Singapore HDB Resale Market Guide 2026: Price Trends, What Drives Values and How to Read HDB Data

The HDB resale market in Singapore is one of the most transparent and data-rich property markets in the world. HDB publishes quarterly resale price indices, transacted price data by flat type and town, and volume statistics — yet most buyers and sellers never go beyond checking the headline figure. This guide teaches you how to read the data properly, what drives HDB resale prices in different estates, and what the Q1 2026 numbers actually mean for your buying or selling strategy.

Quick Answer — HDB Resale Market at a Glance (Q1 2026)

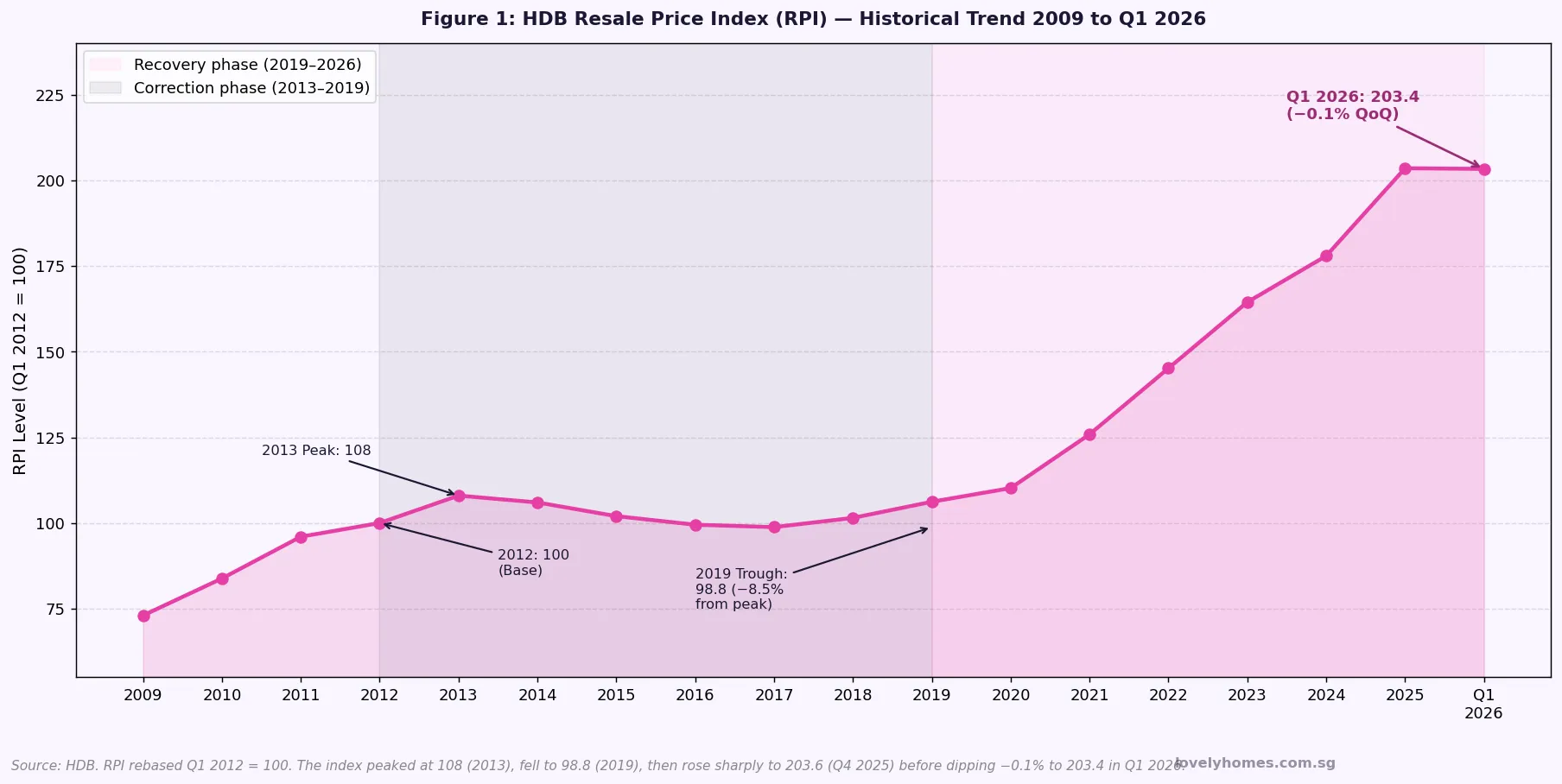

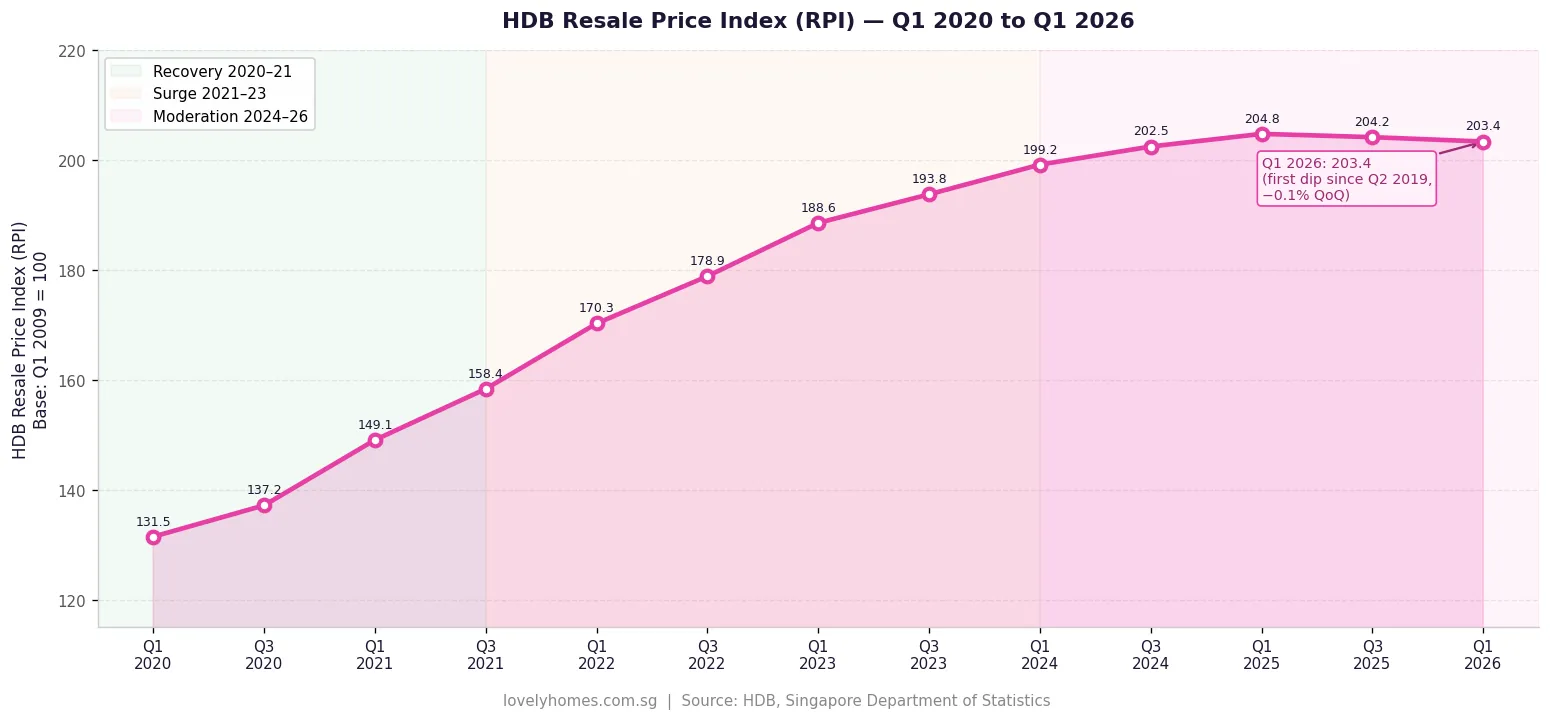

- The HDB Resale Price Index (RPI) stood at 203.4 in Q1 2026, a −0.1% quarter-on-quarter dip — the first decline since Q2 2019 and a sign of market moderation after six years of growth.

