Published: 17 May 2026 | Sources: URA, EdgeProp, The Edge Singapore, Stacked Homes

Quick Answer: What Is the Bayshore Drive GLS and Why Does It Matter?

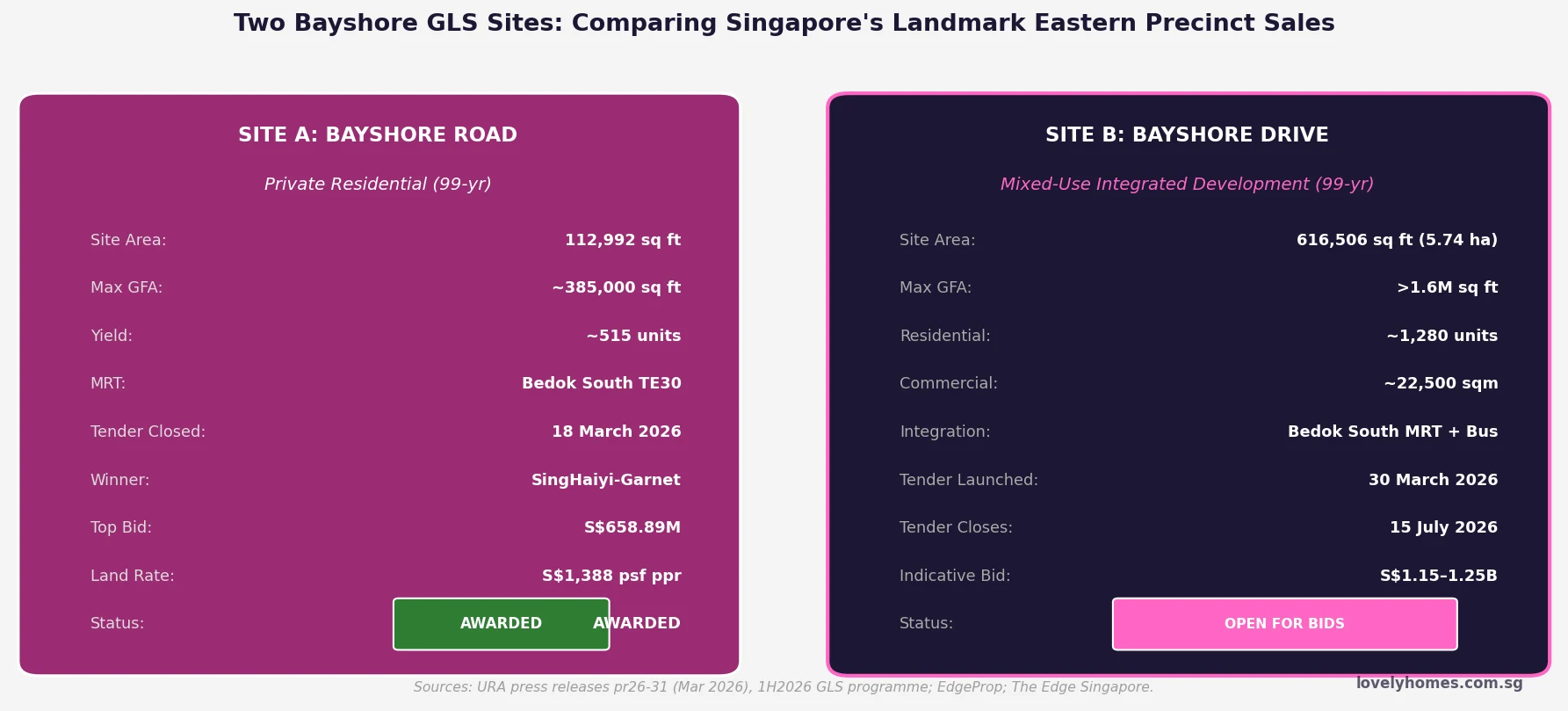

The Bayshore Drive mixed-use GLS site is the second government land sale in the Bayshore precinct and the sole mixed-use plot in the URA’s 1H 2026 GLS Programme.

At 5.74 hectares (616,506 sq ft) with a maximum GFA of over 1.6 million sq ft, it is one of Singapore’s largest single GLS sites in years.

The site can yield approximately 1,280 residential units plus around 22,500 sqm of commercial space, integrated with Bedok South MRT (TE30) and a new bus interchange.

Tender closes 15 July 2026 at noon. Industry analysts forecast 2–6 bids with the top bid reaching S$1.15–S$1.25 billion (S$1,150–S$1,250 psf ppr).

The first Bayshore GLS site (Bayshore Road, private residential, 515 units) was awarded to SingHaiyi-Garnet at S$1,388 psf ppr in March 2026 — a land rate record for the eastern precinct.

When completed (estimated late 2030s), the development will anchor Singapore’s newest 60-hectare waterfront residential estate on the Eastern tip of the island.

Singapore’s Next Landmark: The Bayshore Precinct Takes Shape

The Urban Redevelopment Authority (URA) launched the tender for the Bayshore Drive mixed-use Government Land Sale (GLS) site on 30 March 2026, marking a significant milestone for Singapore’s eastern waterfront development agenda. The tender — which closes on 15 July 2026 at noon — is for a 99-year leasehold plot that will become the centrepiece of the Bayshore precinct, a new 60-hectare estate that URA has been planning since its 2019 Master Plan.

The Bayshore precinct is positioned between East Coast Park and the upcoming Thomson-East Coast Line (TEL) corridor, flanking the Bedok South (TE30) and Bayshore (TE29) MRT stations. It is envisioned as a car-lite, green-intensive residential and commercial node — and with two major GLS tenders now in play, the precinct is transitioning from long-term planning aspiration to concrete development reality.

Figure 1: Two Bayshore GLS sites in 2026 — Site A (Bayshore Road, awarded March 2026) vs Site B (Bayshore Drive, tender closes July 2026). Sources: URA, EdgeProp.

Site B: The Bayshore Drive Mixed-Use Plot in Detail

The Bayshore Drive site (referred to as “Site B” in this analysis) is materially larger and more complex than the Bayshore Road residential plot (Site A). Key specifications:

Parameter

Details

Site area

616,506 sq ft (5.74 hectares)

Tenure

99-year leasehold

Maximum GFA

>1.6 million sq ft

Residential yield

~1,280 units

Commercial component

~22,500 sqm (minimum requirement)

Infrastructure integration

Bedok South MRT (TE30), new bus interchange, pedestrian/cycling paths

Tender launched

30 March 2026

Tender closes

15 July 2026, 12:00 noon

Expected bids

2–6 developer consortiums

Indicative top bid

S$1.15B–S$1.25B (S$1,150–S$1,250 psf ppr)

The commercial requirement of 22,500 sqm is significant — it ensures that the successful developer cannot treat the site as a purely residential play, but must deliver a meaningful retail, food and beverage, and services podium that will serve the wider Bayshore community. This mirrors the model used at major integrated developments such as Tampines Mall/Century Square (integrated with Tampines MRT) and Bedok Residences (integrated with Bedok MRT). At 1,280 residential units above a commercial podium and an MRT station, the Bayshore Drive development is likely to be branded and marketed as one of Singapore’s most ambitious integrated residential projects since One-North Eden or Tengah Town.

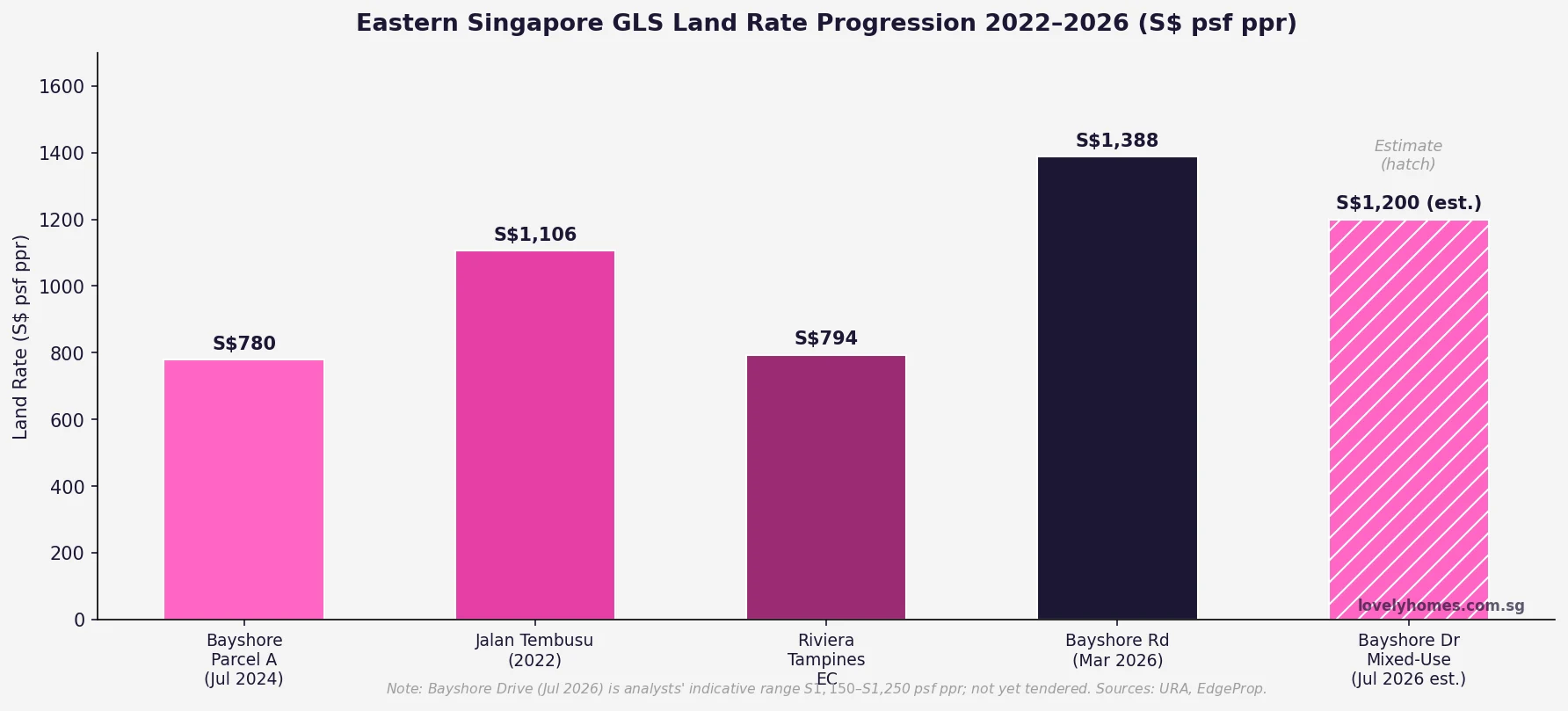

Figure 2: Eastern Singapore GLS land rate progression 2022–2026 in S$ psf ppr. Bayshore Drive (July 2026) is analysts’ indicative range; not yet awarded. Sources: URA, EdgeProp, The Edge Singapore.

Site A: What the Bayshore Road Award Tells Us About Site B Pricing

The Bayshore Road residential GLS site (Site A) provides the clearest pricing anchor for analysing Site B. That tender closed on 18 March 2026 with eight bids — the highest number of bids for a private residential GLS site since January 2022 — with SingHaiyi-Garnet submitting the top bid of S$658.89M, or S$1,388 psf per plot ratio (ppr). The second-highest bid came within 2% of the winner’s, indicating strong developer conviction about the precinct’s value proposition.

For Site B, the calculus is different. The mixed-use mandate (22,500 sqm of commercial space) adds operational complexity and carries some development risk relative to a pure residential site. However, the MRT and bus interchange integration provides substantial anchor value — both through the captive retail audience and through the premium pricing that integrated developments command versus stand-alone condominiums. Industry analysts suggest the mixed-use overlay could support a somewhat lower land rate (S$1,150–S$1,250 psf ppr) than the residential-only Site A (S$1,388 psf ppr), but the sheer scale of the site means total bid values could still reach S$1.84B–S$2B.

Worked Example: What the Bayshore Drive Development Might Cost Buyers

Indicative Breakeven and Launch Pricing

Assuming the winning bid lands at S$1,200 psf ppr (within the forecast range):

Land cost: S$1,200 × estimated GFA ~1.6M sq ft = ~S$1.92B.

Adding construction (~S$500–S$600 psf of GFA), professional fees, finance, and developer margin (~15%), the all-in development cost suggests a breakeven of approximately S$2,400–S$2,600 psf on the residential component.

Indicative launch price (typically 15%–20% margin above breakeven): S$2,750–S$3,100 psf.

Typical 2-bedroom unit (700–800 sqft): approximately S$1.93M–S$2.48M.

Typical 3-bedroom unit (1,000–1,100 sqft): approximately S$2.75M–S$3.41M.

For a SC buyer purchasing a 2-bedroom unit at S$2.2M as a first private property:

BSD = S$3,600 + S$3,600 + S$19,200 + S$26,000 + (S$200,000 × 5%) = ~S$62,400. ABSD: 0% (first property).

Down payment (25%): S$550,000. Bank loan (75% LTV, S$1,650,000 @ 1.80% fixed): ~S$5,838/month. TDSR requires minimum gross household income of ~S$10,600/month to qualify.

