Singapore Condo MCST Guide 2026: Maintenance Fees, AGM, By-Laws and Your Rights as a Subsidiary Proprietor

Every condominium and privatised executive condominium in Singapore is governed by a Management Corporation Strata Title — the MCST. If you own a condo unit, you are automatically a member of the MCST. The monthly maintenance fees that hit your bank account, the Annual General Meeting (AGM) notice that lands in your letter box each year, the by-law that governs what colour your front door can be, the sinking fund that pays for the carpark resurfacing in 2030 — all of this flows from the MCST framework.

Yet the MCST is one of the least understood aspects of condo ownership in Singapore. Most buyers ask about price, location, and facilities; few ask about management fee trajectory, sinking fund adequacy, or the quality of the Management Council before they sign. This guide fixes that gap. It explains how MCSTs work, what your rights and obligations are as a Subsidiary Proprietor (SP), how maintenance fees are set, what the AGM process involves, and how to handle disputes — covering the full framework under the Building Maintenance and Strata Management Act (BMSMA) Cap 30C, administered by the Building and Construction Authority (BCA) and adjudicated at the Strata Titles Board (STB).

Quick Answer — MCST at a Glance

- Every condo or privatised EC is automatically governed by an MCST from the moment the first subsidiary strata certificate of title is issued. You cannot opt out.

- As a unit owner (Subsidiary Proprietor / SP), you must pay monthly contributions — a management fund charge (for day-to-day operations) and a sinking fund charge (for capital works). Together these form your “maintenance fee”.

- The MCST is governed by an elected Management Council (MC) of up to 10 councillors chosen at the AGM. Day-to-day operations are usually delegated to a Managing Agent (MA).

- The AGM must be held once a year. SPs can vote on the annual budget, elect the MC, pass special resolutions (which require a 75% majority by share value), and raise issues via a general meeting.

- Typical monthly maintenance fees in 2026 range from about S$250 (studio in budget condo) to S$1,700+ (4BR in premium development).

- The sinking fund must by law be maintained at no less than 10% of the total annual contributions, but most well-managed developments target significantly more.

- Disputes between SPs and the MCST — or between SPs — are adjudicated by the Strata Titles Board (STB), which is a specialist tribunal under the BMSMA.

- Before buying a condo, check the MCST’s annual accounts, AGM minutes, and sinking fund balance. A poorly managed MCST with a depleted sinking fund is a major hidden liability.

