Loan-to-Value (LTV) is the single most important number in a Singapore home-purchase budget. It tells you, before anything else, the maximum slice of the property price the bank is willing to lend — and therefore the cash and CPF you need to bring yourself. Misread it by even five percentage points and you may find yourself short by tens of thousands of dollars on completion day.

This guide walks you through the LTV framework as it stands in 2026 — the rate ladder by housing-loan count, how tenure and age cut into the cap, how LTV interacts with TDSR and MSR, and the practical decisions buyers face. The framework is set by the Monetary Authority of Singapore (MAS) Notice 645 and reinforced by HDB’s own concessionary loan rules.

Quick Answer — LTV at a glance

Bank loan, first housing loan: up to 75% LTV, tenure up to 30 years for private (25 years for HDB).

Second housing loan: up to 45% LTV; third or more: up to 35%.

If tenure exceeds 30 years OR runs past borrower age 65: caps drop to 55% / 25% / 15%.

HDB Concessionary loan: up to 75% LTV, 25-year max tenure.

The cash component of the down-payment is at least 5% (private) or 10% (HDB Concessionary).

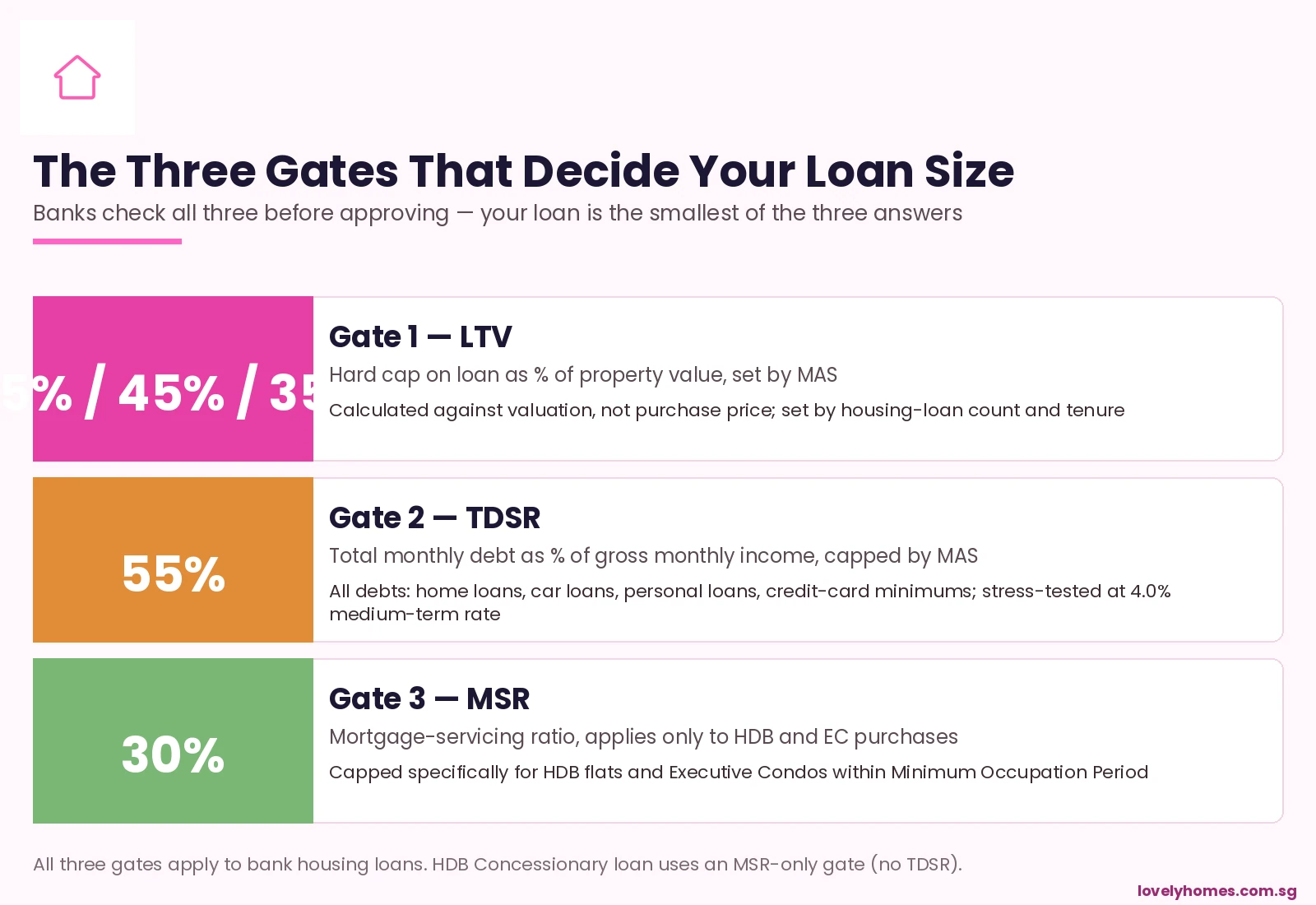

LTV is one of three gates — you must also pass TDSR (55%) and, for HDB/EC, MSR (30%).

What Is Loan-to-Value — and Why Does It Exist?

LTV is the ratio of the housing loan amount to the property’s purchase price or market value, whichever is lower. Banks use it as a first-pass risk control: a higher LTV means thinner equity from the borrower, which means less cushion if property prices fall.

MAS sets the LTV ceiling industry-wide. The ceiling has been progressively tightened since the cooling-measure era began in 2013, as the regulator’s priority shifted from supporting first-time owner-occupiers to discouraging investment-driven leverage. The most recent recalibration was December 2021, which lowered LTV on second housing loans from 50% to 45% and on third loans from 40% to 35%. That framework remains in force in 2026.

LTV limits Singapore 2026 — the cap that sets the size of your loan.

The 2026 LTV Ladder — Bank Housing Loans

The headline number you have heard — “75% LTV” — only applies to first-time housing-loan borrowers under standard tenure. Once you have an existing housing loan or stretch the tenure beyond the conservative limit, the cap falls sharply.

Figure 1: LTV ladder for bank housing loans, by housing-loan count and tenure.

Borrower scenario

Standard LTV

If tenure > 30 yrs OR runs past age 65

No outstanding housing loan

75%

55%

One outstanding housing loan

45%

25%

Two or more outstanding loans

35%

15%

Two practical points are worth flagging. First, the 30-year tenure rule does not mean a 30-year loan is always available — banks themselves often cap tenure earlier for older borrowers. Second, the “outstanding housing loan” count includes loans for properties you co-own as a guarantor or as a second name on the title; the regulator does not look only at your primary mortgage.

Cash Component — The Mandatory Minimum

LTV defines the maximum the bank will lend; the rest must come from the buyer. But of that “rest”, a minimum portion must be in cash and cannot be funded from CPF Ordinary Account.

Loan type

Minimum cash

Balance from CPF or cash

Bank loan, 75% LTV

5% of price

20% of price

Bank loan, 55% LTV (long tenure)

10% of price

35% of price

Bank loan, 45% LTV (2nd loan)

25% of price

30% of price

HDB Concessionary loan

10% of price

15% of price (CPF or cash)

The cash floor is the practical constraint that catches most upgraders by surprise. A buyer with a S$1.5M target and 75% LTV needs S$75,000 cash on the table at exercise day — on top of BSD, ABSD, and legal fees. CPF Ordinary Account balances cannot substitute for this minimum.

The Three Gates — LTV, TDSR, and MSR

LTV is only one of three caps. Banks must also satisfy:

Figure 2: The three gates — your loan is the smallest of the three answers.

LTV — absolute % of property value, set by MAS as above.

TDSR (Total Debt Servicing Ratio) — total monthly debt repayments capped at 55% of gross monthly income, stress-tested against a 4.0% medium-term interest rate even though current bank rates are well below that. All debts count: home loans, car loans, education loans, personal loans, credit-card minimum repayments.

MSR (Mortgage Servicing Ratio) — only for HDB flats and Executive Condos within MOP, capped at 30% of gross monthly income.

The bank computes the maximum loan under each rule and lends you the smaller of the three. A buyer at 75% LTV but with a heavy car loan can find their actual loan capped by TDSR rather than LTV; an HDB buyer with no other debts often finds MSR — not LTV — is the binding constraint.