What the Bayshore Development Means for Surrounding Property

The progressive build-out of Bayshore precinct is exerting an upward force on property values across the southern Bedok estate, particularly for units along or near the TEL corridor. The Bedok South Horizon HDB cluster’s record-breaking S$1.17M 4-room transaction in April 2026 — at S$1,168 psf, within spitting distance of nearby condominium prices — is a direct manifestation of this precinct-lift effect. As the Bayshore Drive development progresses from tender to construction to completion (likely 2031–2033), each milestone is expected to ratchet up capital values for both existing resale condominiums (Bayshore Park, Savannah CondoPark, Costa del Sol) and newly MOP-ed HDB flats in the Bedok South area.

For investors, the key question is whether the current resale condominiums in the Bayshore belt — trading at S$1,200–S$1,500 psf for older 99-year leasehold stock — offer sufficient margin of safety relative to new-launch pricing at S$2,750–S$3,100 psf. The wide gap suggests that legacy stock currently looks relatively attractive on a PSF basis, though age and remaining lease tenure must be factored into any long-term return analysis.

FAQ: Bayshore Drive GLS Tender 2026

When does the Bayshore Drive GLS tender close?

The tender closes on 15 July 2026 at 12:00 noon. URA typically takes 2–4 weeks to evaluate bids and announce the winning developer, so the result is expected around August 2026. Once awarded, the developer has a set construction commencement period (typically 12–24 months) and a completion deadline specified in the GLS conditions.

Can members of the public bid on a GLS site?

No. GLS tender submissions are open to licensed housing developers only, not individual buyers. Individual buyers will have the opportunity to purchase units from the developer once the project is launched for sale — typically 2–3 years after the GLS award, following design approval, building plan submission, and construction commencement. Buyers interested in the Bayshore Drive development should track URA’s project approval notices and register their interest with the eventual developer once pre-sales commence.

Why is the Bayshore precinct significant for Singapore’s property market?

Bayshore is one of the last large-scale undeveloped coastal precincts in Singapore, sitting between the established Bedok estate and the East Coast Park waterfront. Its 60-hectare footprint, combined with the TEL’s Bedok South and Bayshore stations, positions it as a greenfield opportunity comparable in scope to the earlier development of Tampines, Punggol, and — more recently — Tengah. The two 2026 GLS sites have confirmed developer confidence in the precinct and put a market-clearing price on Bayshore land. Once the integrated development is completed, Bayshore will have a fully formed commercial podium, an MRT-integrated community, and direct park-connector access to East Coast Park — a lifestyle combination that currently commands S$3,000+ psf only in CCR districts like Orchard or River Valley.

How does the Bayshore Drive site compare to other mixed-use GLS awards?

The Bayshore Drive site’s 1,280-unit yield and 22,500 sqm commercial mandate place it in the tier of Singapore’s largest mixed-use integrated developments. Comparable precedents include the Canberra MRT integrated development (~700 units + retail), Tampines Ave 11 mixed-use (1,190 units, commercial podium, awarded 2023), and the Holland Village mixed-use extension. At S$1.15–S$1.25B indicative bid, it would represent the largest single land transaction in Singapore’s eastern region, underscoring the government’s confidence that the Bayshore precinct can sustain premium pricing while still delivering meaningful supply to the market.

Should I buy near Bayshore now before the GLS development is completed?

This is an investment decision that depends on your holding period, risk tolerance, and financial profile — and LovelyHomes does not provide personalised investment advice. The general market view is that legacy resale condominiums in the Bayshore/Bedok South belt (Bayshore Park, Savannah CondoPark, etc.) offer a significant PSF discount relative to what new Bayshore launches are expected to cost. However, these older projects carry shorter remaining leasehold tenures (typically 40–55 years remaining as of 2026), which affects financing options (CPF withdrawal restrictions apply), refinancing, and eventual resale value. Always verify remaining lease tenure via URA’s REALIS before purchasing. Consult a licensed valuerer and financial adviser before committing.

Disclaimer: All pricing forecasts, land rate estimates, and development projections are indicative only and sourced from published analyst commentary and industry research desks as at May 2026. Actual GLS bid results, development timelines, and new-launch pricing may differ materially. This article does not constitute investment advice. Verify all information directly with URA at ura.gov.sg before making any decisions.

Q1 2026 private residential prices (URA PPI) rose an estimated 0.8–1.2% quarter-on-quarter — a continued moderation from the 2021–2022 peak, consistent with the government’s stated aim of sustainable growth.

New home sales rebounded to roughly 3,400 units in Q1 2026 — the strongest quarter since late 2022 — driven by launches including Hudson Place Residences and a pipeline of OCR projects attracting HDB upgraders.

Record supply wave: an estimated 12,400 private residential units are projected to complete in 2026, nearly 65% above the 10-year average. This is the largest single-year pipeline in over a decade.

SORA 3-month has declined from a peak of ~3.72% in early 2024 to approximately 2.48% in April 2026, and is forecast to ease further to 2.30–2.40% by year-end as the US Federal Reserve continues its gradual easing cycle.

The May 2026 EC cooling measures (raising the EC income ceiling to S$16,000 and extending EC MOP) may boost near-term EC demand but reduce second-hand private condo demand at the upgrader tier.

The HDB resale market remains supported by the large MOP cohort (13,484 units in 2026) but faces price headwinds from higher supply and more stringent HDB Plus/Prime resale restrictions.

Investment property outlook: continued compression of gross yields toward the mortgage rate makes leveraged residential investment increasingly return-dependent on capital appreciation rather than income.

Key risk for H2 2026: any reversal of US Federal Reserve easing (e.g., re-acceleration of inflation) that pushes SORA back above 3% would materially increase holding costs and could trigger price corrections in the upper-OCR / RCR segments.

Where Singapore Property Stands at Mid-2026

Singapore’s private residential market enters the second half of 2026 in a state of controlled equilibrium. Prices are stable but not falling; transaction volumes have recovered from the 2023–2024 trough; and the government has maintained its full suite of demand-side cooling measures without any signal of relaxation. The Urban Redevelopment Authority (URA) Q1 2026 flash estimate (released 1 April 2026) showed the Private Residential Property Price Index up approximately 0.8–1.2% quarter-on-quarter — consistent with the 1.0–1.5% per-quarter trend observed since cooling measures were tightened in April 2023.

The headline stability, however, masks significant divergences by segment. Mass-market OCR condominiums have outperformed CCR and RCR on both price growth and transaction volumes, driven by HDB upgrader demand from the record MOP cohort documented in our guide to the HDB MOP Supply Bumper 2026. CCR properties, weighed by the 60% foreigner ABSD and a narrowing pool of domestic investors at current yields, have shown minimal price movement since 2023.

Figure 1: Singapore Private Residential PPI and New Home Sales Q1 2021 – Q4 2026 (Forecast). Sources: URA, editorial projections. Past data is approximate; Q2–Q4 2026 are projections, not official URA forecasts.

The Supply Wave: A Record 12,400 Completions in 2026

The single most consequential factor for the H2 2026 outlook is supply. As a result of the government’s aggressive Government Land Sales (GLS) programme from 2021 to 2023, an estimated 12,400 private residential units are slated for completion in 2026 — approximately 65% above the 10-year average of around 7,500 units per year. The pipeline remains elevated in 2027 at roughly 10,800 units before reverting toward average in 2028. This sustained supply injection is the primary mechanism the government is relying upon to contain price inflation without deploying further demand-side cooling measures.

For renters and rental investors, the supply wave is already visible in the data. As reported in our analysis of the Singapore Private Rental Market Q1 2026, the URA non-landed rental index rose just 0.3% quarter-on-quarter in Q1 2026 — a near-plateau after three years of double-digit annual rental growth. CCR vacancy rates have risen above 10%, and RCR vacancy is approaching that level. OCR remains tighter at 7–9%, supported by HDB upgrader demand and expat families seeking suburban accommodation near international schools.

For owner-occupiers purchasing new launches in H2 2026, the supply wave is a neutral-to-positive factor: more choice, potentially more negotiating power on developer pricing, and a broader resale comparables base when they eventually sell. For investors relying on capital appreciation, the supply headwind is real — historically, periods of above-average residential completions in Singapore have correlated with softer PPI growth in the 12–24 months following peak supply.

The Rate Path: SORA Easing Creates Affordability Tailwind

Figure 2: Residential Supply Pipeline 2022–2028 (left) and SORA 3M / Indicative Mortgage Rate Path 2024–H2 2026 (right). Sources: MAS, industry data, editorial projections.

The Singapore Overnight Rate Average (SORA) — the benchmark for most floating-rate home loans since the phase-out of SIBOR — has fallen from approximately 3.72% (3-month compounded) in early 2024 to around 2.48% as of May 2026. Most analysts project a further decline to 2.30–2.40% by end-2026, contingent on the US Federal Reserve executing two additional 25-basis-point cuts in the second half of the year.

For borrowers on SORA-pegged mortgages (the majority of floating-rate borrowers), this translates into indicative all-in mortgage rates declining from around 3.9–4.2% in early 2024 toward 3.2–3.4% by Q4 2026 — a reduction of roughly 60–80 basis points from peak. On a S$900,000 mortgage over 25 years, this corresponds to monthly instalment savings of approximately S$280–360, meaningfully improving affordability and reducing the cash-flow subsidy required for investment properties.

Borrowers considering whether to refinance or reprice in H2 2026 should weigh the remaining lock-in period and clawback provisions against the declining rate environment. With SORA continuing to ease, there is an argument for delaying a fixed-rate lock-in and remaining on SORA until rates stabilise.

EC Cooling Measures and the Upgrader Pipeline

The Ministry of National Development (MND) announced adjustments to Executive Condominium (EC) rules on 8 May 2026, raising the household income ceiling to S$16,000 (from S$14,000) and extending the EC resale MOP. Our analysis of the EC Cooling Measures May 2026 examined the demand implications in detail. The income ceiling increase is expected to draw some households who previously opted for private condos into the EC segment — a market segment that combines public housing pricing with private amenities — potentially softening demand for the lower end of the OCR private condo market in the S$1.3–1.8M range.

At the same time, the extended MOP for ECs means that the supply of EC units coming to the open market will be deferred — a modest support factor for OCR private prices in the medium term. The net effect on private condo prices is likely to be a modest negative for the S$1.3–1.8M tier but neutral for higher price points.

HDB Resale: Supported by MOP Wave, Restrained by Plus/Prime Rules

The HDB resale market has performed strongly in the first half of 2026, with transaction volumes elevated by the largest MOP cohort on record and the continued million-dollar flat phenomenon (with City Vue @ Henderson setting a S$1.728M record in April 2026). However, the introduction of the HDB Plus and Prime classification (effective from the February 2023 BTO exercise) introduces a structural change in the resale market that will become more visible from 2033 onwards: Plus and Prime flats, when they come to the open resale market, will face income-ceiling restrictions and (for Prime) Singapore-Citizen-only buyer eligibility, which may compress price discovery versus unrestricted Standard resale flats.

In the near term (H2 2026), the HDB resale market remains supported. Demand from buyers priced out of the private market, the continuing Proximity Housing Grant (PHG) of up to S$30,000, and a sustained supply of Standard-classified resale flats from the 2021 MOP cohort all point to stable transaction volumes at 25,000–27,000 transactions per year.

Worked Example: What Easing Rates Mean for a H2 2026 Purchaser

Consider a Singapore Citizen family (the Tans) looking to buy a S$1.4M 3-bedroom OCR condo in Q3 2026 as their first private residential property. They have S$350,000 in downpayment funds (25% of purchase price) and will borrow S$1,050,000 at an indicative floating rate of 3.30% per annum (SORA + spread, as at Q3 2026 projection).

Monthly instalment: S$5,098 (S$1.05M over 25 years at 3.30% pa)

TDSR check: household income required at 55% cap = S$9,269/month minimum; Tan family income S$14,000/month → TDSR 36.4% — passes comfortably.

BSD: S$37,600 on S$1.4M (first S$180k × 1% + next S$180k × 2% + next S$640k × 3% + remaining S$400k × 4%)

ABSD: Nil (first property for Singapore Citizens)

Total cash at completion: Downpayment S$350,000 + BSD S$37,600 + legal fees ~S$4,500 = approximately S$392,100

Compared to an equivalent purchase in Q1 2024 (mortgage rate ~4.1%), the lower rate saves approximately S$350/month — S$105,000 over 25 years in interest, all else equal. The rate tailwind is meaningful for first-time buyers; for investors, it reduces but does not eliminate the negative cash-flow problem at current CCR and RCR yield levels.

What Might Come Next: Key Signals to Watch in H2 2026

Several catalysts could shift the H2 2026 outlook materially in either direction. On the upside, a larger-than-expected US Federal Reserve rate cut cycle could bring SORA below 2% and re-stimulate investor demand that has been dormant since 2022; the launch of major integrated developments (including Sim Lian’s Holland Plain dual-parcel project and potential launches in the Greater Southern Waterfront) could drive a new round of price discovery in the S$2,500–3,500 psf range; and continued strong employment growth in financial services and tech could sustain rental demand at the upper end of the market.

On the downside, a re-acceleration of US inflation forcing the Fed to pause or reverse easing (which occurred briefly in Q1 2024) would push SORA back toward 3% and materially worsen affordability; the record completion pipeline landing simultaneously with rising vacancy could depress rental rates below what investors have modelled; and any policy signal from the government that it is considering further demand-side measures (such as tightening the ABSD for Singapore Citizens on second properties above 20%) would immediately dampen transaction volumes.

The most likely base case for H2 2026 is a continuation of the current equilibrium: private residential prices flat-to-up 1–2% per annum in OCR and HDB resale, moderate transaction volumes, and a gradual improvement in affordability as SORA eases. This is not a bull market for property investors, but it is a stable environment for genuine owner-occupiers looking to buy well.

Frequently Asked Questions

Will Singapore property prices fall in H2 2026?