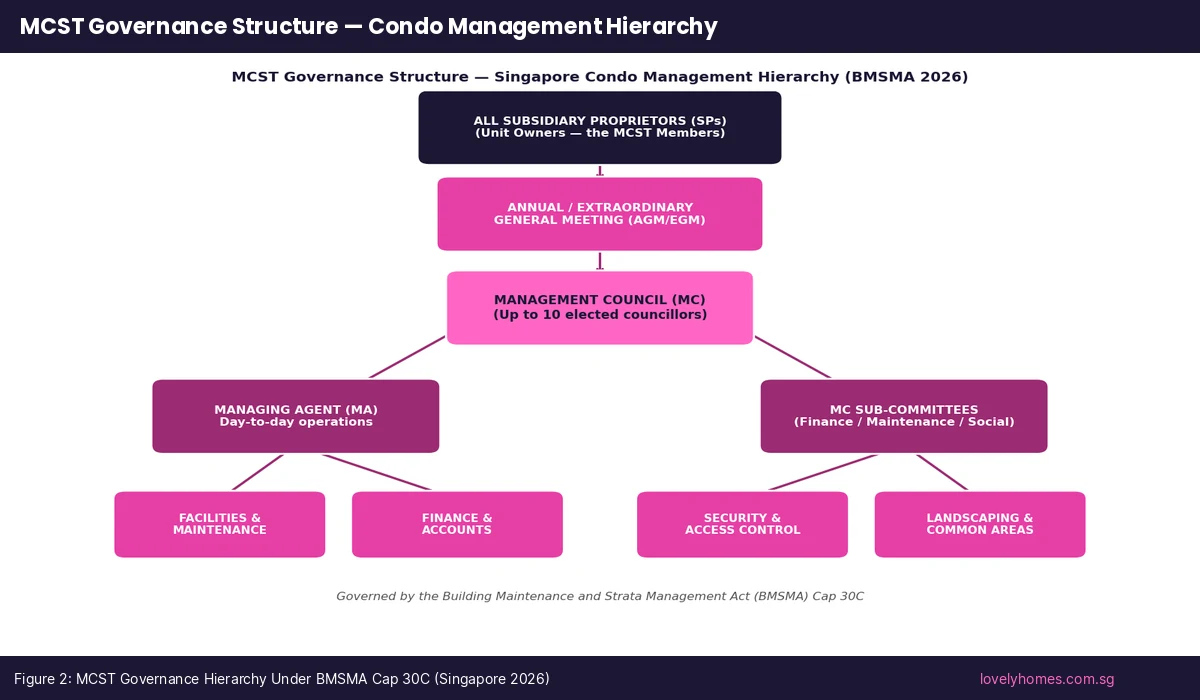

What Is an MCST?

An MCST — Management Corporation Strata Title — is the legal body that owns, manages, and maintains the common property of a strata-titled development. Common property is everything that is not part of an individual lot — the pool, gym, lobby, lifts, carpark, garden, external façade, rooftop, and all the pipes and cables running through the common areas. The MCST is a body corporate under the BMSMA: it can sue and be sued, enter contracts, hold bank accounts, and own property (specifically, the common property it manages).

Singapore’s MCST system derives from the Strata Titles Act (Cap 158) and the BMSMA. The MCST is formed automatically when the Commissioner of Buildings registers the strata roll. Each MCST has a unique strata title plan number — e.g., “MCST No. 1234” — which is filed with the Singapore Land Authority (SLA). An MCST covers exactly one strata development. There is no such thing as a shared MCST across multiple developments.

Share Values — The Key to MCST Voting and Fees

Each lot (unit) in the development is assigned a share value by the Singapore Land Authority at the time the strata plan is approved. Share values are calculated based on the floor area of the unit relative to all units in the development. A 2BR unit of 800 sqft in a development with a total share value of 1,000 might be assigned a share value of 8. Share values matter for two reasons: they determine your proportionate share of the maintenance fees; and they determine your voting weight at general meetings (each share value = one vote).

The Management Fund and Sinking Fund

MCSTs collect contributions through two separate accounts, both mandatory under the BMSMA:

Management Fund

The management fund covers the operational costs of running the development. This includes the MA’s fees, security guard salaries and contracts, utilities for common areas, cleaning and landscaping, lift maintenance, swimming pool upkeep, pest control, insurance premiums (for fire and public liability), and minor repairs. The management fund is essentially the development’s operating budget.

Sinking Fund

The sinking fund is a capital reserve for major, long-term works — repainting the external façade, replacing the lifts (typically every 20–25 years), resurfacing the carpark, upgrading the security system, replacing ageing pipes, and replacing major mechanical and electrical plant. Under BMSMA s.38(4), the sinking fund must be maintained at no less than 10% of total annual contributions. In practice, a well-managed development that is 15+ years old will typically hold a sinking fund equal to 2–5 years of total annual contributions.

Typical Maintenance Fee Ranges in 2026

Singapore’s maintenance fee landscape in 2026 spans a wide range depending on development tier, facilities, and unit size. Industry figures suggest the following broad ranges:

| Development Tier | Studio / 1BR | 2BR | 3BR | 4BR+ |

|---|---|---|---|---|

| Budget / Small Boutique (<300 units, basic facilities) | S$250–S$320 | S$370–S$470 | S$470–S$600 | S$650–S$900 |

| Mid-Tier (300–600 units, pool/gym/function room) | S$320–S$450 | S$500–S$700 | S$700–S$950 | S$950–S$1,250 |

| Premium / Full-Facilities (600+ units, concierge, indoor sports, spa) | S$500–S$700 | S$800–S$1,100 | S$1,100–S$1,500 | S$1,500–S$2,500+ |

These are indicative only. In a large development like Tampines Concourse or The Pinnacle@Duxton (if it were private), the lower per-unit cost benefits from economies of scale. A boutique development of 20 units with a rooftop pool will have a disproportionately high per-unit fee because the fixed costs are spread over fewer owners. Maintenance fee rates are set annually by the MC at the AGM and can increase over time, particularly as buildings age and require more expensive maintenance.