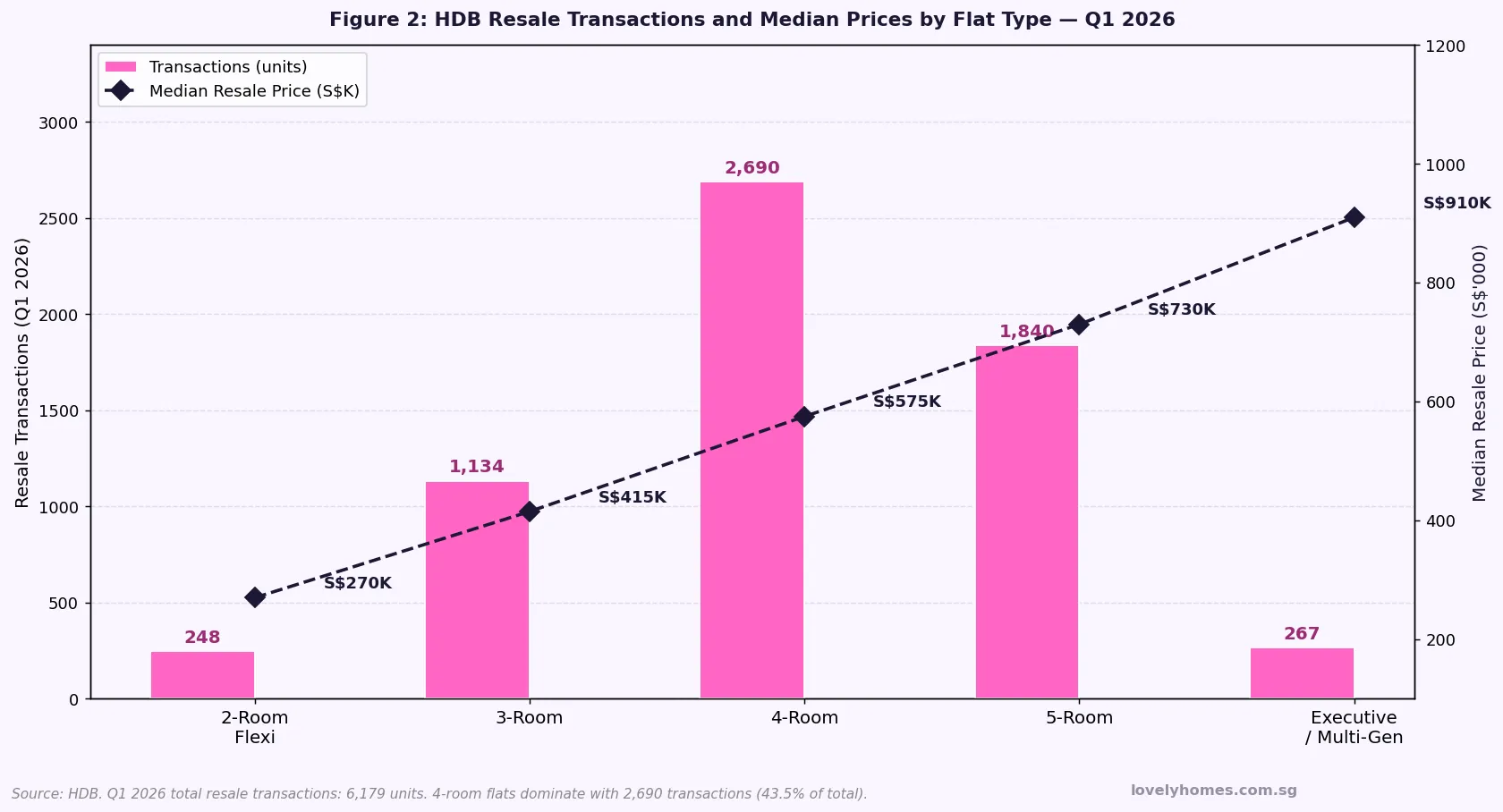

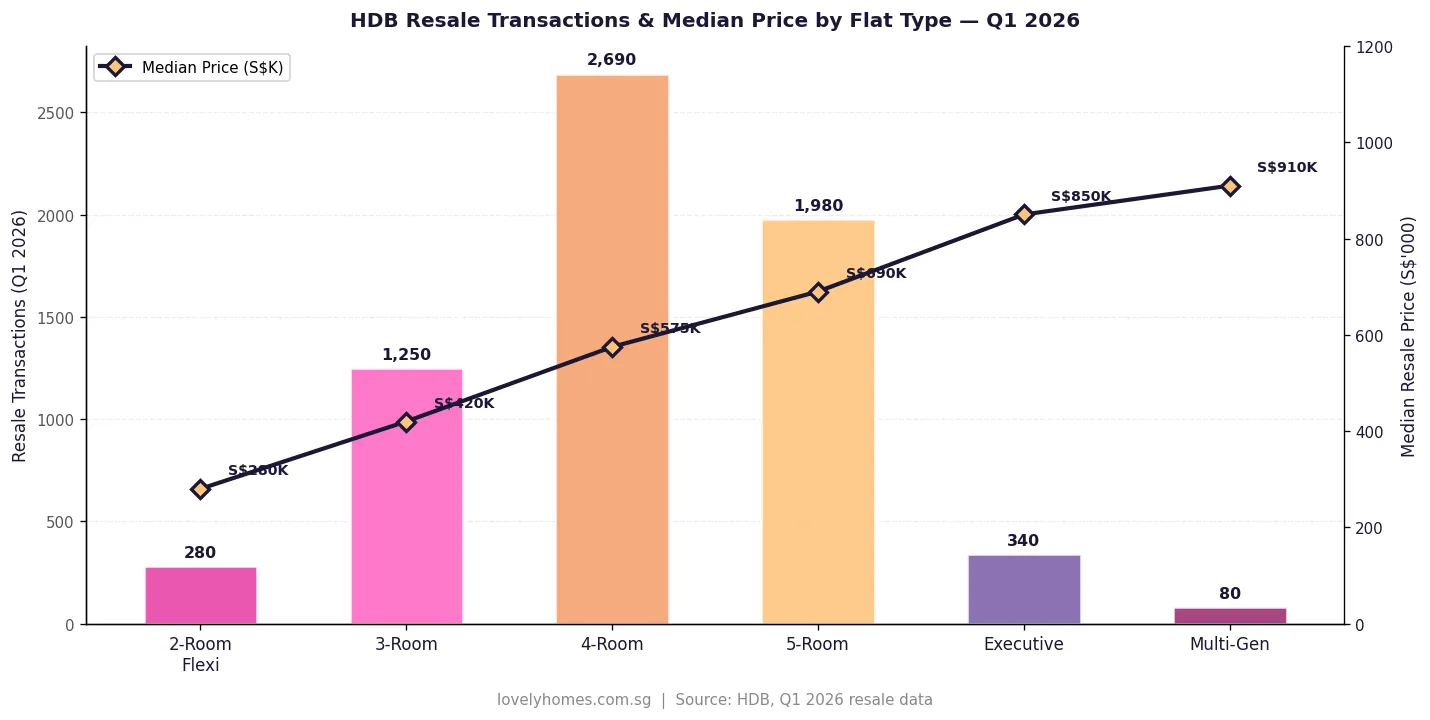

- Total HDB resale transactions in Q1 2026 were approximately 6,620 flats, with 4-room flats the most transacted at 2,690 units.

- Median prices ranged from S$280,000 for 2-room Flexi flats to S$910,000 for multi-generation flats.