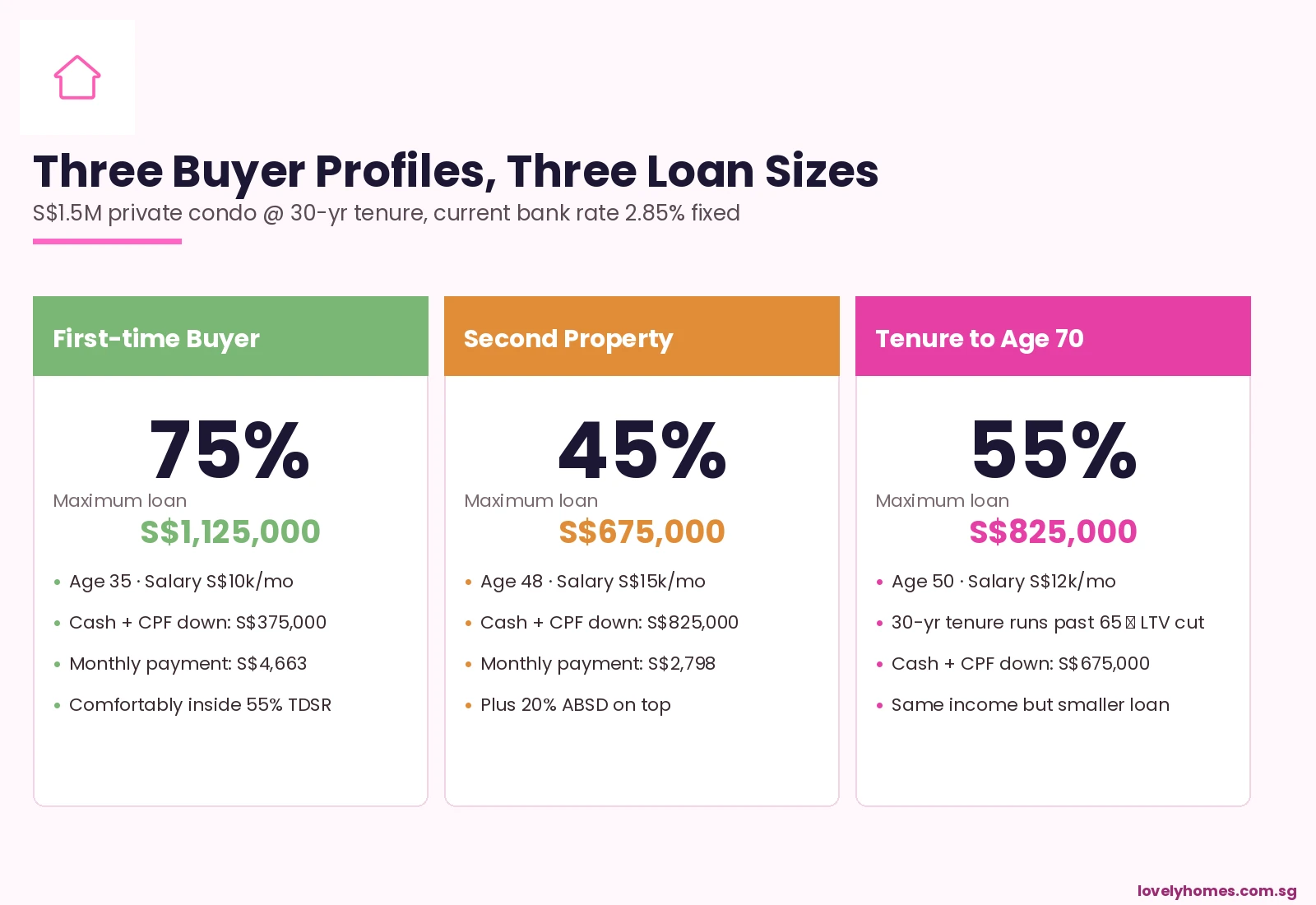

Worked Example — Three Buyer Profiles, Three Loan Sizes

Consider three buyers all looking at the same S$1.5M private condo, taking a 30-year loan at 2.85% fixed:

Figure 3: Three buyer profiles compared on identical S$1.5M condo.

The first-time buyer at age 35, salary S$10k/month, no other loans, gets the textbook 75% LTV: S$1,125,000 loan, S$375,000 down (5% cash + 20% CPF/cash). Monthly payment S$4,663 — comfortably inside 55% of S$10k.

The second-property buyer at age 48 with one outstanding home loan is capped at 45% LTV: S$675,000 loan only, S$825,000 down. This buyer also pays 20% ABSD on the new property — an additional S$300,000.

The upgrader to a tenure that runs past age 65 at age 50 is capped at 55% LTV (because the 30-year tenure runs to age 80, well past 65): S$825,000 loan only. Same income as the second buyer, but bigger loan because no existing housing loan; still smaller than the first-time buyer because of the tenure rule.

HDB Concessionary Loan — A Different Beast

The HDB Concessionary loan, available to buyers of new and resale HDB flats meeting income and ownership criteria, runs on its own framework:

LTV: up to 75% of valuation, identical to first-time bank loan.

Tenure cap: 25 years for new flats, 25 or 30 years for resale depending on age.

Interest rate: pegged to CPF Ordinary Account rate plus 0.1% — currently 2.60% (CPF OA at 2.5% + 0.1% spread, rate-locked).

MSR-only gate: 30% of gross income, no separate TDSR overlay.

Rule of two: Singapore households are limited to two HDB Concessionary loans across a lifetime, with a five-year wait between the first and second.

For comparable risk profiles, the Concessionary loan typically beats bank loans on cost; the trade-off is the more rigid tenure cap and the requirement to deplete CPF OA balances above S$20,000 first.

What This Means for You as a Buyer in 2026

The 2026 environment is the tightest LTV regime Singapore has had in two decades. Combined with stress-tested TDSR at 4.0% and ABSD at 20% on second properties for citizens, the effective leverage available to a typical buyer is materially below where it sat pre-2018.

Three practical conclusions:

Plan around the binding gate, not around LTV alone. Run all three checks before committing — ask your banker to model TDSR with all your debts, and MSR if you are buying HDB or EC.

Tenure is now a real lever for older buyers. Choosing a 25-year tenure that ends before 65 can keep you on the 75% LTV track even at age 40. Stretching to 30 years past 65 cuts to 55%.

Reserve capital, not just cash. The 5% mandatory-cash floor is the headline; in practice you also need BSD, ABSD, legal fees, and a six-month reserve buffer. A S$1.5M purchase typically requires S$120,000 in cash on the table at exercise.

Frequently Asked Questions

Is LTV calculated on the purchase price or the valuation?

The lower of the two. If a property is bought at S$1.5M but the valuation is S$1.45M, the bank applies LTV to S$1.45M. The remaining S$50,000 must be covered in cash — this is the dreaded “valuation gap” that catches buyers in rising markets.

Does selling my existing property before buying a new one reset my LTV count?

Yes — provided the existing housing loan is fully discharged before the OTP date on the new purchase. Banks check the credit bureau records on the day of credit assessment, and a discharged loan no longer counts as outstanding. This is why “sell-then-buy” buyers can access the 75% LTV track that “buy-then-sell” buyers cannot.

Can I take a 35-year loan if I am only 30 years old?

The MAS framework permits it, but bank policies vary. Most banks prefer to cap tenure at 30 years even for young borrowers. Even where 35 years is permitted, the over-30 tenure rule kicks in and reduces the LTV cap to 55% on the first loan — usually a poor trade-off.

Does my spouse’s housing loan affect my LTV count?

If you co-borrow on a single property, you are counted as one applicant for LTV purposes. If your spouse has a separate property in their sole name with an outstanding loan, that does not count against you when you buy in your sole name — this is the basis of decoupling strategies that release ABSD allowance.

What happens if my loan application is approved but my income drops before completion?

Banks reserve the right to re-underwrite at completion. A material income drop (typically more than 20%) between approval and completion can lead to a loan reduction or, in extreme cases, withdrawal. Buyers facing this should engage their banker proactively rather than wait for completion day.

Are there any loans that bypass LTV?

Not for residential property. Some private banks offer “lombard” or asset-backed lending against shares, bonds, or insurance policies, which sit outside the housing-loan framework, but these are not housing loans and the security is the financial portfolio, not the property. They are an option mainly for high-net-worth borrowers with substantial liquid investments.

Does SORA-pegged versus fixed-rate make a difference to LTV?

No. LTV is set by the housing-loan count and tenure, regardless of the rate type. Fixed and floating loans face the same LTV cap. Choice between fixed and SORA is a separate decision driven by rate outlook and personal risk preference.

This article provides general information about LTV and related housing-loan rules in Singapore as at May 2026. It is not financial, tax, or legal advice. LTV ceilings, cash-component rules, TDSR and MSR are set by the Monetary Authority of Singapore, the Inland Revenue Authority of Singapore, and the Housing & Development Board, and may be amended at any time. For authoritative figures, consult MAS, HDB, CPF Board, the Urban Redevelopment Authority, and SingStat. Before signing an Option to Purchase, engage a licensed Singapore mortgage banker, conveyancing solicitor, and where relevant a financial planner to model your situation specifically.

Seller’s Stamp Duty (SSD) of 12%, 8%, or 4% applies if you sell within 3 years of purchase (private residential properties)

Agent commission is typically 1–2% of sale price — negotiable; CEA-registered agents only

CPF funds used must be refunded to CPF OA with Accrued Interest (compounded at 2.5% p.a.) upon sale

The sale process from OTP to legal completion typically takes 10–12 weeks for private property; 8–12 weeks for HDB

Outstanding mortgage must be discharged from sale proceeds; early repayment penalty may apply (lock-in period)

No Capital Gains Tax in Singapore — profits from property sales are generally not taxed unless you are classified as a property trader by IRAS

Decoupling a property before sale may reduce ABSD on a subsequent purchase but requires careful legal structuring to avoid Section 33A anti-avoidance provisions

Selling Property in Singapore — Overview

Singapore’s property market has no Capital Gains Tax — meaning that profits from the sale of residential property are generally not subject to income tax, provided IRAS does not classify you as conducting a property trading business. However, selling a property in Singapore does involve a web of stamp duties, CPF refund obligations, agent fees, legal costs, and outstanding loan discharges. Understanding these costs upfront prevents unpleasant surprises at the point of sale.

