Singapore Luxury Homes and Safe-Haven Demand: CCR Surges +2.0% in Q2 2026

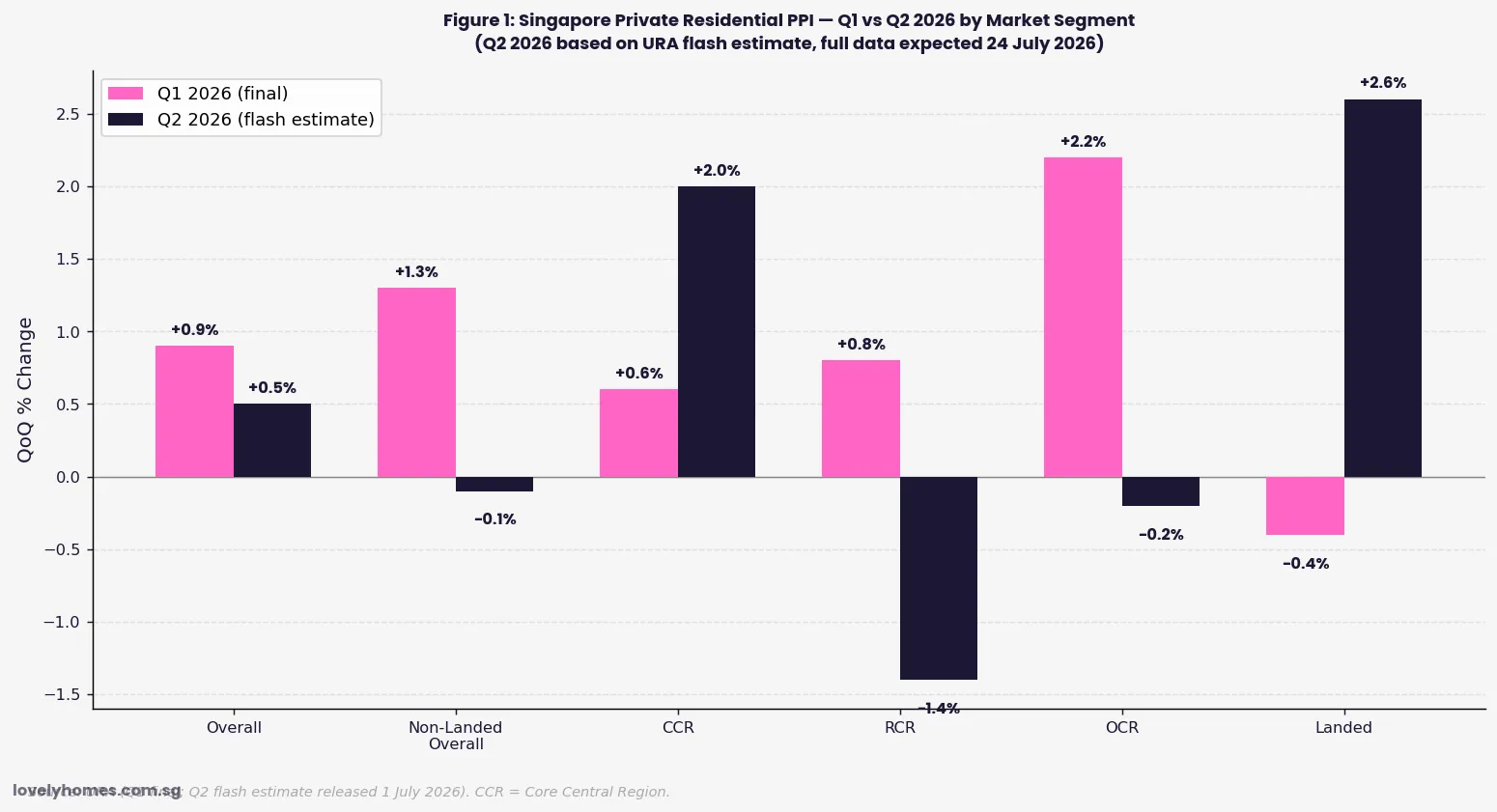

- Singapore’s Core Central Region (CCR) posted a +2.0% price increase in Q2 2026 — the strongest of any market segment and a sharp reversal from Q1’s tepid +0.6%.

