Singapore Strata Title and MCST Guide 2026: Management Fees, Sinking Fund, By-Laws and En Bloc Rights

Strata title is the legal framework that governs ownership and shared management in Singapore’s condominiums, executive condominiums, townhouses, shophouses, and other multi-unit developments. When you buy a condominium unit in Singapore, you are buying a strata-titled property — you own your individual unit outright while sharing ownership of the common areas with all other unit owners as a collective body. This guide explains what strata title means in practice: how the Management Corporation Strata Title (MCST) operates, what management fees and sinking funds cover, your rights as a subsidiary proprietor, and how strata law intersects with en bloc collective sales.

- Strata title splits a development into individual lots (your unit) and common property (lobbies, lifts, pools, carparks) owned collectively by all unit owners as an MCST.

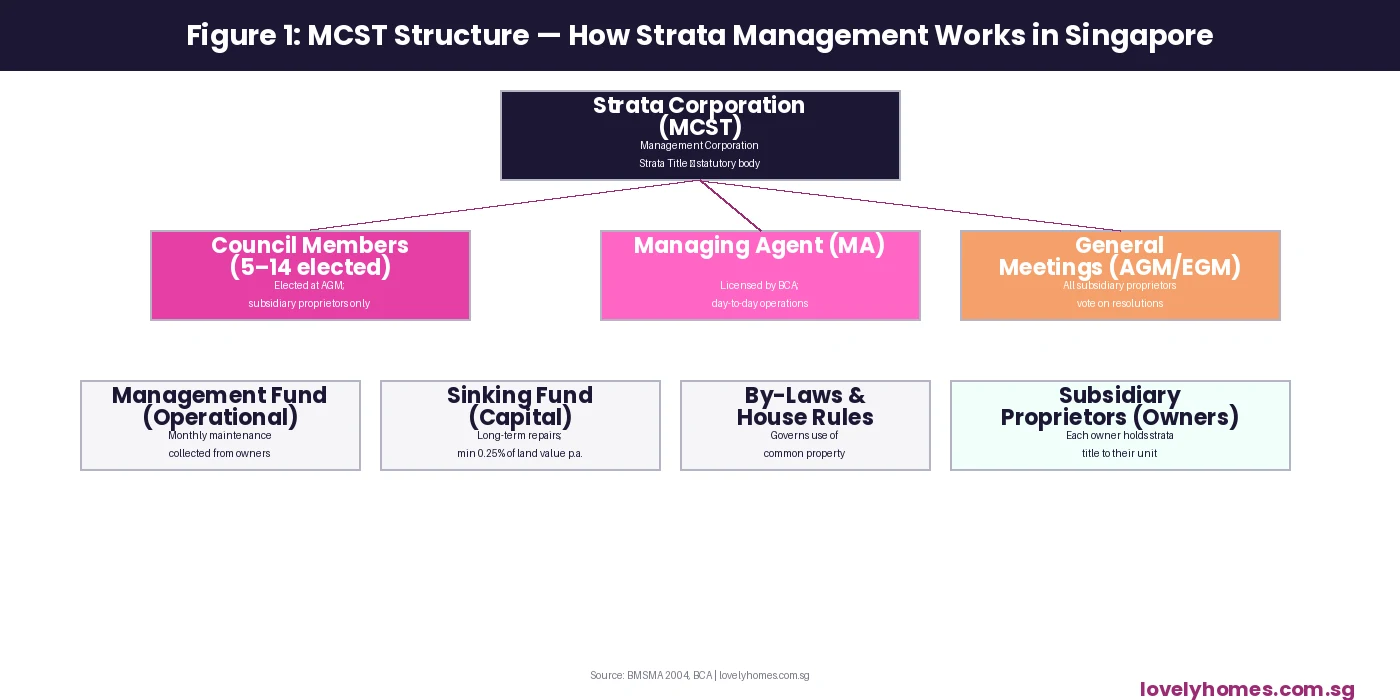

- The MCST (Management Corporation Strata Title) is a statutory body created automatically when a strata development is registered — it has legal personality and can sue, be sued, and enter contracts.

- All unit owners are subsidiary proprietors and have equal legal right to attend and vote at general meetings (AGM and EGM).

- A Council of 5–14 elected members (elected at the AGM) handles day-to-day decisions; a Managing Agent (MA) licensed by BCA is typically appointed for operational management.