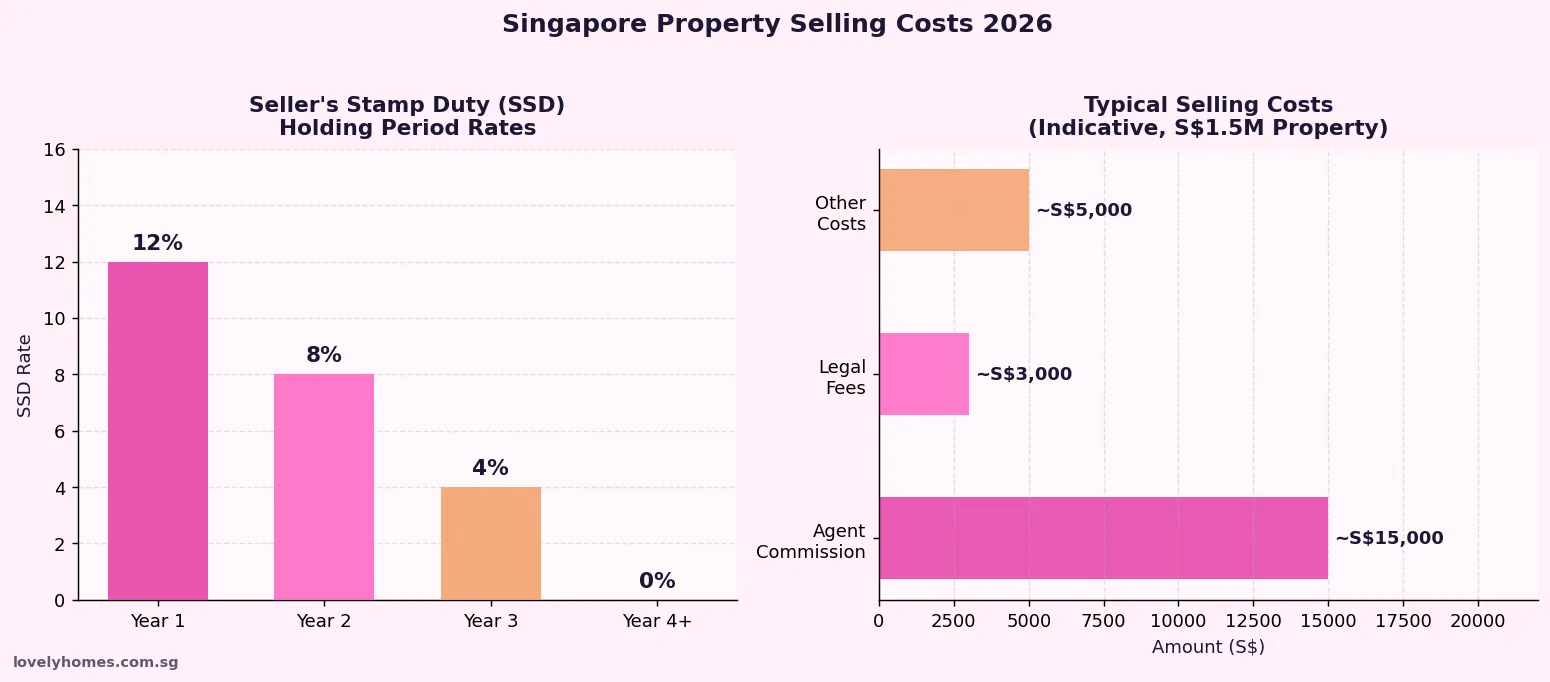

The Seller’s Stamp Duty (SSD) — introduced in January 2011 and most recently recalibrated in April 2023 — is the most significant policy lever for sellers. At 12% for properties sold within the first year of purchase, SSD is designed to deter speculative flipping. This guide covers every major cost and step for selling a private residential property (condo, landed, or HDB) in Singapore in 2026.

Figure 1: Seller’s Stamp Duty (SSD) rates and indicative selling cost components for a S$1.5M property, Singapore 2026.

Seller’s Stamp Duty (SSD) — Rates and Rules

Seller’s Stamp Duty is payable by the seller if a residential property is sold within 3 years of its purchase date (for private properties). The rates are based on the higher of the sale price or market value:

Holding Period

SSD Rate (Current, from Apr 2023)

SSD on S$1.5M Sale

Up to 1 year

12%

S$180,000

More than 1, up to 2 years

8%

S$120,000

More than 2, up to 3 years

4%

S$60,000

More than 3 years

0%

Nil

HDB flats are not subject to SSD, but have their own MOP (Minimum Occupation Period) of 5 years — during which the flat cannot be sold on the resale market at all.

All Costs When Selling Your Property

Cost

Typical Amount

Paid by / When

Agent Commission

1–2% of sale price

Seller; at completion

Legal Fees (conveyancing)

~S$2,500–S$4,000

Seller; at completion

Seller’s Stamp Duty (SSD)

0–12% of sale price (if <3 years)

Seller; within 14 days of OTP exercise

Mortgage Early Repayment Penalty

0.75–1.5% of outstanding loan (if in lock-in)

Seller; upon full redemption at completion

CPF Refund (OA + Accrued Interest)

All CPF used + 2.5% p.a. compound interest

Mandatory; deducted from proceeds at completion

Property Tax (prorated to sale date)

Varies by AV; prorated to completion date

Seller; adjusted at completion

HDB Admin Fee (HDB resale only)

S$40–S$80

Seller; to HDB

Worked Example: Selling a S$1.5M Condo Purchased 2 Years Ago

Scenario: SC seller, selling a condo purchased in April 2024 for S$1.4M, now selling in April 2026 at S$1.5M. Outstanding bank loan: S$900,000. CPF used: S$200,000 OA + S$10,000 accrued interest.

Gross Sale Price: S$1,500,000

Less SSD (8% × S$1.5M, sold in year 2): −S$120,000

Less Agent Commission (1.5%): −S$22,500

Less Legal Fees: −S$3,000

Less Outstanding Loan Redemption: −S$900,000

Less CPF Refund (S$200K + S$10K interest): −S$210,000

Net Cash Proceeds to Seller: S$1,500,000 − S$120,000 − S$22,500 − S$3,000 − S$900,000 − S$210,000 = S$244,500

Of which cash in hand (after CPF returned to CPF, not to pocket): ~S$244,500 (cash) + S$210,000 returned to CPF OA

Note: This example excludes any early repayment penalty on the bank loan. Verify with your bank and a property consultant. IRAS may treat profits as income if you are assessed as a property trader — consult a tax professional if you have sold multiple properties in recent years.

The Private Property Sale Process — Step by Step

For a private residential property (condominium or landed), the sale process broadly follows these stages over 10–12 weeks:

Appoint a CEA-licensed agent (or sell directly). Agent markets the property, manages viewings, and facilitates negotiations.

Accept an offer and grant an OTP. The buyer pays an Option Fee (typically 1% of agreed price). The OTP is valid for 14 days (standard) — extendable to 21 days by agreement.

Buyer exercises OTP — pays the balance 4–9% deposit within the OTP period. Both buyer and seller appoint conveyancing solicitors.

Solicitors conduct due diligence — title search, CPF charge check, Inland Revenue caveats, mortgagee consent if applicable.

Completion — typically 8–10 weeks after OTP exercise. Sale proceeds are disbursed, mortgage is redeemed, CPF is refunded, and keys are handed over.

Frequently Asked Questions

Is there Capital Gains Tax on property sales in Singapore?

No. Singapore does not impose a Capital Gains Tax on property sales by individuals. Profits from property sales are not taxable — provided IRAS does not classify you as a property trader (i.e. someone who buys and sells properties as a business, subject to income tax on profits). If you have sold multiple properties in a short period, consult a tax professional to confirm your IRAS classification. The Inland Revenue Authority of Singapore (IRAS) administers all property tax matters.

How is the CPF refund calculated when I sell my property?

Upon selling your property, you must refund to your CPF OA: (1) all CPF funds withdrawn for the property (down payment, monthly instalments, BSD, legal fees funded by CPF), plus (2) accrued interest at 2.5% per annum, compounded annually, on those withdrawn amounts. This refund goes back into your CPF OA — it is not a tax, but it reduces the cash proceeds you receive. The CPF Board calculates the exact refund amount at completion. For long-held properties with large CPF withdrawals, accrued interest can be significant.

What if the sale price is less than the outstanding loan and CPF refund?

If the sale proceeds are insufficient to fully redeem the outstanding mortgage and refund all CPF funds with accrued interest, you would face a shortfall. In this scenario, you would need to top up the difference in cash. This is sometimes called a “negative sale.” To avoid this situation, sellers should always compute their minimum viable sale price before listing — accounting for loan balance, CPF refund, SSD, agent fees, and legal costs.

Can I avoid SSD by transferring the property to a family member?

No. SSD applies to all legal transfers of residential property within the holding period — including transfers to family members, whether by sale, gift, or trust arrangement. IRAS treats these as disposals subject to SSD. Section 33A of the Stamp Duties Act also provides anti-avoidance powers allowing IRAS to look through artificial arrangements designed to circumvent stamp duty obligations. Seek advice from a qualified stamp duty lawyer before attempting any form of property restructuring.

What happens if I have an HDB bank loan and sell before 3 years?

Unlike private property, HDB flats carry no SSD on their own — however, HDB resale flats cannot be sold during the 5-year MOP. If you have a bank loan (not an HDB concessionary loan) on a private property, an early redemption penalty (clawback) of 0.75%–1.5% of the outstanding loan may apply if you sell during the loan’s lock-in period (typically 1–3 years). Check your bank’s loan terms carefully before committing to sell. HDB concessionary loans do not carry lock-in penalties.

Disclaimer: Information on this page is for general reference only and does not constitute professional property, legal, financial, or tax advice. Stamp duty rules, CPF policies, and property regulations may change — verify all details with IRAS (iras.gov.sg), CPF Board (cpf.gov.sg), and HDB (hdb.gov.sg) before transacting. Consult a CEA-licensed property agent and a qualified solicitor for transaction-specific advice. LovelyHomes.com.sg does not hold a real estate agency licence.

Singapore Citizens and Eligible PRs may purchase HDB resale flats; certain restrictions apply to singles and PRs

The standard resale process takes 12–16 weeks from Option to Purchase (OTP) to key collection

Resale buyers may tap CPF Housing Grants: Enhanced CPF Housing Grant (EHG), Family Grant, and Proximity Grant — up to S$120,000 combined

HDB Loan Eligibility (HLE) letter or bank Approval-in-Principle (AIP) must be obtained before OTP is exercised

Cash-over-Valuation (COV) must be paid entirely in cash and is no longer disclosed by HDB — buyers and sellers negotiate based on market

