Singapore HDB Selling Guide 2026: Step-by-Step Process, Selling Costs, COV and Net Proceeds

Quick Answer: Selling Your HDB Flat in 2026 — Key Facts

- Minimum Occupation Period (MOP): 5 years for standard BTO and resale flats; 10 years for Plus/Prime BTO launched from February 2024. Must be completed before registering intent to sell.

- Selling process: Register Intent to Sell → list flat → grant OTP (21-day validity) → buyer exercises OTP → HDB Resale Portal submission → completion. Typical timeline: 8–16 weeks.

- COV (Cash Over Valuation): if agreed price exceeds HDB valuation, the difference is paid entirely in cash by the buyer. Obtain an HDB Value Report before issuing the OTP.

- Selling costs: agent commission (1–2%), legal fees (~S$2,500–S$4,000), HDB admin fee (S$40). Total cash costs typically S$15,000–S$25,000 for a S$700K flat.

- CPF refund: full CPF principal withdrawn plus accrued interest at 2.5% p.a. returns to your CPF OA — not a cash cost, but reduces your cash proceeds.

- Seller’s Stamp Duty (SSD): 12% (Year 1), 8% (Year 2), 4% (Year 3) of sale price if you sell within 3 years. Zero after 3 years — most HDB sellers are unaffected as MOP exceeds SSD period.

- After selling: 30-month wait to buy a new HDB flat from HDB directly. No restriction on buying an HDB resale flat on the open market.