The Management Council — How Your Condo Is Governed

The Management Council (MC) is elected at the AGM by the SPs of the development. The MC is responsible for the management and control of the use and enjoyment of the common property, and for carrying out the powers and duties of the MCST under the BMSMA. The MC can have up to 10 councillors. It elects a Chairperson, Secretary, and Treasurer from among its members. MC meetings are typically held monthly or bi-monthly.

In practice, many MC councillors are owner-occupiers with a genuine stake in how well the development is managed. Inactive or absentee-dominated MCs — where the majority of councillors are landlords who do not live in the development — can lead to conflicts between short-term cost minimisation and the long-term wellbeing of the asset. Owner-occupiers buying for the long term should consider attending AGMs and, if they have the time, standing for election to the MC.

The Managing Agent (MA)

Most MCSTs engage a professional MA to handle the operational day-to-day work. Singapore’s leading MAs include CBRE Property Management, Savills Property Management, Jones Lang LaSalle, Knight Frank Property Asset Management, and a number of specialist condo management firms. The MA is hired by and reports to the MC. The MA does not own or control the MCST — it is a contractor. The MA’s contract is typically a 1-to-3-year appointment, renewed (or re-tendered) at the MC’s discretion.

The MA typically handles: collection of maintenance fees, payment of invoices, procurement of service contracts (lifts, security, pest control), organising the AGM, keeping strata roll records, liaising with BCA on regulatory compliance, and managing day-to-day resident queries and complaints.

The Annual General Meeting (AGM)

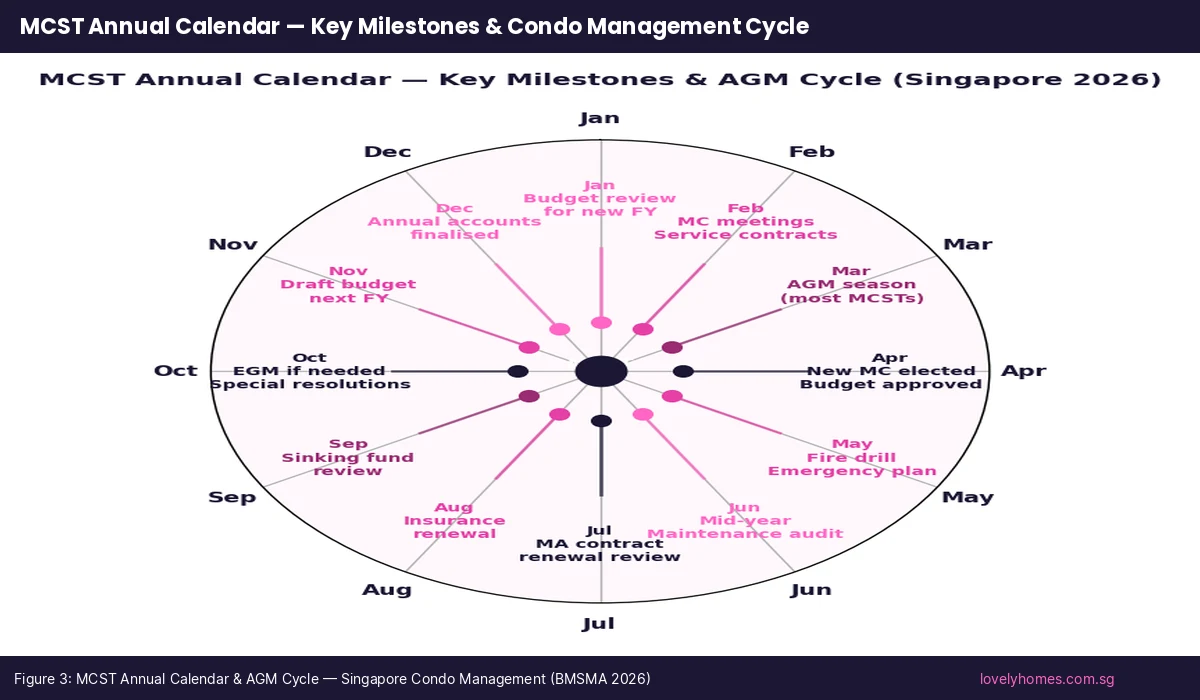

The AGM is the primary mechanism through which SPs exercise democratic control over their MCST. Under BMSMA s.27, the first AGM must be held within 13 months of the MCST’s formation. Thereafter, the AGM must be held at least once every calendar year and not more than 15 months after the preceding AGM. Most Singapore condominiums hold their AGM between January and April, after the financial year end.