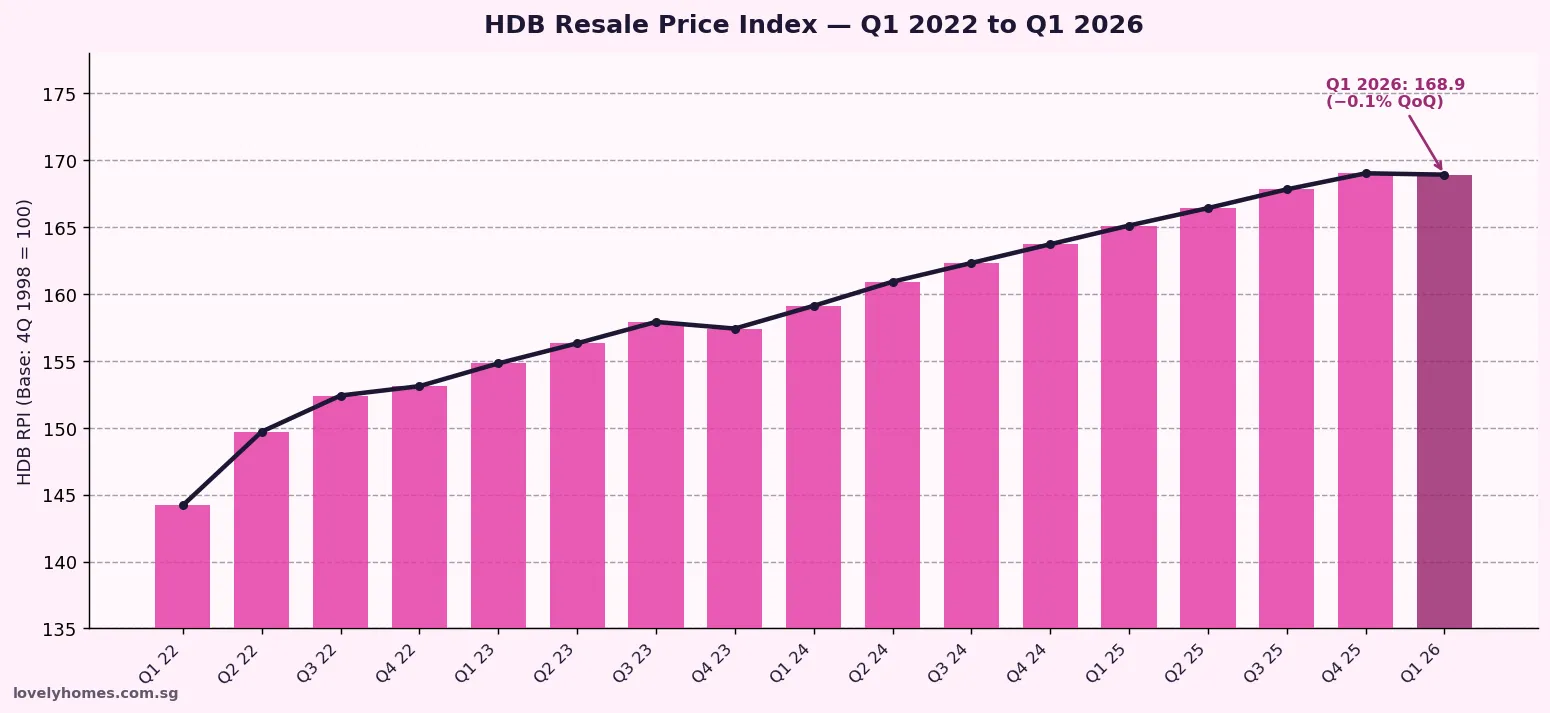

HDB resale prices fell −0.1% QoQ in Q1 2026 (first decline since Q2 2019), though 412 million-dollar transactions set an all-time record

Proximity Housing Grant (S$30,000) available if you live within 4 km of parents/children

What Is an HDB Resale Flat?

A resale HDB flat is a Housing & Development Board flat that has been previously owned by at least one household, has completed its Minimum Occupation Period (MOP) of at least 5 years, and is now available for purchase on the open secondary market through HDB’s resale portal. Unlike a Build-to-Order (BTO) flat — which involves purchasing directly from HDB at a subsidised price with a multi-year wait — a resale purchase is a private transaction between seller and buyer, with HDB administering the eligibility checks and transaction registration.

As of Q1 2026, the HDB Resale Price Index (RPI) stands at 168.9 — representing a rise of approximately 17% from Q1 2022 and a slight moderation of −0.1% quarter-on-quarter, the first quarterly dip since Q2 2019. The resale market remains characterised by sustained demand from upgraders, PRs, and those who cannot wait for BTO completion.

Figure 1: HDB Resale Price Index (RPI) — Q1 2022 to Q1 2026. Source: HDB / URA flash estimates.

Who Can Buy an HDB Resale Flat?

Eligibility for HDB resale flat purchase is governed by HDB’s Ethnic Integration Policy (EIP) and Resale Eligibility Scheme. The primary conditions are as follows:

Buyer Type

Conditions

CPF Grants Available

SC Married Couple (both SC)

May buy any HDB resale flat; MOP 5 years

EHG (up to S$120K) + Family Grant (up to S$50K) + Proximity Grant

SC + PR Family Nucleus

At least 1 SC; can buy any resale flat

EHG (SC portion); reduced Family Grant

SC Singles (≥35 years old)

May only buy 5-room or smaller HDB flat; income ≤ S$7,000

Singles Grant (up to S$25K); EHG Singles

PR Family (no SC)

May buy after PR for 3 years; restricted flat types

No CPF grants; must wait 3 years PR

Foreigners

Not eligible to buy HDB resale flats

N/A

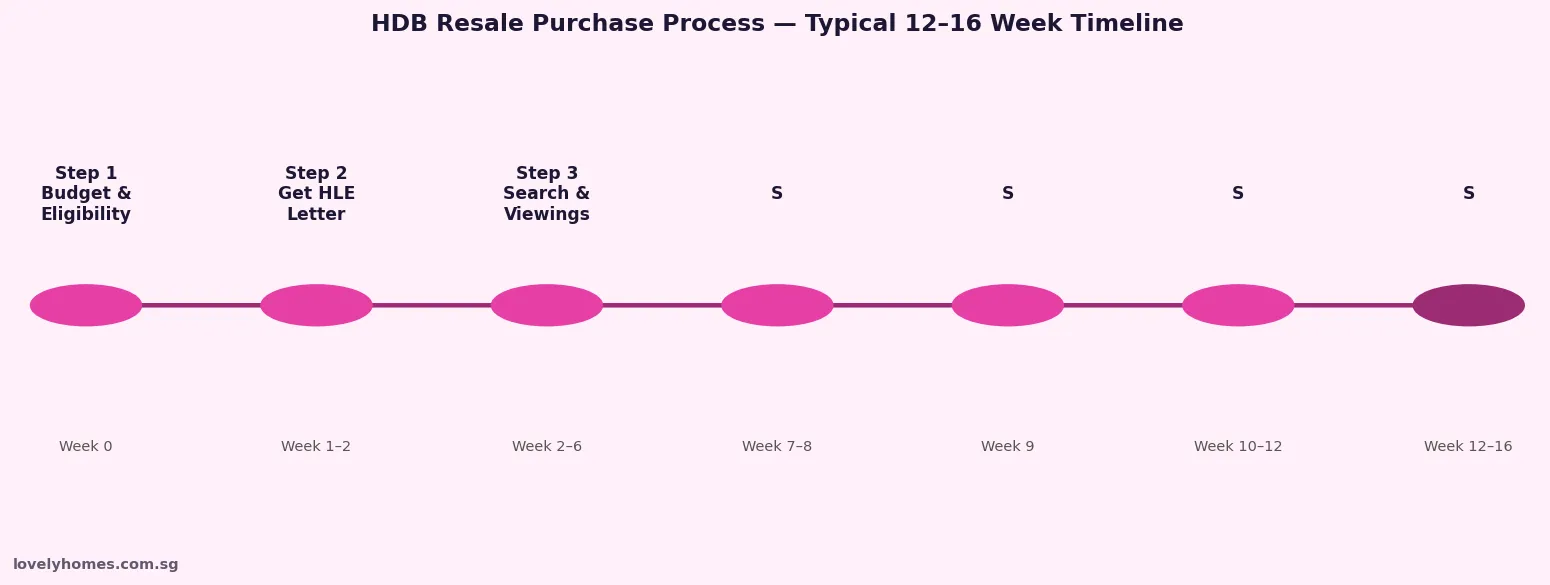

The HDB Resale Purchase Process — Step by Step

Buying an HDB resale flat involves a structured 12–16 week process administered jointly between the buyer, seller, and HDB’s portal. Below is the typical timeline:

Step 1 — Establish your budget and eligibility. Determine your income ceiling, grant eligibility, CPF OA savings, and maximum loan quantum. Use HDB’s e-Services portal to check eligibility. If using an HDB concessionary loan, apply for a Housing Loan Eligibility (HLE) letter. If using a bank loan, obtain an Approval-in-Principle (AIP).

Step 2 — Engage a CEA-registered property agent (optional but recommended). You may transact directly using HDB’s resale portal, or appoint a Council for Estate Agencies (CEA)-licensed agent. All agents must be CEA-registered. Agent commission of 1–2% of the purchase price is typically borne by the buyer on the buyer’s side.

Step 3 — Search and shortlist. Browse HDB Flat Portal or property portals for listings. Factor in HDB’s Ethnic Integration Policy (EIP) quotas — some blocks may have reached their Chinese, Malay, or Indian quota, restricting the sale to certain ethnic groups.

Step 4 — Grant the Option to Purchase (OTP). The seller grants the buyer an OTP in exchange for an Option Fee of S$1 to S$1,000 (negotiated). The OTP is valid for 21 calendar days. Once the OTP is issued, both parties register their intent on HDB’s resale portal.

Step 5 — Exercise the OTP. Within 21 days, the buyer must exercise the OTP by paying an Exercise Fee (up to S$5,000 minus the Option Fee). At this point, both buyer and seller must submit the resale application to HDB via the portal simultaneously. A conveyancing solicitor is appointed.

Step 6 — HDB Appointment. HDB reviews the application (approximately 4–8 weeks) and schedules a completion appointment. At this appointment, financial documents, CPF pledges, and legal transfers are completed.

Step 7 — Completion and key collection. Keys are handed over, and the transaction is registered with SLA. The buyer officially becomes the registered owner of the flat.

CPF Housing Grants for Resale HDB (2026)

Grant

Maximum Amount

Eligibility Condition

Enhanced CPF Housing Grant (EHG)

S$120,000 (family) / S$60,000 (singles)

First-timer; income ≤ S$9,000 (family) / ≤ S$4,500 (singles); must work continuously for 12 months

Family Grant

S$50,000 (both SC) / S$40,000 (SC+PR)

At least one applicant first-timer; buying for family nucleus

Note: Figures are illustrative. BSD and legal fees (approximately S$9,600 and S$2,500–4,000 respectively) are additional. Verify your specific scenario with HDB or a licensed property consultant.