- Industry observers and URA data point to a safe-haven demand thesis: high-net-worth individuals from Asia and globally are channelling wealth into Singapore amid geopolitical uncertainty in 2026.

- Good Class Bungalow (GCB) deals in H1 2026 are reported to average S$2,121 per square foot — near all-time highs despite lower transaction volumes.

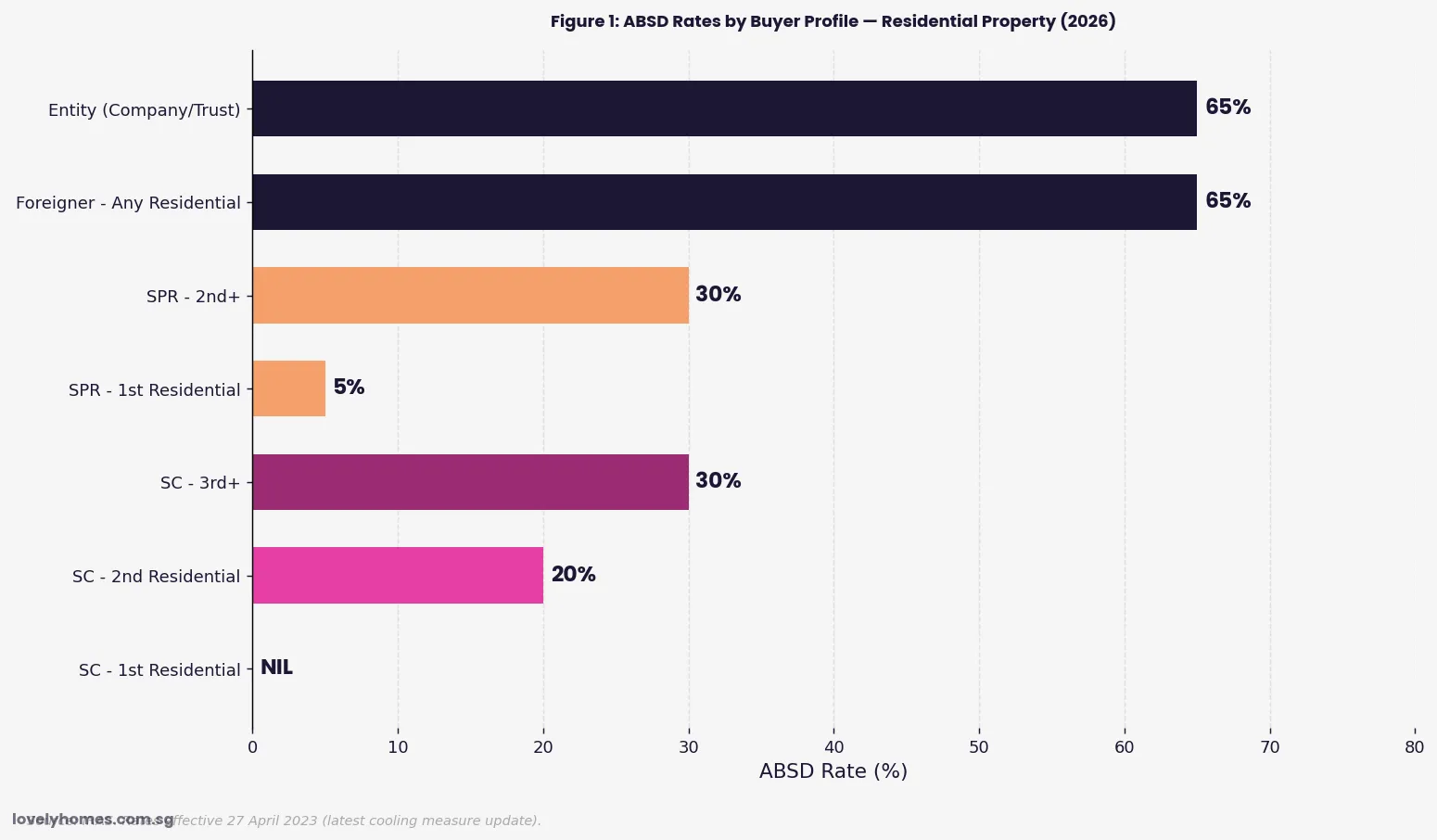

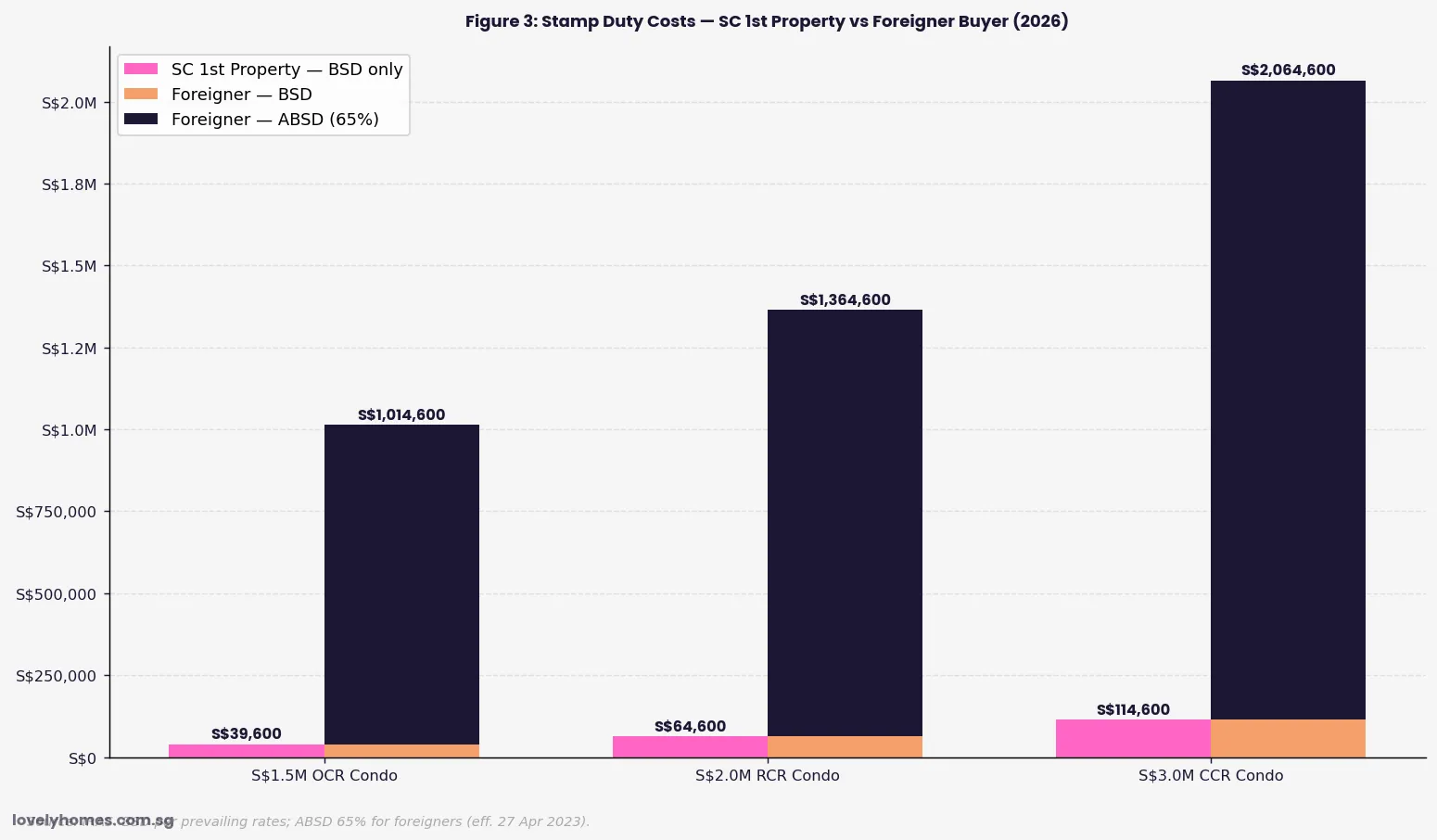

- Foreigner buying share of private residential transactions remains below 2% due to the 65% ABSD, but dollar volumes in the CCR continue to outpace other regions.

- The luxury market is bifurcating: sub-S$3M OCR and RCR condos are softening (OCR -0.2%, RCR -1.4% in Q2 2026), while trophy assets above S$5M are tightening.

- Singapore’s combination of rule of law, no capital gains tax, SGD strength, and geopolitical neutrality underpins its premium positioning among global wealth management centres.

- Full Q2 2026 transaction data is expected from URA on 24 July 2026 — the flash estimate published 1 July 2026 covers pricing only, not full volumes.

CCR Surges 2.0% in Q2 2026 as Luxury Demand Returns

Singapore’s Core Central Region (CCR) property market recorded a 2.0% price increase in Q2 2026, according to the Urban Redevelopment Authority’s flash estimate released on 1 July 2026. This makes the CCR the best-performing segment of the