Rental Yield vs Capital Gain Singapore 2026: The Property Investor’s Decision Framework

Quick Answer: Rental Yield or Capital Gain?

- Rental yield measures annual rental income as a percentage of property value. Gross yields in Singapore range from roughly 2.2% (landed, CCR) to 5.0% (OCR condos, non-mature HDB). Net yield after tax, maintenance, and vacancy is typically 1–1.5 percentage points lower.

- Capital gain is the appreciation in property value over the holding period. Singapore private residential prices rose roughly 30% between 2020 and 2022, but growth has moderated to 1–3% per annum post-cooling measures.

- At current mortgage rates of ~3.5–4.2% per annum (SORA-pegged and fixed), most Singapore investment properties produce neutral to negative cash flow — the investor is effectively subsidising the mortgage in exchange for capital appreciation.

- HDB flats as investment properties produce the highest net yields (4–5%) but are subject to owner-occupier rules — you cannot buy an HDB resale flat purely as an investment while owning other property.

- The correct choice depends on your liquidity needs, tax position, holding period, and leverage tolerance.

- The 60% ABSD on foreigners and 20% on Singapore Permanent Residents for second property purchases fundamentally reshape yield maths for those cohorts.

- A Singapore Citizen paying 20% ABSD on a second property raises the effective entry cost by S$300,000 on a S$1.5M condo — requiring a higher yield or longer hold to break even.