Key Costs When Buying an HDB Resale Flat

Cost Item

Amount / Rate

Payment Method

Option Fee

S$1–S$1,000

Cash

Exercise Fee

Up to S$5,000 (minus Option Fee)

Cash

Cash-over-Valuation (COV)

Market-determined (if price > HDB valuation)

Cash only

Buyer’s Stamp Duty (BSD)

1–6% progressive on purchase price

CPF OA or cash (14 days)

ABSD (if applicable)

5% (PR 1st property) / 20% (SC 2nd property) etc.

Cash (14 days)

Legal Fees

~S$2,500–S$4,000

CPF OA or cash

Agent Commission (buyer side)

1–2% of purchase price (if appointed)

Cash

Frequently Asked Questions

Can a foreigner buy an HDB resale flat?

No. Only Singapore Citizens and Singapore Permanent Residents (in a family nucleus with at least one SC, and after 3 years of PR status) are eligible to purchase HDB resale flats. Foreigners cannot buy HDB flats under any circumstances.

What is Cash-over-Valuation (COV) and how does it work?

COV is the difference between the agreed purchase price and HDB’s official valuation of the flat. If you agree to pay S$650,000 for a flat valued by HDB at S$620,000, the COV is S$30,000. COV must be paid entirely in cash — it cannot be financed through an HDB or bank loan, and cannot be paid using CPF funds. HDB no longer publishes COV data; buyers and sellers negotiate based on recent transacted prices (available on HDB’s resale flat prices portal).

Can I use CPF to pay for an HDB resale flat?

Yes. You may use your CPF Ordinary Account (OA) savings to pay for the down payment, remaining purchase price (after loan), BSD, and legal fees. However, COV must be paid in cash. CPF usage is subject to the Valuation Limit (you can only use CPF up to the HDB valuation of the flat, not the transacted price). CPF funds used attract Accrued Interest (currently 2.5% per annum), which must be refunded to your CPF account upon sale.

How long does the HDB resale process take?

From the issuance of the OTP to key handover, the HDB resale process typically takes 12 to 16 weeks. The OTP itself has a 21-calendar-day validity period. After both parties register on HDB’s portal, HDB typically takes 4 to 8 weeks to schedule the completion appointment. Delays can occur if eligibility issues arise, if financing takes longer, or if there are outstanding issues with the flat (e.g. renovation works, outstanding season parking).

What is the Ethnic Integration Policy (EIP) and how does it affect buyers?

The Ethnic Integration Policy (EIP) limits the percentage of flats in each HDB block and neighbourhood that can be owned by each ethnic group (Chinese, Malay, Indian/Others). This ensures racial integration. If the EIP quota for your ethnicity in a particular block has been reached, you cannot purchase a flat there — even if the seller is willing. Check EIP quotas using HDB’s online EIP checker before shortlisting a flat.

Disclaimer: Information on this page is published for general reference only and does not constitute professional property, legal, financial, or CPF advice. HDB eligibility rules, grant quantum, and resale procedures may change — verify all details with HDB directly at hdb.gov.sg or through a CEA-registered property consultant before transacting. LovelyHomes.com.sg does not hold a real estate agency licence.

Joint Tenancy vs Tenancy in Common Singapore 2026: Which Is Right for You?

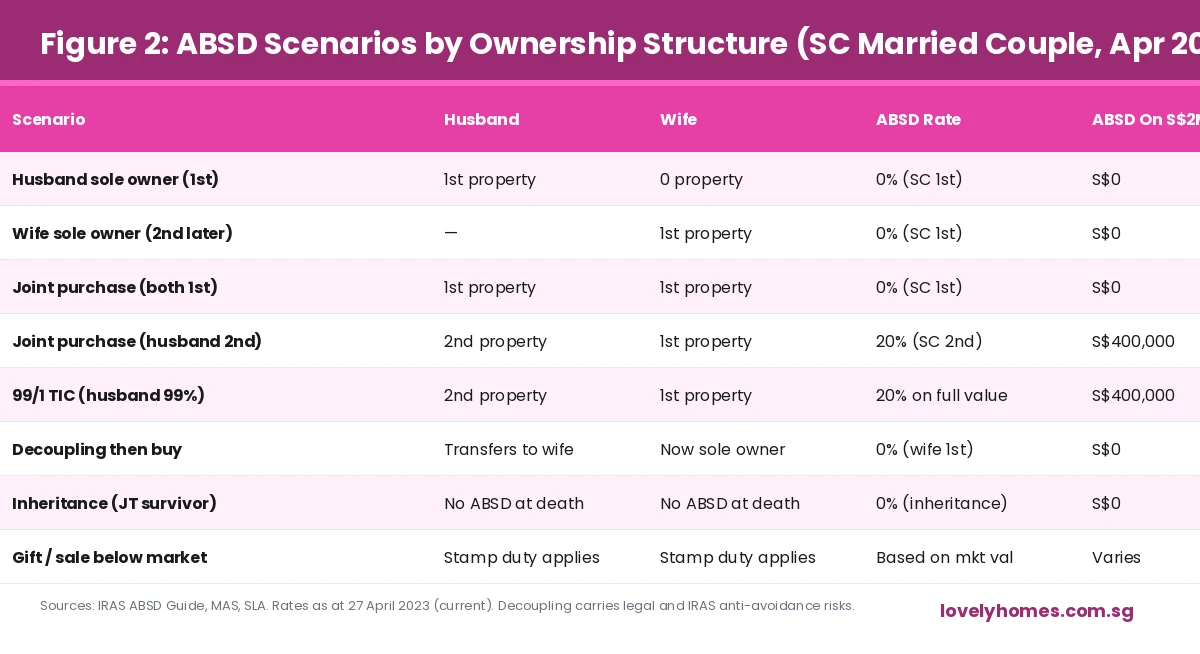

When two or more people purchase a property together in Singapore, they must choose between two legal ownership structures: Joint Tenancy (JT) or Tenancy in Common (TIC). This choice has significant consequences for estate planning, ABSD exposure, CPF usage, and how the property is inherited on the death of one owner. It is also at the centre of several controversial IRAS-flagged property structuring strategies, including the now-notorious “99-to-1” arrangement that attracted an anti-avoidance warning in April 2023. This guide explains each structure clearly, with worked ABSD scenarios and estate-planning implications for Singapore buyers in 2026.

Quick Answer — Key Takeaways

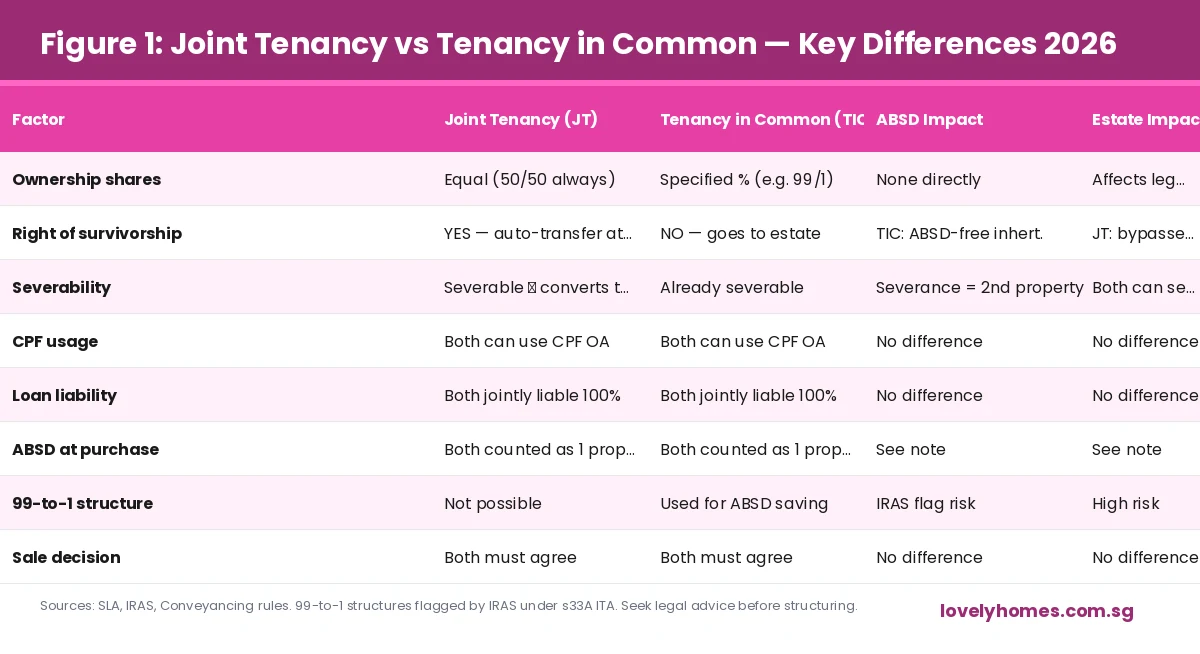

Joint Tenancy (JT): Both owners hold equal undivided shares. On death, the surviving owner automatically inherits the deceased’s share by the right of survivorship — bypassing probate. Commonly used by married couples for matrimonial homes.

Tenancy in Common (TIC): Owners hold specified percentage shares (e.g. 60/40, 99/1). Each owner’s share forms part of their estate on death and is distributed per their will or intestacy laws. More flexible but requires careful estate planning.

ABSD risk for TIC: The IRAS has flagged TIC structures (especially 99/1 and 1/99) as potentially falling within the anti-avoidance provisions of Section 33A of the Income Tax Act if the primary purpose is ABSD avoidance. Seek legal advice before using TIC for tax-saving purposes.

You can convert: A JT can be severed (converted to TIC) by any one owner’s unilateral act of severance. Conversely, TIC owners can merge their interests into a JT by mutual agreement.

CPF usage: Both JT and TIC allow CPF OA usage for the property purchase, subject to the CPF Withdrawal Limit. CPF accrued interest is charged on the amount withdrawn and must be refunded on sale.

Decoupling: TIC is the starting structure for a decoupling exercise, where one co-owner sells their share to the other — but this has ABSD and legal risks. See our decoupling guide for the full analysis.

What Is Joint Tenancy in Singapore?