Why HDB Sellers Need a Clear Strategy in 2026

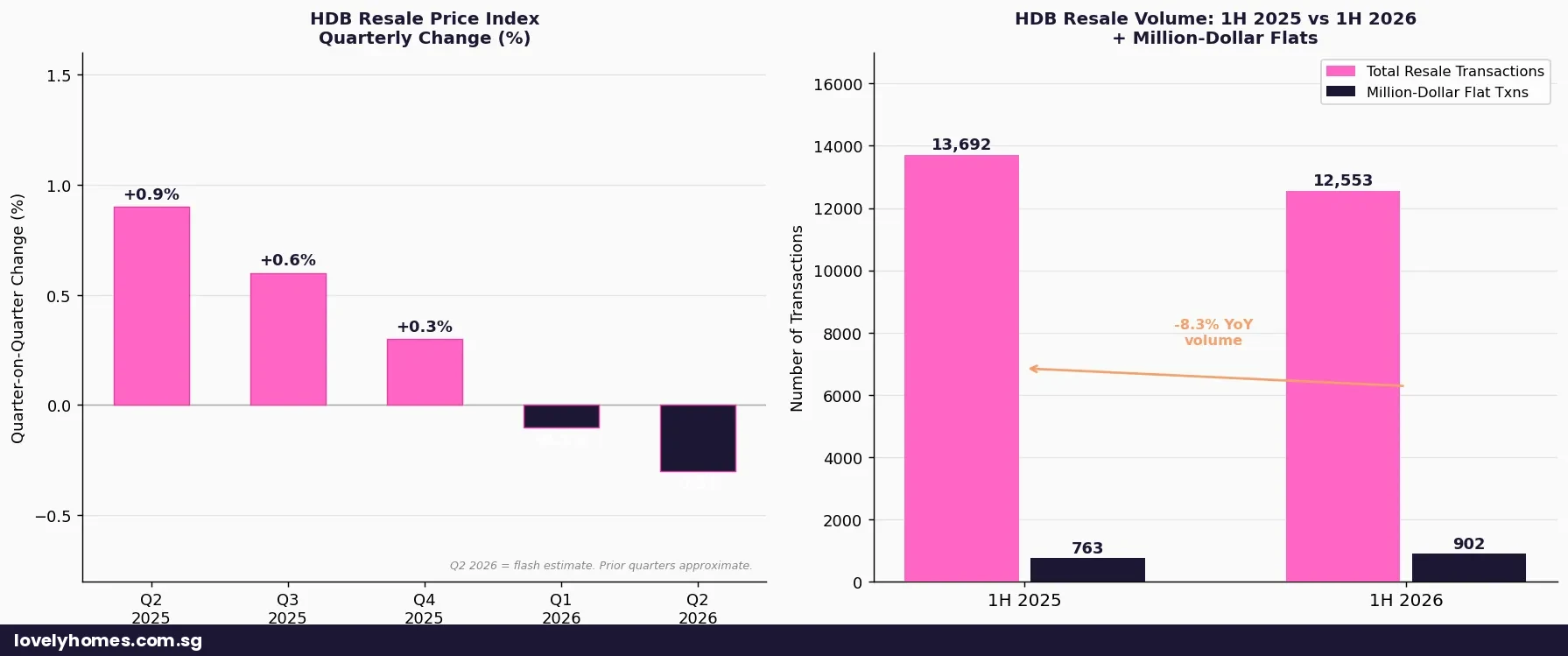

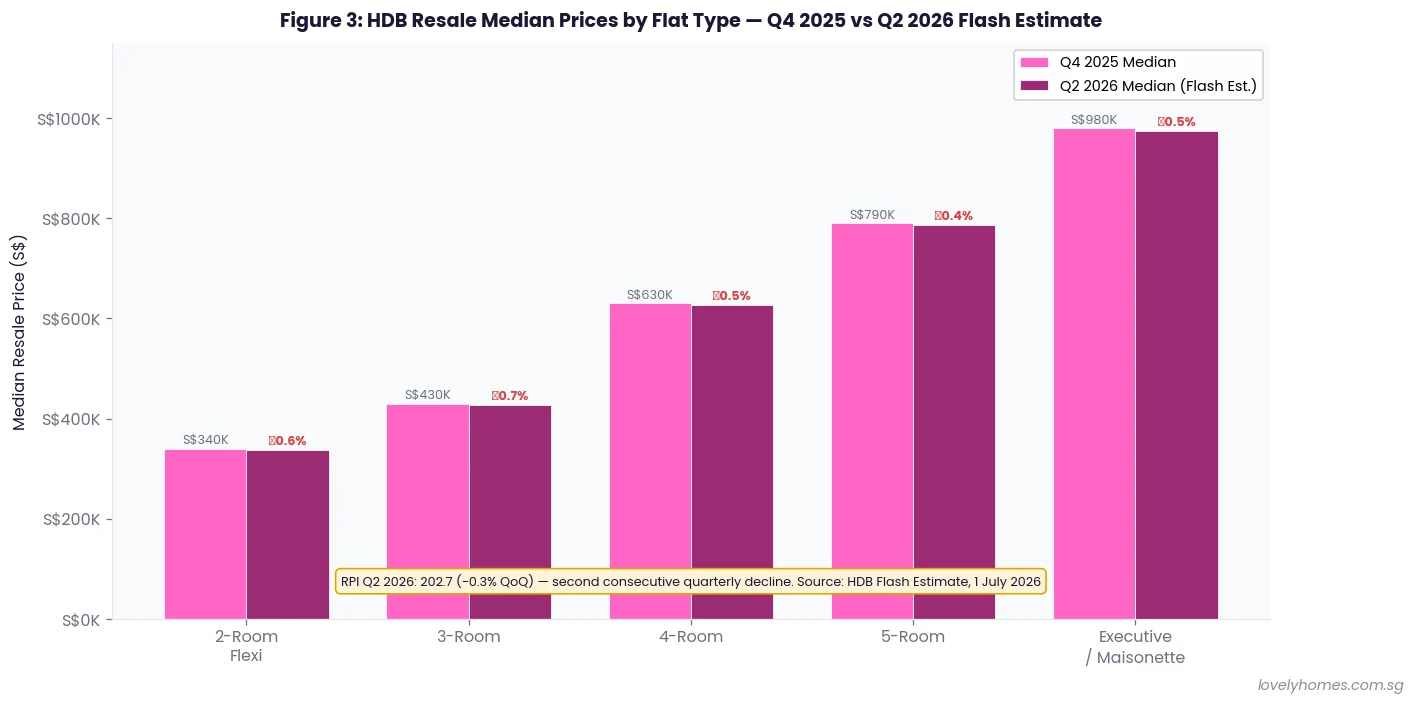

Selling an HDB flat is one of the most significant financial decisions a Singapore household will make. The HDB resale market transacted over 25,000 flats in 2025, with median prices ranging from S$338,000 for a 2-room Flexi to nearly S$975,000 for Executive/Maisonette flats. In the first half of 2026 alone, 902 flats sold for S$1 million or more — a record.

Yet the market is softening. The HDB Resale Price Index fell to 202.7 in Q2 2026 (down 0.3% quarter-on-quarter), the second consecutive quarterly decline — the first back-to-back drop since 2018–2019. For sellers, timing, pricing strategy, and a clear calculation of net proceeds are more important than ever.

This guide walks through the complete HDB selling process, the costs involved, what happens to your CPF and mortgage proceeds, and the rules you need to know before you hand over the keys.

Step 1: Check Your Eligibility — MOP and Other Requirements

Before marketing your flat, confirm you meet all eligibility requirements. The Minimum Occupation Period (MOP) is the most important gate.

Standard flats: 5 years from the date of key collection. If you collected keys on 15 August 2021, your MOP completes on 15 August 2026.

Plus and Prime BTO flats (launched from February 2024 onwards): 10-year MOP. These cover flats in locations deemed highly attractive — near MRT interchanges, city-fringe, or prime area — introduced to slow speculative resale of Government-subsidised units in these locations.

Additional checks: all owners and essential occupiers on the flat must meet citizenship and residency criteria; outstanding HDB loans must be discharged at completion; the flat must not be subject to enforcement action.