Standard AGM Agenda

A typical AGM agenda includes: (1) adoption of the previous year’s financial accounts and auditor’s report; (2) approval of the budget for the coming financial year (management fund and sinking fund contributions); (3) election of the Management Council; (4) appointment of the auditor; (5) any motions submitted by SPs; and (6) any other business. The budget approval item is the most consequential — it sets the monthly maintenance fee for the year ahead.

Voting at the AGM

Votes at an AGM are counted in one of two ways depending on the resolution type. Ordinary resolutions (routine decisions like budget approval and election of councillors) are decided by a simple majority of the share values of SPs present and voting. Special resolutions (which include significant changes like amending by-laws, changing the method of allocation of contributions, or entering major contracts above a threshold) require 75% of the share values of all SPs — not just those present. This is a high bar and means that contentious changes to how a development is managed require broad consensus.

Extraordinary General Meetings (EGMs)

EGMs can be called between AGMs by the MC, or by SPs representing at least 25% of the total share value submitting a written requisition. EGMs are used for urgent decisions — unexpected major repairs, a change of MA, or resolutions that cannot wait for the next AGM. The notice requirements for an EGM are the same as for an AGM: at least 14 days’ written notice must be given to all SPs.

By-Laws — What You Can and Cannot Do in Your Condo

By-laws are the rules that govern behaviour within a strata development. The BMSMA prescribes a set of default by-laws in the Second Schedule that apply to every development unless specifically amended by a special resolution at a general meeting. These default by-laws cover matters such as: not interfering with the peaceful enjoyment of other lots; keeping animals only with MC approval; not hanging laundry on the external façade; not obstructing common property; not making structural alterations without MC approval; and not creating noise nuisance.

Developments may add their own by-laws to supplement the statutory defaults. A development with a strict “no pets” policy, a ban on short-term rentals (Airbnb is already prohibited by law in Singapore for stays under 3 months), or a rule requiring parquet flooring to be covered by rugs to reduce noise transmission, can encode these in its registered by-laws. Registered by-laws are binding on all SPs, tenants, and residents — including buyers who purchase the unit after the by-law was registered.

Before buying a resale condo, ask your solicitor to obtain the MCST’s registered by-laws and review them carefully. A by-law prohibiting pets, for instance, may not be waivable even with the MC’s informal approval — the by-law governs.

Your Rights and Obligations as a Subsidiary Proprietor

As an SP, you have a set of substantive rights and corresponding obligations under the BMSMA:

| Your Rights | Your Obligations |

|---|---|

| Attend and vote at AGMs/EGMs | Pay maintenance contributions on time (late fees apply) |

| Stand for election to the Management Council | Comply with MCST by-laws and the BMSMA |

| Inspect the MCST’s financial accounts and strata roll | Obtain MC approval before carrying out renovations affecting common property or load-bearing structures |

| Submit motions for consideration at general meetings | Not cause nuisance or hazard to other residents |

| Apply to the Strata Titles Board to resolve disputes | Maintain your lot in good repair so as not to damage common property |

| Share in the common property proportionate to share value | Not carry out alterations to common property without consent |

Renovation Approvals — The Most Common Flashpoint

Renovation disputes are the most frequent source of conflict in Singapore condominiums. The key rules under the BMSMA and HDB/BCA guidelines (for SPs who engage licensed renovation contractors) are: any works that affect or penetrate the floor slab, any works that affect the common property (including the external façade, windows, and any shared walls), and any hacking or structural works, require prior MC approval. The SP must submit a renovation application to the MA with details of the works, the contractor’s name and licence number, and drawings or specifications as required. The MC has the right to inspect the works and to require rectification if the works deviate from what was approved.