entire private residential market for the quarter — outpacing the overall market gain of 0.5% and standing in sharp contrast to the Rest of Central Region (RCR, -1.4%) and Outside Central Region (OCR, -0.2%), which both posted price declines.

The CCR’s outperformance is particularly notable given the backdrop: the wider Singapore private residential market has been moderating since early 2025, with the URA Private Property Price Index (PPI) recording gains of just 0.9% in Q1 2026 and 0.5% in Q2 2026 — well below the 8.4% full-year gain of 2023. The surge in CCR prices reflects a specific dynamic: demand from wealth-preserving investors, both domestic and international, for premium Singapore residential assets.

The Safe-Haven Thesis: Why Singapore Is Attracting Global Wealth

Industry observers note that Singapore’s luxury property market has increasingly attracted demand driven not by speculative gain but by wealth preservation. Several structural factors reinforce Singapore’s position as a premium repository of global capital in 2026.

Geopolitical diversification: Ongoing conflicts in Europe, rising trade tensions between the United States and China, and political uncertainty in multiple Southeast Asian nations have prompted high-net-worth individuals to diversify their real-asset holdings into jurisdictions perceived as politically stable. Singapore — with its neutral foreign policy, independent judiciary, and transparent legal framework — is among a short list of global cities offering this combination.

No capital gains tax: Singapore does not tax capital gains on property disposal (subject to the IRAS’s anti-speculation rules around short-term trading). For investors holding a property for more than three years, any appreciation is fully exempt from tax. This contrasts sharply with major competing markets: the United Kingdom taxes property gains at 18–28%, Australia at the marginal income rate, and Hong Kong at stamp duty and property tax regimes that have been progressively tightened.

Singapore Dollar resilience: The Monetary Authority of Singapore (MAS) manages the Singapore Dollar within a policy band that has delivered steady appreciation against a trade-weighted basket since the 1980s. For USD or EUR-denominated investors, Singapore property effectively provides implicit currency protection alongside the real-asset yield.

Rule of law and property rights: Singapore property title is freehold or 99-year leasehold under a clear and well-enforced framework. Title searches are transparent, conveyancing is regulated, and disputes are adjudicated by courts with a strong track record of enforcing property rights. There is no risk of compulsory acquisition without fair compensation under the Land Acquisition Act.