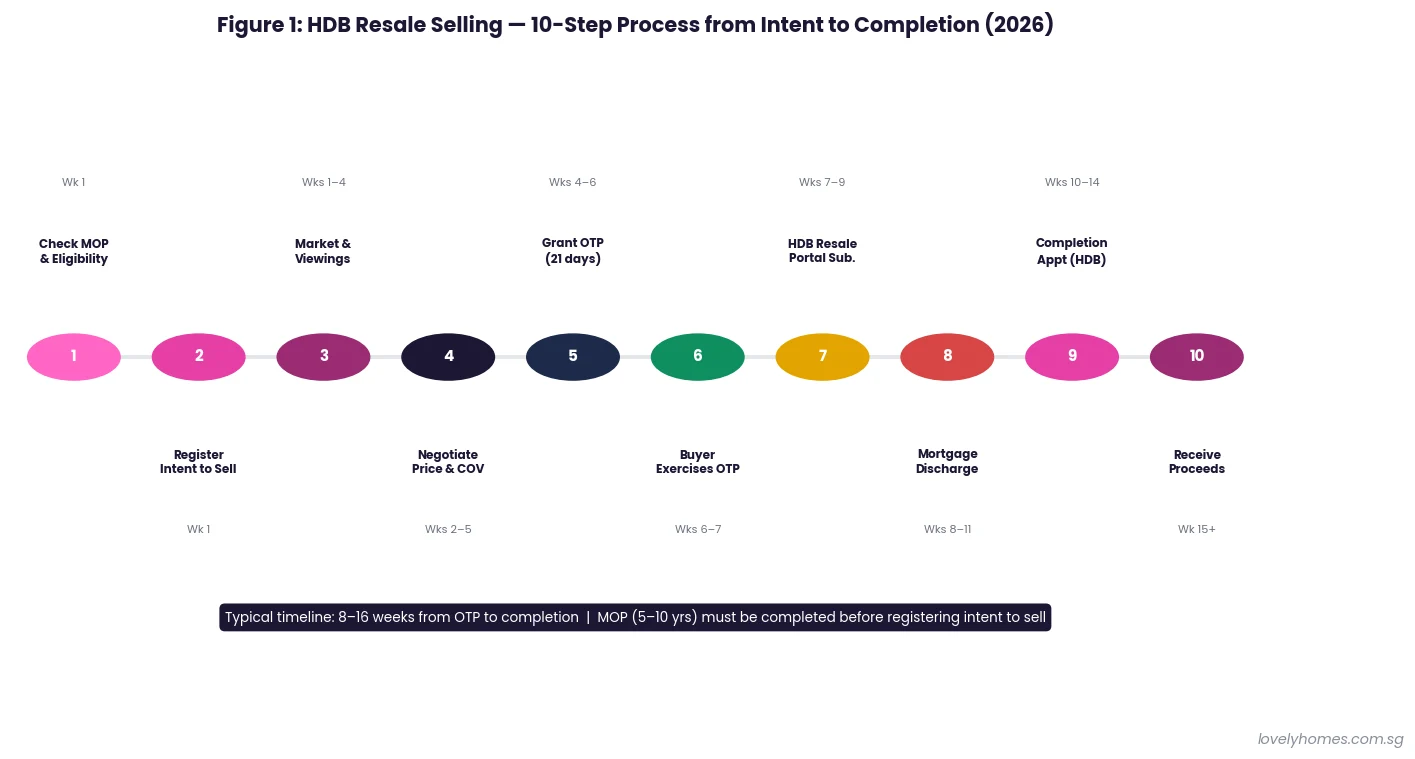

The 10-Step HDB Resale Selling Process

Step 1 — Check MOP and eligibility: Confirm MOP completion via My HDBPage. Review outstanding loan balance and CPF withdrawal history to estimate net proceeds before committing to a price.

Step 2 — Register Intent to Sell (ITS): Submit via HDB Resale Portal. HDB prepares the flat’s valuation and confirms eligibility. ITS valid for 12 months; admin fee S$40 payable by seller.

Step 3 — Market and conduct viewings: List on property platforms via your agent. Prepare an inventory of included fittings. Be transparent about flat condition, remaining lease, and any outstanding arrears.

Step 4 — Negotiate price and COV: If the agreed price exceeds HDB’s valuation, the difference (COV) is paid entirely in cash by the buyer. Obtain an HDB Value Report before issuing the OTP.

Step 5 — Grant Option to Purchase (OTP): Issue the buyer a signed OTP. Option fee is by agreement (typically S$500–S$2,000; minimum S$1). OTP valid 21 calendar days — the buyer’s exclusive right to purchase.

Step 6 — Buyer exercises OTP: Buyer pays exercise fee and countersigns. If the buyer does not exercise within 21 days, OTP lapses and the option fee is forfeited to the seller.

Step 7 — Submit via HDB Resale Portal: Both parties submit their respective portions within 7 calendar days of OTP exercise. HDB assesses eligibility and confirms valuation.

Step 8 — Mortgage discharge: Your solicitor coordinates discharge of any outstanding mortgage. Balance is settled from sale proceeds at completion.

Step 9 — Completion appointment: Scheduled by HDB 4–8 weeks after portal approval. Attend in person (or via authorised solicitor). Sale price paid, mortgage discharged, flat transferred.

Step 10 — Receive proceeds and hand over keys: Net proceeds disbursed. CPF refund credited to your OA. Vacate on or before completion date.