A broad price correction in Singapore residential property in H2 2026 is not the base-case outlook. The government has consistently demonstrated its willingness to deploy cooling measures to prevent sharp price increases but has not historically used them as a tool to drive prices down. The supply wave and moderating rents create headwinds, but the sustained demand from HDB upgraders and first-time private buyers, combined with easing interest rates, provides a floor. The most vulnerable segments to modest price softening are high-end CCR condominiums (where investment demand has retreated) and rental-heavy RCR units where vacancy is rising. Broad OCR and HDB resale prices are expected to remain stable to modestly positive.

Is now a good time to buy a private condo in Singapore?

For genuine owner-occupiers buying their first or only property, H2 2026 offers a reasonable entry environment: interest rates are declining from their 2023–2024 peak, there is more supply choice than at any time since 2014, and developers are offering more flexible payment schemes and occasional price adjustments on slower-moving units. For investors buying a second residential property (attracting 20% ABSD for Singapore Citizens), the break-even analysis is less compelling — the ABSD alone requires 7+ years of net rental income to recover at current yield levels. The Rental Yield vs Capital Gain guide provides a detailed worked example for investment property decision-making.

How does the 2026 GLS supply wave affect new launch prices?

The 1H 2026 GLS Confirmed List (released December 2025) provides for approximately 4,575 private residential units across nine confirmed sites — 50% above the 10-year average. Historically, a surge in land supply has tempered developer bids (land prices), which in turn constrains the launch prices developers can profitably offer. The Holland Plain Parcel B tender result — where Sim Lian was the sole bidder at S$1,491 psf ppr — illustrates this dynamic: even for a prime District 10 site, developers are bidding cautiously when the land pipeline is generous. This suggests new launch prices in H2 2026 are unlikely to see the sharp upside surprises seen during the 2021–2022 supply drought period.

What is the rental market outlook for H2 2026?

Singapore’s private rental market is transitioning from a supply-deficit landlord’s market (2020–2023) toward a more balanced market as the completion pipeline lands. The URA non-landed rental index — which rose approximately 50% cumulatively between 2020 and 2023 — has essentially plateaued since Q3 2024. In H2 2026, the accelerating supply wave (12,400 completions projected for full year) is expected to increase vacancy further in CCR and RCR and keep rental growth near zero or mildly negative across most segments. OCR and HDB remain tighter, supported by the HDB upgrader cohort — families who have sold their HDB flat but are waiting for their new private purchase to complete often rent in the interim.

Should I lock in a fixed-rate mortgage now or wait for SORA to fall further?

The answer depends on your risk profile and how much further you expect SORA to fall. With SORA at approximately 2.48% (May 2026) and projected at 2.30–2.40% by year-end, most fixed-rate packages are currently priced at 3.0–3.3% per annum for a 2-year lock-in — which does not represent a compelling premium over a SORA-pegged floating package (currently 3.0–3.5% depending on the spread). If you believe SORA will fall below 2% within 12–18 months (which would require aggressive Fed easing), staying on a floating rate makes sense. If you prioritise payment certainty and are concerned about upside rate surprises, a 2-year fixed package at 3.0–3.2% provides a reasonable hedge. The Refinancing Singapore 2026 guide walks through the break-even analysis.

What are the biggest risks to Singapore property in H2 2026?

The three principal risks to the Singapore property outlook in H2 2026 are: (1) a re-acceleration of US inflation forcing the Federal Reserve to maintain or raise rates, which would push SORA back toward 3% and significantly worsen affordability for mortgaged households; (2) a sharper-than-expected vacancy increase in the private rental market causing rental income to fall below what investors have underwritten, triggering some forced selling; and (3) an unexpected government policy tightening — such as an increase in the ABSD for Singapore Citizens on second residential properties above the current 20%. None of these is the base case, but all are plausible tail risks that property investors should model into their downside scenarios.

How does the HDB Plus/Prime classification affect the resale market outlook?

In the near term (2026–2032), the impact is limited — the first Plus and Prime cohorts from the February 2023 BTO exercise will not MOP until around 2033. From 2033 onwards, however, the structural change becomes significant: Plus and Prime resale flats will only be buyable by income-ceiling-eligible households, and Prime resale flats are restricted to Singapore Citizens only. This narrows the effective buyer pool relative to unrestricted Standard resale flats. Property investors or upgraders holding Standard resale flats will be in a structurally stronger position than those whose eventual exit is via a Plus or Prime resale — a point that is often overlooked in discussions of the RFC framework’s impact on resale market dynamics.

This article is a market analysis and commentary for informational purposes only. It does not constitute financial advice, investment advice, or a solicitation to buy or sell any property or financial instrument. All price indices, transaction volumes, SORA projections, and market forecasts are editorial estimates based on publicly available data from URA, HDB, and MAS, and are subject to significant uncertainty. Past market performance is not indicative of future results. Consult a licensed financial adviser and property professional before making any investment or purchase decision.

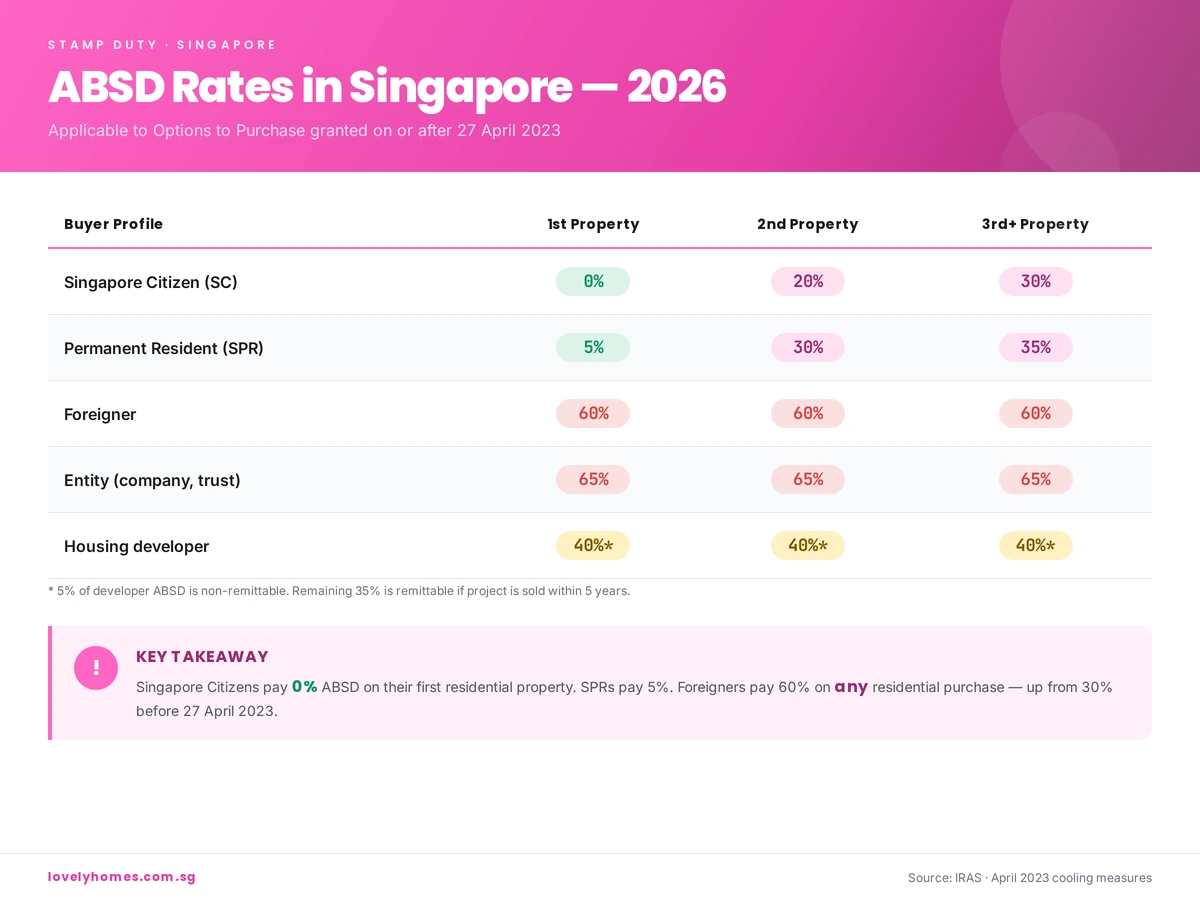

ABSD Singapore — short for Additional Buyer’s Stamp Duty — is the single largest upfront cost most buyers face when purchasing a second (or third, or fourth) residential property in Singapore. If you are buying as a foreigner, ABSD can add 60% of the purchase price to your cost. If you are a Singapore Citizen buying your second property, that figure is 20%. Get this number wrong in your budgeting, and you can very quickly wipe out years of planning.

This guide walks you through exactly how ABSD works in 2026 — who pays, how much, how it is calculated, what remissions are available, and the legitimate strategies property buyers use to manage it. All figures reflect the Government’s 27 April 2023 cooling measures, which remain the applicable framework. For the latest rates, always check the IRAS Additional Buyer’s Stamp Duty page.

Quick Answer — ABSD at a glance

Singapore Citizens: 0% on 1st property, 20% on 2nd, 30% on 3rd+

Singapore PRs: 5% / 30% / 35%

Foreigners: 60% on any residential property

Companies, trusts and other entities: 65%

ABSD is payable within 14 days of signing the Option to Purchase (OTP) or Sale & Purchase Agreement.

What is ABSD and Why Does It Exist?

ABSD is a transaction tax levied on the buyer when acquiring a residential property in Singapore. It sits on top of the regular Buyer’s Stamp Duty (BSD) that every buyer pays. Where BSD is progressive and maxes out at 6% for the portion of price above S$3 million, ABSD is a flat rate applied to the entire purchase price or market value (whichever is higher).

The tax was introduced in December 2011 as part of the Government’s suite of cooling measures — the tools Singapore uses to moderate speculative demand, manage affordability for owner-occupiers, and prevent the kind of runaway price inflation seen in other global cities. Because it targets second-and-subsequent-property buyers and non-citizens disproportionately, ABSD is the single most powerful lever in the cooling-measures toolbox. You can read more about the broader framework in our Property Cooling Measures section.

ABSD Rates in Singapore (2026)

The table below sets out the ABSD rates currently in force. Rates apply based on the profile of the buyer at the time the Option to Purchase (OTP) is granted.

ABSD rates by buyer profile — applicable to OTPs granted on or after 27 April 2023.

Buyer Profile

1st Residential Property

2nd Residential Property

3rd & Subsequent

Singapore Citizen (SC)

0%

20%

30%

Singapore Permanent Resident (SPR)

5%

30%

35%

Foreigner (non-PR individual)

60%

60%

60%

Entity (e.g. company, trustee for a trust)

65%

65%

65%

Housing developer

40%*

40%*

40%*

* 5% of a developer’s ABSD is non-remittable. The remaining 35% is remittable subject to conditions, including selling all units in a qualifying project within five years.

How ABSD is Calculated — A Worked Example

ABSD is applied to the higher of the purchase price or the market value of the property. It is not charged on a tiered basis — the full rate applies to the entire amount.

Example: A Singapore Citizen couple already owns their first home (a 4-room HDB flat). They decide to buy a S$2,000,000 resale condominium in District 15 as an upgrader investment. ABSD on the second property for a Singapore Citizen is 20%.

Purchase price: S$2,000,000

ABSD (20%): S$400,000

BSD (progressive, on S$2m): approximately S$64,600

Total stamp duty payable: S$464,600

That S$400,000 ABSD alone would consume most of the typical upgrader’s CPF and cash reserves. This is why many Singaporean couples take the ‘sell first, buy second’ upgrade route — selling the existing HDB or condo before buying the next home — which we cover later in this guide.

Who Pays ABSD? Exemptions and Special Cases

ABSD applies when you purchase an additional residential property. Commercial property, industrial property, and pure-land parcels are not within its scope. A property is counted toward your “property count” if:

You hold the title as a sole owner, joint tenant, or tenant-in-common;

You are a beneficial owner via a trust;

You are a beneficiary of an estate that holds residential property.

Properties not counted include: properties you merely reside in but do not own (e.g. as a tenant), inherited shares in a deceased estate within the administration period, and certain industrial/commercial units.

Executive Condominiums (ECs)

For new ECs bought directly from the developer during the minimum occupation period of the scheme, ABSD is not triggered because the buyer must commit to an owner-occupier arrangement. ABSD rules apply normally if an EC is purchased on the resale market after its 5-year MOP and 10-year privatisation milestones.

Free Trade Agreement (FTA) Nationals

Citizens and Permanent Residents of countries with which Singapore has an FTA extending National Treatment on stamp duty — namely Iceland, Liechtenstein, Norway, Switzerland, and United States citizens — are accorded the same ABSD treatment as Singapore Citizens. An eligible US citizen buying their first Singapore residential property therefore pays 0% ABSD, not 60%.

ABSD Remission Schemes — How to Get Some (or All) of It Back

Several remission schemes let qualifying buyers claim back part or all of the ABSD they initially pay. The big three to know are:

1. Married Couple Remission (Sale of First Residential Property)

If a Singapore Citizen (or mixed SC & SPR, SC & foreigner) couple buys a replacement home before selling their existing one, they can apply for ABSD remission provided they sell the first property within six months of the later of (a) the date of purchase of the replacement property, or (b) the TOP/CSC date if buying an uncompleted unit. This is effectively a “grace period” that allows upgraders to move without double-paying ABSD.

