Singapore Joint Property Ownership Guide 2026: Tenancy-in-Common vs Joint Tenancy Explained

- Two legal structures: Joint Tenancy (equal shares, right of survivorship) and Tenancy-in-Common (any split, no survivorship — shares pass via will).

- ABSD is profile-based: each co-buyer pays ABSD according to their own buyer profile and property count — there is no ABSD discount for buying jointly.

- CPF is individual: each co-owner draws from their own CPF Ordinary Account (OA) in proportion to their ownership share.

- TDSR applies jointly: both co-buyers’ incomes are combined, and so are all their existing financial obligations — the 55% TDSR ceiling covers the full loan repayment.

- Decoupling is possible for properties held as Tenancy-in-Common — one co-owner buys out the other’s share, paying ABSD only on the acquired portion. Not possible for Joint Tenancy without first converting.

- Right of survivorship in Joint Tenancy automatically transfers the deceased’s share to the surviving owner — bypassing probate. TIC shares fall under the estate and require a will or intestacy rules.

- Singapore Citizens buying together as first-time buyers pay 0% ABSD. If either buyer already owns a residential property, they pay 20% ABSD on the full price.

What is Joint Property Ownership in Singapore?

When two or more people purchase a residential property together in Singapore, they become co-owners. Singapore law recognises two forms of co-ownership: Joint Tenancy and Tenancy-in-Common. The choice between them affects inheritance, the ability to sell independently, stamp duty strategy, and — crucially — your exposure to the Additional Buyer’s Stamp Duty (ABSD) on future purchases.

Joint ownership is extremely common in Singapore. Most married couples purchasing an HDB flat or private condominium do so as joint owners, combining incomes to pass the Total Debt Servicing Ratio (TDSR) and Mortgage Servicing Ratio (MSR) thresholds set by the Monetary Authority of Singapore (MAS). Unmarried siblings, parents and children, and business partners also frequently co-purchase investment properties.

Understanding the legal and financial mechanics before you sign the Option to Purchase (OTP) is essential. The ownership structure you choose on day one determines what options you have years later — including whether you can decouple to buy a second property without ABSD.

Joint Tenancy vs Tenancy-in-Common: The Core Differences

The two ownership structures share the feature that all co-owners are equally responsible for the mortgage — both are jointly and severally liable to the lender. Beyond that, they diverge significantly.