The Luxury Segment in Numbers: What the Data Shows

The Q2 2026 URA flash estimate provides pricing data but not full transaction volumes — those will be released with the full Q2 statistics on approximately 24 July 2026. However, the H1 2026 market narrative is already forming from the available data points.

| Market Segment | Q1 2026 PPI Change | Q2 2026 PPI Change (Flash) | H1 2026 Direction |

|---|---|---|---|

| Overall Private Residential | +0.9% | +0.5% | Moderating |

| Non-Landed Overall | +1.3% | -0.1% | Softening |

| CCR (Core Central Region) | +0.6% | +2.0% | Accelerating |

| RCR (Rest of Central Region) | +0.8% | -1.4% | Correcting |

| OCR (Outside Central Region) | +2.2% | -0.2% | Cooling |

| Landed Residential | -0.4% | +2.6% | Rebounding |

The data shows a clear bifurcation: mid-market mass-market condominiums (OCR and RCR) are softening or correcting, while the premium CCR segment and landed residential — the two categories most associated with high-net-worth buying — are strengthening. This is consistent with the safe-haven demand thesis: wealth-preserving buyers are focused on premium Singapore assets, not the mass-market segment where supply from new GLS sites is more acute.

Landed residential and GCBs: Industry data cited in market commentary indicates that Good Class Bungalow (GCB) transactions in H1 2026 averaged approximately S$2,121 per square foot — near historical highs. While GCB volume has been subdued (fewer than 20–30 transactions per half typically), the average transacted PSF points to the depth of demand at the very top of the market. GCBs are the only residential asset class in Singapore where the absolute supply is fixed by planning policy: there are approximately 2,800 GCB plots gazetted in 39 designated GCB Areas, and no new GCB land has been released since the 1990s.

ABSD as a Structural Filter: Who Is Still Buying at the Top End?

The 65% ABSD for foreigners did not eliminate luxury CCR buying — it filtered it. At the S$5 million price point, a foreign buyer pays S$3,250,000 in ABSD alone. The buyers who can absorb this cost are a qualitatively different group from the pre-2023 foreign luxury buyer cohort: predominantly ultra-high-net-worth (UHNW) individuals or family offices for whom the ABSD represents a tolerable cost of admission to a prized asset class rather than a prohibitive barrier.

The primary luxury buyer base in 2026 remains Singapore Citizens and PRs, who face no ABSD (SC 1st property) or 5% ABSD (SPR 1st property) respectively. Singapore-based UHNW families who have grown their wealth over the past two decades through private equity, technology, or trade finance are the backbone of CCR demand. A secondary and growing segment is foreign family office principals who have established Single Family Office (SFO) structures in Singapore under the Monetary Authority of Singapore’s SFO incentive framework — these are resident in Singapore and may qualify for SC or PR status over time.

What This Means for Property Buyers in Singapore

The CCR’s Q2 2026 outperformance is both a market signal and a policy-test. It signals that the ultra-premium segment is resilient to macroeconomic headwinds and retains structural demand even at historically high price levels. The question for the government is whether this resilience in the top tier justifies ongoing caution about relaxing the foreigner ABSD — or whether the bifurcation (luxury up, mass-market softening) suggests the cooling measures are having their intended effect of segmenting demand without depressing the overall market.

For Singapore Citizens and PRs looking at the CCR, the data suggests that the window of Q4 2025 / Q1 2026 softness (CCR posted only +0.6% in Q1) may have already passed. If the CCR’s Q2 2026 momentum carries into Q3, the entry window could narrow further. Buyers targeting premium properties — Orchard Road, Sentosa Cove, River Valley, Buona Vista — may find pricing firming through the second half of 2026.