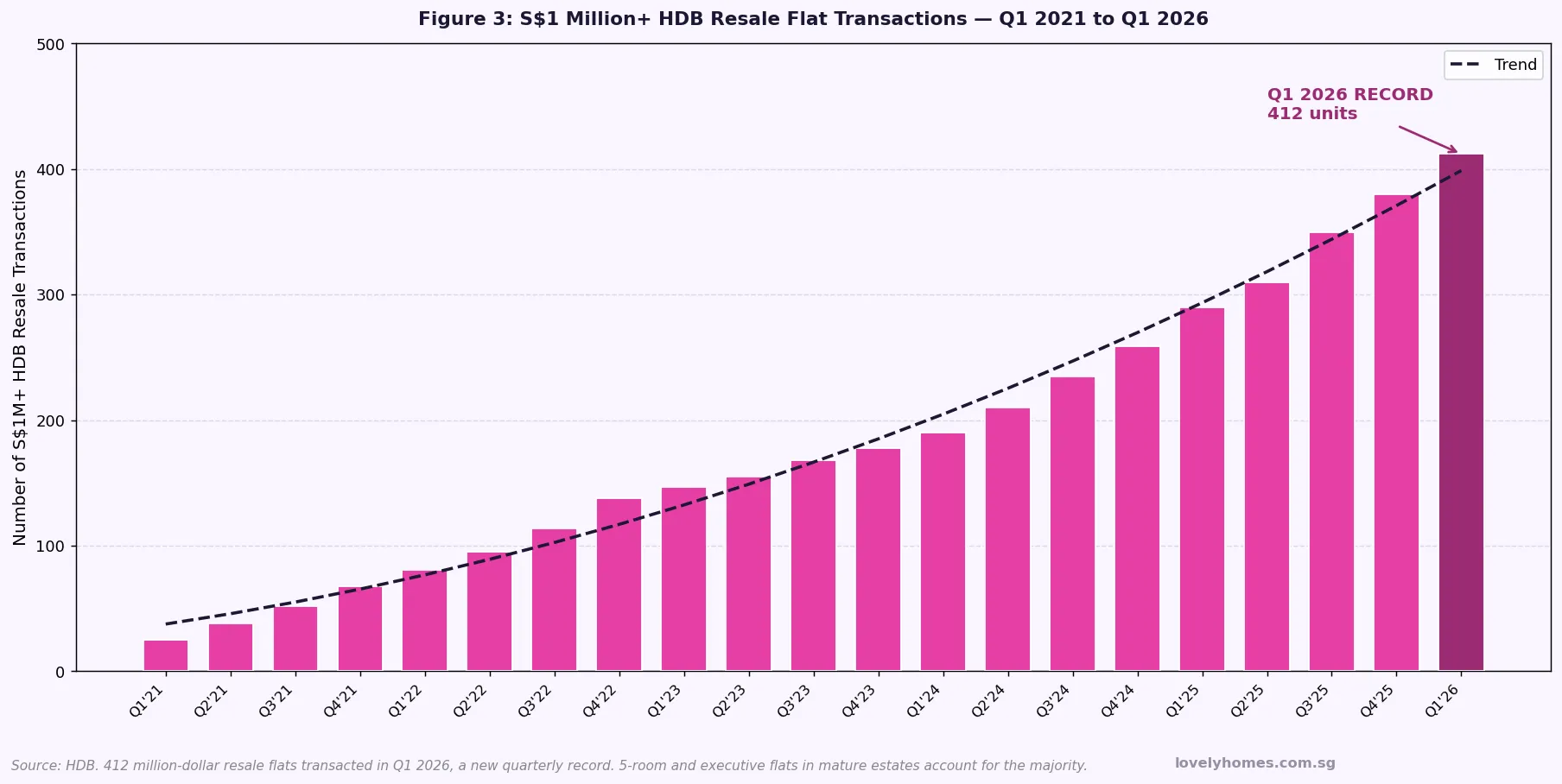

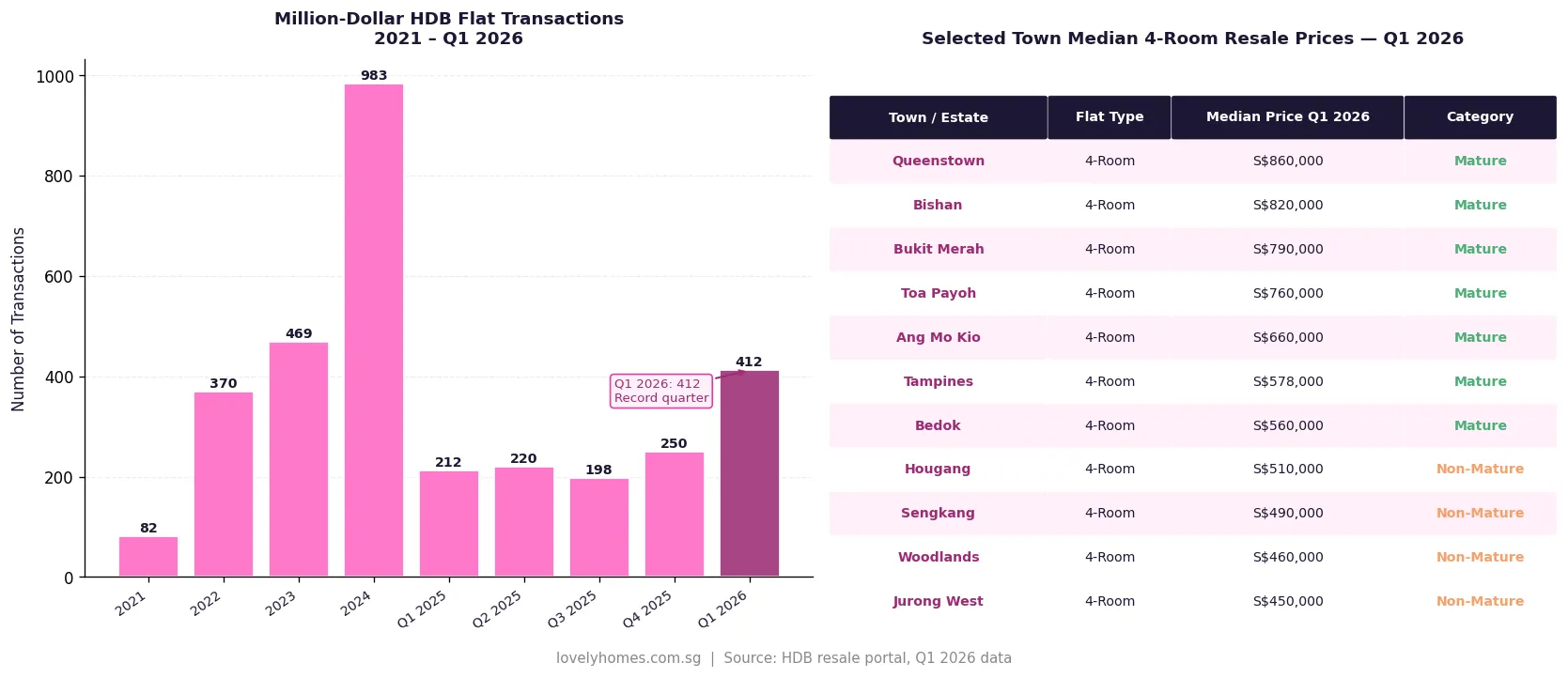

- 412 HDB flats transacted at S$1 million or above in Q1 2026, a new quarterly record.

- Mature estates (Queenstown, Bishan, Bukit Merah, Toa Payoh) continued to command median 4-room prices of S$760,000–S$860,000 — substantially above non-mature estates at S$450,000–S$510,000.

- The 15-month wait-out period for private property sellers buying HDB resale (introduced April 2023) continues to suppress some upgrader demand in the mid-range segment.

- URA Q2 2026 flash estimates for private property are expected in early July 2026; comparable HDB resale data will follow approximately two weeks later.

What Is the HDB Resale Price Index (RPI) and How Is It Compiled?

The HDB Resale Price Index is a quarterly statistic published by the Housing & Development Board that measures the change in resale prices of HDB flats over time. The base period is Q1 2009 = 100. An RPI of 203.4 in Q1 2026 means that the average price of an HDB resale flat is approximately 103.4% higher than it was in Q1 2009 — or, expressed differently, prices have more than doubled over 17 years.

The RPI is a mix-adjusted index. Rather than simply averaging transaction prices — which would be distorted by changes in the mix of flat types transacted each quarter — HDB uses a hedonic regression methodology that controls for flat type, storey range, floor area, estate, and remaining lease. This makes the RPI a more reliable indicator of underlying price change than raw median price movements.