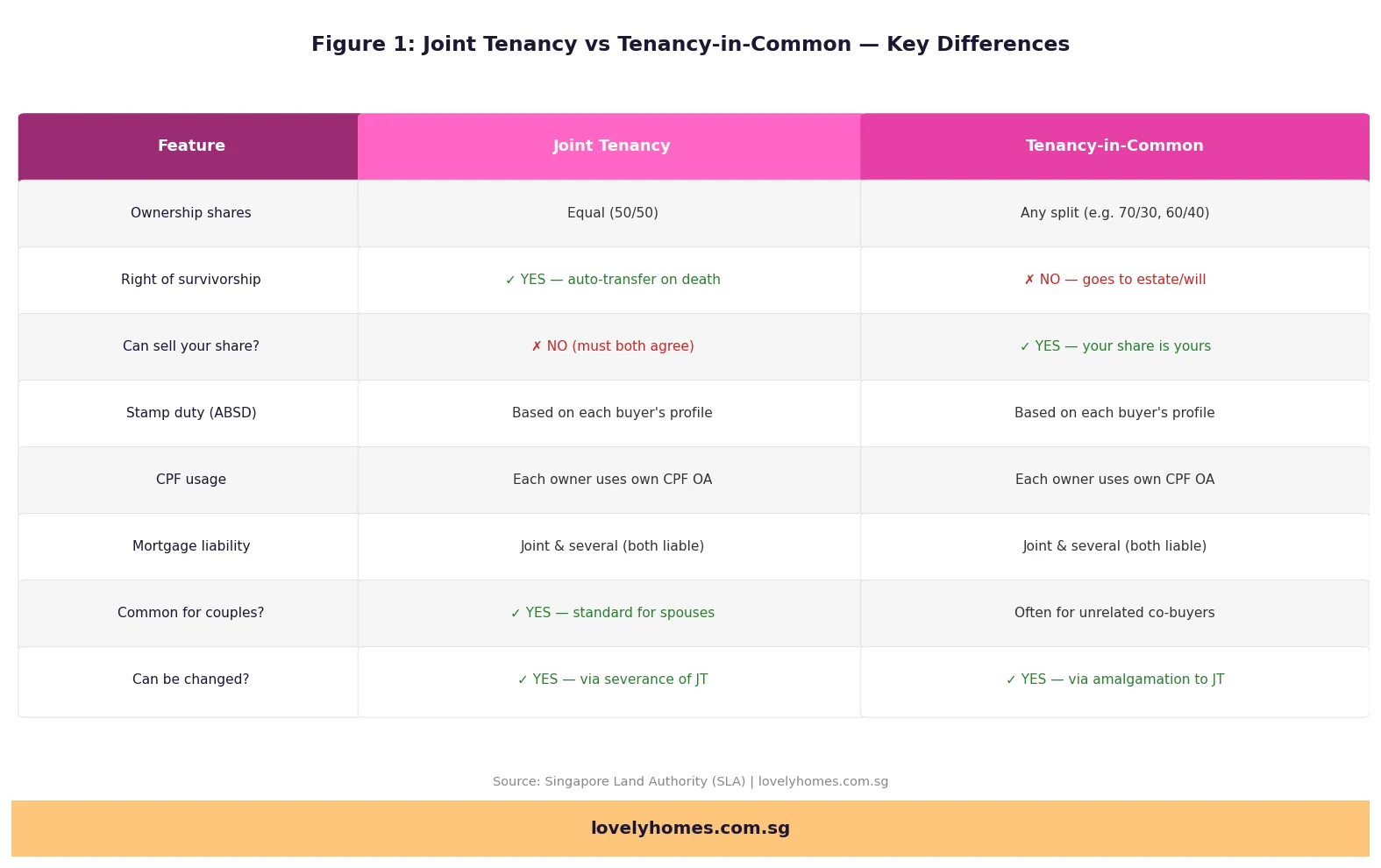

Joint Tenancy treats the property as a single, indivisible whole. Each owner holds an equal share by law — a married couple in joint tenancy each hold 50%, regardless of how much each contributed to the purchase. If one owner dies, their interest automatically passes to the surviving owner(s) by the right of survivorship, outside of the deceased’s estate. This is why joint tenancy is the default choice for married couples: it avoids probate complications and ensures the family home passes seamlessly.

Tenancy-in-Common, by contrast, allows co-owners to hold defined, unequal shares — for example, 70/30 or 80/20 — reflecting their respective CPF and cash contributions. Each co-owner’s share is a distinct legal interest that they can will to a beneficiary, sell independently (with the other owner’s knowledge but not necessarily consent, depending on the sale structure), or use as a platform for decoupling. There is no right of survivorship: if a Tenancy-in-Common co-owner dies intestate, their share passes under Singapore’s Intestate Succession Act, not automatically to the co-owner.

Figure 1: Key differences between Joint Tenancy and Tenancy-in-Common in Singapore. Source: Singapore Land Authority (SLA) | lovelyhomes.com.sg