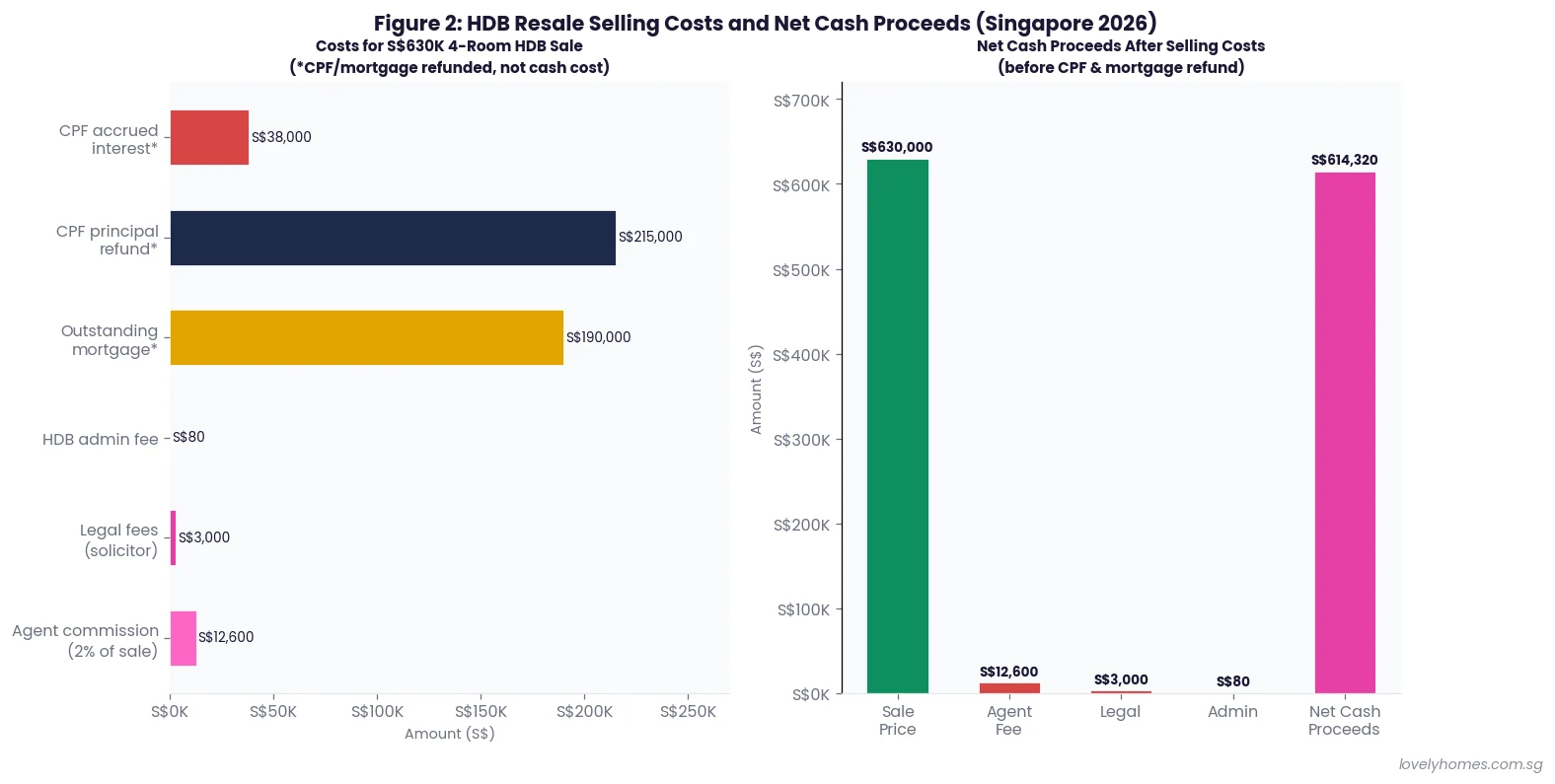

Selling Costs and Net Proceeds

Direct Cash Selling Costs

Agent commission: no mandated rate; market norm is 1–2% of the sale price. On a S$700,000 flat this ranges from S$7,000 to S$14,000. The commission is negotiable and deductible for income tax purposes if the flat is investment property.

Legal fees: solicitor’s fees for conveyancing, CPF redemption, and mortgage discharge typically total S$2,500–S$4,000 all-in.

HDB admin fee: S$40 per party (S$40 buyer, S$40 seller) payable at completion.