Joint Tenancy (JT) is an ownership structure in which two or more co-owners hold a property collectively without any specified individual share. Each joint tenant holds an undivided interest in the entire property — not a 50% slice, but a whole-of-property interest held simultaneously with the other joint tenants. The four unities of Joint Tenancy must be present: unity of time (same time of acquisition), unity of title (same instrument of transfer), unity of interest (equal shares), and unity of possession (equal right to possess the whole property).

The defining feature of Joint Tenancy is the right of survivorship (jus accrescendi). On the death of one joint tenant, their interest in the property automatically passes to the surviving joint tenant(s) — regardless of what the deceased’s will says. The property does not form part of the deceased’s estate and does not go through probate. This makes JT the preferred structure for married couples who want a simple, automatic estate outcome without the complexity and delay of probate proceedings.

What Is Tenancy in Common in Singapore?

Tenancy in Common (TIC) is an ownership structure in which co-owners hold specified, separate shares of the property. Unlike JT, TIC owners do not hold the property collectively — each holds a defined percentage (e.g. 70% / 30%, or 99% / 1%) that can be independently dealt with, mortgaged, or bequeathed. Only unity of possession is required — TIC owners need not have acquired the property at the same time or under the same instrument.

On the death of a TIC owner, their share does not pass automatically to the other co-owner(s). Instead, it becomes part of the deceased’s estate and is distributed according to their will (or under the Intestate Succession Act if there is no will). This means TIC ownership requires more deliberate estate planning — but it also provides greater flexibility for owners with different estate objectives, different financial contributions to the purchase, or different intended inheritance outcomes.

Figure 1: Joint Tenancy vs Tenancy in Common — Key Differences, Singapore 2026. Sources: SLA, IRAS, Conveyancing Law. Indicative only — seek legal advice for your specific situation.

ABSD and Ownership Structure — The Critical Interaction

The most important practical difference between JT and TIC for Singapore property buyers in 2026 is how each structure interacts with Additional Buyer’s Stamp Duty (ABSD). ABSD is calculated based on the higher of the two co-buyers’ property count. If a Singapore Citizen (SC) husband who already owns a property buys with his SC wife who has no property, the purchase is treated as a “second property” for ABSD purposes — attracting 20% ABSD on the full purchase price — regardless of whether they use JT or TIC.

The ABSD rules were deliberately designed to prevent ownership structuring from being used as an ABSD avoidance mechanism. A 99/1 TIC arrangement — where the husband holds 1% and the wife holds 99%, ostensibly making the wife the “primary” owner — does not reduce the ABSD payable. IRAS applies ABSD based on each buyer’s property count. If the husband (with existing property) is on the title at all, the purchase is assessed at his higher ABSD rate on the full market value. The IRAS also has Section 33A anti-avoidance powers that can be invoked where an arrangement’s primary purpose is ABSD avoidance — potentially leading to reassessment, penalties, and interest.

Figure 2: ABSD Scenarios by Ownership Structure — SC Married Couple, April 2026. Sources: IRAS ABSD Guide, MAS. Rates as at 27 April 2023 (current). Illustrative only — seek professional advice before structuring.

Summary: Key Differences at a Glance

Dimension

Joint Tenancy

Tenancy in Common

Individual share specified?

No — equal undivided interest

Yes — e.g. 70/30, 99/1

Right of survivorship?

Yes — auto-passes on death

No — goes to estate

Can be bequeathed in will?

No (survivorship overrides will)

Yes

Probate required on death?

No

Yes (for the deceased’s share)

ABSD treatment

Higher count of any co-owner applies

Higher count of any co-owner applies

Convertible to the other?

Yes — by severance (any 1 owner)

Yes — by agreement (all owners)

Typical use

Matrimonial home, equal-share investment

Unequal contributions, estate planning

Decoupling suitability

Must sever to TIC first

Directly usable (with risks)

Worked Example: Estate Planning with TIC vs JT

Scenario: Mr Tan (60%) and Mrs Tan (40%) own a S$3M condo in TIC

Mr Tan passes away (no will)His 60% share → estate

Under Intestate Succession Act (married, 2 adult children)Wife gets 50% of 60% = 30%; children share remaining 30%

Mrs Tan now owns40% (original) + 30% (inheritance) = 70%

Each child now owns15% of the condo

Children’s ABSD position if they buy their own propertyThey “own” 15% — counts as a property for ABSD

If JT had been used insteadMrs Tan inherits 100% automatically. Children inherit nothing.

Key lessonTIC requires a carefully drafted will to avoid unintended outcomes

How to Convert Between Joint Tenancy and Tenancy in Common

Converting from Joint Tenancy to Tenancy in Common (severance) can be done unilaterally by any one joint tenant — it does not require the consent of the other co-owner(s). A joint tenant serves written notice of severance on the other co-owner(s), and a declaration is registered with the Singapore Land Authority (SLA). Upon registration, the JT converts to a TIC in equal shares (e.g. 50/50 for two former joint tenants). If the severing party wants unequal shares, they must transfer the relevant portion of their interest to the other co-owner — which may attract stamp duty and ABSD if the recipient thereby “acquires” an additional property interest.

Converting from Tenancy in Common back to Joint Tenancy requires the agreement of all co-owners and the re-execution of a transfer instrument, registered with SLA. The four unities must be re-established. This is less common but may be appropriate when co-owners who originally split their shares for estate planning purposes later want to consolidate for simplicity.

The 99-to-1 Structure and IRAS Anti-Avoidance

The “99-to-1” or “1-to-99” TIC structure gained notoriety in Singapore around 2021–2022 as a mechanism purportedly used by married couples to reduce ABSD. The arrangement involves one spouse (who already owns a property) purchasing just 1% of a new property, while the other spouse (who owns nothing) purchases 99%. The intended logic was that the 99% owner — being a “first-time buyer” — would attract 0% ABSD on their 99% share, with only 1% of the value attracting the higher ABSD rate.

IRAS expressly addressed this in April 2023, clarifying that ABSD applies to the full value of the property for each buyer, based on the buyer’s property count — not proportionate to their ownership share. A husband who buys even 1% of a property where he already owns another property is treated as a “second property” buyer on the full purchase price. Additionally, IRAS warned that 99-to-1 arrangements could be subject to the general anti-avoidance provision in Section 33A of the Income Tax Act, which empowers IRAS to disregard or reconstruct transactions that are not entered into for bona fide commercial reasons, or that are primarily for the purpose of obtaining a tax advantage. Buyers who have entered into such arrangements are advised to seek a legal opinion on their exposure.

What This Means for You in 2026

For most married couples buying their first home together, Joint Tenancy remains the simpler and more appropriate structure. The right of survivorship provides automatic estate protection without the cost or complexity of probate, and the equal share assumption aligns with the typical matrimonial home context. For investors, business partners, or co-owners with meaningfully different financial contributions or different estate objectives, Tenancy in Common with a clearly drafted will is the more appropriate structure — but it requires professional legal advice to ensure the intended outcome.

The ABSD landscape of 2026 has made property ownership structuring significantly more fraught. The 60% ABSD on foreign purchases, the 20% on SC second properties, and IRAS’s active anti-avoidance posture mean that creative structuring carries real legal risk. The safest path is to engage a conveyancing solicitor and a property tax advisor before executing any co-ownership arrangement, particularly where one of the buyers already holds a residential property.

What Might Come Next

There is ongoing industry discussion about whether Singapore’s ABSD regime will be relaxed for specific categories — particularly the 60% foreign-buyer rate, which has significantly reduced CCR transaction volumes since 2023. Any reduction in foreign ABSD could trigger a wave of CCR resale activity, changing the dynamics for TIC investors who hold CCR properties jointly with foreign spouses. On the estate-planning side, Singapore does not currently impose inheritance tax or estate duty (abolished in 2008) — meaning TIC inheritance of property is tax-free. Should Singapore ever reintroduce estate duty as part of a broader fiscal package, TIC structures with careful will-drafting could become even more strategically important.

Can a husband and wife hold a property in different ownership structures for different properties?

Yes. Each property is a separate legal transaction. A married couple can hold their matrimonial home under Joint Tenancy while holding an investment property under Tenancy in Common (with different specified shares). The ownership structure for each property is chosen independently at the time of purchase and can be changed subsequently through the appropriate legal processes (severance for JT→TIC, or mutual transfer for TIC→JT).

Does Tenancy in Common affect the CPF usage rules?

No. Both Joint Tenancy and Tenancy in Common allow each co-owner to use their CPF Ordinary Account (OA) savings for the property purchase, subject to the CPF Withdrawal Limit and Valuation Limit. In a TIC arrangement, each owner’s CPF contribution is typically proportionate to their ownership share — though the CPF Board does not strictly enforce this proportionality. On sale, each owner must refund their own CPF OA withdrawals plus accrued interest (at 2.5% per annum) from their respective sale proceeds.

Can a foreigner co-own a Singapore private condo as a Tenancy in Common co-owner?

Yes. Foreign nationals can co-own Singapore private condominiums (not landed property or HDB flats) under either Joint Tenancy or Tenancy in Common. A foreigner co-owner will attract the 60% ABSD on their proportionate share of the purchase price. In a 50/50 TIC with a foreigner, ABSD applies at 0% for the SC co-owner’s 50% (assuming first property) and 60% for the foreigner’s 50% — resulting in a blended ABSD rate of 30% on the full purchase price. This is significantly lower than a sole foreigner purchase at 60% but still a substantial cost.

What happens to a joint tenancy when the parties divorce?

Divorce does not automatically sever a Joint Tenancy. The JT continues in force until the Family Court issues an ancillary order dealing with the matrimonial property, or until one party serves a notice of severance. In practice, the Family Court’s ancillary order will typically either direct the sale of the property (with proceeds distributed as ordered) or award the property to one spouse with a transfer obligation. Once the Family Court order is made, the property is usually transferred to sole ownership or sold, effectively terminating the JT. During the divorce proceedings, neither party can unilaterally sell the property without the other’s consent or a court order.

Is there stamp duty payable when converting from Joint Tenancy to Tenancy in Common?