2. Mixed-Nationality Married Couples

An SC spouse married to a foreigner buying a matrimonial home jointly can enjoy SC rates (rather than foreigner rates) if the property will be used as their matrimonial home and conditions are met. Again, for a first joint home this means 0% ABSD.

3. Developer ABSD Remission

Licensed housing developers pay 40% ABSD upfront (5% non-remittable, 35% remittable) on land purchased for residential development. The 35% is remittable upon meeting development and sales conditions — typically completing the project and selling all units within 5 years.

Remissions must be applied for within strict timeframes (usually 14 days of the triggering event). We strongly recommend engaging a conveyancing lawyer who is experienced in stamp-duty remission applications before signing any OTP where remission will be relied upon.

ABSD vs BSD: What is the Difference?

Every property purchase in Singapore attracts Buyer’s Stamp Duty (BSD), which is a progressive tax on the purchase price:

1% on the first S$180,000

2% on the next S$180,000

3% on the next S$640,000

4% on the next S$500,000

5% on the next S$1,500,000

6% on the portion above S$3,000,000 (residential only)

BSD applies to every buyer; ABSD is the additional layer that may or may not apply depending on your citizenship status and property count. BSD and ABSD are payable together, within 14 days of signing the OTP.

The History of ABSD in Singapore (2011–2026)

Understanding how we arrived at today’s ABSD rates helps you anticipate where the Government may go next. The key milestones:

December 2011: ABSD introduced. Foreigners paid 10%; entities 10%; SPRs 3% on 2nd property; SCs 3% on 3rd+.

January 2013: First major hike. Foreigners to 15%, entities 15%, SPRs 5%/10%, SCs 7%/10% on 2nd/3rd.

July 2018: Rates raised again amid a reflating market. Foreigners to 20%, entities to 25%.

December 2021: Another round. Foreigners to 30%, entities to 35%, SPR 2nd property to 25%, SC 2nd to 17% / 3rd to 25%.

April 2023: The current regime. Foreigners doubled to 60%, entities to 65%, SPR 2nd to 30%, SC 2nd to 20%.

Each tightening has coincided with a period of accelerating private-residential price growth. For a full chronology including LTV, SSD and TDSR changes, see our comprehensive Property Cooling Measures archive.

How to Legally Minimise Your ABSD Bill

ABSD is not optional, but there are a handful of legitimate strategies buyers use to reduce the amount payable or to avoid triggering higher rates:

Sell first, then buy. For couples upgrading, timing the sale of your existing HDB or condo before the purchase of the next means you never hold two properties simultaneously and therefore pay 0% ABSD on the new first home (as an SC).

Use the matrimonial home remission. A mixed SC–foreigner couple buying their matrimonial home jointly enjoys SC rates if structured correctly.

Decouple responsibly. Where one spouse transfers their share of an existing property to the other, only the transferring spouse is freed to buy a second property as a “first” purchase. Decoupling has legal, CPF refund, and mortgage implications — always take specialist advice first.

Consider commercial or industrial property instead. Commercial and industrial properties do not attract ABSD. They have their own financing, GST, and tax considerations — but for investors focused on yield, they are worth analysing. See our Property Investment section for how commercial yields compare with residential.

Look offshore for second and third properties. Singaporeans investing in Malaysia (JB/Iskandar), Thailand, the UK, Australia, or Japan pay no ABSD to the Singapore Government for those purchases. Each destination has its own foreign-buyer regime, which we cover in our Foreign Property Investment guide.

Time your citizenship/PR application carefully. For families where PR or citizenship is in progress, the ABSD profile at the date the OTP is granted determines the rate. Moving the OTP date by a few weeks can, in edge cases, change the applicable rate by 15–25 percentage points.

Frequently Asked Questions

Is ABSD payable on the land value or the built-up value?

ABSD is calculated on the higher of the purchase price or the market value of the property at the time of acquisition. For new launches, this is typically the purchase price; for resale, IRAS may apply an independent market valuation.

When exactly is ABSD due?

Within 14 days from the date of the document triggering the duty — usually the signing of the Option to Purchase (for resale) or the Sale & Purchase Agreement (for new launches). Late payment attracts penalties.

Can CPF be used to pay ABSD?

No. ABSD (like BSD) cannot be paid from CPF directly at the point of purchase — it must be paid in cash. You can, however, apply for CPF reimbursement after the stamping is complete, drawing from your Ordinary Account against the purchase price.

Do I pay ABSD if I inherit a property?

No. A property acquired by way of inheritance is not a purchase and does not attract ABSD on the transfer itself. However, an inherited property does count toward your property count for future purchases.

I already own a commercial shophouse. Do I pay ABSD on my residential condo?

The residential-only count means commercial and industrial holdings are not included in your ABSD property count. If you are a Singapore Citizen buying your first residential property while owning commercial real estate, you still pay 0% ABSD.

How does ABSD affect an Executive Condominium purchase?

Buying a new EC from the developer under the EC scheme does not attract ABSD during the initial owner-occupation period. Once an EC is privatised (10 years after TOP) and traded on the open market, normal ABSD rules apply.

What to Do Next

ABSD changes how much house you can afford, how you time an upgrade, and sometimes whether a purchase makes sense at all. If you are weighing your options right now, we suggest three next steps:

If you are an upgrader, study our Upgrader Guide — the sequencing question (sell first vs buy first) is the single biggest lever for managing ABSD.

Review current market conditions in our Property News and Property Trends sections — if further cooling measures are telegraphed, timing your OTP becomes critical.

Looking at a specific development? Our detailed condo reviews — including One Marina Gardens, Arina East Residences, and our Aurea vs Chuan Park showdown — include the full ABSD-inclusive cost breakdown for various buyer profiles, so you can see the true entry cost before committing.

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. ABSD rates and remission rules change over time. Always verify the current position on the IRAS Stamp Duty page and consult a licensed conveyancing lawyer or tax specialist before acting on any property transaction.

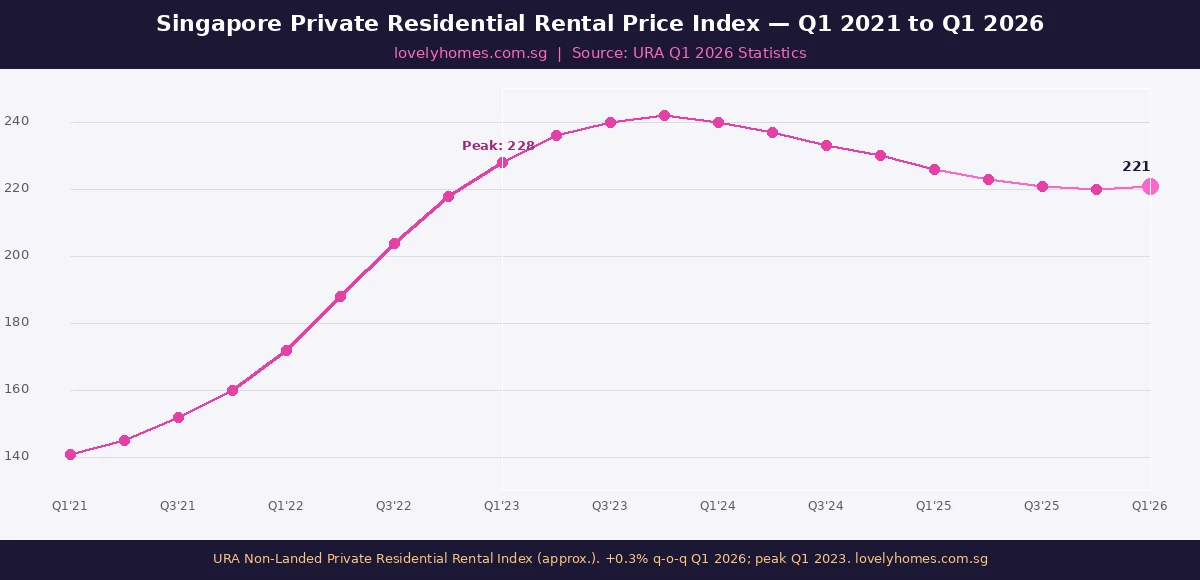

Rental index movement: URA’s non-landed private residential rental price index rose by +0.3% quarter-on-quarter in Q1 2026 — a near-stabilisation after 7 consecutive quarters of decline from the Q1 2023 peak.

Annual context: Over the full year 2025, private residential rents fell approximately 6–8% from their 2023 peak, unwinding roughly a quarter of the surge recorded during 2022–2023.

Supply pipeline: URA’s April 2026 data release confirms approximately 55,800 private housing units (including ECs) in the pipeline for completion over the next several years — a large structural overhang on rents.

HDB rental market: HDB approved subletting of whole flat volumes declined year-on-year in Q1 2026, but the median HDB whole-unit rent remains robust at S$2,500–S$3,200 for 4–5 room flats.

Tenants: Overall negotiating position for tenants improved significantly compared to 2022–2023; vacancy rates for private condos in OCR rose to approximately 7–9% in Q1 2026.

Outlook: Analysts expect private rents to remain broadly flat or edge up 0–2% through 2026 as demand from returning expatriates and work-pass holders partially offsets the supply glut.

When URA released its Q1 2026 full private residential statistics on 24 April 2026, the headline private residential price index grabbed attention: a 0.9% quarter-on-quarter rise, revised sharply upward from the flash estimate of 0.3%. Less remarked upon — but equally significant for landlords, tenants and property investors — was the rental index, which edged up a modest 0.3% in Q1 2026 after seven straight quarters of decline from the market peak in early 2023.

This article provides a comprehensive analysis of the Singapore private rental market in Q1 2026: where rents are, how they got there, which segments and regions are stabilising or still under pressure, and what the large supply pipeline means for landlords and tenants through the remainder of 2026 and into 2027.

Figure 1: URA Non-Landed Private Residential Rental Price Index, Q1 2021–Q1 2026. Rents surged 62% from Q1 2021 to the Q1 2023 peak before declining steadily; Q1 2026 shows the first positive quarterly reading in seven quarters. Source: URA | lovelyhomes.com.sg

Context: The Rental Surge, the Correction, and the Stabilisation

Singapore’s private rental market experienced an extraordinary run between mid-2021 and early 2023. Multiple structural forces converged simultaneously: a pandemic-era construction backlog delayed completions by 12–24 months; returning expatriates and a surge in S-Pass and Employment Pass (EP) holders concentrated demand; and HDB flat owners waiting for their own BTO completions flooded the private rental market. The URA non-landed rental index rose approximately 62% from Q1 2021 to its Q1 2023 peak — an extraordinary appreciation that made Singapore one of the most expensive rental markets in Asia during that window.

From Q2 2023 onwards, the correction was gradual but persistent. Completions of projects deferred from 2021–2022 began hitting the market in waves. Work-pass holders rationalised accommodation costs as global tech hiring slowed. HDB BTO completions (delayed by the construction backlog) began accelerating in 2024, freeing up some demand. By Q4 2025, the private rental index had fallen approximately 7.5% from its peak — unwinding some, but not all, of the pandemic-era gains.

Q1 2026’s +0.3% reading is therefore significant as a directional signal: the rental market has not collapsed back to pre-pandemic levels (as some landlords feared) but has instead stabilised at a level roughly 50% above Q1 2021 values. Whether this represents a floor or merely a pause before further softening depends critically on how quickly the pipeline of 55,800 remaining units is absorbed.

Rental Rates by Segment and Region: Where Is the Value?

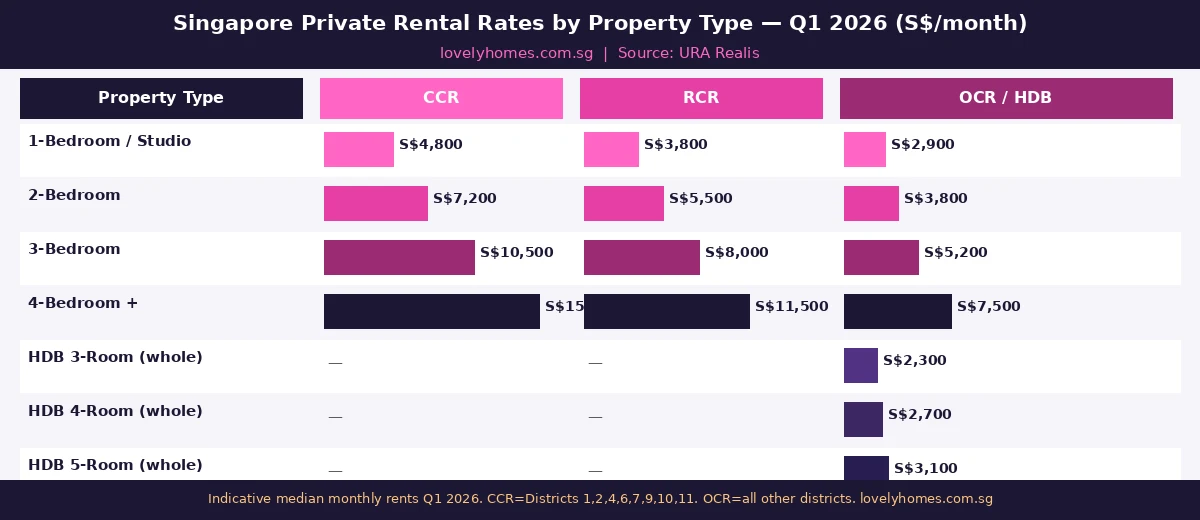

Figure 2: Indicative median monthly rents by property type and URA market segment in Q1 2026. OCR represents the best value-for-money position for most tenant profiles. Source: URA Realis | lovelyhomes.com.sg

The rental market in Q1 2026 is highly segmented by both property type and location. The Core Central Region (CCR — Districts 1, 2, 4, 6, 7, 9, 10, 11) commands the highest rents, but has also seen the largest absolute corrections from its 2023 peak. A 2-bedroom CCR unit that rented for S$8,500–S$10,000 per month in early 2023 now transacts at approximately S$6,800–S$7,500. The Rest of Central Region (RCR) — mid-tier condos in Districts 3, 5, 8, 12–15, 20 — has proven more resilient, driven by domestic upgrader demand and relative affordability compared to CCR.