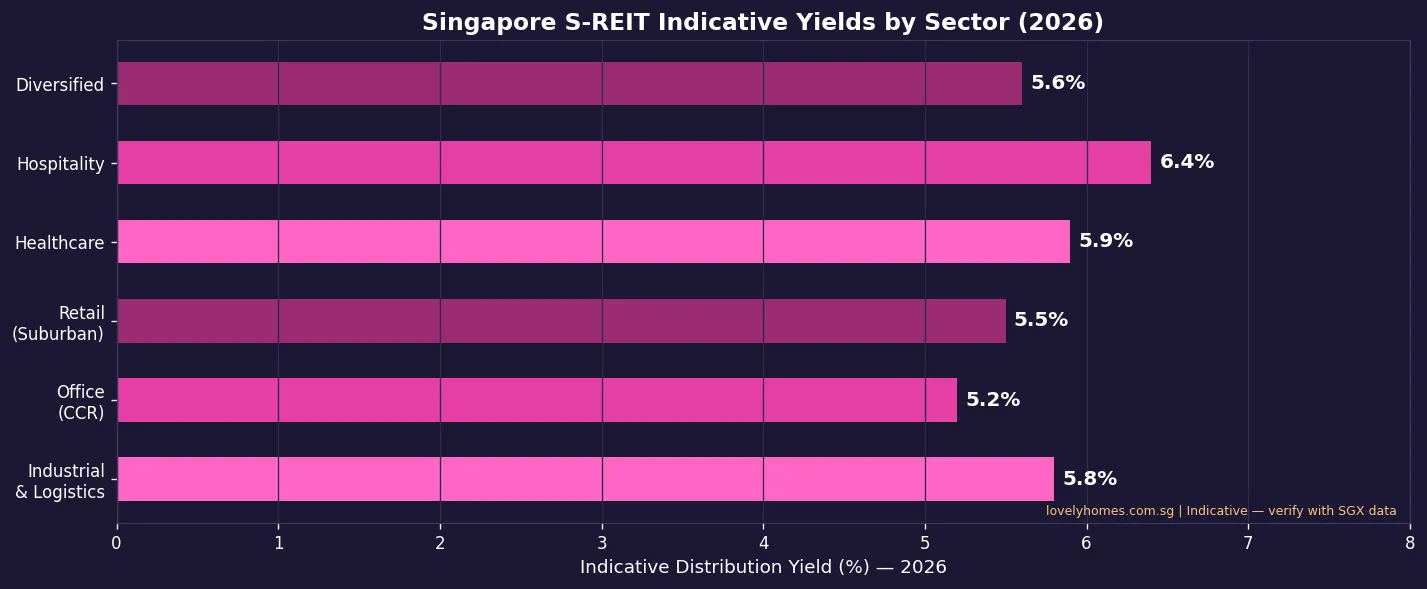

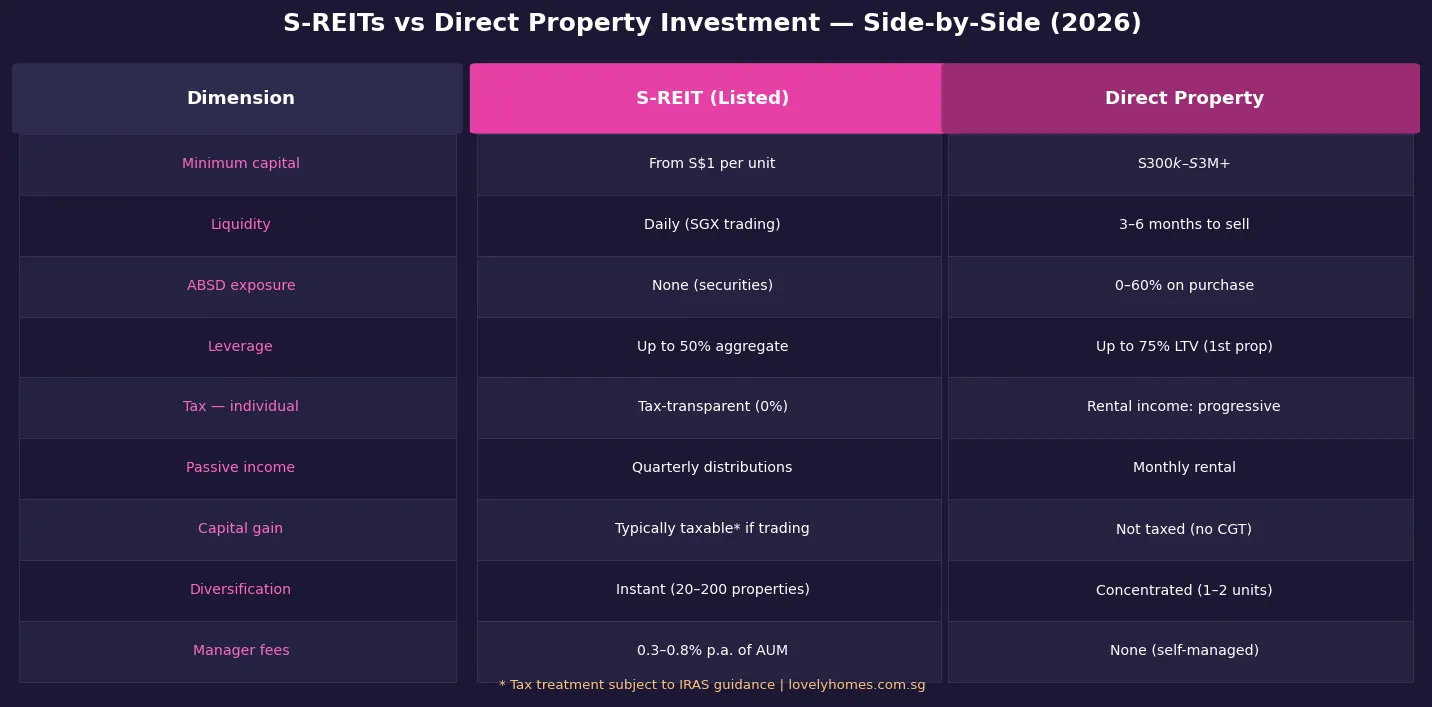

- Diversification into Singapore REITs offers yield exposure with no ABSD, no management burden, and far lower minimum capital.