- Two funds are mandatory: the Management Fund (operational maintenance) and the Sinking Fund (capital repairs and long-term works).

- Monthly contributions are collected based on your unit’s share value — a number assigned at the point of development approval that reflects your unit’s relative size and floor level.

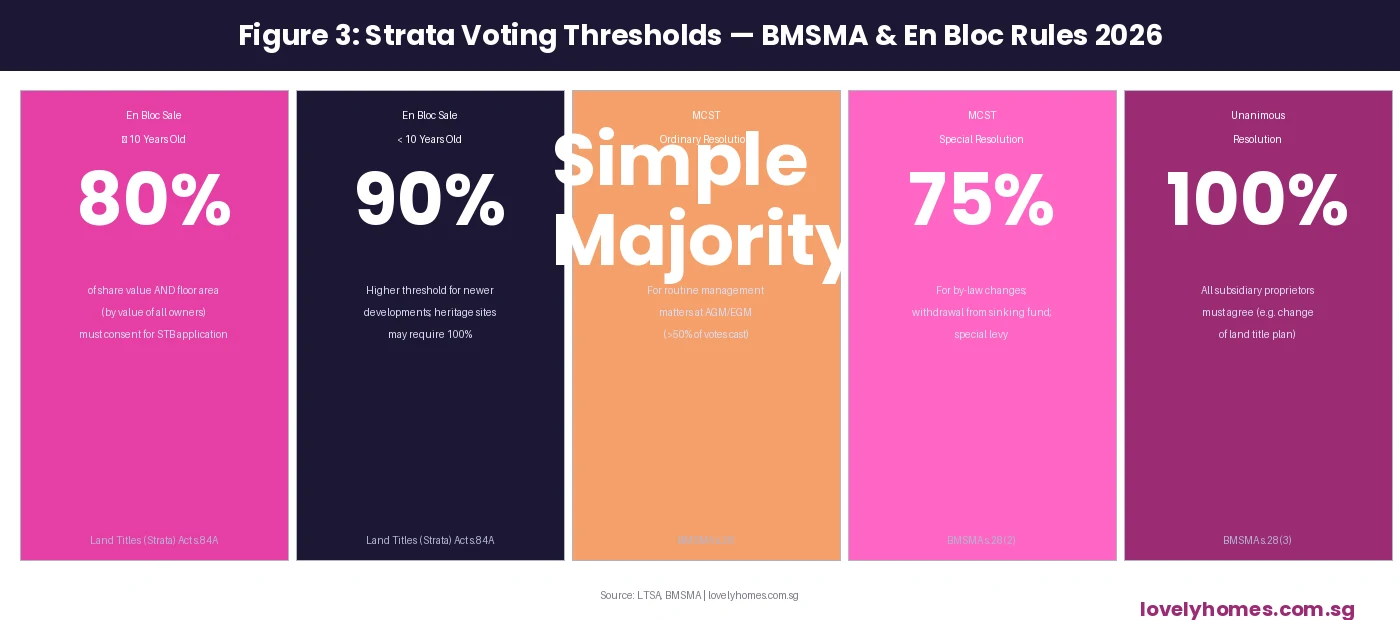

- By-laws govern use of common property and can be changed by special resolution (75% of votes cast at a general meeting).

- En bloc collective sale requires 80% consent (by share value and floor area) for developments at least 10 years old, or 90% for newer ones.

What Is Strata Title?

Strata title is a form of property ownership introduced in Singapore by the Land Titles (Strata) Act (LTSA), which allows a single piece of land to be subdivided vertically into multiple strata lots — each independently owned — while designating the remaining areas as common property shared by all lot owners. The concept originated in New South Wales, Australia in the 1960s and was adapted for Singapore in the 1960s, when high-rise residential development began in earnest.

Every strata development in Singapore has a strata plan filed with the Singapore Land Authority (SLA), which delineates the boundaries of each individual lot (measured in floor area) and designates all remaining areas — corridors, lifts, void decks, swimming pools, gymnasiums, carparks, and landscaped grounds — as common property. Your Certificate of Title will show your strata lot number, floor area, and share value in the development.