The Outside Central Region (OCR) is the segment showing the most rental stability in Q1 2026. Tenants priced out of CCR/RCR during the 2022–2023 boom have remained in the OCR, particularly in Tampines, Woodlands, Sengkang and Punggol, where rental yields for private condos remain approximately 3.0–3.5% on a gross basis. The Changi Business Park employment cluster in particular sustains demand for Tampines-area rentals from corporate tenants at rates of S$3,500–S$4,500 per month for a 2-bedroom unit.

Segment

Q1 2023 Median (2BR)

Q1 2026 Median (2BR)

Change

Vacancy Rate (est.)

CCR

~S$8,500

~S$7,200

−15%

~10–12%

RCR

~S$6,500

~S$5,500

−15%

~8–10%

OCR

~S$4,200

~S$3,800

−10%

~7–9%

The Supply Pipeline: 55,800 Units and What It Means

URA’s Q1 2026 statistics confirm a supply pipeline of approximately 55,800 private housing units (including executive condominiums) under construction or approved for construction. This is a substantial number relative to the annual new private housing completion rate of approximately 8,000–12,000 units per year in recent years. Spread across the 2026–2029 window, the pipeline represents approximately 4–7 years of average annual supply at historical absorption rates.

Not all of this supply will hit the rental market simultaneously. Owner-occupied units, units purchased as investment properties by buyers with long-term holding horizons, and units absorbed directly into owner-occupier demand (e.g., from HDB upgraders who sell their flat and move in) do not add to rental supply. In practice, analysts estimate that approximately 20–30% of new private completions in Singapore enter the rental market. On that basis, the pipeline implies approximately 11,000–17,000 additional rental units over the next 3–4 years — a meaningful but not overwhelming increment on a market of approximately 50,000–55,000 rental private residential units.

HDB Rental Market: A Different Dynamic

The HDB whole-unit rental market (subletting of HDB flats with HDB approval) operates differently from the private market. HDB restricts subletting to Singapore Citizens and PRs who are not concurrently buying another property, and enforces minimum subletting periods of 6 months. As a result, the HDB rental market is less volatile than private rentals. In Q1 2026, whole-unit HDB rentals showed modest quarterly softening, but the median whole-unit rent for a 4-room flat across Singapore remains approximately S$2,600–S$2,900 per month — still significantly above pre-pandemic levels of S$1,800–S$2,200. This provides a competitive floor under OCR private condo rents, since tenants choosing between a large well-located HDB flat and a smaller private studio will typically anchor their price comparison to HDB rental rates.

Worked Example: Tampines Investor — Rental Yield Recalculation Q1 2026

Mr Lim purchased a 2-bedroom private condo in Tampines in Q4 2021 for S$1,100,000. He rented it out in Q1 2023 at S$4,400 per month (gross yield 4.8%). By Q1 2026, the same unit rents for approximately S$3,800 per month as competition from new completions in the OCR has increased.

Current gross yield: (S$3,800 × 12) ÷ S$1,100,000 = 4.15%

Net yield (after property tax, maintenance, vacancy 2 mths/yr): approximately 2.8–3.1%

Capital appreciation since purchase: Q1 2026 OCR private condo resale value approximately S$1,370,000 — a gain of approximately S$270,000 (24.5% in 4.5 years)

Total return (rental + capital): approximately S$270,000 (capital) + S$190,000 (cumulative rent collected net of costs) = S$460,000 total return on S$1,100,000 — an annualised return of approximately 8.5%

This illustrates that even with the rental correction, the total return for investors who bought in 2021 and held through to 2026 has been strong, primarily driven by capital appreciation. The rental yield compression is real but manageable for investors with low leverage.

Outlook: Flat to Slightly Positive Rents Through 2026

The consensus view among Singapore property market analysts as of May 2026 is that private rents will remain broadly flat to marginally positive (0–2% growth) through the remainder of 2026. The key supporting factors are: modest improvement in global corporate hiring conditions; Singapore’s ongoing position as a preferred regional base for financial, technology and professional services firms; and the relative affordability of Singapore rentals compared to Hong Kong (which saw a 12–15% rental increase in 2025). The key headwinds remain the large supply pipeline and the stickiness of tenant habits formed during the correction (preference for smaller units, room rentals, or longer-term leases with break clauses).

For tenants, Q1 2026 is arguably the most tenant-friendly rental market Singapore has seen since 2020 — vacancy rates are elevated, landlords are willing to negotiate on fit-out allowances, and lease terms have become more flexible. For landlords and investors, the focus should shift to maintaining occupancy at competitive rents, minimising void periods and monitoring the pipeline of completions in their sub-market.

Frequently Asked Questions

Are Singapore private rents still falling in 2026?

The broad decline has largely stabilised. URA’s Q1 2026 data shows the non-landed private residential rental index rose +0.3% quarter-on-quarter — the first positive reading after seven consecutive quarterly declines from the Q1 2023 peak. However, the recovery is uneven: CCR and RCR rents are still 12–15% below their peak, while OCR rents have declined by a smaller 8–10% and are showing more stable trends. The large supply pipeline of 55,800 units means a sharp rental recovery is unlikely in 2026, but the worst of the correction appears to be behind us.

Which areas in Singapore have the best private rental yields in 2026?

In Q1 2026, the best gross rental yields for private condos are generally found in the OCR, particularly in employment-hub-adjacent towns: Tampines (near Changi Business Park), Woodlands (near Woodlands Regional Centre), Sengkang and Punggol (Seletar Aerospace/Punggol Digital District). Gross yields in these areas are approximately 3.2–4.0% for private condos, compared to 2.5–3.2% in CCR and 2.8–3.5% in RCR. HDB whole-unit rentals in mature OCR estates (Tampines, Bedok, Ang Mo Kio) can generate gross yields of 3.8–4.5% on a resale valuation basis, making them the highest-yielding mainstream residential asset class in Singapore.

Can a foreigner rent a private condo in Singapore?

Yes. Foreigners with valid immigration passes (Employment Pass, S-Pass, Dependent Pass, Long-Term Visit Pass or Student Pass) may rent private residential property in Singapore with no restriction. Foreigners may also rent HDB rooms (but not whole HDB flats unless the flat owner has obtained HDB approval for whole-unit subletting and the tenants meet HDB’s eligibility criteria). There is no cap on the rental amount or tenure for private condos, subject to the landlord’s minimum subletting period (most leases are 1–2 years). Short-term rentals of fewer than 3 months in private residential property are prohibited under the Planning Act and the Housing Agents Act.

Will Singapore rents rise or fall in the second half of 2026?

Most market analysts as of May 2026 expect Singapore private rents to remain broadly flat to slightly positive (0–2% growth) through the second half of 2026. The supply pipeline remains the dominant headwind — with approximately 55,800 private units under construction, completions will continue adding to available rental stock through 2027. However, demand from returning expatriates, regional hub activity and Singapore’s continued attractiveness as a base for financial and technology firms should partially offset supply pressure. The most likely scenario is rental stability with modest sequential gains in the OCR, and continued modest weakness in CCR luxury rentals where supply concentration is highest.

How does Singapore rental income get taxed?

Rental income from Singapore properties is taxable as income under the Income Tax Act and must be declared to IRAS in the annual personal income tax return. For Singapore-based property owners, net rental income (gross rent minus allowable deductions — mortgage interest, property tax, maintenance fees, fire insurance, and a deemed 15% of gross rent for repairs and maintenance if you do not claim actual repair costs) is added to your total income and taxed at your marginal income tax rate. For non-resident individuals (those who are not tax residents of Singapore), rental income is subject to a flat withholding tax rate. IRAS provides a rental income guide on iras.gov.sg, and property owners should retain all receipts for allowable deductions.

Disclaimer: Rental rate figures in this article are indicative estimates based on URA Realis caveat data, HDB rental approval statistics and publicly available market commentary as at May 2026. They are not guaranteed returns and do not constitute investment advice. Actual rental rates vary by floor, facing, renovation standard, lease term and prevailing market conditions at the time of listing. Readers should verify rental benchmarks on URA Realis and consult a MAS-licensed property professional before making any investment decision. LovelyHomes does not provide brokerage services.

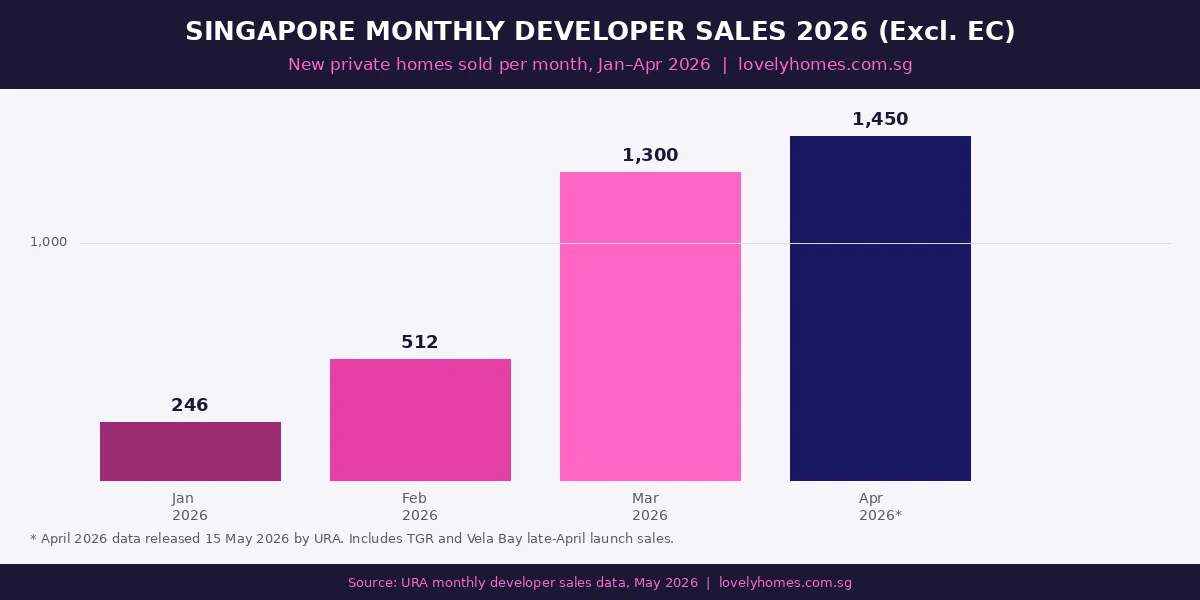

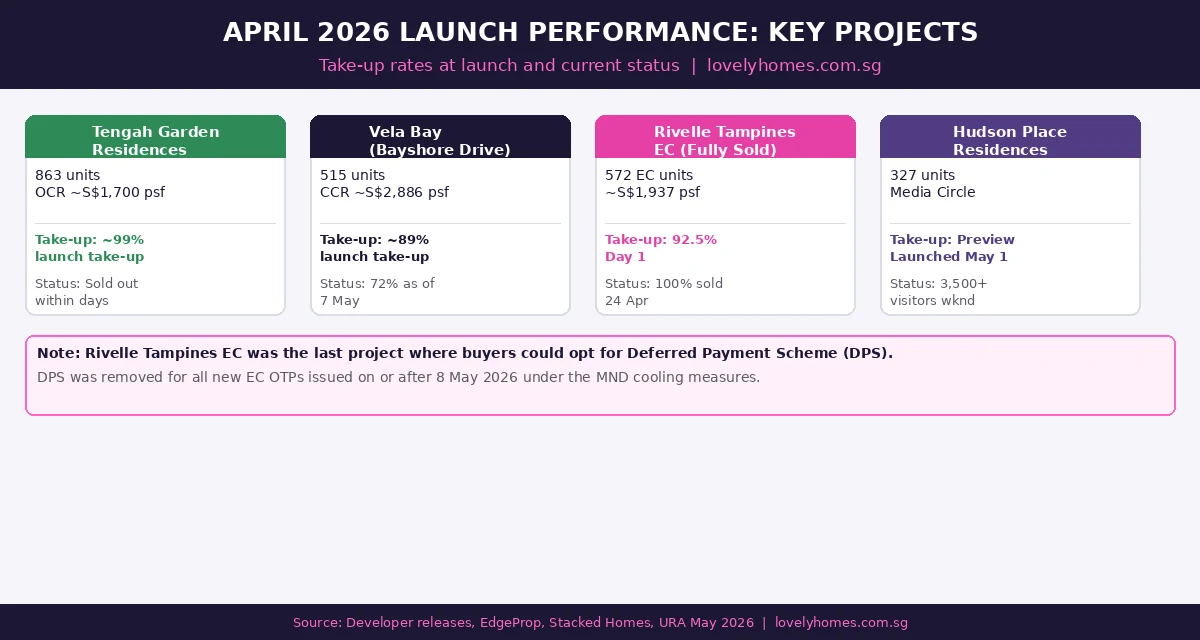

Quick Answer — Singapore Developer Sales April 2026

URA released April 2026 monthly developer sales data on 15 May 2026.