How ABSD Applies to Joint Property Purchases

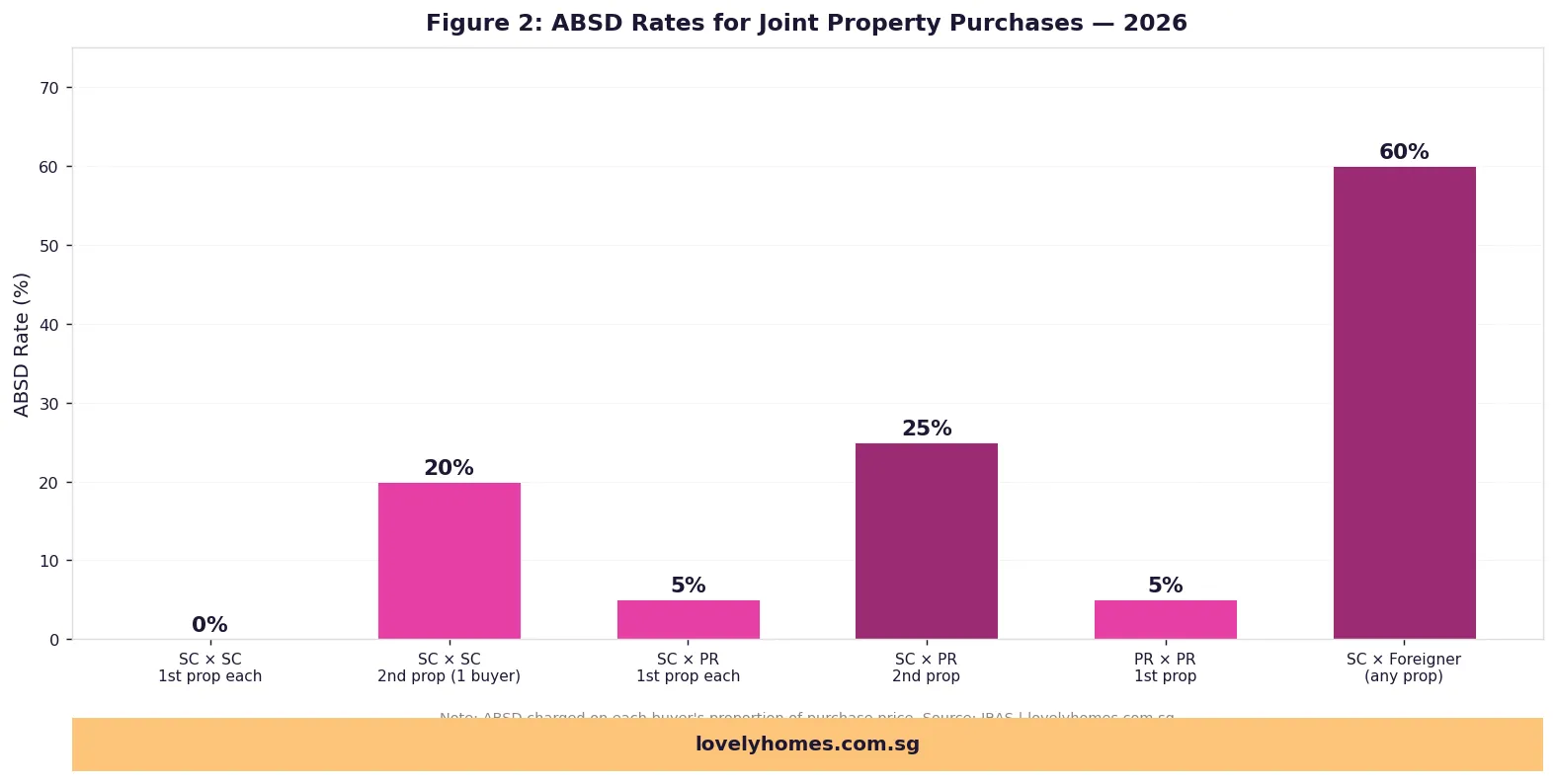

The Additional Buyer’s Stamp Duty (ABSD), administered by the Inland Revenue Authority of Singapore (IRAS), applies whenever a buyer acquires an additional residential property. For joint purchases, the rule is straightforward but often misunderstood: ABSD is computed based on the profile of the buyer who attracts the higher rate.

This means that if a Singapore Citizen (SC) and a Permanent Resident (PR) buy together, and the PR is deemed to be acquiring a second property (5% ABSD applies to PRs on their first property, 25% on their second), the ABSD rate applicable to that joint purchase reflects the higher-rate buyer’s position. The full ABSD is computed on the full purchase price.

More practically: an SC married couple buying their first property together pay 0% ABSD. But if either spouse already owns a property — even one inherited or received as a gift — the couple faces a 20% ABSD on the full price of the new purchase. At S$1.5 million, that is S$300,000 payable in cash (ABSD cannot be funded from CPF OA). This is the biggest single financial surprise for HDB upgraders who have not sold their flat before exercising an OTP on a new property.