Understanding Rental Yield: Gross vs Net

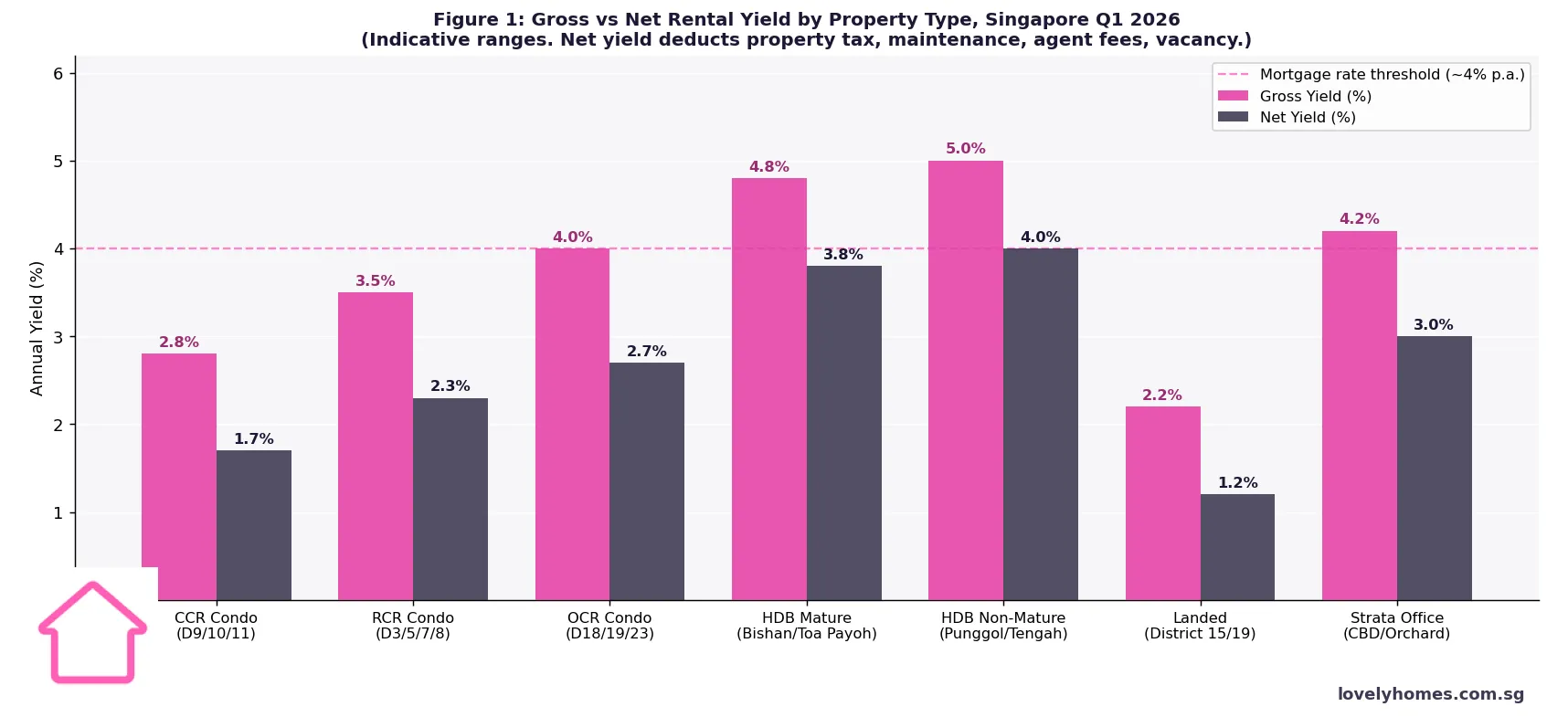

Rental yield is the simplest metric for property investors — it tells you how much income the property generates relative to its cost. However, the headline gross yield figure can mislead. Gross yield divides annual rental income by the property price. Net yield, which is far more meaningful, deducts all recurring ownership costs: property tax (at the non-owner-occupier rate), maintenance fees, agent commissions and vacancy allowance, insurance, and any management costs.

In Singapore’s high-tax environment for investment properties, the gap between gross and net yield is substantial. Investment-rate property tax for a non-owner-occupied residential unit is assessed on the Annual Value (AV) — which the Inland Revenue Authority of Singapore (IRAS) estimates at market rent — at rates of 11% on the first S$30,000 AV and up to 27% on AV above S$90,000 (effective 2024). This alone can reduce your gross yield by 0.8–1.2 percentage points. See our guide to capital gains and rental income tax for the full deduction analysis.

The yield picture in Q1 2026 tells a clear story. OCR condominiums and non-mature HDB flats offer the most attractive net yields (2.7–4.0%) for Singapore Citizen investors who own no other residential property. CCR condominiums, where purchase prices have risen fastest, show compressed net yields of 1.7% — well below the prevailing mortgage rate of 3.5–4.2%. A CCR investor at current prices is implicitly betting on capital appreciation rather than income.

The mortgage-rate threshold line on Figure 1 is critical: any property with a net yield below the investor’s mortgage rate produces negative cash flow. The investor’s equity is being drawn down each month until either (a) rental rates rise, (b) the mortgage is refinanced to a lower rate, or (c) the property is sold. For most CCR and landed investments at current prices, this is the reality.