April was driven by two blockbuster late-month launches: Tengah Garden Residences (~863 units, OCR, ~S$1,700 psf) and Vela Bay (515 units, CCR, ~S$2,886 psf), which together cleared approximately 1,224 units in a single 48-hour launch weekend.

Rivelle Tampines EC (572 units) was fully sold out in April — the last EC project in 2026 where buyers could use the Deferred Payment Scheme (DPS) before it was removed on 8 May 2026.

Q2 2026 has begun with stronger momentum than Q1 2026’s 1,294-unit total (which was weaker due to a light launch calendar).

The declining SORA rate (now ~1.20%, down from peak 3.68%) is improving affordability for new home buyers on floating-rate loans.

Key Q2 pipeline still to launch: Lentor Gardens Residences (499 units), and further OCR projects as GLS sites progress.

Singapore’s Urban Redevelopment Authority (URA) released its monthly developer sales statistics for April 2026 on 15 May 2026, and the headline picture is a significant rebound from Q1 2026’s subdued volumes. After a first quarter that recorded just 1,294 new private homes sold excluding executive condominiums — a figure depressed by a deliberately thin launch calendar — April’s late-month double launch of Tengah Garden Residences and Vela Bay changed the narrative.

For buyers, developers, and investors watching Singapore’s new launch market, April 2026 provides several important data points. This article breaks down what the monthly figures show, which projects drove the numbers, what the fully-sold Rivelle Tampines EC tells us about post-cooling-measures demand, and what to expect through the rest of Q2 2026.

1. Q1 2026 in Context: A Quiet Quarter by Design

Before analysing April, it is important to understand why Q1 2026 was so subdued. The 1,294 new private homes sold (excluding ECs) across January to March represented a 60% quarter-on-quarter fall from Q4 2025’s elevated volumes. This was not demand weakness — it reflected a deliberately compressed launch pipeline.

Developers held back launches in early 2026 after the strong 2H 2025 absorption. January saw just 246 units transacted and February approximately 512, both reflecting Lunar New Year seasonality and minimal new launches. March rebounded sharply when Pinery Residences (588 units, 92.3% sold) launched, driving March’s total to approximately 1,300 units — the busiest month of the quarter.

Figure 1: Singapore new private home developer sales by month, January to April 2026. April’s jump reflects the late-month TGR and Vela Bay launches.

2. April’s Headline: The Double Launch Weekend

The defining event of April 2026 was a single late-month launch weekend where two major projects went on sale simultaneously — Tengah Garden Residences (TGR) in the Outside Central Region (OCR) and Vela Bay in Bayshore, Core Central Region (CCR). Together, these two projects accounted for approximately 1,378 units and achieved combined take-up of around 89% in 48 hours, representing roughly 1,224 units sold over one weekend.

The performance of these two launches illustrates a key dynamic in Singapore’s 2026 market: quality supply at the right pricing attracts immediate buyer conviction, even at very different price points. TGR’s OCR pricing (~S$1,700 psf) targets HDB upgraders and first-time private buyers; Vela Bay’s CCR pricing (~S$2,886 psf) targets investment-grade buyers, permanent residents, and high-net-worth individuals comfortable with Singapore’s ABSD framework.

Figure 2: Key project performance in April 2026 — TGR and Vela Bay drove the late-month surge, while Rivelle Tampines EC cleared its final units.

3. Rivelle Tampines EC: The Last DPS Sale of 2026

Rivelle Tampines, the 572-unit executive condominium at Tampines Street 95 developed by Sim Lian Group, completed its sell-out in April 2026. The project had launched on 21 March 2026 with a spectacular 92.5% Day 1 take-up at a median price of S$1,937 psf — the best EC launch since Hundred Palms Residences in 2017. The remaining units were fully taken up during the second ballot on 24 April 2026.

What makes Rivelle Tampines historically significant is that 87.9% of its buyers opted for the Deferred Payment Scheme (DPS) — and all of those OTPs were issued before 8 May 2026, the date on which the Ministry of National Development announced the removal of DPS for new ECs as part of the EC cooling package.

Under DPS, EC buyers need only pay the down payment and service the loan when they collect their keys (typically 3–4 years later), rather than making progressive payments during construction. The scheme was popular among buyers with existing home loans who did not want to service two mortgages simultaneously. With DPS now gone for all new EC OTPs from 8 May 2026 onwards, Rivelle Tampines buyers were effectively the last cohort to benefit.

April’s data, when viewed alongside March’s strength and the EC sell-out, points to an active Q2 2026 for Singapore’s new launch market. Several observations:

Pricing resilience: The fact that both a S$1,700 psf OCR project and a S$2,886 psf CCR project achieved near-90% launch take-up confirms that buyers across different budgets remain engaged when product quality is there. Singapore’s private home price index rose 0.9% in Q1 2026 (revised up from the initial flash estimate of 0.3%) and the pipeline suggests continued modest appreciation.

EC supply adjustment: With DPS removed and MOP doubled to 10 years, the EC buyer calculus has changed. First-timers still benefit from income-ceiling eligibility and lower entry prices than private condos, but the investment horizon is longer and the payment obligation is heavier without DPS. Near-term EC launches (watch for Canberra Drive and Senja Close tenders when awarded) will test this new demand profile.

SORA tailwind: The 1-month SORA rate’s continued decline to approximately 1.20% (from its 3.68% peak in 2023) means floating-rate home loan payments have fallen meaningfully. A buyer with a S$900,000 floating-rate loan at SORA + 0.80% now pays approximately S$3,960/month versus approximately S$5,300/month at peak SORA — a difference of over S$1,300/month. This affordability improvement is supporting buyer confidence across the market. See our home loan comparison guide for the full 2026 rate picture.

Q2 launch pipeline: Several significant projects remain to launch through June 2026. Lentor Gardens Residences (499 units, RCR) is expected to test OCR/RCR crossover pricing. For a broader view of what is coming in 2026’s new launch pipeline, see our New Launch Condo Pipeline article.

Summary Table: Q1–Q2 2026 Developer Sales at a Glance

Period

New Private Homes Sold (excl. EC)

Key Driver

Context

Jan 2026

~246

No major launches; LNY season

Quiet start to year

Feb 2026

~512

Pent-up demand, small projects

Pre-EC announcement

Mar 2026

~1,300

Pinery Residences (92.3% Day 1)

Strongest Q1 month

Apr 2026

~1,450*

TGR + Vela Bay double launch weekend; Rivelle EC cleared

Q2 rebound begins

Q1 2026 Total

1,294 (as at 26 Mar caveat data)

Limited launch calendar

Down 60% q-o-q; set to revise up with full Mar caveats

* April 2026 figure estimated. Official URA data released 15 May 2026; includes late-April TGR and Vela Bay launch sales.

FAQ: Singapore April 2026 Developer Sales

When does URA release monthly developer sales data?

URA releases monthly developer sales statistics on the 15th of the following month. April 2026 data was therefore published on 15 May 2026. The data includes the number of units launched, sold, and unsold for each development, with prices and units based on Options to Purchase (OTPs) issued by developers. The URA e-Service portal (eservice.ura.gov.sg) provides the full data table.

Why was Q1 2026 new home sales so low?

Q1 2026’s 1,294 new private homes sold (excluding ECs) represented a 60% fall from Q4 2025’s elevated levels, but this primarily reflected a thin launch calendar rather than a demand collapse. Developers launched fewer developments in Q1 2026, with only six projects (including two ECs) coming to market. When projects did launch — particularly Pinery Residences in March — they achieved very high take-up rates (92.3% for Pinery), confirming strong underlying buyer demand.

What is Tengah Garden Residences and who is it for?

Tengah Garden Residences (TGR) is an OCR condominium in Tengah, Singapore’s newest housing district in the western region. The project offers approximately 863 units at an indicative price of around S$1,700 psf — competitive for a new OCR launch with direct access to the Tengah Town Centre MRT (Jurong Regional Line) when completed. TGR targets HDB upgraders, first-time private property buyers, and investors seeking yield at OCR price points. It is NOT an EC, so Singapore PRs and foreigners are also eligible to purchase (subject to ABSD).

Can Rivelle Tampines EC buyers still use DPS?

Yes — buyers who received their OTP from Rivelle Tampines before 8 May 2026 are entitled to retain the Deferred Payment Scheme (DPS) arrangements they agreed to. The MND’s announcement removing DPS for ECs applies only to OTPs issued on or after 8 May 2026. Since all Rivelle Tampines units had OTPs issued before that date (the last units were sold on 24 April), those buyers are grandfathered under the old rules.

What EC projects are coming next after Rivelle Tampines?

Singapore’s EC pipeline for the remainder of 2026 and into 2027 includes sites that have been tendered or are awaiting tender under the 1H 2026 GLS programme. Key upcoming EC sites include Canberra Drive and Senja Close. These projects will launch under the new EC framework (10-year MOP, 90% first-timer allocation, no DPS), so their sales performance will be the first real-world test of buyer appetite for the revised rules.

This article is based on URA monthly developer sales data released on 15 May 2026, supplementary reporting from industry sources, and developer announcements. Sales figures for April 2026 include estimates and approximations where official caveat data may not yet be fully lodged. Always verify the most current figures at the URA Property Market Information portal. This is not investment advice. Consult a licensed financial adviser or property consultant before making any property purchase decision.

Hudson Place Residences is a mixed-use residential launch in one-north, Singapore’s established research, technology, media and biomedical hub. The source materials position it for residents who want proximity to the one-north employment base, education cluster and the wider Greater one-north transformation.

Live-Work Demand

one-north is described in the source pack as a 200-hectare business park with a growing professional base across technology, media and biomedical sectors.

Mixed-Use Convenience

The development includes up to 400 sqm of non-strata commercial space on the first storey, adding day-to-day convenience within the estate.

Education Cluster

New Town Primary is stated as within 1 km, with Fairfield Methodist and Queenstown Primary listed in the 1-2 km band. Tanglin Trust, INSEAD, NUS and ACS (I) are highlighted nearby.