The RPI is distinct from the median transacted price, which is the midpoint of all resale prices in a given period and is influenced by the mix of flats transacted. A quarter with unusually high sales of large 5-room flats in mature estates will show a higher median price even if underlying prices have not changed. The RPI strips out this compositional effect. For understanding whether prices are rising or falling, the RPI is the right metric; for understanding how much to pay for a specific flat type in a specific estate, median transacted prices and psf figures are more useful.

Reading HDB Resale Volume: What Transaction Counts Tell You

Volume data — the number of resale transactions in a given period — is a leading indicator of market sentiment. Volumes typically rise when sentiment is bullish (buyers are willing to transact), and fall when buyers are cautious or when supply alternatives (BTO launches, new private launches) absorb demand. HDB publishes resale volume data monthly via the HDB Resale Flat Prices dataset on data.gov.sg, updated within approximately two weeks of the end of each month.

In Q1 2026, total HDB resale volumes were approximately 6,620 transactions. The 4-room flat segment dominated at 2,690 transactions, followed by 5-room at 1,980. 3-room flats at 1,250 and executive/multi-gen flats at 420 combined make up the remainder. The dominance of 4-room flats reflects both the breadth of stock — 4-room flats are the most common type in the HDB inventory — and the preference of first-timer upgrader families for this size.

What Drives HDB Resale Prices in Different Estates?