Understanding Capital Gain: The Singapore Track Record

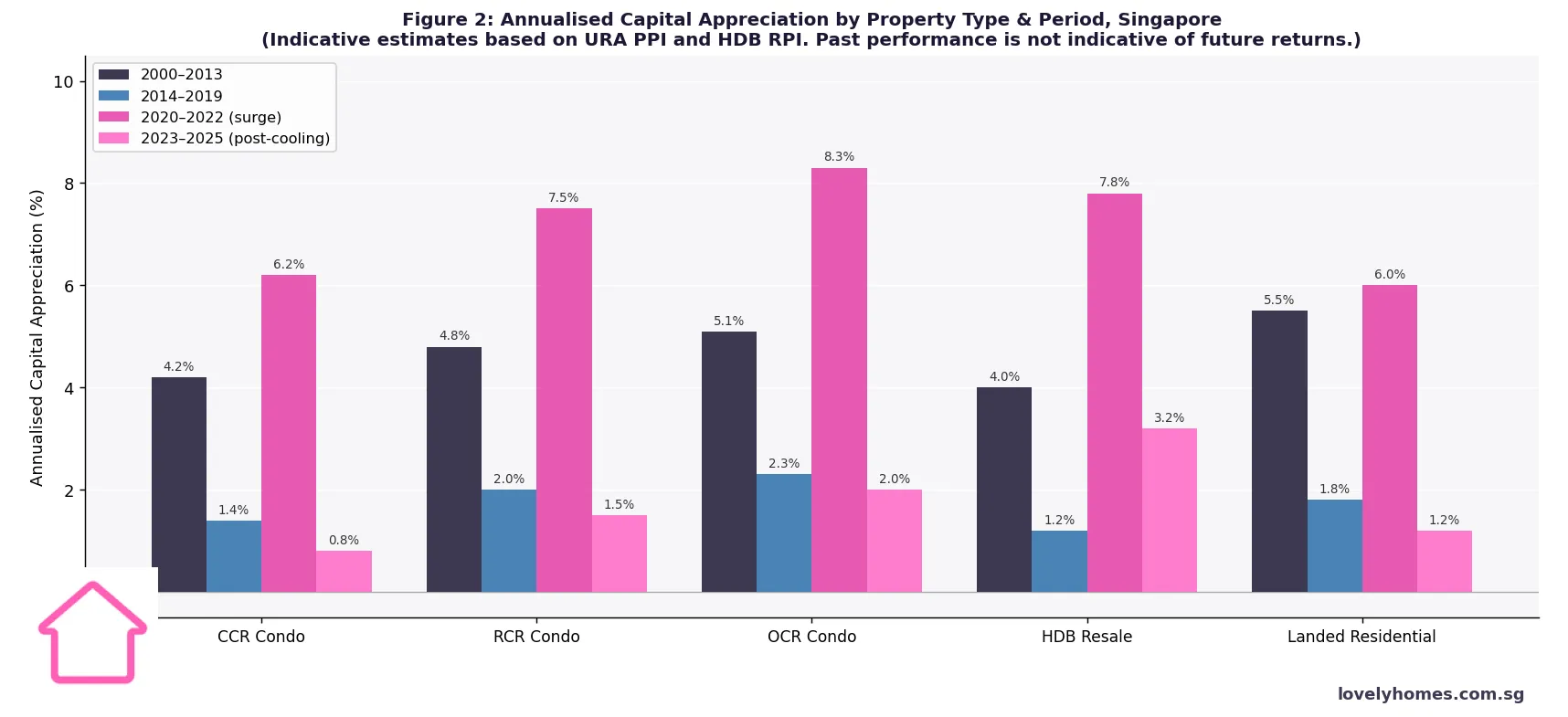

Singapore residential property delivered strong long-run capital appreciation — particularly the 2000–2013 period, which included the post-SARS recovery, two rounds of quantitative easing, and robust population growth. OCR condos and landed property produced annualised gains of 5–6% over that period. However, the 2014–2019 period — dominated by progressive rounds of cooling measures, the Total Debt Servicing Ratio (TDSR) framework, and population growth moderation — saw annualised gains compress to 1.2–2.3% across all property types.

The 2020–2022 surge was exceptional: the pandemic-era ultra-low interest rate environment (SORA briefly fell to 0.22% in 2021), pent-up demand, and a structurally undersupplied resale market drove annualised gains of 6–8% across OCR and HDB. This period is unlikely to repeat in the near term given current mortgage rates of 3.5–4.5% and the government’s demonstrated willingness to deploy cooling measures.

The 2023–2025 post-cooling stabilisation shows OCR condos and HDB resale at 2–3.2% per annum — more sustainable but insufficient to justify a leveraged investment at current LTV and mortgage rate assumptions unless the investor has a 10+ year horizon.

The ABSD Factor: How Stamp Duty Reshapes the Calculus

Singapore Citizens purchasing a second residential property pay 20% ABSD on the purchase price, effective from 27 April 2023. On a S$1.5M OCR condo, this amounts to S$300,000 — an additional upfront cost that must be recovered before the investment breaks even. At a net yield of 2.7% (post all costs), the investor earns approximately S$40,500 per annum in net rental income. At that rate, it takes over seven years of rental income alone to recover the ABSD cost — before accounting for mortgage interest subsidisation.

This is why the property-vs-REIT comparison has become increasingly compelling. Singapore REITs attract zero ABSD, no property tax, no maintenance fees, and no tenant management burden, with gross distributions of 5–8% in many sectors. The trade-off is that REITs do not offer the leverage of a mortgage-financed property and are subject to equity market volatility. See the dedicated S-REIT Investment Guide 2026 for a detailed comparison.