What Might Come Next

The full Q2 2026 private residential statistics from URA (expected 24 July 2026) will reveal whether the CCR volume recovery matched the price recovery. If CCR transaction volumes in Q2 2026 show a meaningful uptick from the subdued Q1 levels, it would confirm the demand recovery is broad-based rather than driven by a small number of high-value transactions. Conversely, a further Q3 2026 reading above +1.5% CCR PPI growth could bring the CCR back onto the radar of the government’s cooling measure review — though any specific policy response ahead of the next scheduled review is speculative.

The full Q2 2026 HDB resale statistics (expected from HDB around 23 July 2026) will provide a complementary read on the mass-market segment — and whether the flash estimate’s -0.3% RPI decline was accurately captured. Taken together, the two data releases in late July 2026 will give the market its clearest picture yet of whether Singapore’s property bifurcation — luxury strengthening, mass-market moderating — is the dominant theme for H2 2026.

Frequently Asked Questions

Why is the CCR doing better than the RCR and OCR in 2026?

The Core Central Region comprises Districts 1–4 and 9–11 — the prime downtown and Orchard Road belt. It attracts a qualitatively different buyer profile: high-income Singapore residents, wealth-preserving investors, and family office principals. This cohort is less sensitive to interest rate cycles and supply pipeline impacts because they are buying premium or trophy assets rather than investment units. In contrast, the RCR and OCR have seen more mid-market supply from new Government Land Sales (GLS) sites, and their buyer base — including upgraders and first-time condo buyers — is more sensitive to mortgage rates and HDB resale price trends.

Can foreigners still buy Singapore luxury property given the 65% ABSD?

Yes, but the economics have changed dramatically since the April 2023 cooling measures. On a S$5 million CCR condo, a foreign buyer faces S$3,250,000 in ABSD alone. This effectively restricts the foreign luxury buyer market to ultra-high-net-worth individuals or family office structures where the ABSD is an acceptable cost of entry. MAS data suggests foreign buyer volumes remain below 2% of all private residential transactions — but their average deal size is materially higher than the market average, meaning they contribute disproportionately to CCR dollar volume.

What is a Good Class Bungalow (GCB) and why are prices so high?

Good Class Bungalows are the most exclusive form of landed residential property in Singapore, located within 39 designated GCB Areas gazetted under the URA Master Plan. GCBs must occupy a minimum land area of 1,400 square metres (about 15,000 sqft) and are subject to strict development controls. The supply is fixed at approximately 2,800 plots — no new GCB land has been created since the 1990s. Combined with strong demand from Singapore’s wealthiest families and a long-standing restriction on foreign ownership (SLA approval required), GCBs represent the most inelastic supply in the Singapore property market. Average transacted PSF of approximately S$2,121 in H1 2026 reflects this structural scarcity premium.

When will the full Q2 2026 property transaction data be released?

The Urban Redevelopment Authority typically releases full quarterly private residential statistics approximately 3–4 weeks after the quarter ends. The Q2 2026 flash estimate (covering the PPI only) was released on 1 July 2026. The full data — including transaction volumes, unit counts, new sales, sub-sales, and resale transactions by region and property type — is expected around 24 July 2026. LovelyHomes will cover the full release when it is published. For HDB resale statistics, the Q2 2026 full data (including median prices by flat type and town) is expected around 23 July 2026.

Is Singapore’s luxury property market in a bubble?

This is a contested question among market analysts. Arguments against a bubble: Singapore property prices are underpinned by genuine end-use demand, a restricted land supply, and government cooling measures that actively suppress speculative demand; the ABSD itself is the most powerful anti-bubble tool in the market. Arguments for caution: CCR prices are near historical highs on a PSF basis; low transaction volumes mean that a small number of trophy deals can move the index; and if global macroeconomic conditions worsen materially — reducing the “safe-haven” narrative — demand could soften quickly. The MAS monitors private residential price trends closely through its Financial Stability Review process, and will act if it assesses that price growth is becoming detached from fundamentals. As at July 2026, the government has not signalled any concern about a bubble in the CCR.