Figure 2: ABSD rates for joint purchases by buyer-profile combination. ABSD is computed on the full purchase price. Source: IRAS | lovelyhomes.com.sg

CPF Usage in Joint Property Purchases

The Central Provident Fund (CPF) Board allows each co-owner to use their own CPF Ordinary Account (OA) savings towards a jointly-owned property, subject to the Valuation Limit and Withdrawal Limit rules. Each co-owner’s CPF usage is capped in proportion to their ownership share.

For HDB properties, this is straightforward: each co-owner uses their OA for the down payment and monthly mortgage servicing, with the Mortgage Servicing Ratio (MSR) capping total repayments at 30% of gross monthly income. For private properties (condominiums, landed homes, ECs post-privatisation), the TDSR cap of 55% of gross monthly income applies. Critically, CPF usage for private property is also subject to the Valuation Limit — once total CPF withdrawn equals the property’s original purchase price or valuation (whichever is lower), further CPF can only be used if the property has at least 60 years’ remaining lease at the time of purchase, and CPF usage may be further pro-rated for properties with shorter leases.

In a Tenancy-in-Common structure, CPF accrued interest — the interest CPF Board charges on OA monies withdrawn for property — must be refunded to each co-owner’s CPF account upon sale, proportionally. This accrued interest accumulates at the CPF OA interest rate (currently 2.5% per annum on the first S$20,000, 3.5% thereafter — effective 1 January 2024) and can significantly reduce the net cash proceeds from a property sale after many years of ownership.

Decoupling: Converting Ownership to Access a Second Property

Decoupling is a legal strategy whereby one co-owner transfers or sells their share in a jointly-owned property to the other, so that the departing co-owner is no longer a property owner and can subsequently purchase a second property as a “first-time buyer” — paying 0% ABSD (for SCs) instead of 20%.

Decoupling requires the property to be held as Tenancy-in-Common. A Joint Tenancy must first be severed (converted to TIC) via a Deed of Severance lodged with the Singapore Land Registry before decoupling can proceed. The process involves: (1) severing the joint tenancy if applicable; (2) the selling co-owner executing a Transfer Instrument conveying their share to the buying co-owner; (3) the buying co-owner paying ABSD on the acquired share’s value (not the full property value, if they already own the remaining share); and (4) legal fees typically S$3,000–S$5,000 per party.

IRAS scrutinises decoupling transactions under anti-avoidance provisions. Where the transfer is purely nominal and consideration is not reflective of market value, IRAS may challenge the arrangement. Always engage a licensed conveyancing solicitor and ensure the transfer price is at or close to open-market value for the share being transferred.

Note: As at 2026, HDB flats cannot be decoupled in the same manner as private residential properties, due to HDB rules prohibiting partial transfers of HDB flat ownership except in specific circumstances (e.g. matrimonial transfers upon divorce, or change in family nucleus for eligibility purposes). The decoupling strategy is therefore most relevant to private residential property owners.