The MA will typically send a renovation notice to neighbours within the affected units before works commence. Renovation hours are governed by the BMSMA and the NEA: Monday to Saturday 9am–6pm; no works on Sundays and public holidays.

Dispute Resolution — The Strata Titles Board

The Strata Titles Board (STB) is the specialist tribunal established under the BMSMA to adjudicate disputes arising in strata developments. Filing a complaint with the STB is significantly cheaper and faster than going to court. The STB handles disputes between SPs, between SPs and the MCST/MC, and between the MCST and its MA. Common STB applications include: enforcement of by-laws; disputes over maintenance fee quantum; improper conduct at AGMs; failure of the MCST to carry out repairs; and disputes over the validity of a special resolution.

Before filing at the STB, parties are required to attempt mediation at the Singapore Mediation Centre (SMC). Many condo disputes — particularly neighbour noise complaints and renovation disputes — are resolved at mediation without proceeding to a full STB hearing.

Worked Example — Buying a Resale Condo: MCST Due Diligence

Ms Chen is purchasing a resale 3BR condominium in the East Coast (D15) for S$1,650,000. Before exercising the OTP, her solicitor requests the following MCST documents from the vendor’s solicitor:

- The most recent 3 years of annual financial accounts (management fund and sinking fund audited statements).

- The last 2 years of AGM minutes.

- The current year’s approved budget and contribution rates.

- Any outstanding arrears on the unit being purchased.

- A copy of the registered by-laws (including any special by-laws passed since the development was completed).

- Any pending special levies or special assessments (capital works that have been voted for at an AGM but not yet reflected in the monthly maintenance fee).

From the accounts, she notes that the sinking fund stands at S$1.2M for a 180-unit development — approximately S$6,700 per unit. Given the development is 18 years old and will need a major façade repainting and lift replacement within the next 5 years (estimated cost: S$2.5M), she raises with her agent that the sinking fund appears under-funded. At the AGM 3 months earlier, a special levy of S$3,000 per unit was voted through to top up the sinking fund. This is a real cash cost she factors into her budget. Armed with this analysis, she negotiates a S$20,000 price reduction. Monthly maintenance fee: S$780 (her 3BR unit’s share value × contribution rate of S$5.50 per share value per month).

What Might Change — MCST Reform and BCA Digitalisation

The BCA has been progressively digitalising MCST administration. By 2025, all MCST annual accounts and AGM minutes must be filed electronically with BCA via the Integrated Property Management System (IPMS). This creates a searchable public record of every registered MCST in Singapore — a significant transparency improvement for prospective buyers conducting due diligence. The BCA has also been reviewing minimum sinking fund contribution requirements, with a proposal to increase the 10% minimum for older developments (15 years+) to better reflect actual capital expenditure needs. Any regulatory change here would increase monthly fees for owners of older condominiums.

Frequently Asked Questions

Can the MCST prevent me from renting out my unit?

Generally, no. The MCST cannot prohibit an SP from renting out their lot — the right to rent out a freehold or leasehold unit is a fundamental property right. However, the MCST can and typically does require: (a) advance notice of any tenancy and the tenant’s details for the strata roll; (b) the SP to ensure the tenant complies with all MCST by-laws; and (c) that tenancy periods comply with the legal minimum of 3 months (short-term rentals are prohibited in Singapore for all private residential properties). If a tenant repeatedly violates by-laws, the MCST can take action against the SP (as the lot owner responsible for the tenant’s conduct) rather than against the tenant directly.

What happens if I do not pay my maintenance fees?

Under BMSMA s.40, the MCST may recover unpaid contributions as a debt due in any court. The MA will first send reminder letters and impose late payment charges (typically 2–5% per month on the overdue amount, as specified in the by-laws). If the arrears persist, the MCST may obtain a judgment against the SP and register a charge against the unit on the land register — effectively a lien on the property that must be discharged before any sale can proceed. In extreme cases, the MCST may apply for a court order for the sale of the unit to recover arrears, although this is rare in practice. Arrears do not disappear on a change of ownership — buyers should confirm there are no outstanding contributions before completing a resale purchase.