Compiled from local source materials dated Jan-Apr 2026

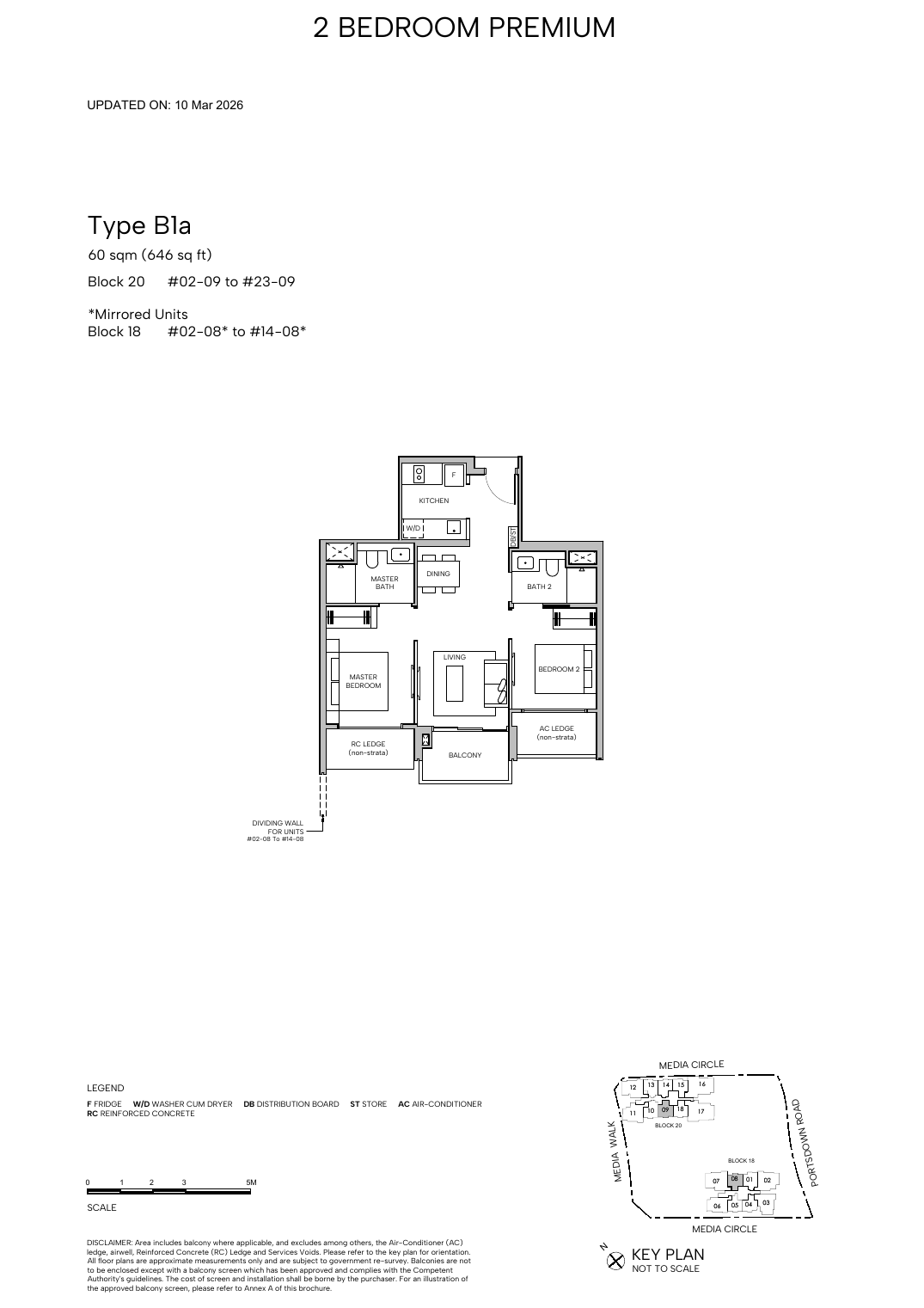

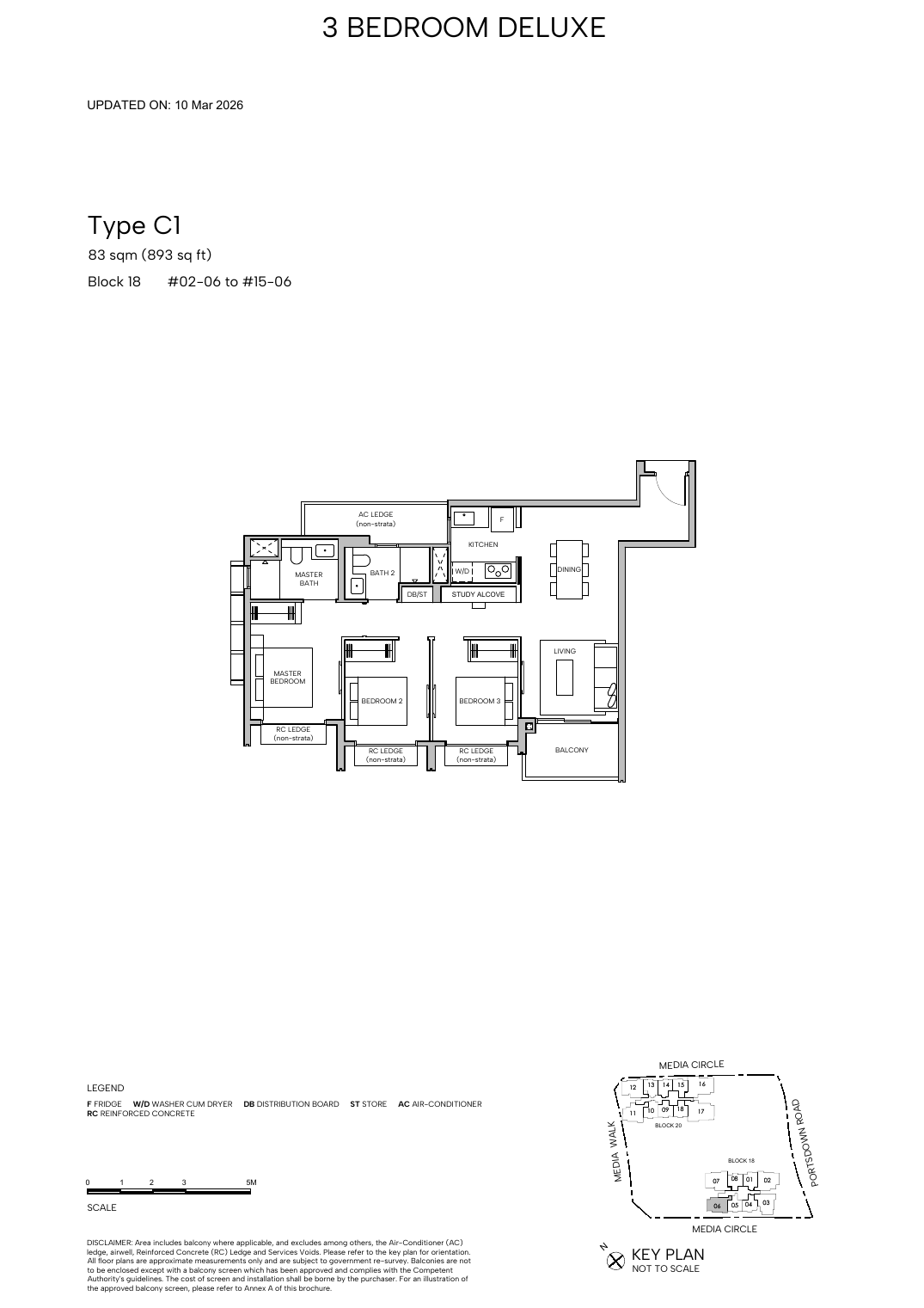

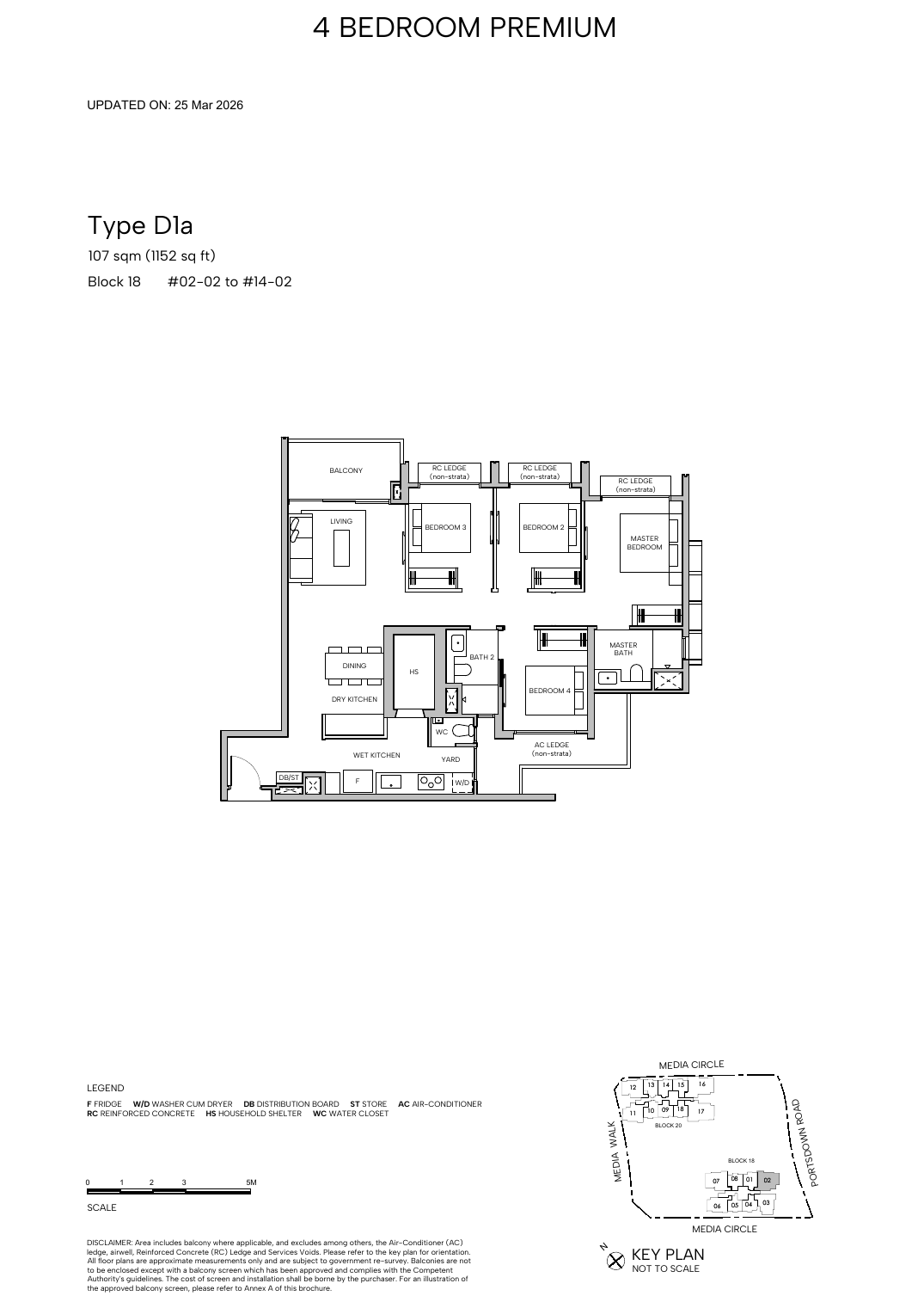

Unit Mix And Indicative Pricing

Unit Type

Typical Area

Source Notes

2-Bedroom Premium

60 sqm / 646 sqft

B1a-B1d

2-Bedroom Premium + Study

64 sqm / 689 sqft

B2-B3

3-Bedroom Deluxe

83 sqm / 893 sqft

C1

3-Bedroom Premium

86-98 sqm / 926-1,055 sqft

C2-C4

4-Bedroom Premium

107 sqm / 1,152 sqft

D1a-D1b

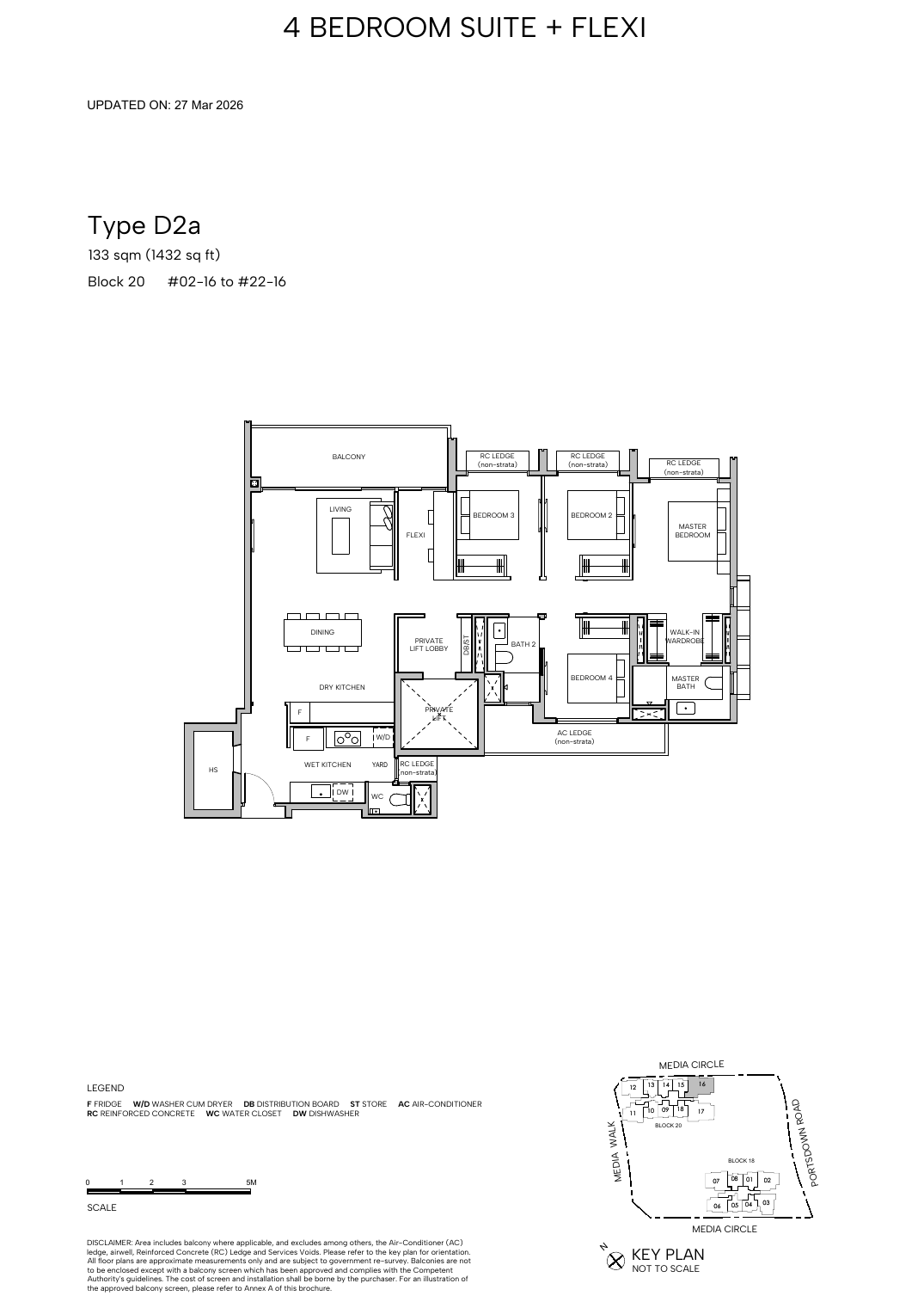

4-Bedroom Suite + Flexi

133 sqm / 1,432 sqft

D2a-D2b

Penthouses

Not stated in floor-plan pack

5 penthouses listed in unit distribution

Pricing note: source marketing materials include indicative examples such as 2-bedroom homes around S$1.5x million and 2-bedroom + study homes around S$1.6x million. Treat all pricing as indicative only and confirm against the latest developer sales package.

Location And Connectivity

Business Park

one-north ecosystem

Home to technology, media, biomedical and research employers across the wider 200-hectare business park.

Roads

AYE / CTE access

Source materials reference major expressway access for islandwide connectivity.

Car-lite

Shuttle mobility

The source pack lists SWAT Mobility, Alice Shuttle and One North Rider options within one-north.

Lifestyle

Star Vista / Ghim Moh / NUS

Source materials highlight nearby retail, market and education nodes in the west.

Schools And Amenities

Within 1km

New Town Primary School, according to source material.

Within 1-2km

Fairfield Methodist School and Queenstown Primary School are listed in the source location pack.

Education cluster

Tanglin Trust, INSEAD, ESSEC, NUS and ACS (I) are highlighted in the project information pack and local project details.

Business demand

The one-north cluster includes MNCs and institutions cited in the source materials, including Grab, SEA, P&G and Razer.