Upfront Cost Comparison: Sole vs Joint Purchase

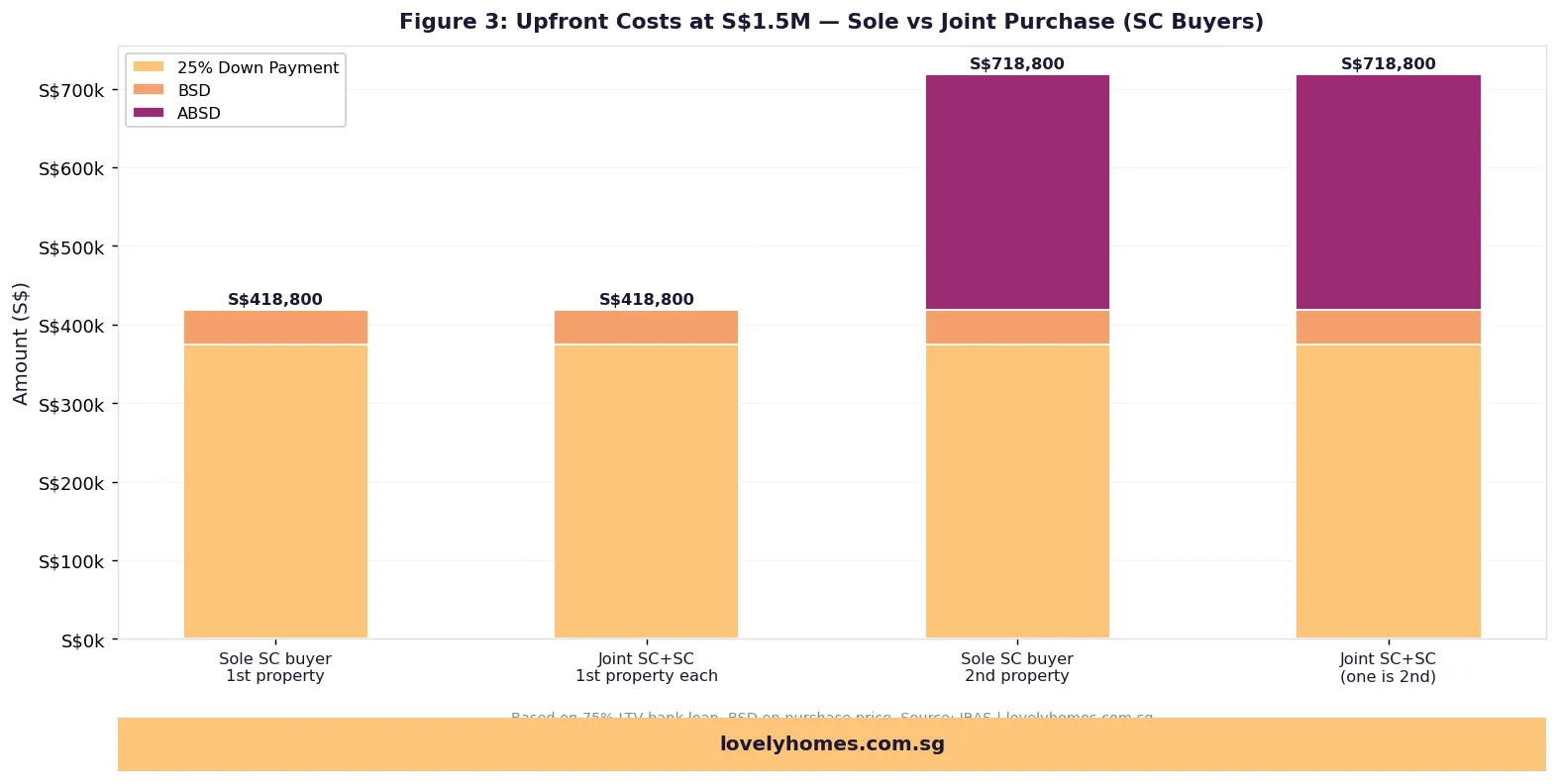

Figure 3: Upfront costs for sole vs joint purchase at S$1.5M — SC buyer profiles (25% down payment assumed, bank financing). Source: IRAS | lovelyhomes.com.sg

The upfront cost difference between a joint first-time purchase and a joint purchase where one party already owns a property is substantial. The chart above illustrates the ABSD component: for a couple buying their first property together at S$1.5 million, there is no ABSD. If either party already owns a home, the couple pays S$300,000 in ABSD — entirely in cash — in addition to the 25% down payment of S$375,000 and BSD of approximately S$43,800. Total upfront outlay jumps from roughly S$418,800 to S$718,800.