The single largest driver of HDB resale prices is estate classification — specifically, whether the flat is in a mature or non-mature estate. HDB classifies 24 of its 26 towns as either mature or non-mature; the two newest, Tengah and Bidadari (Woodleigh), sit in between. Mature estates include Queenstown, Toa Payoh, Bishan, Bukit Merah, Ang Mo Kio, Clementi, Tampines, Marine Parade, Kallang/Whampoa, Geylang, Bedok, Serangoon, Hougang (partial), and Pasir Ris. Non-mature estates include Woodlands, Jurong West, Bukit Batok, Bukit Panjang, Choa Chu Kang, Sembawang, Sengkang, Punggol, and Yishun.

Within the mature-non-mature distinction, five further factors determine the price premium or discount a specific block commands:

MRT and transport connectivity is the most consistent price driver in Singapore research. Flats within a 5-minute walk of an MRT station typically command a 5–15% premium over comparable flats in the same estate further from the station, depending on the line, the interchange status, and the destination accessibility. The Thomson-East Coast Line has boosted prices in previously underserved areas such as Woodlands North and Caldecott.

Remaining lease has become increasingly important since the introduction of the CPF remaining-lease framework in 2019. Flats with fewer than 60 years of lease remaining are significantly harder to finance with CPF, and many banks apply stricter LTV limits. In practice, this suppresses demand and prices for older flats in mature estates, while newer BTO cohorts completing their MOP in the same estate attract a premium.

School catchment drives demand in proximity to popular primary schools with competitive phases 2A and 2B registration. Flats within 1 kilometre of consistently over-subscribed primary schools — such as Raffles Girls’ Primary, Nan Hua Primary, and Catholic High Primary — command a measurable premium, particularly among families with primary-school-aged children making buying decisions in Q4 and Q1.

Block storey and flat orientation account for a further 3–8% variance within the same block. High-floor corner units with unobstructed city or greenery views can command premiums substantially above median, while low-floor units facing a car park or multi-storey car park trade at a discount.

Recent upgrader activity and MOP waves create localised price effects. When a large BTO project completes its 5-year MOP in a non-mature estate, the sudden availability of relatively new flats for resale can temporarily suppress prices for that flat type in that town as supply increases. Conversely, in a mature estate where no new BTO completions are due, scarcity sustains prices.

Town-by-Town Analysis: Mature vs Non-Mature Estate Pricing

The table below summarises median 4-room resale prices for selected towns in Q1 2026, sourced from HDB’s resale portal data. These figures represent the midpoint of all registered resale transactions for that flat type in that town in the quarter and are indicative only — individual block, floor, and remaining lease will cause material variation within any estate.

| Town / Estate | Classification | Median 4-Room Price (Q1 2026) | Approx. Median PSF |

|---|---|---|---|

| Queenstown | Mature | S$860,000 | ~S$930 |

| Bishan | Mature | S$820,000 | ~S$890 |

| Bukit Merah | Mature | S$790,000 | ~S$860 |

| Toa Payoh | Mature | S$760,000 | ~S$820 |

| Ang Mo Kio | Mature | S$660,000 | ~S$715 |

| Tampines | Mature | S$578,000 | ~S$625 |

| Bedok | Mature | S$560,000 | ~S$605 |

| Hougang | Non-Mature | S$510,000 | ~S$555 |

| Sengkang | Non-Mature | S$490,000 | ~S$530 |

| Woodlands | Non-Mature | S$460,000 | ~S$500 |

| Jurong West | Non-Mature | S$450,000 | ~S$487 |

The Million-Dollar HDB Flat Phenomenon: What Is Driving It?

In Q1 2026, 412 HDB resale flats transacted at S$1 million or above — a new record for a single quarter. This compares with 82 transactions in the whole of 2021, 370 in 2022, 469 in 2023, and 983 in 2024. The trajectory is clear: what was once a curiosity has become a structural feature of Singapore’s resale market.

The drivers of million-dollar HDB transactions are well-documented by HDB and academic researchers. The vast majority of million-dollar transactions involve large flat types (5-room, executive, and multi-generation) in mature estates with strong MRT accessibility. Queenstown, Bishan, Toa Payoh, Kallang/Whampoa, and Bukit Merah account for a disproportionate share of such transactions. Floor level and remaining lease also matter: high-floor executive flats with 80–90 years of lease remaining in well-maintained blocks trade at significant premiums.

The broader macro context matters too. The April 2023 cooling measures (which raised ABSD for second-property Singapore Citizens from 17% to 20% and for foreigners from 30% to 60%) suppressed some private property demand and redirected a portion towards the HDB resale market. At the same time, the 15-month wait-out period for private property owners purchasing HDB resale flats means that private-to-public downgraders face a meaningful waiting cost, which tends to push up the price they are willing to pay when they can transact. These two dynamics — more buyers competing for top-tier HDB resale flats and a constrained supply of such units — sustain million-dollar transaction volumes even as overall HDB prices plateau.

How to Use HDB Resale Data for Buying and Selling Decisions

The most important data source for any HDB buyer or seller is the HDB Resale Flat Prices dataset, available free at data.gov.sg. This dataset lists every registered HDB resale transaction by address (block and street), flat type, storey range, floor area (sqm), resale price, remaining lease, and month of registration. Updated monthly with approximately a 2–4 week lag, it is the primary reference for any price benchmarking exercise.

For a seller, the process is: identify all 4-room resale transactions in your block and neighbouring blocks over the past 6–12 months. Isolate the transactions by storey range (high, mid, low) closest to your own floor. Compute the median price and median psf. Compare your flat’s specifications (floor area, remaining lease, renovation state) against those comparables to arrive at a pricing range. A well-renovated high-floor unit with 75+ years remaining lease should price at or above the top quartile of comparables; an older low-floor unit below the median.

For a buyer, the same dataset allows you to compute the Cash Over Valuation (COV) — the difference between the transacted price and the HDB-assessed value — though COV is not published directly. Instead, compare the transacted price against the HDB valuation you receive after submitting an Intent to Buy. If transacted prices for comparable units consistently exceed valuations by S$20,000–S$50,000, factor that COV into your cash planning: COV must be paid in cash, not CPF.

Our Singapore HDB Resale Price Index Guide 2026 covers how to interpret RPI movements in full, while our HDB Resale Buying Process Guide 2026 walks through the full transaction process from HFE application to key collection.

Worked Example: The Lim Family’s Resale Pricing Strategy

Profile: Mr and Mrs Lim (Singapore Citizens), sellers of a 5-room HDB flat in Ang Mo Kio, 1,291 sqft, Floor 12–14, MOP cleared January 2024. They purchased at S$520,000 in 2019 and used S$150,000 CPF (with S$40,000 accrued interest by 2026) and an HDB loan at 2.6%.