The legislation governing strata management in Singapore is the Building Maintenance and Strata Management Act (BMSMA), administered by the Commissioner of Buildings under the Building and Construction Authority (BCA). The BMSMA came into force in 2005, consolidating and updating the earlier Land Titles (Strata) Act provisions on management, and was significantly amended in 2017 to strengthen owner rights and governance.

The MCST — Who It Is and How It Works

The Management Corporation Strata Title (MCST) is a statutory body that comes into existence automatically when the strata development is registered with the SLA. It has its own legal personality — it can enter into contracts (with managing agents, insurers, contractors), open bank accounts, sue, and be sued. Every subsidiary proprietor is automatically a member of the MCST by virtue of owning a unit in the development. The MCST’s legal authority, governance framework, and financial obligations are set out in the BMSMA.

The Council

The MCST is governed by a Council of elected subsidiary proprietors, comprising between 5 and 14 members depending on the size of the development. Council members are elected at the Annual General Meeting (AGM), serve for one year, and may stand for re-election. Only subsidiary proprietors (or their nominees, who must be individuals, not companies) may serve on the Council. The Council makes day-to-day management decisions on behalf of the MCST — approving expenditure, directing the managing agent, and setting maintenance schedules — within limits set by the general meeting.

The Managing Agent

Most MCSTs appoint a Managing Agent (MA) — a licensed property management company — to handle day-to-day operational tasks: collecting management fees, maintaining common area facilities, engaging contractors, handling resident feedback, and administering the development’s accounts. MAs must hold a valid licence from BCA. The appointment of the MA is approved at the AGM or EGM, and the MA acts as agent of the MCST, not as a principal.

General Meetings

The MCST must hold an Annual General Meeting (AGM) within 15 months of the preceding AGM. At the AGM, the management fund budget for the coming year is approved, council members are elected, and the MA’s appointment is ratified. Extraordinary General Meetings (EGMs) may be convened by the Council or by requisition of subsidiary proprietors holding at least 25% of total share value. Decisions at general meetings are made by ordinary resolution (simple majority of votes cast), special resolution (75% of votes cast), or unanimous resolution (100% agreement), depending on the matter.