For Singapore Permanent Residents (SPR), the ABSD on a second residential property rises to 30%, making the break-even period even longer. For foreigners, the 60% ABSD renders residential property investment (as opposed to owner-occupation) economically untenable in most cases. Commercial property, which does not attract ABSD and where foreigners can invest freely, offers a structurally more favourable framework for non-citizen investors.

Summary Table: Rental Yield vs Capital Gain at a Glance

| Factor | Rental Yield Focus | Capital Gain Focus |

|---|---|---|

| Best property type | OCR condo, non-mature HDB | CCR / RCR condo, landed |

| Typical gross yield | 3.5–5.0% | 2.2–3.5% |

| Monthly cash flow | Near break-even to positive | Typically negative (subsidised) |

| Ideal hold period | 3–7 years | 7–15 years |

| Liquidity risk | Lower (OCR wider buyer pool) | Higher (CCR narrower pool) |

| Key risk | Vacancy, yield compression | Cooling measures, rate rises |

| ABSD impact (2nd property, SC) | Significant — 7+ yr payback | Significant — 10+ yr payback |

| Alternative | S-REITs (5–8% distributions) | Growth REITs / commercial |

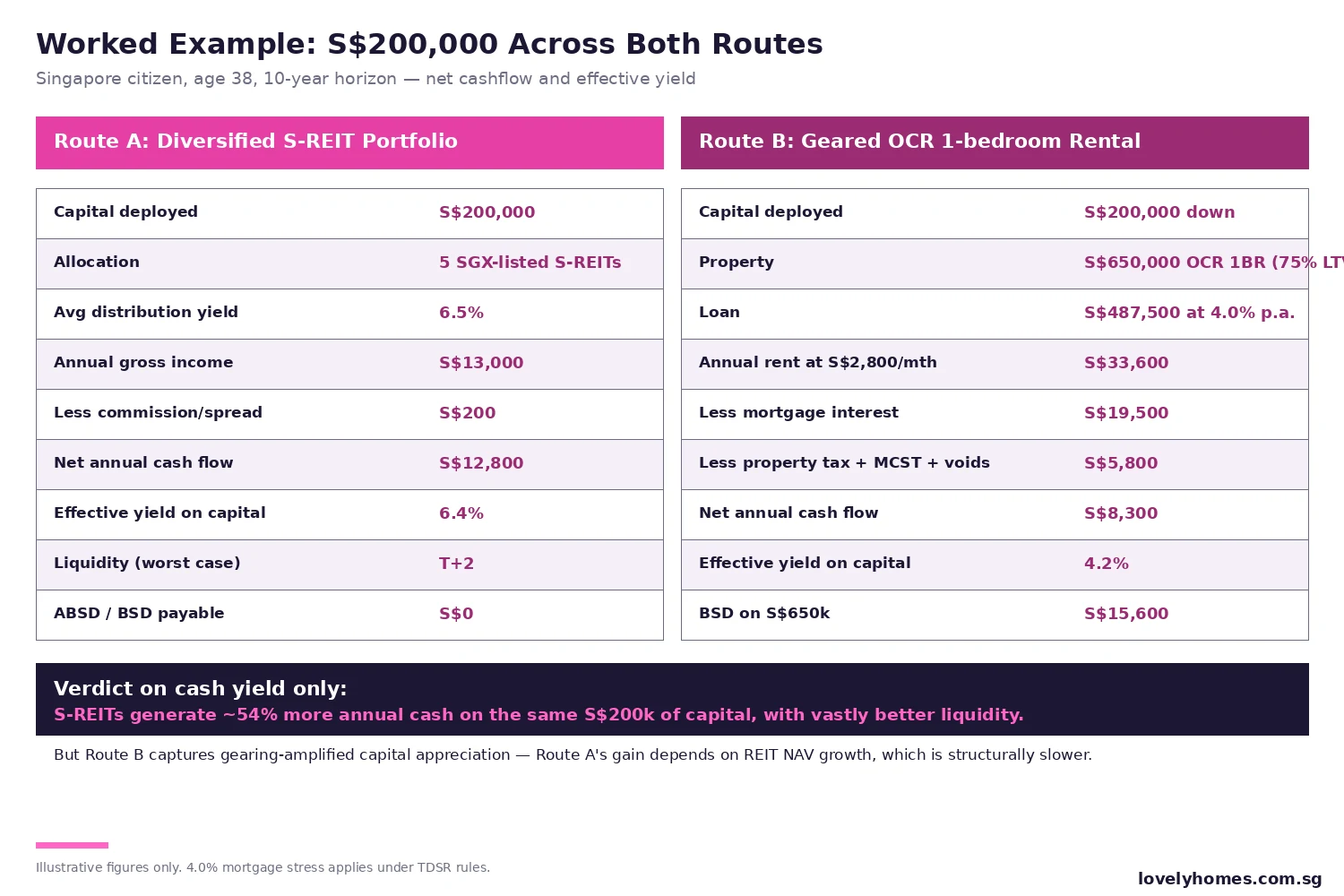

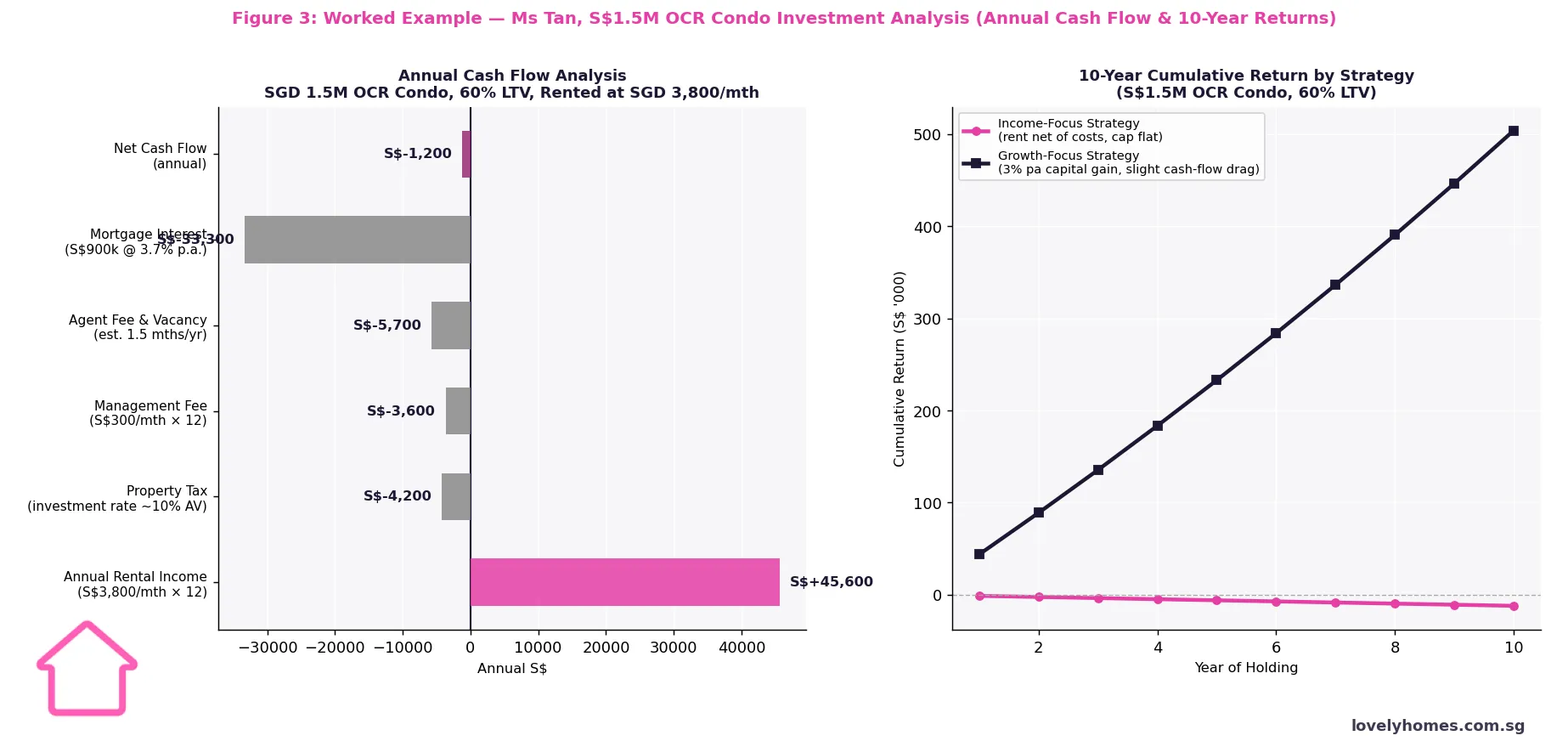

Worked Example: Ms Tan’s S$1.5M OCR Condo

Ms Tan, 42, is a Singapore Citizen with one HDB flat (fully paid). She wishes to invest S$1.5M in a second residential property — a 2-bedroom OCR condo in Tampines. She pays 20% ABSD (S$300,000) plus 5% BSD (S$44,600), bringing the total acquisition cost to S$1,844,600. She finances 60% of the purchase price (S$900,000) via a bank loan at 3.7% per annum (SORA spread, 25-year tenure) after satisfying the TDSR Singapore 2026 constraint at her household income of S$18,000/month.