Market benchmarking: Using the data.gov.sg dataset, they identify 18 transactions of 5-room flats in their estate over the past 12 months: floors 07–09 ranged from S$580,000–S$620,000; floors 10–14 ranged from S$610,000–S$665,000; floor 15+ ranged from S$650,000–S$700,000. Median for their storey band: S$635,000.

Their flat’s specifications: 76 years remaining lease (2026). Recently renovated kitchen and bathrooms (2022, S$35,000 spend). North-facing with corridor view (modest discount). No outstanding Town Council arrears.

Pricing decision: Given renovation premium but below-median orientation, they price at S$638,000 — fractionally above the storey-band median. They receive two offers: S$625,000 (no agent, cash-light buyer) and S$640,000 (buyer using CPF and bank loan). They accept the second offer.

Net proceeds calculation: Gross S$640,000 − outstanding HDB loan (S$195,000) − CPF refund with accrued interest (S$190,000) − legal fees (S$2,500) = approximately S$252,500 net cash to the Lims after completion. They use this as the down payment for an RCR resale condo, subject to the 15-month wait-out period (they are SPR buyers) not applying to them as Singapore Citizens without a pre-existing private property interest.

Why This Matters: HDB as a Wealth Accumulation and Affordability Tool

The HDB resale market occupies a unique position globally: it is simultaneously a public housing programme and a significant component of household wealth for the majority of Singapore residents. More than 80% of Singapore residents live in HDB flats, and for most of them, the flat represents the single largest asset on the household balance sheet. Understanding how to read market data, price correctly, time the market cycle, and manage the proceeds of a resale transaction is therefore a financial literacy issue with material consequences.

The Q1 2026 RPI dip of −0.1% is modest and may not persist, but it represents the first evidence of supply catching up with demand after the extraordinary 2021–2023 surge. The June 2026 BTO launch of 6,952 flats across 7 projects — including Plus and Prime-category flats in Lakeview/Shunfu and Kallang/Whampoa — will provide further supply that, upon TOP in 5–6 years, adds to the MOP pipeline. Buyers considering a resale flat today should factor in this medium-term supply trajectory when assessing whether to pay a market-rate or below-market price in a particular estate.

For sellers, the plateau in overall RPI does not mean all estates are equally flat: the data shows continued strength in well-located mature estates and continued moderation in non-mature estates where BTO supply has been most generous. Estate-level and block-level analysis, not national headline figures, should drive pricing decisions.

What Might Come Next: URA Q2 Flash Estimates and HDB Policy Watch

The URA Q2 2026 private residential property flash estimates are expected in the first week of July 2026, with HDB’s comparable Q2 resale statistics following approximately two weeks later. These will be the first quarterly data points to reflect a full quarter of market activity since the June 2026 BTO launch and the Lorong Puntong GLS tender (launched June 2026, tender close expected mid-July 2026). Industry observers are watching whether the modest Q1 2026 RPI dip translates into a sustained trend or whether volumes and prices recover in Q2 driven by year-end school-allocation planning by families.

On the policy front, the Ministry of National Development has indicated no immediate plans to adjust existing HDB resale market measures. The 15-month wait-out period and the PLH 10-year MOP rules introduced in May 2026 are expected to remain in place for the foreseeable future. Any relaxation would likely require evidence of a sustained demand-driven price correction, which the Q1 2026 data alone does not provide.

Frequently Asked Questions

What does the RPI −0.1% in Q1 2026 mean in practical terms?

A −0.1% quarter-on-quarter change in the RPI means that, controlling for flat type, storey range, floor area, estate, and remaining lease, the average resale price in Q1 2026 was marginally lower than in Q4 2025. In absolute terms, a flat that would have been worth S$650,000 at the Q4 2025 pricing level is now worth approximately S$649,350 at Q1 2026 pricing — a difference of S$650. This is a statistical signal of a turning point rather than a meaningful financial impact on any individual transaction. The significance is in the directionality: it is the first decline in six years and suggests the period of sustained price growth has paused, if not reversed. Whether this becomes a sustained trend depends on supply (BTO completions, MOP waves) and demand (income growth, interest rates, immigration policy) dynamics over the next 2–4 quarters.

How do I find the actual transacted prices for flats near the one I want to buy?

The most direct source is the HDB Resale Flat Prices dataset on data.gov.sg, updated monthly. You can download the full dataset as a CSV and filter by block, street, flat type, and storey range. Alternatively, the HDB Resale Portal (myHDBPage) provides a built-in comparable transaction search for buyers with an active Intent to Buy. The HDB Resale Portal also shows HDB’s assessed valuation for each flat, which you can compare against recent transacted prices to gauge the current COV level. SRX and 99.co also aggregate this data in more user-friendly dashboards, though they typically have a 1–3 week lag relative to data.gov.sg.

Is the 15-month wait-out period for private property sellers buying HDB resale still in force?

Yes. The 15-month wait-out period, introduced on 30 September 2022, requires a person who has disposed of a private residential property (whether by sale, gift, or compulsory acquisition) to wait 15 months before submitting an Intent to Buy for an HDB resale flat. This applies to both the main applicant and all listed occupiers. The period is measured from the date of disposal (typically the legal completion date for a sale, or the date of distribution for a gift). There are limited exceptions: persons over 55 buying a 4-room or smaller flat are exempt. The measure was introduced to reduce private-to-public downgrader demand pressure on the HDB resale market and remains in force as at June 2026.

How does the remaining lease of an HDB flat affect its resale value?

Remaining lease affects resale value through two direct channels. First, CPF withdrawal is restricted for flats with fewer than 60 years remaining lease, which narrows the pool of eligible buyers and reduces their purchasing power — the immediate effect is a discount to market. Second, bank financing may be more restrictive for short-lease flats, as banks apply LTV adjustments when the property’s remaining lease at the end of the loan term is below certain thresholds. Empirically, research shows that HDB flats lose value more rapidly once remaining lease falls below 60 years, and the effect accelerates below 40 years. For sellers, a flat with 80–90 years remaining trades at a meaningful premium over an otherwise identical flat with 55–60 years remaining.

Can Singapore Permanent Residents buy HDB resale flats, and are there restrictions?

