you sell your HDB after executing the EC Sales and Purchase Agreement, you may be subject to ABSD at 20% on the EC, but may apply for ABSD remission from IRAS provided the HDB is disposed of within six months of the EC SPA date. The remission is available to married SC couples and requires a formal application — it is not automatic. Failure to meet the six-month timeline results in forfeiture of any ABSD remission.

Are there any resale restrictions during the MOP?

During the Minimum Occupation Period, the EC may not be sold, transferred, or sublet as a whole unit without HDB approval. Individual bedrooms may be rented to lodgers with HDB approval — the same rules that apply to HDB flat owners. The owner must continue to occupy the unit as their principal residence throughout the MOP. Breaching MOP restrictions is treated as an offence under the Housing and Development Act and the Planning Act, and may result in compulsory acquisition of the unit by HDB at the original purchase price — a severe financial consequence. After the MOP expires, the EC may be transacted freely on the open market.

Are ECs a good investment in 2026?

ECs have historically been strong investments for eligible buyers due to the price discount at launch relative to comparable private condos, CPF grant support for eligible applicants, and the capital appreciation that typically accompanies privatisation. Past ECs that TOPed around 2017–2020 and privatised around 2027–2030 are, in many cases, transacting at premiums of 40–60% over their original launch prices in 2014–2018. However, the extension of the holding period to 10 years (MOP) and 15 years (privatisation) for new-regime ECs significantly changes the investment calculus — it reduces the short-cycle gain that previous buyers enjoyed and increases the commitment required. ECs remain a sound medium-to-long-term investment for buyers who genuinely intend to live in the property, but are less suitable as shorter-horizon plays. As with any property purchase, future value is not guaranteed — economic conditions, interest rates, supply, and government policy all influence outcomes.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore HDB Upgrading Guide 2026: Costs, ABSD, CPF and Step-by-Step Process

- Singapore Home Loan Complete Guide 2026: HDB Loans, Bank Loans, TDSR, MSR and Best Rates Explained

- Singapore Property Decoupling Guide 2026: Save ABSD, Costs, Risks and Step-by-Step Process

- Singapore Property Investment Guide 2026: How to Buy, Rent and Build Wealth Through Property

- Singapore Property Conveyancing Guide 2026: OTP, S&P Agreement, Legal Fees and Timelines Explained

Disclaimer: This article is intended as general information only and does not constitute legal or financial advice. EC eligibility, income ceilings, ABSD rates, MOP rules, and privatisation timelines are set by government policy and may be revised without notice. All figures are based on information available as at June 2026. Always verify current conditions with the Housing & Development Board (HDB), the Inland Revenue Authority of Singapore (IRAS), and a qualified property solicitor before making any purchase decision. Past capital appreciation of ECs does not guarantee future returns. LovelyHomes does not act as a property agent and does not endorse any developer or property service provider.