Summary Table: Joint Ownership at a Glance

| Factor | Joint Tenancy | Tenancy-in-Common |

|---|---|---|

| Shares | Equal (50/50 by law) | Any ratio (e.g. 70/30) |

| Survivorship | Auto-transfer to survivor | Passes to estate / will |

| Independent sale of share | Not possible | Possible (co-owner’s interest) |

| Decoupling eligibility | Must sever JT first | Yes — directly possible |

| CPF usage | Each owner’s OA (50/50) | Each owner’s OA (in share ratio) |

| ABSD profile | Higher of two profiles applies | Higher of two profiles applies |

| TDSR calculation | Combined income, combined obligations | Combined income, combined obligations |

| Best suited for | Married couples, family home | Investors, unequal contributors, decoupling strategy |

Worked Example: Lim Couple — Joint Purchase with ABSD Implication

Scenario: Mr Lim (SC, 38) and Mrs Lim (SC, 36) are HDB flat owners (4-room in Tampines, purchased 2019 — MOP completed August 2024). They wish to buy a 2-bedroom resale condominium in District 19 for S$1,350,000 as a joint investment property without first selling their HDB flat.

Buyer profiles: Both Mr and Mrs Lim own the HDB flat jointly. A second property purchase makes both of them “second-time buyers”.

ABSD payable: SC buying 2nd residential property = 20% ABSD.

- ABSD = 20% × S$1,350,000 = S$270,000 (payable in cash within 14 days of OTP exercise)

- BSD = 1% × S$180,000 + 2% × S$180,000 + 3% × S$640,000 + 4% × S$350,000 = S$1,800 + S$3,600 + S$19,200 + S$14,000 = S$38,600 (can use CPF OA)

- 25% down payment = S$337,500 (at least 5% in cash, remainder CPF OA)

- Total upfront ≈ S$646,100 (cash component alone ≈ S$337,500 + S$270,000 = S$607,500)

TDSR check: Bank loan 75% × S$1,350,000 = S$1,012,500 at 4.0% over 25 years → monthly repayment ~S$5,330. Combined gross income S$14,000/month. TDSR = S$5,330 / S$14,000 = 38.1% — well within the 55% cap. ✓

Alternative (sell first): If the Lims sell their HDB flat before exercising the OTP on the condo, their subsequent purchase is as first-time buyers (assuming they have no other property). ABSD = 0%. Total upfront drops by S$270,000. The trade-off: interim accommodation costs and the risk of timing the property market.

Why This Matters: Common Joint-Ownership Mistakes

Joint property ownership mistakes in Singapore typically fall into three categories. The first is choosing the wrong structure: couples who intend to decouple later but buy in Joint Tenancy find they must pay additional legal fees for the severance step — a cost and delay that Tenancy-in-Common would have avoided from the outset.

The second is overlooking the ABSD trigger: many buyers assume that buying jointly means only one of them “owns” the property, or that ownership below 50% is somehow exempt from ABSD. IRAS does not distinguish — any ownership interest in a residential property, however small, counts for ABSD-profile purposes.

The third is CPF accrued interest surprise at exit: couples who have used substantial CPF OA funds over a long holding period are often shocked to discover that the CPF Board requires full refund of withdrawn amounts plus accrued interest upon sale. On a property held for 15 years with S$300,000 CPF withdrawn, accrued interest at 2.5–3.5% per annum compounds to over S$130,000 — meaningfully reducing net cash proceeds.

What Might Come Next: Policy Outlook

The Singapore government has made clear in successive Budget and National Day Rally statements that property cooling measures — including ABSD — remain calibrated to prevent speculative demand and preserve housing affordability. There is no current signal that ABSD rates for joint purchases will be relaxed. If anything, the 2023 rate hikes (to 60% for foreigners and 20% for SC second-time buyers) indicate that the authorities remain willing to tighten when prices surge.

On decoupling, IRAS has not yet announced specific anti-avoidance regulations targeting Tenancy-in-Common transfers between spouses, but practitioners note increased scrutiny on transactions where the transferring price deviates materially from open-market value. Buyers considering decoupling in 2026 should document their transactions carefully and obtain an independent valuation.

The Urban Redevelopment Authority’s (URA) long-run supply pipeline — including the Government Land Sales (GLS) programme’s 4,745-unit Confirmed List for the second half of 2026 — is intended to moderate price growth over the medium term, which may reduce the urgency of complex joint-ownership strategies for buyers who can wait.