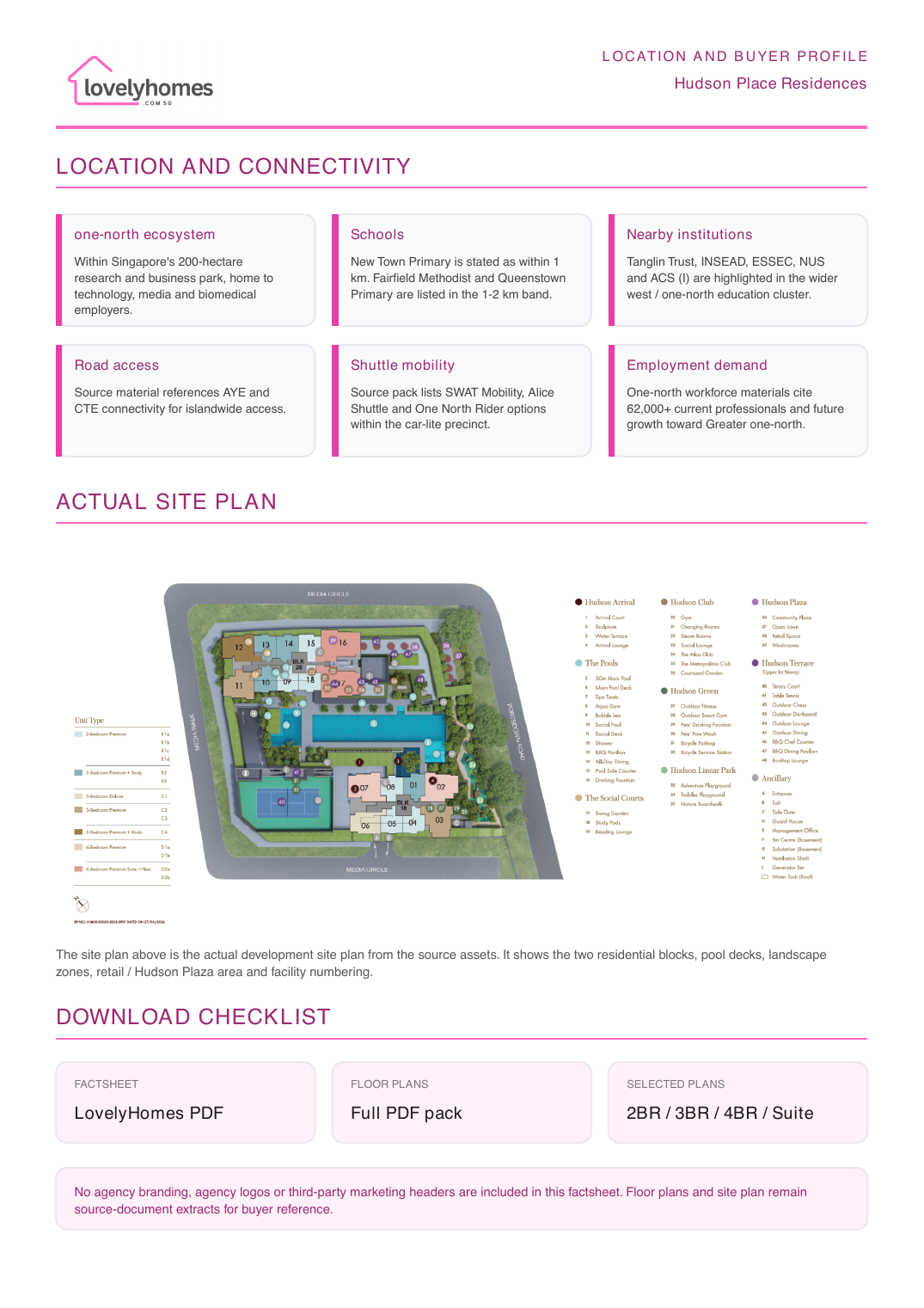

Site Plan

Actual site plan from source material – not a location map or brochure cover.

Facilities And Development Images

Arrival court50m main poolSocial poolTennis courtGymSteam roomsCo-working gardenPet parkOutdoor diningHudson Plaza retail

Selected Floor Plans

Unit-type note: Hudson source materials begin at 2-bedroom homes. No 1-bedroom floor plan or 1-bedroom stack was available in the supplied source floor-plan pack.

2-Bedroom Premium – Type B1a, 60 sqm / 646 sqft

3-Bedroom Deluxe – Type C1, 83 sqm / 893 sqft

4-Bedroom Premium – Type D1a, 107 sqm / 1,152 sqft

4-Bedroom Suite + Flexi – Type D2a, 133 sqm / 1,432 sqft

The project is at 18 and 20 Media Circle in District 5, within the Queenstown / one-north planning area.

How many units are there?

The source project details list 327 apartments, with up to 400 sqm of non-strata commercial space.

Does Hudson Place Residences have 1-bedroom units?

No 1-bedroom stack was provided in the source unit mix or floor-plan pack used for this page. The supplied unit mix starts from 2-bedroom homes.

Which primary school is within 1 km?

New Town Primary School is listed by the source location materials as within 1 km.

Ready to explore Hudson Place Residences?

Speak to LovelyHomes on WhatsApp for the latest availability, pricing and showflat arrangements. We will share the clean factsheet and floor plans for quick review.

Disclaimer. Prices, unit mix, specifications, site plans, floor plans and facility lists are indicative only and subject to change by the developer without notice. Information has been compiled from local source materials including the Hudson Place Residences project details document, information pack, site plan and floor-plan pack, verified for this update on 15 May 2026. LovelyHomes.com.sg is not the project developer. Artist impressions are for illustrative purposes only.

Quick Answer — Chinese capital and Singapore property in 2026

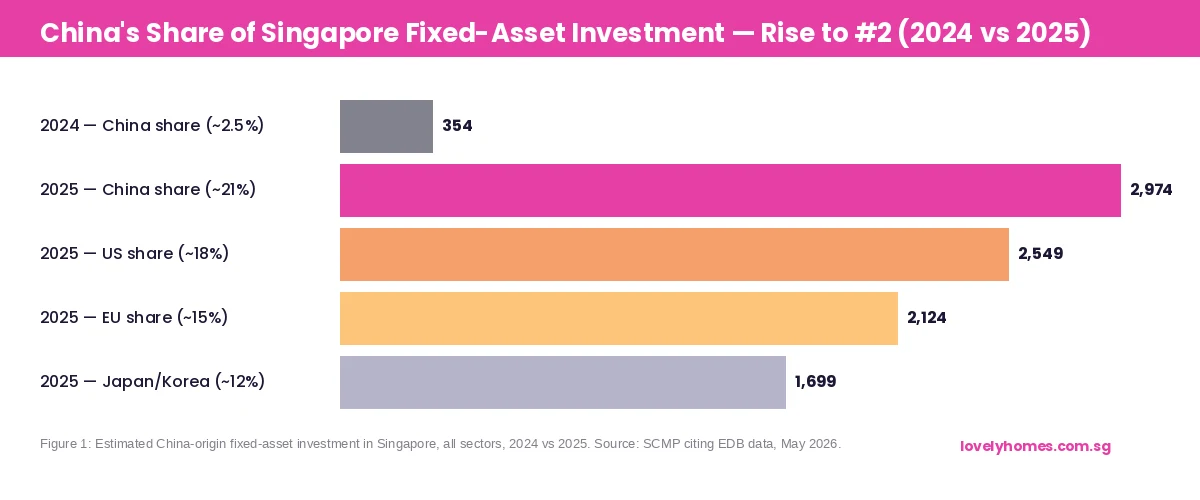

China became the second-largest source of fixed-asset investment in Singapore in 2025, accounting for approximately 21% of S$14.16 billion in total committed fixed-asset investment across all sectors — up from around 2.5% the prior year.

Chinese-linked developers are actively bidding for Government Land Sales (GLS) sites and replenishing their residential land banks in Singapore.

The 60% ABSD on foreign residential purchases has not deterred Chinese developers, who pay 40% developer ABSD (5% non-remittable, 35% remittable on qualifying sale of all units).

Individual Chinese nationals buying Singapore residential property still face the full 60% ABSD on any purchase — there is no bilateral tax treaty carve-out between China and Singapore on ABSD.

The Singapore government has acknowledged the investment flows but has given no indication of relaxing the existing cooling-measures framework in response.

China’s Investment Surge — From Marginal to Major Player

Singapore has always been a destination for global capital. What is new in 2026 is the pace and scale at which mainland Chinese money has repositioned itself within the city-state’s investment ecosystem. According to data cited by South China Morning Post and corroborated by regional financial media in early May 2026, China-origin fixed-asset investment in Singapore across all sectors totalled an estimated S$2.97 billion in 2025 — representing around 21% of Singapore’s total S$14.16 billion in committed fixed-asset investment. This compares to approximately S$354 million (2.5%) in 2024.

The drivers of this shift are multiple and mutually reinforcing. Geopolitical tensions between China and the United States, ongoing uncertainty in Hong Kong’s role as a regional financial hub, a domestic Chinese property market that remains structurally stressed, and Singapore’s well-understood legal and regulatory environment have all contributed to capital outflows from China that disproportionately target Singapore. For Chinese institutional investors, Singapore is familiar — the legal system is English-language common law, property rights are robustly protected, and there is a large existing Mandarin-speaking business community.

Figure 1: Estimated China-origin fixed-asset investment in Singapore vs selected other sources, 2025. Source: SCMP citing EDB data, May 2026.

How This Flows Into the Property Market

Fixed-asset investment encompasses manufacturing plants, data centres, logistics hubs, financial services operations, and real estate. The property-market channel specifically manifests in three ways.

Developer land banking. Chinese-linked property developers — firms with mainland Chinese ownership or significant Chinese institutional backing — have become active bidders in Singapore’s GLS programme. Forsea Holdings (Chinese-owned) was awarded the one-north Queensway residential site in 2025. Qingjian Realty (with Chinese sovereign-fund links via its parent Qingjian Group) remains active in EC and private residential land. These firms are not new to Singapore but their bidding frequency and scale have increased materially since 2024.

Commercial real estate. Chinese institutional investors have been acquiring strata-titled commercial and industrial assets — office floors, retail shophouses, and industrial units — which do not attract ABSD. For investors seeking Singapore-dollar exposure to Singapore real estate without the 60% ABSD drag, commercial property is the natural vehicle. Freehold shophouses along heritage corridors in Districts 1, 2, and 7 have attracted particular interest from Chinese family offices.

Residential purchases by high-net-worth individuals. Despite the 60% ABSD, ultra-high-net-worth (UHNW) Chinese nationals continue to purchase Singapore condominiums and Good Class Bungalows (GCBs). The motivation is not yield — at 60% ABSD, net yields are essentially negligible relative to purchase cost. The motivation is capital preservation, residency (Singapore PR applications are often easier to support when accompanied by a significant economic footprint), and portfolio currency diversification into Singapore dollars.

Figure 2: Selected GLS bids with noted Chinese-linked developer participation, 2024–2026. Source: URA, industry research, LovelyHomes analysis.

The two CCR GLS sites currently on tender — Peck Hay Road (closing 11 June 2026, ~315 units) and River Valley Green Parcel C (closing 18 June 2026, ~470 units) — are expected to attract bids in the S$1,600–S$1,800 psf per plot ratio (ppr) range based on comparable recent transactions. Industry observers cite Chinese-linked developers as likely participants in both tenders, noting that CCR sites present strong brand positioning for marketing to Chinese UHNW buyers, whose preference for Core Central Region addresses remains robust even at 60% ABSD rates. The alternative interpretation is that units are priced to reflect the ABSD cost as part of the marketing proposition for other buyer profiles — mixed-nationality couples, FTA nationals, or Singapore Citizen investors — rather than purely targeting foreign buyers.

Factor

Impact on Singapore Property Market

Chinese developer GLS bids

Supports land price floors; higher bid confidence means higher implied launch prices, positive for existing condo valuations in surrounding areas

Commercial property demand

Compresses shophouse and strata commercial yields; buyers seeking income plays face tighter cap rates

UHNW residential purchases

Supports CCR luxury segment; limited volume impact on mass-market prices

60% ABSD on foreigners

Continues to substantially limit volume of Chinese individual purchases; policy unchanged

Developer ABSD (40%)

Requires developers to sell all units within 5 years to recover 35% remittable component; creates inventory-clearing incentive

What Singapore’s Position Means for Local Buyers

The surge in Chinese institutional investment is primarily a commercial and developer-side phenomenon. For the Singaporean household buying their first home or upgrading from HDB to private, the direct impact is limited. The mass-market Outside Central Region (OCR) residential segment — where most Singaporean buyers transact — is not significantly influenced by Chinese developer activity, which is concentrated in the CCR and selected RCR developments.

The more relevant indirect effect is on GLS land prices. Increased international developer competition for GLS sites elevates winning bid prices, which flow through to higher launch prices and, with a lag, higher resale prices in surrounding areas. This is a slow-moving structural force rather than a near-term price driver. The Holland Plain Parcel B result (Sim Lian sole bid at S$1,491 psf ppr) in May 2026 — noticeably below the S$1,600–S$1,750 psf ppr range that six-to-eight-bidder competition would have implied — illustrates that developer caution persists even as Chinese interest in the broader investment landscape grows.

For property investors evaluating Singapore condos against a 60% ABSD exposure for Chinese buyers, the read-through is nuanced. Strong Chinese interest in Singapore as an investment destination is a medium-term positive for capital values. But the 60% ABSD is a sufficiently high barrier that it effectively segments the market: Chinese buyers are a price-setter in the ultra-luxury CCR segment but not a material volume driver in broader residential transaction statistics.

What Might Come Next