Annual cash flow breakdown:

- Rental income: S$3,800/month × 12 = S$45,600

- Property tax (investment rate, estimated AV S$33,600): ~S$4,200

- Management fee (S$300/month): S$3,600

- Agent and vacancy allowance (1.5 months/year): S$5,700

- Mortgage interest (S$900k × 3.7%): S$33,300

- Net annual cash flow: approximately –S$1,200 (slightly negative)

The gross yield on the purchase price is 3.04%. The net yield (after all costs, before mortgage principal) is approximately 2.72% — below the mortgage rate of 3.7%. Ms Tan is effectively subsidising the mortgage by about S$1,200 per annum, plus the opportunity cost of the S$300,000 ABSD (foregone investment return at 3% = S$9,000/year).

Capital appreciation scenario: If the property appreciates at 3% per annum over 10 years, the gross capital gain is approximately S$515,000. After selling costs (BSD on seller side N/A — no SSD after 3 years), agent commission (~1%), and assuming no further Seller’s Stamp Duty (the Seller’s Stamp Duty applies for 3 years post-purchase per the property’s holding period), the net gain before tax is approximately S$495,000. Over 10 years, total net return (rental income net + capital gain) is approximately S$483,000 — an annualised return on total equity deployed of roughly 5.5% per annum.

By comparison, the same S$300,000 ABSD + S$600,000 downpayment (S$900,000 total equity) invested in a diversified S-REIT portfolio at a conservative 6% gross distribution yield with 2% capital growth would yield approximately S$690,000 over 10 years — a meaningfully higher outcome with no tenant management, no maintenance, and no mortgage. The direct property route wins primarily if capital appreciation exceeds 3% per annum or if rental rates rise materially.

Why This Matters for Singapore Investors in 2026

The investment property thesis in Singapore has always rested on three pillars: land scarcity, population growth, and government commitment to maintaining a stable housing market. All three remain broadly intact, but the near-term environment is more challenging than the 2020–2022 peak. Mortgage rates have risen from near-zero to 3.5–4.5%, vacancy rates in the private rental market have crept up from sub-5% to 7–10% in CCR and RCR, and the government has maintained or tightened cooling measures (most recently the EC cooling measures of May 2026).

Investors entering the market in 2026 should model conservatively: assume net yields of 2.5–3.5% for OCR condos, capital appreciation of 2–3% per annum (not the 7–8% of 2021–2022), a mortgage rate of 3.5–4.0%, and a 10+ year hold period for the investment to produce an acceptable risk-adjusted return. The ABSD payback period must be factored into the break-even analysis.

What Might Come Next

Several factors could materially shift the yield/growth calculus in the medium term. On the positive side: a sustained decline in Singapore Overnight Rate Average (SORA) benchmarks (linked to US Federal Reserve easing) would reduce mortgage rates and improve cash flows; continued strong foreign talent attraction supporting rental demand; and the progressive unveiling of the Greater Southern Waterfront and Jurong Lake District transformations creating new capital appreciation pockets. On the negative side: an expansion of the pipeline of private residential completions from the record 1H 2026 Government Land Sales programme could compress rents; any tightening of the foreign talent inflow policy would reduce rental demand; and a deterioration in the global economic environment could dampen transaction volumes and prices.

Investors are encouraged to treat property as one component of a diversified portfolio, weigh the liquidity and ABSD constraints explicitly, and consult a licensed financial adviser before committing capital at these price levels.

Frequently Asked Questions

What is the difference between gross yield and net yield in Singapore property?

Gross yield divides annual rental income by the property’s market value or purchase price — it gives you a quick comparison benchmark. Net yield deducts all recurring ownership costs: property tax (charged by IRAS at the investment rate, not the lower owner-occupier rate), maintenance fees, sinking fund contributions, agent commission for finding tenants (typically half a month’s rent per year), vacancy allowance, and insurance. For Singapore condominiums, the gap between gross and net yield is typically 1.0–1.5 percentage points, meaning a property with a 4% gross yield might deliver only 2.5–3.0% net. When evaluating a property for investment, always use net yield as the baseline for comparison against mortgage costs and alternative investments.

Is rental income from Singapore property taxable?

Yes. Rental income from a Singapore property is subject to personal income tax at your marginal rate, which can be as high as 24% for high-income individuals. However, the income is assessed on a net basis — you may deduct allowable expenses including mortgage interest (the interest component, not principal), property tax, maintenance fees, agent commissions, and a deemed 15% allowance on gross rent as an alternative to tracking actual expenses. A property generating S$45,600 gross rent with actual deductible expenses of S$46,800 would produce a taxable loss — which can offset other income in some circumstances. See our guide to capital gains and rental income tax for a full worked example of both the actual-expense and deemed-expense paths.