Seller’s Stamp Duty: applies only if you sell within 3 years of acquisition: 12% (Year 1), 8% (Year 2), 4% (Year 3). Most HDB sellers pay zero as MOP (5 years) exceeds the SSD period.

CPF Refund — Returned to Your OA, Not a Cash Loss

All CPF OA funds withdrawn for the property — downpayment, stamp duty, and monthly instalments — must be refunded to your CPF OA on sale. The refund amount is the total principal withdrawn plus accrued interest at 2.5% p.a., compounded annually from each withdrawal date. This is not a penalty: it restores to your OA the interest it would have earned had the funds remained invested. You can use the refunded CPF for your next property purchase.

HDB Resale Prices: What to Expect in 2026

The HDB Resale Price Index (RPI) fell 0.3% to 202.7 in Q2 2026 — the second consecutive quarterly decline and the first back-to-back drop since 2018–2019. Transaction volume was approximately 6,268 units in Q2 2026, down year-on-year from peak 2023 levels. Despite the index softening, the million-dollar segment remains buoyant: 491 transactions at S$1M+ in Q2 2026, totalling 902 for the first half of 2026 — up 18.2% year-on-year.

Mainstream 4-room flats in non-mature towns transact at S$550,000–S$680,000; comparable units in mature estates command S$680,000–S$820,000 and above. Sellers in non-mature towns face stiffer competition as BTO completions add supply.

Summary: HDB Resale Selling Reference Table

| Item | Detail | Notes |

|---|---|---|

| MOP (standard) | 5 years from key collection | BTO, resale, DBSS |

| MOP (Plus/Prime) | 10 years from key collection | BTO from Feb 2024 exercise |

| ITS admin fee | S$40 (seller) | HDB Resale Portal; ITS valid 12 months |

| OTP option fee | Typically S$500–S$2,000 | Forfeited if buyer does not exercise |

| OTP validity | 21 calendar days | Exclusive purchase right for buyer |

| Portal submission | Within 7 days of OTP exercise | Both parties submit independently |

| Total timeline | 8–16 weeks (OTP to completion) | Can be faster for straightforward cases |

| Agent commission | 1–2% of sale price | Negotiable; no mandated rate |

| Legal fees | S$2,500–S$4,000 | Conveyancing + discharge disbursements |

| SSD | 12% / 8% / 4% (Years 1–3) | Zero after 3 years |

| CPF refund | Principal + 2.5% p.a. accrued interest | Returns to CPF OA; available for next purchase |

| Post-sale HDB wait | 30 months (new flat from HDB only) | No restriction on buying open-market resale |

Worked Example: Ms Lim Sells Her 5-Room HDB in Ang Mo Kio

Ms Lim (Singapore Citizen) purchased a 5-room BTO in Ang Mo Kio in July 2018 at S$680,000, collecting keys in July 2019. MOP completed July 2024. She lists in May 2026 and agrees a sale price of S$950,000 in July 2026. HDB valuation: S$910,000; COV: S$40,000 (paid in cash by buyer).

Selling costs: agent commission 1.5% = S$14,250 | solicitor S$3,200 | HDB admin S$40 | SSD: S$0 (>3 years). Total cash costs: S$17,490.

Outstanding HDB mortgage balance at completion: S$310,000.

CPF refund (principal + accrued interest): CPF principal withdrawn S$195,000 + accrued interest at 2.5% p.a. over ~7 years = approximately S$38,500. Total: S$233,500 returned to CPF OA.

Net proceeds calculation:

- Sale price: S$950,000

- Less selling costs: −S$17,490

- Less mortgage discharge: −S$310,000

- Less CPF refund (to OA): −S$233,500

- Net cash in hand: S$389,010

- CPF OA receives: S$233,500 (available for next property purchase)

Why Selling Strategy Matters in 2026

The second consecutive quarterly decline in the HDB RPI signals a shift from the 2022–2023 peak. Sellers who price accurately and understand their net proceeds are better positioned to time upgrades effectively. For those planning a move to private property, the six-month ABSD remission window is a critical constraint: buying first and selling HDB within six months allows the 20% ABSD to be refunded, but missing the window is costly.