Severance of a Joint Tenancy (converting from JT to TIC in equal shares) does not involve a transfer of ownership and generally does not attract stamp duty, as no beneficial interest changes hands. However, if the severance results in unequal shares (e.g. one co-owner transferring 10% of their interest to the other), Buyer’s Stamp Duty (BSD) and potentially ABSD will apply to the transferred portion. For example, if the recipient already owns a property, ABSD at the applicable rate applies to the market value of the interest transferred. This is a key consideration in decoupling structures. See our decoupling guide for the full analysis.

Can I leave my Tenancy in Common share to anyone I choose in my will?

Yes, subject to Singapore’s intestacy and family provision laws. A TIC owner can bequeath their share to any person — family member, friend, charity, or trust — provided they have a valid, witnessed will. Singapore does not currently have forced heirship rules (unlike some civil law jurisdictions), so a TIC owner has broad testamentary freedom over their property share. However, the Inheritance (Family Provision) Act allows certain family members (spouses, children) to apply to court for a greater share of the estate if the will does not adequately provide for them. Executors should seek legal advice when a TIC property forms a significant part of the estate.

DISCLAIMER: All information in this article is for general informational and educational purposes only and does not constitute legal, tax, or financial advice. Ownership structuring decisions have significant stamp duty, estate, and legal implications. The IRAS anti-avoidance provisions under Section 33A of the Income Tax Act can apply to arrangements entered into for the purpose of obtaining a tax advantage. Readers should consult a qualified conveyancing solicitor and a property tax advisor before making any ownership structuring decisions. LovelyHomes.com.sg is an independent editorial platform. Refer to official sources: IRAS (iras.gov.sg), SLA (sla.gov.sg), CPF Board (cpf.gov.sg), Ministry of Law (mlaw.gov.sg).

For most Singaporeans, the home loan is the largest financial commitment of their lives — and in a market where private condo prices now range from S$1.2 million to S$4 million and beyond, getting the loan structure right can save (or cost) hundreds of thousands of dollars over a 25–30 year mortgage. This guide covers everything you need to know about home loans in Singapore in 2026: how much you can borrow, what the rates look like, how to compare packages, and how to build the strongest possible loan application.

Quick Answer — Singapore Home Loan Basics 2026

Maximum LTV: 75% for first private property (5% cash + 20% CPF/cash); 45% if holding an existing property

TDSR cap: Total monthly debt repayments cannot exceed 55% of gross monthly income

Typical fixed rates (2026): 2.5%–3.5% p.a. for 2–3 year lock-in packages

SORA benchmark: 3-month SORA fluctuates; total SORA-linked rate approximately 3.3%–3.8% in April 2026

Maximum loan tenure: 30 years (or limited so borrower does not exceed age 65 at loan end)

IPA (In-Principle Approval): Obtain before visiting any showflat — it defines your budget precisely

Singapore Home Loan Key Parameters 2026

Private residential properties — framework in force as at 24 April 2026

55% of gross monthly income — all debt obligations

Mortgage Servicing Ratio (MSR)

30% of gross income — applies to HDB and EC loans only

Stress Test Rate

Typically 4% p.a. or prevailing rate + 2%, whichever is higher

Typical Fixed Rate (2026)

~2.5%–3.5% p.a. (3-year package) — compare across banks

Typical SORA-linked (2026)

3M SORA + spread (~0.7%–0.9%); total ~3.3%–3.8% p.a.

Max Loan Tenure

30 years (private); 25 years if borrower age at end of tenure >65

Source: MAS Regulations + MND / bank rate surveys — 24 April 2026

lovelyhomes.com.sg

How Much Can You Borrow? LTV, TDSR, and Stress Tests Explained

Your maximum home loan in Singapore is determined by three overlapping constraints. The most restrictive of the three sets your actual limit.

1. Loan-to-Value (LTV): For a private property loan from a bank, the LTV ceiling is 75% of the purchase price or market value (whichever is lower) for buyers with no outstanding property loans. This means a maximum loan of S$1.387 million on a S$1.85 million purchase. If you hold an existing property loan (e.g., you are buying a second property before selling the first), the LTV drops sharply to 45%, requiring a 55% down payment. These LTV rules are set by MAS and apply uniformly across all banks.

2. Total Debt Servicing Ratio (TDSR): Your total monthly repayments across all debts — home loan, car loan, personal loan, credit card minimum payment, student loan — must not exceed 55% of your gross monthly income. Banks assess TDSR at a stress-tested rate (the higher of 4% p.a. or the prevailing rate plus 2%) to ensure your repayment capacity holds under adverse rate conditions. A joint applicant’s income can be combined; however, guarantors’ income typically cannot be included for TDSR purposes.

3. Loan Tenure Cap: Banks impose a maximum tenure of 30 years, subject to the borrower not exceeding age 65 at loan maturity. A 45-year-old borrower is therefore limited to a 20-year tenure; a 35-year-old can take the full 30 years. Shorter tenure = higher monthly instalment but lower total interest paid. Longer tenure = lower monthly instalment but significantly higher total interest cost over the life of the loan.

Down Payment: What You Need in Cash vs CPF

At 75% LTV, the required down payment is 25% of the purchase price. Of this 25%, at least 5% must be in cash (hard cash — not CPF, not bank loan). The remaining 20% can be funded from any combination of cash and CPF Ordinary Account (OA) savings. This means a buyer purchasing a S$2 million condo must have at least S$100,000 in cash available on the day of OTP exercise, plus access to S$400,000 in additional cash and/or CPF OA for the remaining down payment component.

For upgraders who have just sold an HDB, the CPF OA refund (principal + accrued interest) can provide a significant top-up — in many cases, several hundred thousand dollars — making the 20% non-cash component relatively manageable. The critical cash requirement is the minimum 5%.

Fixed Rate vs SORA-Linked: Which Package is Right for You?

The Singapore Overnight Rate Average (SORA) replaced SIBOR as the benchmark rate for floating-rate home loans from 2021 onwards. As of April 2026, the 3-month compounded SORA sits in the range of approximately 2.5%–3.0%, with bank spreads of 0.7%–0.9%, producing effective all-in SORA-linked rates of approximately 3.3%–3.8% per annum. Fixed-rate packages for 2–3 year lock-in periods are broadly competitive at 2.5%–3.5% p.a. depending on the bank and loan quantum.

Fixed Rate vs SORA-Floating — When Each Makes Sense

Package Type

Rate Profile

Best For

Key Risk

Fixed Rate (2–3 yr lock-in)

Rate fixed for 2–3 yrs, then reverts to board/SORA

Buyers who want payment certainty; rate rising environment

Early repayment penalty during lock-in

SORA Floating

Rate moves monthly with 3-month SORA + spread

Buyers expecting rates to fall; short hold period

Payment volatility; budgeting harder

Fixed + SORA Hybrid

First 2 yrs fixed, then SORA

Hedge approach; balance of certainty and flexibility

Transition risk if SORA spikes after lock-in expires

HDB Concessionary Loan (HDB only)

2.6% p.a. flat (CPF OA rate + 0.1%); 80% LTV

HDB flat buyers; first-timers with limited cash

Only for HDB flats; not available for private property

Key Takeaway

As at April 2026, fixed rates are broadly competitive with SORA-linked packages. Buyers planning a >5-year hold with stable income generally benefit from a 2-year fixed package for predictability, then re-finance at the end of the lock-in.

Source: MAS / bank surveys — April 2026

lovelyhomes.com.sg

Worked Example — S$1.85m New Launch Purchase

The following illustrates the full upfront financial requirement for a Singapore Citizen couple buying their first private property (a new launch condo at S$1.85 million) after selling their HDB flat.

Worked Example — S$1.85m New Launch Condo Purchase (SC, First Property)

Item

Amount

Basis

Purchase Price

S$1,850,000

New launch indicative price

Down Payment (25%)

S$462,500

5% cash (S$92,500) + 20% CPF/cash (S$370,000)

Buyer’s Stamp Duty (BSD)

~S$62,100

Progressive BSD table; paid in cash within 14 days of OTP

ABSD (SC 1st property)

S$0

0% for Singapore Citizen first purchase

Loan Amount (75% LTV)

S$1,387,500

Subject to TDSR and stress test

Monthly Instalment (3% fixed, 30 yr)

~S$5,849/month

Estimated; varies by bank and package

TDSR threshold (55% rule)

Monthly income ≥ S$10,635 (combined, all debts)

To support the above instalment with zero other debt

Legal / Conveyancing (est.)

~S$3,500–S$5,000

One-time cost; varies by law firm

Total Upfront Cash Required

~S$100,000–S$110,000

5% cash down + BSD + legal (CPF funds balance)

Key Takeaway

A Singapore Citizen couple with a combined gross monthly income of S$12,000 can comfortably qualify for a S$1.387 million home loan on a S$1.85 million first property, using CPF OA for the 20% non-cash component of the down payment.

Source: IRAS + MAS + Bank estimates — 24 April 2026

lovelyhomes.com.sg

How to Secure the Best Home Loan: A Step-by-Step Approach

1. Pull your credit report: Before approaching any bank, request your credit report from Credit Bureau Singapore (CBS). A credit score above 1,844 (AA or BB grade) gives you the strongest negotiating position. Clear any outstanding small debts that may drag down your score.

2. Compile your income documents: The standard package is your most recent 3 months’ payslips, latest CPF contribution history statement (12 months), Notice of Assessment (NOA) for the past 2 years, and your NRIC. Self-employed buyers need their NOA for 2 years plus certified management accounts or bank statements. Commission-based earners typically have their variable income haircut by 30% for TDSR calculation.

3. Obtain IPAs from at least 3 banks: Compare the IPA quantum, the indicative rate offered, and the lock-in terms. Banks compete actively for quality home loan customers; do not accept the first offer. Use a mortgage broker if you prefer to have the comparison done for you, but be aware they receive referral fees and may not compare all available options.

4. Read the fine print on lock-in periods and clawback: Most competitive fixed-rate packages have a 2–3 year lock-in during which early redemption triggers a penalty (typically 1.5% of the outstanding loan). Check also for legal fee subsidies, valuation fee waivers, and free conversion clauses — these can save S$3,000–S$8,000 in the first year and are worth negotiating.