Frequently Asked Questions

1. Can a Singapore Citizen and a foreigner buy a property together in Singapore?

Yes, but the ABSD implication is significant. Where one co-buyer is a foreigner (non-SPR), the applicable ABSD rate for the joint purchase is the foreigner rate of 60%, applied to the full purchase price. This applies regardless of which co-owner holds what share. Foreigners purchasing residential property in Singapore are restricted to non-landed residential property (condominiums, apartments) in most cases — landed residential property requires prior approval from the Minister for Law under the Residential Property Act.

2. How does Joint Tenancy affect my estate planning?

In a Joint Tenancy, the right of survivorship overrides any will you have written with regard to that property. If you hold your home in Joint Tenancy and your will directs that the property should go to your children, your will is ineffective on that point — the property passes automatically to the surviving joint tenant(s). If you want to direct your property interest via your will, you must convert your ownership to Tenancy-in-Common first by executing a Deed of Severance. The conversion does not affect the mortgage and can be done at any time without triggering ABSD or BSD.

3. Does adding a co-owner to an existing property trigger ABSD?

Yes. Adding a co-owner to a property that you already own involves a transfer of a partial interest in that property. The new co-owner is treated as acquiring a property interest, and ABSD applies based on their buyer profile and property count — on the market value of the share being transferred. An exception applies for transfers between spouses under certain conditions (e.g., for love and affection or matrimonial transfer), but these require careful legal structuring. Always consult a solicitor before adding a co-owner.

4. Can I use my CPF OA to pay the other co-owner’s share of the purchase price?

No. CPF OA funds can only be used to service your own share of the property — you cannot top up a co-owner’s shortfall using your CPF. Each co-owner’s CPF contribution is limited to their proportional ownership share. For example, in a 70/30 Tenancy-in-Common property priced at S$1,000,000, the 70% owner can withdraw from their CPF OA up to 70% of the Valuation Limit, and the 30% owner up to 30%.

5. What is the ABSD remission for married couples buying their first property together?

There is no ABSD to remit in the first place — Singapore Citizens buying their first residential property pay 0% ABSD regardless of whether they buy jointly or alone. The relevant remission for couples applies when an SC married couple buys a second property together: they can apply for an ABSD remission (refund) if they sell their existing property within 6 months of completing the purchase of the new private property. The remission is not automatic — it must be applied for via IRAS within 6 months of the sale completion of the first property.

6. What happens to a jointly-owned property during a divorce?

Upon divorce, jointly-owned property is subject to the division of matrimonial assets under the Women’s Charter. The court may order the property to be sold and proceeds split, or direct one spouse to transfer their share to the other — with the receiving spouse paying any applicable stamp duty on the transfer. Transfers ordered by the court in matrimonial proceedings may be eligible for ABSD and BSD remission; consult a family law solicitor for the applicable rules, which have specific conditions.

7. Can I decouple if my property has an outstanding HDB concessionary loan?

Decoupling is only relevant for private residential properties — not HDB flats. HDB flats cannot be decoupled in the same way because HDB rules prohibit partial transfers of flat ownership except in prescribed circumstances (divorce, death, change of flat ownership for eligibility purposes, etc.). If you want to apply decoupling strategy, you must first complete your HDB flat’s Minimum Occupation Period, sell the flat, and then purchase two separate private properties — one in each spouse’s name — to avoid the ABSD on a second property.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty Singapore 2026: BSD Rates & Calculator Guide

- HDB Minimum Occupation Period (MOP) Guide 2026

- HDB Resale Guide 2026: Step-by-Step Complete Guide

- Singapore Condo Resale Guide 2026: Step-by-Step Buyer’s Complete Guide

- Singapore Mortgage Refinancing Guide 2026

- Singapore Property Succession & Inheritance Guide 2026

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or tax advice. Property ownership structures, ABSD rates, CPF rules, and HDB regulations are subject to change. Readers should verify information with the relevant authorities — the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg, the Central Provident Fund Board (CPF) at cpf.gov.sg, the Singapore Land Authority (SLA) at sla.gov.sg, and the Housing & Development Board (HDB) at hdb.gov.sg — and consult a licensed conveyancing solicitor and/or a registered property agent before making any property transaction decisions.