Singapore Permanent Residents (SPRs) can purchase HDB resale flats but face additional restrictions compared to Singapore Citizens. SPRs cannot purchase new BTO flats (except as part of a household with at least one SC). For resale, the SPR household must have obtained a valid HDB Flat Eligibility (HFE) letter, which is granted if the SPR has held PR status for at least 3 years. SPRs are subject to ABSD of 5% on their first residential property, and if buying as a single SPR, they must be at least 35 years old. SPR households are also subject to the Ethnic Integration Policy quota when purchasing resale flats. Our HDB Flat Eligibility Guide 2026 covers SPR eligibility in full.

What CPF grants can I use when buying an HDB resale flat?

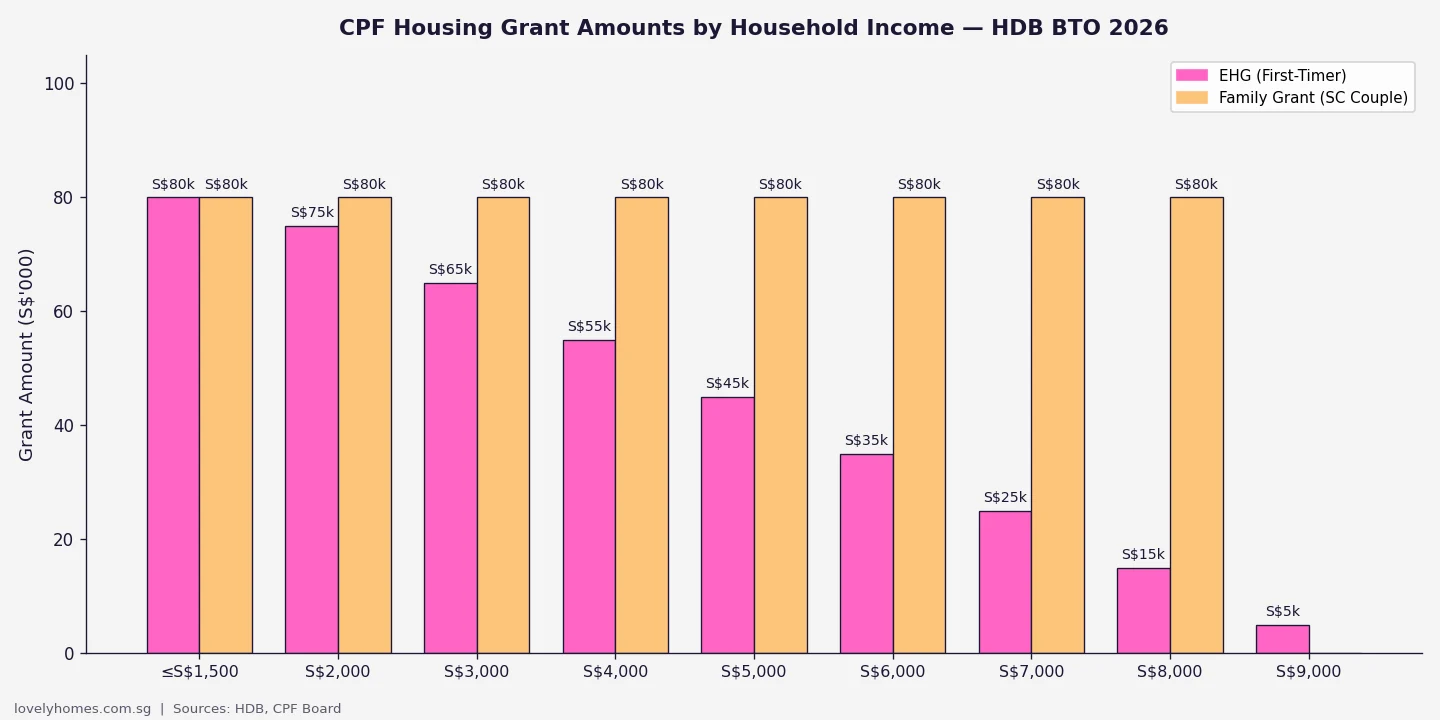

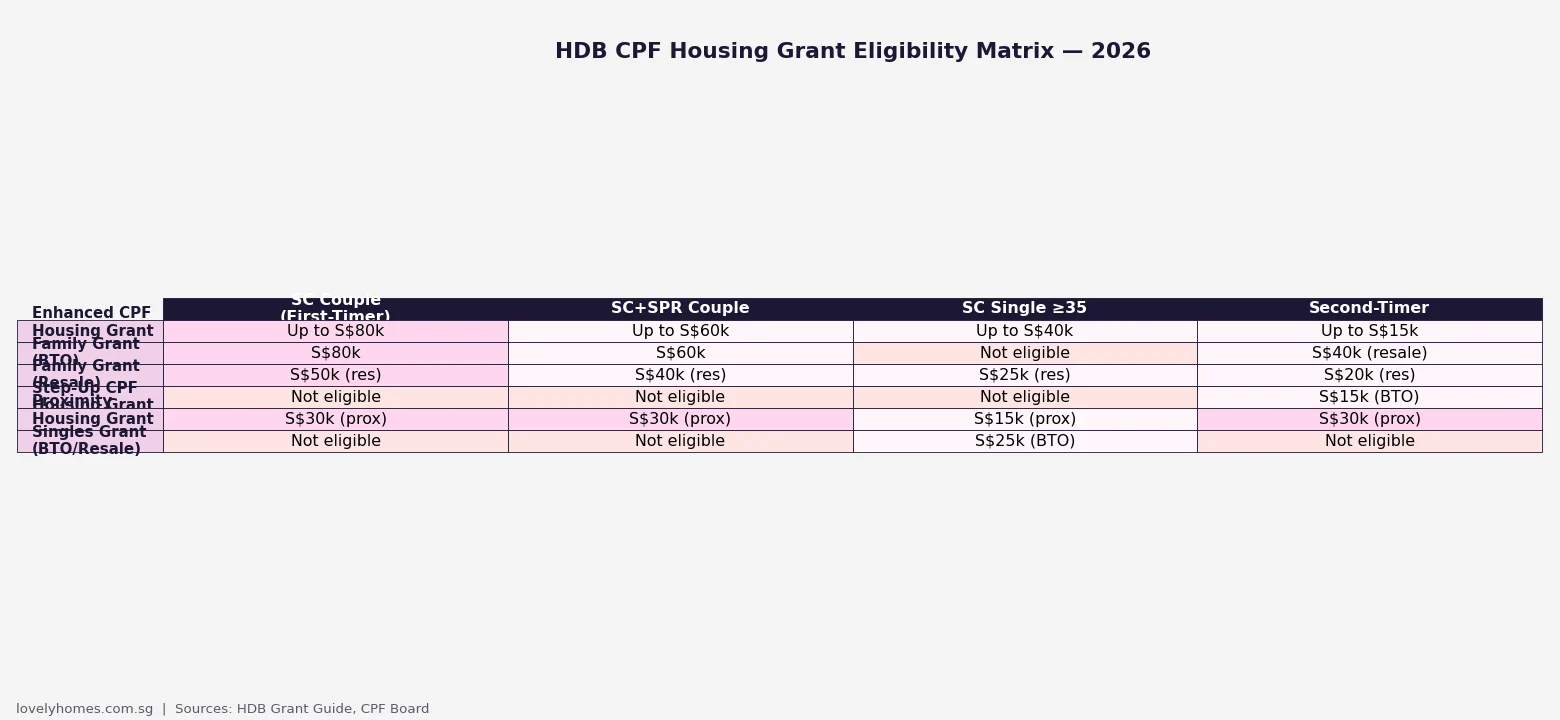

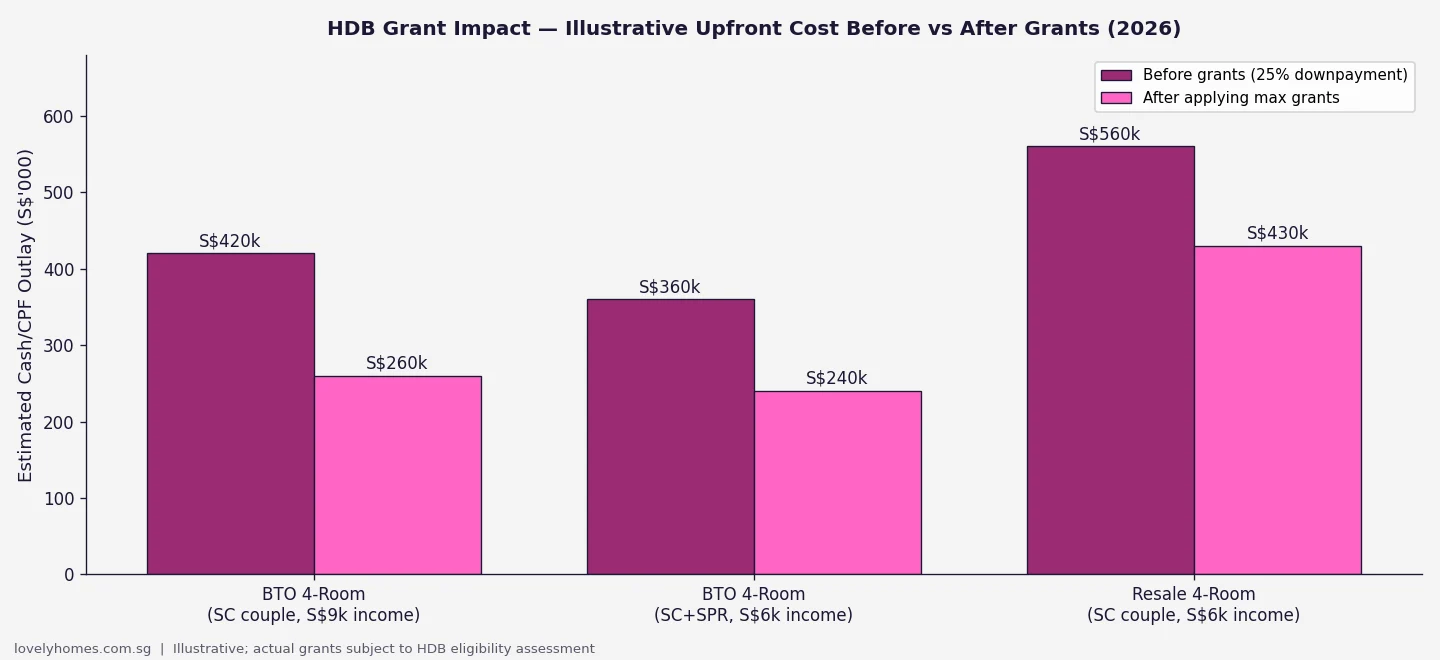

HDB resale buyers may be eligible for the Enhanced Housing Grant (EHG), Family Grant, and Proximity Housing Grant (PHG), subject to household income ceilings and eligibility criteria. For a first-timer SC couple buying a resale flat, the maximum combined grants can reach up to S$230,000 (EHG S$120,000 + Family Grant S$80,000 + PHG S$30,000) at the lowest income tier. The EHG is income-tested and tapers from a maximum of S$120,000 for households earning S$1,500 or less per month to S$0 for those earning above S$9,000. Unlike BTO grants, resale grants are not subject to a flat-type restriction — they can be applied to any flat type in any estate. Our CPF Housing Grant Guide 2026 explains each grant scheme in detail.

Is ABSD payable when buying an HDB resale flat?