Can I use CPF to fund an investment property in Singapore?

Yes, you can use CPF Ordinary Account (OA) funds to fund the downpayment and monthly instalments for a second residential property, subject to certain conditions. The CPF usage limit is generally 120% of the property’s valuation limit, and the property must have a remaining lease of at least 20 years. However, all CPF funds used — plus accrued interest at 2.5% per annum — must be refunded to your CPF account from the sale proceeds when you sell. This accrued interest effectively reduces your net profit from the investment. Many investors underestimate this cost; a property held for 20 years could have an accrued interest liability of 65% or more of the original CPF amount used.

How does Seller’s Stamp Duty affect my investment exit strategy?

Seller’s Stamp Duty (SSD) applies to private residential properties sold within 3 years of purchase: 12% in year 1, 8% in year 2, and 4% in year 3. If you purchase a S$1.5M condo and sell within 12 months, SSD is S$180,000 — a massive cost that eliminates most short-term investment gains. SSD does not apply after the 3-year holding period. This means the effective minimum hold for a leveraged property investment is at least 3 years; most investors target 5–10 years to allow the ABSD, SSD, and acquisition costs to be absorbed into a meaningful capital gain. The ABSD guide contains a full table of stamp duty rates by buyer profile and property type.

What are the best alternatives to direct property investment in Singapore?

Singapore offers several liquid alternatives to direct residential property investment. Singapore REITs (S-REITs) trade on SGX and offer diversified exposure to commercial, industrial, retail, healthcare, and data-centre real estate with gross distributions of 5–8% and no ABSD, no management burden, and high liquidity. Freehold strata offices in the CBD carry no ABSD for foreigners and offer yields of 3.5–5%. CPF Investment Scheme (CPFIS) products allow some CPF OA and SA funds to be invested in REITs and property-linked instruments. For investors who want Singapore property exposure without the capital outlay, some private funds and family-office structures offer fractional exposure to residential or commercial portfolios. The commercial property guide and REITs guide provide detailed comparisons.

Should I prioritise yield or growth when buying an investment property?

The correct priority depends on your financial profile. If you have high monthly cash commitments and cannot sustain a negative-cash-flow property for an extended period, yield should take priority — an OCR condo or resale HDB (if eligible) provides a better income cushion. If you have substantial savings, a long investment horizon (10+ years), and a high income that covers any monthly shortfall, a CCR or prime-location property may deliver superior absolute capital gains over the long run, even if the annual cash flow is negative. In the current rate environment (mortgage rates 3.5–4.2%), properties with gross yields below 4% are cash-flow negative even without accounting for ABSD, so ensure you model both the yield and the capital appreciation case explicitly before committing.

How do I calculate the net return on a Singapore investment property?

Total net return = (Net rental income over hold period) + (Sale price – Purchase price – Acquisition costs – Selling costs). Acquisition costs include BSD, ABSD, legal fees (roughly S$3,000–S$6,000 for a condo purchase), and agent commission. Selling costs include agent commission (1–2% of sale price), legal fees, and any SSD if sold within 3 years. If CPF was used, you must also account for CPF accrued interest repaid to the CPF account on sale. Divide total net return by the equity deployed (downpayment + ABSD + all upfront costs) and the number of years held to derive an annualised return on equity. For most S$1.5M OCR condos purchased in 2026 with 20% ABSD, you need a minimum 3.5% per annum capital appreciation and a 10-year hold to match a 6% p.a. REIT distribution on the same equity.

Related Articles

- ABSD Singapore 2026 — Complete Guide

- Singapore REITs Investment 2026

- Capital Gains and Rental Income Tax Singapore 2026

- Commercial Property Investment Singapore 2026

- TDSR Singapore 2026

- Refinancing Home Loan Singapore 2026

- 99-to-1 Property Purchase Singapore 2026

Disclaimer

This article is for general informational purposes only and does not constitute financial, tax, or investment advice. Rental yields, capital appreciation figures, and return projections are illustrative estimates based on publicly available data and should not be relied upon for investment decisions. Past performance of Singapore property markets is not indicative of future returns. All investments carry risk, including the possible loss of principal. Consult a licensed financial adviser, MAS-licensed investment adviser, and IRAS for your specific circumstances. ABSD, SSD, and other stamp duty rates are subject to change without notice.

Tags: Rental Yield Singapore, Capital Gain Property Singapore, Singapore Property Investment 2026, Gross Net Yield, Investment Property Singapore, ABSD Second Property, Singapore Condo Investment, Property vs REITs, OCR Condo Yield, Singapore Property Returns