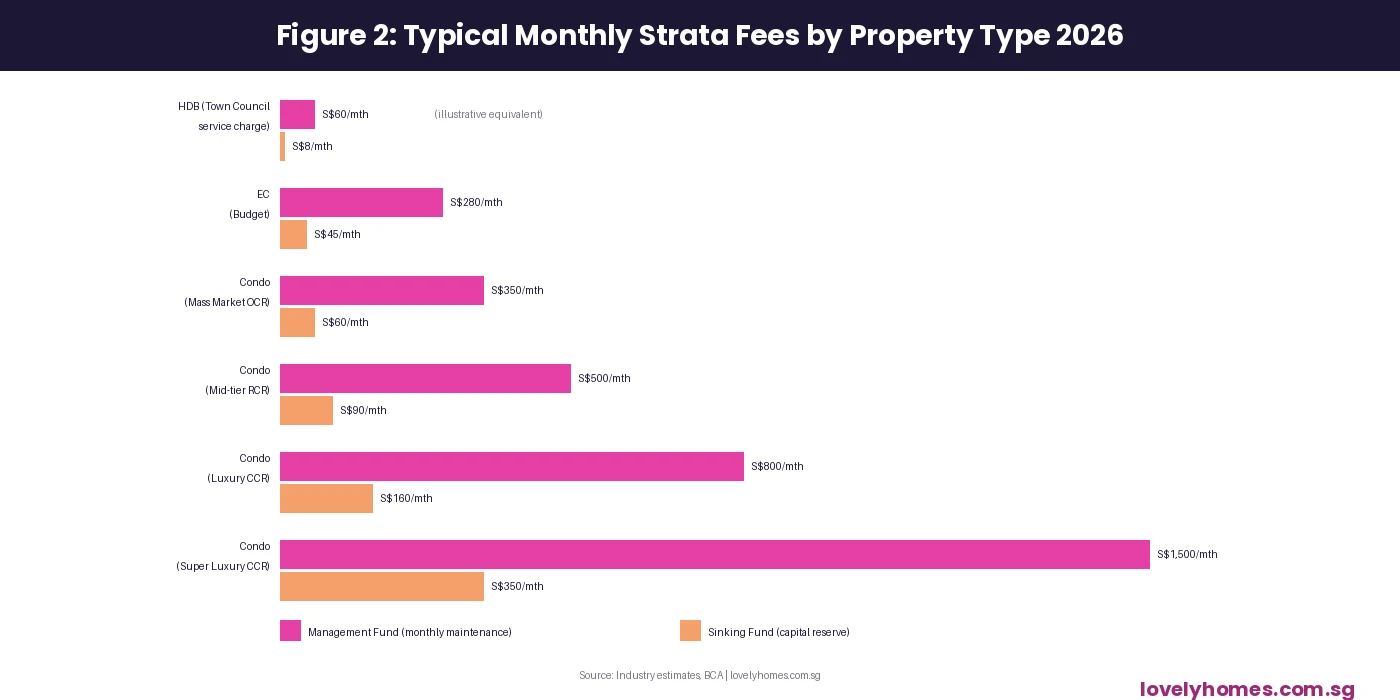

Management Fund and Sinking Fund — What Your Monthly Fee Covers

The BMSMA requires every MCST to maintain two distinct funds:

Management Fund

The Management Fund covers the day-to-day operational costs of the development: managing agent fees, landscaping and cleaning, utility bills for common areas, pest control, routine maintenance and minor repairs, insurance premiums for the development’s common property, and administration costs. Every subsidiary proprietor is required to pay contributions to the Management Fund in proportion to their unit’s share value. The contribution rate is set at the AGM when the annual budget is approved.

Sinking Fund

The Sinking Fund is a long-term capital reserve for major repairs and replacement works that cannot be funded from the Management Fund. Examples include repainting the entire development, replacing lifts, repairing the roof, resurfacing the carpark, and replacing pool filtration systems. The BMSMA requires that the Sinking Fund contribution be at least 10% of the Management Fund contribution, but most well-managed developments set aside considerably more. The Commissioner of Buildings may direct the MCST to increase Sinking Fund contributions if the fund is deemed inadequate relative to the development’s age and condition.

Share Value — How Your Contribution Is Calculated

Your share value is a number assigned to your unit at the point of strata subdivision approval by the SLA. It reflects your unit’s relative size, floor level, and use within the development — larger or higher units typically have a higher share value than smaller or lower units. Share value determines two things: your monthly contribution to the Management Fund and Sinking Fund (fees are proportional to your share value as a fraction of the total share value of the development), and your voting weight at general meetings (each share value equals one vote).

Share values are fixed at the time of development and cannot be changed without unanimous resolution of all subsidiary proprietors and SLA approval. This means that if you buy a penthouse with a share value of 12 and the development has a total share value of 1,200, you contribute 1% of all maintenance costs and have 1% of the total voting weight — regardless of how many units there are.

By-Laws — House Rules with Legal Teeth

The MCST’s by-laws are the rules that govern the use of individual strata lots and common property. Singapore law distinguishes between prescribed by-laws (default rules set out in the Third Schedule of the BMSMA, which apply automatically to every development unless modified) and additional by-laws (rules adopted specifically by the MCST at a general meeting).

Common by-law subject matter includes: prohibition on smoking in common areas, restrictions on pet ownership (type, size, or number), noise curfews, rules about renovation works (times permitted, types of works requiring approval, deposit requirements), guest and visitor access to facilities, and restrictions on the use of facilities (e.g. pool hours, gym booking system). By-laws are enforceable by the MCST. A subsidiary proprietor or occupier in breach of a by-law can be issued a written notice to comply, and persistent breach can result in the MCST applying to the Strata Titles Board (STB) for a compliance order.

| Type of Resolution | Threshold | Common Uses | Legal Basis |

|---|---|---|---|

| Ordinary Resolution | Simple majority of votes cast | Approval of annual budget, election of Council, appointment of MA | BMSMA s.28(1) |

| Special Resolution | 75% of votes cast | Adding/changing by-laws, special levy, withdrawal from Sinking Fund | BMSMA s.28(2) |

| Unanimous Resolution | 100% of all subsidiary proprietors | Amalgamating or subdividing lots, altering the strata plan | BMSMA s.28(3) |

| En Bloc (LTSA) — 10+ yr | 80% of share value and floor area | Collective sale of the entire development | LTSA s.84A |

| En Bloc (LTSA) — under 10 yr | 90% of share value and floor area | Collective sale of newer development | LTSA s.84A |

En Bloc Collective Sale — How Strata Law Enables It

One of the most significant aspects of Singapore’s strata law is the provision for en bloc collective sale under section 84A of the Land Titles (Strata) Act. This allows a majority of owners in a strata development — measured by both share value and floor area — to force the sale of the entire development, including the minority who may not wish to sell. The objective is to prevent a small number of holdout owners from blocking the redevelopment of ageing buildings where the majority have agreed to sell.