Yes. ABSD applies to HDB resale flats in the same way as private residential properties. A Singapore Citizen buying their first residential property (including an HDB resale flat) pays 0% ABSD. A Citizen buying a second residential property pays 20% ABSD on the purchase price. A Singapore PR buying their first residential property pays 5% ABSD. Because ABSD is calculated on the full purchase price and must be paid in cash (CPF cannot be used), the ABSD liability can be material — 20% of S$580,000 on a Tampines 4-room resale would be S$116,000 in cash. For SC couples where one spouse owns private property, the ABSD remission scheme may allow recovery of the ABSD if the private property is sold within 6 months of the HDB resale completion.

Related Articles

- Singapore HDB Resale Price Index Guide 2026: What the RPI Measures and How to Read It

- Singapore HDB Resale Buying Process Guide 2026: Complete Step-by-Step from HFE to Keys

- Singapore HDB Flat Eligibility Guide 2026: HFE Check, Income Ceilings and What Qualifies You

- Singapore HDB CPF Housing Grant Guide 2026: EHG, Family Grant, PHG and More Explained

- Singapore HDB EIP Guide 2026: Ethnic Integration Policy Quotas and Resale Impact

- Singapore Property Financing Guide 2026: LTV, TDSR, MSR and HDB vs Bank Loan Explained

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer: This article is for general informational purposes only and does not constitute financial, legal or professional advice. HDB resale prices are indicative and based on publicly available data; individual transaction prices will vary significantly by block, storey, remaining lease, and flat condition. Always verify prices using official sources including HDB’s Resale Flat Prices dataset at data.gov.sg, and seek advice from a licensed property agent and financial adviser before transacting. For HDB eligibility and grants, refer to hdb.gov.sg. For ABSD and stamp duty matters, refer to iras.gov.sg.