How is the monthly maintenance fee calculated for my specific unit?

Your monthly maintenance fee is calculated as: your share value × the contribution rate per share value per month. The MC sets the contribution rate annually at the AGM when it approves the budget. For example, if your unit has a share value of 8 and the MC has approved a contribution rate of S$60 per share value per month, your monthly maintenance fee is S$480. Within that, the split between management fund and sinking fund contributions is also set by the MC, subject to the BMSMA minimum sinking fund requirement. Your share value is fixed at the time the strata plan is registered and can only be changed by a unanimous resolution of all SPs plus approval from the Commissioner of Buildings — a very high bar in practice.

Can I paint my front door a different colour?

This is one of the most asked questions in Singapore condo forums. The answer depends on whether your front door is considered part of your lot or part of the common property, and whether the development’s by-laws specify approved colours. In most strata developments, the front door is considered a boundary element: the outer surface (facing the common corridor) is common property; the inner surface (facing your unit) is your property. This means you generally cannot change the exterior colour of your door without MC approval. Some developments have standardised door colours as part of the building’s design consistency and enforce this via by-law. Check the development’s by-laws and ask the MA before making any exterior changes.

What is a Special Levy and can the MC impose one without an AGM?

A special levy is a one-time additional contribution charged to SPs to fund a specific capital project — for example, an urgent roof repair, replacing ageing air-handling units, or upgrading the security system beyond what the sinking fund can cover. Under the BMSMA, the MC can impose a special levy for urgent works (where waiting for the AGM would cause disproportionate damage) without first convening a general meeting, but must seek ratification at the next general meeting. For non-urgent capital works, a special levy should ideally be approved by a general meeting before it is imposed. The quantum of the levy is typically proportionate to share value, so each SP pays in line with their proportionate interest in the development.

How do I check the sinking fund health of a condo before buying?

Request the MCST’s audited annual accounts for the past 3 years from the vendor’s solicitor or the MA. The sinking fund balance will appear as a liability in the MCST’s balance sheet. To assess adequacy, compare the sinking fund balance to the development’s age and condition, and any Capital Expenditure Plan (CapEx plan) that the MCST or MA has prepared. A useful rule of thumb: a development that is 10–15 years old in good condition should have a sinking fund of at least S$5,000–S$10,000 per unit; a development over 20 years old should ideally have S$15,000+ per unit. These are rough benchmarks — actual adequacy depends on the specific works required. Also review the AGM minutes for any discussions of upcoming capital works that may trigger a special levy.

Can I attend an AGM as a tenant rather than an owner?

No. Only Subsidiary Proprietors (unit owners) and their authorised proxies may attend and vote at MCST general meetings. Tenants have no standing at the AGM and cannot vote on MCST matters. If you are an SP but cannot attend the AGM in person, you may appoint a proxy by submitting a duly executed proxy form before the meeting. The proxy can be any person — it does not have to be another SP. If you rent out your unit and want a say in how the development is managed, you must attend the AGM personally or appoint a proxy.

Related Articles

- Buying a Condo in Singapore 2026: Complete Guide to Costs, Eligibility and Process

- Renting a Condo in Singapore 2026: Complete Guide to Leases, Costs and Tenant Rights

- Singapore Executive Condo (EC) Buying Guide 2026: Eligibility, Prices and MOP

- Singapore Property Investment Guide 2026: How to Buy, Rent and Build Wealth

- Singapore Property Conveyancing Guide 2026: OTP, S&P Agreement and Legal Fees

- Singapore Property Cooling Measures Timeline 2009–2026

- Singapore Rental Market Guide 2026: HDB and Condo Rents, Yields and Outlook

Disclaimer

This article is published for general informational and educational purposes only. It does not constitute legal, financial, or property management advice. MCST rules, BMSMA provisions, and BCA regulations are subject to amendment. Always refer to the BCA BMSMA resources and the Building Maintenance and Strata Management Act on Singapore Statutes Online for authoritative guidance. For specific MCST disputes or governance issues, consult a Singapore-qualified lawyer or the Strata Titles Board. Maintenance fee figures quoted are indicative industry estimates and will vary by development.