For developments that are at least 10 years old (measured from the date of the Temporary Occupation Permit or Certificate of Statutory Completion, whichever is earlier), the consent threshold is 80% of the total share value and 80% of the total floor area of all lots. For developments less than 10 years old, the threshold rises to 90%. Heritage or conservation properties may require 100% consent, effectively making collective sale impossible without unanimity.

Once the requisite consent is obtained, a Sale Committee is constituted, a marketing agent is appointed, and the development is put up for tender. Following a successful tender, the Strata Titles Board (STB) reviews the transaction to ensure it is not against the interests of minority owners and approves the sale. Dissenting owners may object to the STB on limited grounds (primarily that the transaction is not in good faith or the distribution method is inequitable). Once approved, all owners must sell — dissenting or not.

Worked Example — Monthly Strata Fees for a Typical Singapore Condo Owner

Scenario: Ms Tan owns a 3-bedroom (1,100 sqft) unit in a 300-unit mid-tier condominium in the Rest of Central Region (RCR), completed in 2018. The development has a total share value of 900, and her unit has a share value of 6. The MCST has approved an annual Management Fund budget of S$3,240,000 and a Sinking Fund contribution of S$450,000 for 2026.

Her Management Fund contribution = (6 ÷ 900) × S$3,240,000 ÷ 12 = S$1,800/month (this is on the higher end; mass-market OCR condos typically run S$300–S$500/month for a similar-sized unit). For our illustration using a mid-tier RCR development with extensive facilities (two pools, gym, tennis courts, 24-hour security), S$1,800/month is realistic.

Her Sinking Fund contribution = (6 ÷ 900) × S$450,000 ÷ 12 = S$250/month.

Total monthly strata fees: S$2,050/month. When buying or investing in a strata property, these fees are a real cost of ownership that affects cash flow and net rental yield. A S$4,500/month gross rental income less S$2,050 in strata fees translates to a net rental before tax and other costs of S$2,450/month — a yield compression that buyers often underestimate.

Your Rights as a Subsidiary Proprietor

As a subsidiary proprietor, Singapore law grants you a suite of rights under the BMSMA that the MCST and Council must respect. You have the right to: inspect the MCST’s accounts, rolls, and records (on reasonable notice); attend and vote at all general meetings; stand for election to the Council; receive a notice of any general meeting at least 14 days in advance; challenge any resolution passed in breach of the BMSMA; apply to the STB to resolve disputes with the MCST or neighbouring owners; and receive a copy of the by-laws in force.

You also have responsibilities: to pay your Management Fund and Sinking Fund contributions on time (arrears attract interest), to comply with by-laws, to obtain written approval from the MCST before carrying out renovation works that affect the common property or building structure, and to ensure that your tenants and occupiers also comply with the by-laws.

What Might Come Next for Strata Governance?

Singapore’s strata governance framework has been progressively strengthened over the past decade. The 2017 BMSMA amendments introduced mandatory Council training, tightened the MA licensing regime, and strengthened the STB’s dispute resolution powers. Looking ahead, with an ageing private residential stock and an increasing number of developments approaching the 10-year en bloc window in the late 2020s, observers anticipate further refinements to the collective sale process. The Urban Redevelopment Authority and BCA periodically review the regulatory framework, and industry stakeholders have previously suggested reforms around proxy voting rules, electronic AGMs, and reserve fund adequacy standards.

Frequently Asked Questions

What is the difference between the MCST and the managing agent?

The MCST is the statutory body — it is you and all other owners collectively, and it has legal personality. The managing agent (MA) is a private company appointed by the MCST to carry out day-to-day operational work: collecting fees, managing contractors, maintaining records, and administering the development. The MA acts on behalf of the MCST; it does not own the building or have authority beyond what the MCST’s appointment contract grants. If you disagree with a decision, your recourse is through the Council or at a general meeting of the MCST — not directly with the MA.