For sellers in the mature-estate million-dollar bracket — Queenstown, Toa Payoh, Bishan — demand from buyers priced out of private property remains robust. Well-priced flats in these locations can still transact in weeks. In non-mature towns, longer marketing periods and more price negotiation should be expected.

What Might Come Next

Full Q2 2026 HDB resale statistics (detailed breakdown by town, flat type, and storey) are expected from HDB around 23 July 2026. This will refine pricing benchmarks significantly beyond today’s flash estimate. The private property market Q2 2026 data is expected from URA around 24 July 2026, which will also affect HDB upgrader sentiment.

The Government’s Plus and Prime BTO framework — with its 10-year MOP — will structurally reduce the resale supply of well-located flats from these exercises over the next decade. If the pipeline of Plus/Prime launches grows, it could tighten supply of highly sought-after locations in the medium-term resale market post-2034, providing a price floor for existing mature-estate stock.

Frequently Asked Questions

Should I sell my HDB flat first or buy a new property first?

Selling first avoids the risk of owning two properties simultaneously and paying the 20% Additional Buyer’s Stamp Duty (ABSD) on the second purchase for SC couples. However, it creates the risk of being between homes. The Government’s ABSD remission policy for SC couples allows you to buy a private property first, pay ABSD, then sell your HDB within six months and apply for a full refund — effectively enabling a ‘buy-first’ strategy with a large cash float. See our detailed HDB Upgrader Guide 2026 for the full analysis.

What is COV and must I accept an offer with COV?

COV (Cash Over Valuation) is the difference between the agreed sale price and HDB’s official valuation. The buyer pays this entirely in cash — it cannot be financed by a mortgage or CPF. As a seller, you are free to ask for any price; there is no legal obligation to sell at valuation. However, demanding a high COV in a softening market may prolong your flat’s time on the market. Obtain an HDB Value Report before issuing the OTP so both parties can negotiate with full knowledge of the valuation.

What happens to my CPF accrued interest when I sell?

When you sell, the full CPF principal withdrawn for the property, plus accrued interest at 2.5% p.a. (the CPF OA rate) compounded annually from each withdrawal date, must be refunded to your CPF OA. This is not a penalty — CPF Board restores the interest your OA would have earned had those funds not been withdrawn. The refund comes from your sale proceeds at completion. You can then use the refunded CPF for your next property purchase subject to CPF usage rules.

Can I stay in my flat after the completion date?

Generally, you must vacate on or before the completion date. However, you may negotiate a deferred completion arrangement with the buyer in the OTP: you agree to complete the sale but retain occupation for an additional one to three months, paying the buyer an agreed daily occupancy fee. HDB permits deferred completion arrangements of up to six months; beyond that, HDB’s prior approval is needed. This arrangement must be documented in writing at the OTP stage.

What is the 30-month waiting period and when does it apply?

After selling an HDB flat, there is a 30-month waiting period before you may purchase a new HDB flat directly from HDB (BTO, Sale of Balance Flat exercise, or any HDB-initiated sale). This rule does not apply to buying a resale HDB flat on the open market — you may do so immediately after your current flat’s completion, subject to eligibility. The 30-month rule prevents sequential subsidised-housing transactions that would undermine HDB’s housing subsidies framework.

Do I have to pay Seller’s Stamp Duty on my HDB flat?

Seller’s Stamp Duty (SSD) applies only if you sell within three years of acquiring the flat. Rates: 12% (Year 1), 8% (Year 2), 4% (Year 3) of sale price or market value, whichever is higher. Most HDB sellers are unaffected because the Minimum Occupation Period of five years exceeds the three-year SSD window. Sellers who acquired a flat through extraordinary means (inheritance, court order) should consult a solicitor, as IRAS may assess SSD in some cases.