5. Consider a mortgage offset account: Some banks offer a 100% offset account facility that links your current account balance to your mortgage principal. Funds parked in this account reduce your effective interest cost dollar for dollar. This is particularly valuable for buyers who accumulate savings quickly or receive occasional large bonuses.

Using CPF for Your Home Loan

Your CPF Ordinary Account can be used to fund (a) the initial down payment (the non-cash component of the 25%), (b) the BSD, (c) monthly mortgage instalments up to the Valuation Limit, and (d) legal fees. The key rule is the CPF Usage Limit for private property:

If the property’s remaining lease covers the youngest buyer to age 95, full CPF usage is permitted up to the property’s Valuation Limit.

If the remaining lease does NOT cover the youngest buyer to age 95 but covers at least 60 years, CPF usage is capped pro-rata.

If the remaining lease is less than 30 years, CPF cannot be used at all.

For new launch condos (99-year leasehold, purchased in 2026), the lease will comfortably cover the youngest buyer to age 95 in the vast majority of cases, so full CPF usage is available. Remember: when you sell the property, all CPF monies drawn must be returned to your OA with accrued interest — this is not optional and is enforced automatically by the CPF Board upon completion of sale.

Frequently Asked Questions

Can I take a loan from HDB and a bank simultaneously?

No. The HDB concessionary loan (2.6% p.a., 80% LTV) is available only for HDB flats. Private property purchases must use a bank loan. You cannot hold an HDB loan and a bank mortgage on a private property simultaneously; the two loan types are for distinct property classes.

How does SORA work for home loans?

The Singapore Overnight Rate Average (SORA) is published daily by MAS and represents the weighted average overnight unsecured borrowing rate among banks. Most banks use the 3-month compounded SORA (3M Compounded SORA), which is smoothed and less volatile than the daily rate. Your mortgage rate = 3M Compounded SORA + bank spread. Both components change over time; your monthly instalment adjusts accordingly, typically quarterly. Check the MAS SORA statistics page for the latest published rate.

What is the stress test rate and why does it matter?

Banks assess your TDSR at the higher of (a) 4% p.a. or (b) the prevailing rate plus a 2% buffer. This “stress test rate” is typically higher than the actual rate you will pay, so the loan amount you are approved for is lower than what you could technically service at today’s market rate. This is a deliberate prudential measure to ensure borrowers can still service the loan if rates rise significantly.

Can I refinance during the lock-in period?

You can, but you will typically incur an early redemption penalty of 0.75%–1.5% of the outstanding loan balance. After the lock-in period expires, you are free to re-price (switch to a new package with the same bank) or refinance (move to a different bank) without penalty. Most active mortgage managers review their loan package at the end of every lock-in period.

Does a larger down payment lead to a better rate?

Not directly in Singapore’s home loan market. Unlike some markets where LTV directly influences the mortgage rate, Singapore banks generally offer the same rate bands across LTV ranges (within the MAS limit). However, a larger down payment reduces your loan quantum, which may bring you within a bank’s “premium package” tier (typically loans above S$1.5 million attract slightly different product options). Focus more on the total-cost comparison between packages than on trying to optimise the down payment size for rate purposes.

Disclaimer: All information in this article is for general educational purposes only and does not constitute financial, legal, or mortgage advice. Loan rates, LTV limits, CPF rules, and MAS regulations are subject to change. Always obtain a personalised In-Principle Approval from a licensed bank and consult a licensed financial adviser before committing to any home loan. Interest rates quoted are indicative as at April 2026 and will vary by bank, product, and applicant profile.

Singapore Overnight Rate Average (SORA) — the benchmark that replaced the retired SIBOR in 2024 — has held steady in the 2.85-3.00% band through the first four months of 2026. Floating-rate mortgages pegged to 3-month compounded SORA are pricing at all-in rates around 3.65-3.75% for private condo borrowers, and 3.55-3.65% for HDB borrowers. For anyone weighing a new purchase or a refinance, the April snapshot is the cleanest read of the market since 3M SORA peaked near 3.8% in late 2023.

Private condo floating (SORA+0.75%)bps 370

HDB floating (SORA+0.70%)bps 365

3-month compounded SORAbps 295

Overnight SORA (spot)bps 290

MAS S$-NEER policy bandbps 285

US 10-year Treasury (reference)bps 385

lovelyhomes.com.sgSource: MAS data; bank published rates — April 2026

Where we are

The three-month compounded SORA index stood at 2.95% on 21 April 2026, unchanged from the previous week and inside the narrow trading band of the past two quarters. SORA has declined roughly 85 basis points from its cycle peak in mid-2023 (3.82% on 5 September 2023) but the pace of decline has slowed materially since Q3 2025. The Monetary Authority of Singapore (MAS) has not adjusted its policy stance since October 2023; the S$-NEER policy band remains on an appreciation bias, with unchanged slope and width.

Bank spreads above SORA have narrowed modestly over the past six months. Major local banks are quoting SORA+0.70% to SORA+0.85% on private condo floating-rate loans, down from SORA+0.85% to SORA+1.00% at the start of 2025. The competitive pressure stems from the slower mortgage-book growth banks are seeing (a function of the moderating new-launch volume) — they are fighting harder for each customer.

Fixed-rate alternatives

Two-year and three-year fixed packages have converged with floating pricing. As of mid-April, representative fixed rates are 3.45-3.65% for 2-year fixes and 3.55-3.75% for 3-year fixes. The fixed-to-floating spread, historically 20-40 basis points in favour of fixed when rates were expected to fall, has compressed to zero or even inverted. Borrowers are being offered comparable rates to lock in versus float, reflecting bank expectations that 3M SORA is near the bottom of this cycle.

Fixed vs floating — April 2026

For a new purchase, the choice between fixed and floating is less about betting on rate direction and more about matching your own risk tolerance. Fixed gives cashflow certainty for 2-3 years at essentially the same rate as floating. Floating carries the optionality — if SORA breaks below 2.5% (unlikely absent a major economic shock), monthly instalments fall immediately.

Refinancing

The refinancing window is genuinely open. Borrowers on legacy fixed packages that were priced at 4.0-4.3% during 2023-24 can refinance today to 3.45-3.65% fixed — a 55-85 basis-point saving. On a S$1.0m outstanding balance at a 25-year remaining tenure, a 70 basis-point drop saves approximately S$435 a month in interest, or S$5,220 a year. Net of the S$2,000-3,000 legal and valuation costs of refinancing, the breakeven is inside 8 months.

The tighter TDSR framework applies at refinancing. Your TDSR must still fit within 55% of gross monthly income at the new rate. For investment property, the rental-income haircut (70% of assessed rent) remains in force. Borrowers who have changed employment or whose income has dipped may find the refinancing window narrower than the savings optics suggest; arrange the refinancing conversation with the bank before the lock-in period expires so a renegotiation of terms is an option if TDSR is tight.

HDB loans — HDB concessionary vs bank

HDB concessionary loans remain at 2.60% — the floor of 0.1 percentage point above the CPF Ordinary Account interest rate. Bank HDB loans at SORA-based floating are pricing at 3.55-3.65%, making the HDB loan meaningfully cheaper on a coupon basis. But the eligibility rules remain restrictive: HDB concessionary requires at least one Singapore-citizen buyer, gross monthly household income ceilings of S$14,000 (couple) or S$21,000 (multi-generation), and the household must not own or have owned more than one other property in the last 30 months.

For eligible first-time HDB BTO buyers, HDB concessionary is the default choice — 90 basis points below bank HDB, with the added option to use the HDB Home Protection Scheme (HPS) at concessionary rates. For HDB resale buyers who have outgrown eligibility, bank floating is typically the cheaper route, especially with 2-year fixed packages pricing around 3.45%.

What the MAS signal tells us

MAS’s April 2026 Monetary Policy Statement reiterated the existing stance — S$-NEER appreciation bias maintained, slope and band width unchanged. The statement noted ‘core inflation easing broadly in line with projections’ and ‘the domestic economy expanding at a moderate pace’. No forward guidance was provided. In practice, this means the MAS is watching the same data as the market, and rate volatility is likely to be lower over the next two quarters than it was during the 2023 rate-cycle peak.

The read-across for the mortgage market: 3M SORA is likely to stay in a 2.80-3.10% range through the middle of 2026 unless the US Federal Reserve moves aggressively in either direction. Bank spreads may compress another 5-10 basis points if loan-book growth continues to be sluggish. All-in mortgage rates of 3.60-3.75% are the reasonable planning assumption for a new purchase today.

Three practical moves

If you are buying: the competitive tension between banks is real. Obtain at least three written indicative offers before committing to a loan. Ask for spread (not just headline rate), lock-in period, prepayment penalties and free-conversion clauses. A free-conversion clause after the second year is worth 5-10 basis points against the lowest headline rate.

If you are refinancing: start 4 months before your lock-in ends. Most legacy packages allow a ‘repricing’ with the existing bank 3 months before lock-in ends — use the competing offers from other banks to negotiate a sharper repricing without the legal costs of a full refinance. Savings can land at 80-90% of a full-refinance move with 0% of the hassle.

If you are on a floating-rate loan and considering a fixed: model the break-even by comparing a 24-month sum of current floating payments versus 24 months at the fixed rate, plus the fixed-conversion fee. If the break-even is inside 12 months and you value cashflow certainty, move. If the break-even is further out, the optionality of staying floating is worth more than the spread.

Bottom line

Mortgage rates in April 2026 look settled. Floating at 3.60-3.75%, fixed at 3.45-3.65%, HDB concessionary at 2.60%. The refinancing economics are meaningful for anyone locked into a 2023-vintage fixed package above 4%. For new purchases, run your TDSR at the regulatory stress-test rate of 4.00%, not at the headline rate offered — the same rate banks test your loan against. That way, if rates unexpectedly rise, your cashflow buffer is intact.

Sources: Monetary Authority of Singapore (MAS) SORA daily fix (https://www.mas.gov.sg/); bank published rate sheets for DBS, UOB, OCBC, Maybank and StanChart — April 2026. This article is editorial commentary produced by the LovelyHomes team and does not constitute investment or financial advice. Rates, indices and figures are current as at the date of publication. Buyers and investors should consult a licensed professional before making a property-related decision.