What happens if I do not pay my management fees?

Arrears in Management Fund or Sinking Fund contributions accrue interest at the rate specified in the BMSMA. If arrears remain unpaid, the MCST may file a claim in the Magistrate’s Court or District Court to recover the debt. The MCST also has the right to lodge a caveat against your property title, which will prevent you from selling or mortgaging the property until the arrears are cleared. In practice, MCSTs generally issue written demand letters before taking legal action, but persistent non-payment does result in court proceedings and caveats being lodged.

Can I refuse to participate in an en bloc sale?

You may refuse to sign the collective sale agreement — and if the consent threshold is not met, the sale cannot proceed. However, if the requisite threshold (80% or 90%, as applicable) is obtained by other owners and the Strata Titles Board approves the sale, you are legally compelled to sell, even if you object. Your recourse is to object to the STB on specific grounds — primarily that the sale is not in good faith (e.g. the price is grossly inadequate, or there has been a conflict of interest in the sale process) or that the distribution method is inequitable. Pure disagreement with the sale price does not by itself constitute grounds for a successful STB objection if the price was set by a fair open-market process.

Can I carry out renovation works without MCST approval?

It depends on the nature of the works. Cosmetic works within your unit (painting, replacing flooring, changing kitchen cabinets) that do not affect the structure or common property generally do not require MCST approval. However, any works that affect the structure of the building, penetrate the slab, alter the plumbing or electrical systems serving common areas, or involve changes to the facade require the MCST’s written approval. The MCST’s by-laws will set out a renovation approval process and may require a renovation deposit. Carrying out structural works without approval is a by-law breach and can expose you to a compliance order from the STB and liability for any resulting damage to the building or neighbouring units.

How are disputes between neighbours in a strata development resolved?

The first step is usually direct negotiation or mediation facilitated by the managing agent. If that fails, parties may apply to the Strata Titles Board (STB) for mediation or adjudication on matters such as by-law breaches, unauthorised renovation, common property damage, or noise nuisance. The STB is an administrative tribunal — its proceedings are less formal and expensive than court. For disputes that fall outside the STB’s jurisdiction (e.g. pure contract disputes or tortious claims), the regular courts apply. The Community Disputes Resolution Tribunal (CDRT) also handles certain neighbour disputes, particularly noise and harassment.

What is the difference between a strata-titled property and a non-strata property?

A non-strata property — such as a detached or semi-detached house — has a single land title covering the entire lot. The owner owns both the building and the land beneath it outright, with no shared governance obligations. There is no MCST, no management fee, and no collective ownership of common areas. Strata-titled properties (condominiums, ECs, multi-strata commercial buildings) have individual strata lot titles plus shared ownership of common property, governed by the MCST. When comparing landed versus strata properties in Singapore, the absence of monthly maintenance fees is one of the cost advantages of landed property, though landed owners bear the full cost of their own land and building maintenance individually.

Who regulates MCSTs and managing agents in Singapore?

The Building and Construction Authority (BCA), through the Commissioner of Buildings, regulates both MCSTs and managing agents under the BMSMA. All managing agents and their key personnel must be licensed by BCA; BCA maintains a public register of licensed MAs. If an MA is found to be operating without a licence or in breach of the licensing conditions, BCA may revoke the licence and take enforcement action. Subsidiary proprietors who have concerns about their MCST’s governance — for example, accounts not being produced, AGMs not being held, or the MA acting outside its authority — may report these to BCA or apply to the STB for appropriate orders.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- En Bloc Sale Singapore 2026: Complete Guide to Collective Sales

- Singapore EC Complete Guide 2026: Executive Condominium Eligibility, ABSD, MOP and Privatisation

- Singapore Private Property Buying Guide 2026: Eligibility, ABSD, Financing and Process

- Singapore Property Tax Guide 2026: IRAS Annual Value and How to Pay

- Singapore Condo Buying Process 2026: Step-by-Step from Offer to Keys

- Singapore New Launch Condo Buying Guide 2026

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or property management advice. BMSMA provisions, MCST governance rules, en bloc thresholds, and BCA licensing requirements are subject to change. Always verify the current rules with BCA (bca.gov.sg), the Strata Titles Board (stratatb.gov.sg), and SLA (sla.gov.sg) before making any property decisions. For specific legal advice, consult a licensed Singapore lawyer.