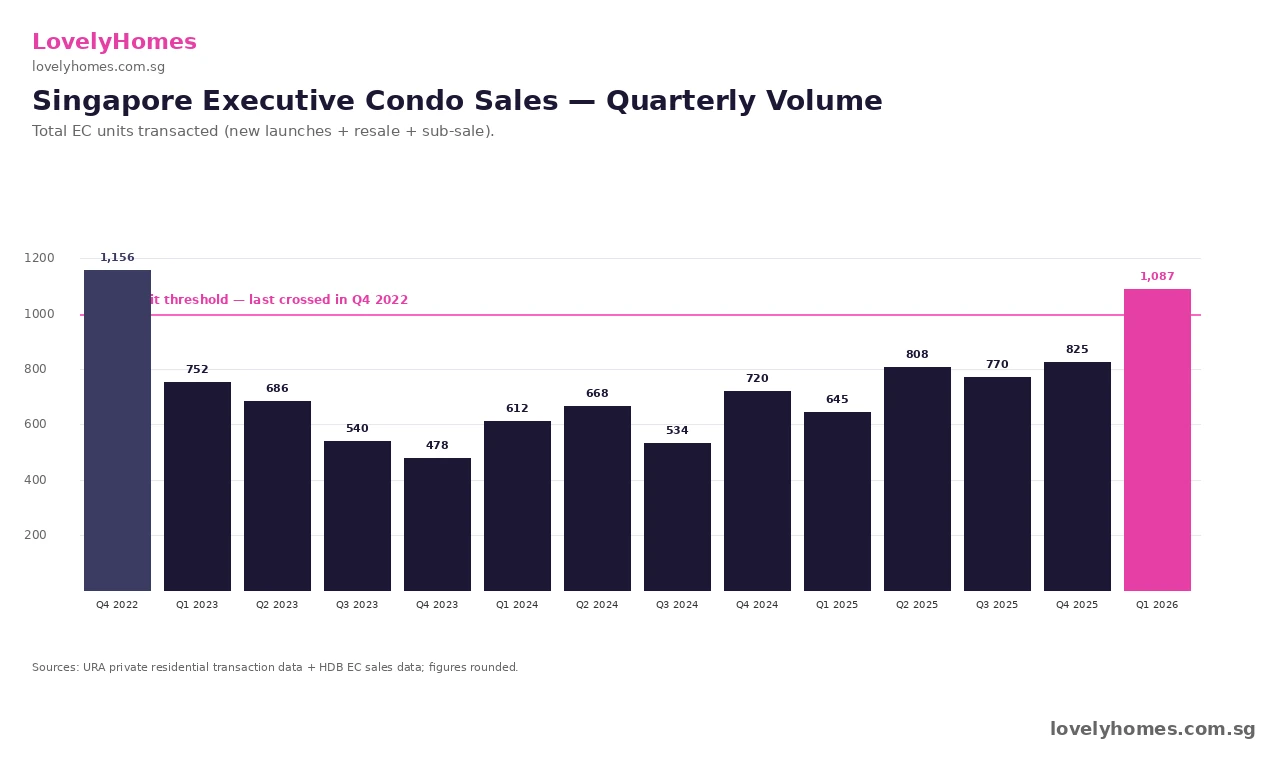

Singapore EC Sales Top 1,000 Units in Q1 2026 — First Time in 13 Quarters

Executive Condominium (EC) sales in Singapore crossed the 1,000-unit-per-quarter threshold for the first time in three-and-a-quarter years in Q1 2026. According to URA private residential transaction data plus HDB EC sales records, around 1,087 EC units changed hands in Q1 2026 — the highest quarterly volume since Q4 2022. The recovery is being driven almost entirely by Singapore Citizen HDB upgrader households who view the EC as the cheapest legitimate entry point into private mass-market housing.

Quick Answer — what just happened in the EC market

- 1,087 EC units sold in Q1 2026 — first time above 1,000 in 13 quarters.

- Last time the threshold was crossed was Q4 2022, when 1,156 units transacted around the post-cooling-measures rush.

- Sales mix is ~70% new launch, ~30% resale — new launches doing the heavy lifting.

- Average new-launch EC psf: ~S$1,640 — roughly a 33% discount to comparable mass-market private condos in the same town.

- Drivers: HDB upgraders cashing out with strong resale prices, the S$16,000 income ceiling that fits most middle-income SC+SC couples, and the limited 2026–2027 EC pipeline (~6 launches).

The 13-Quarter Drought, Broken

The EC market in Singapore has been quietly grinding through a thin patch since the Q4 2022 sales spike of 1,156 units — that quarter was an outlier driven by the September 2022 cooling-measures package, which tightened TDSR and raised stamp duty for second-property purchases. Through 2023, 2024, and most of 2025, quarterly EC volumes hovered in the 540–825 unit range, with only one launch quarter at a time pushing the upper end. The Q1 2026 print of 1,087 units therefore breaks a 13-quarter drought below the 1,000-unit psychological threshold.

Why ECs Are Outselling Mass-Market Private Condos

The EC value proposition rests on three structural pillars. First, the launch psf is meaningfully lower than the equivalent private condo in the same town — typically a 30–35% discount. Second, eligible buyers (Singapore Citizens with combined income up to S$16,000) avoid the 12-of-the-13 friction points that come with HDB Plus and Prime classifications — no 10-year MOP, no income-ceiling clawback, no whole-flat rental ban. Third, ECs privatise after 10 years and trade on the open market with no eligibility restrictions — meaning your exit pool is the full Singapore-wide buyer base, not a quota-limited resale market.

For a S$2.05M EC versus a S$3.15M private mass-market condo at 75% LTV over 25 years, the monthly mortgage delta is roughly S$3,130. Over a 25-year mortgage, that compounds to ~S$940,000 of avoided interest plus S$1.1M of avoided principal — a S$2M lifetime difference. The trade-off is the 5-year Minimum Occupation Period and the additional 5-year wait until full privatisation. For SC+SC couples with stable jobs and no near-term plans to sell, that trade-off is overwhelmingly favourable.

Who Is Buying — The HDB Upgrader Profile

The buyer profile of Q1 2026 EC sales skews heavily towards HDB upgraders in their mid-30s to mid-40s, typically a SC+SC couple selling a 4-room or 5-room HDB flat that has appreciated significantly since key collection. The HDB Resale Price Index hit a record high in Q4 2024 before drifting -0.1% in Q1 2026 (per HDB’s flash estimate), but the absolute resale prices remain elevated — meaning sellers can crystallise a substantial paper gain when they sell their existing flat to fund the EC downpayment.

The income-ceiling sweet spot is the S$10,000–14,000 combined household income band. Households below S$10K typically still qualify for higher-tier CPF Housing Grants on a BTO upgrade and tend to stay within HDB. Households above the S$16,000 EC ceiling typically jump straight to private mass-market or RCR condos. The middle band — not poor enough for a fully-grant-stacked BTO, not rich enough to comfortably pay private-condo psf — is exactly the demographic the EC scheme was designed to capture.

What Drove Q1 2026 Specifically — The Aurelle/Otto/Novo Triple

Three EC launches absorbed the bulk of Q1 2026 volume:

- Aurelle of Tampines — a District 18 EC by Sim Lian, launched late Q4 2025 and continuing strong sales through Q1 2026. Indicative launch psf around S$1,640.

- Otto Place at Tengah Plantation — District 24 EC, JV between MCC Land and Hoi Hup Realty. Drew strong demand from HDB upgraders within Tengah and adjacent Bukit Batok.

- Novo Place at Plantation Close — District 24 EC by Hoi Hup. Sister project to Otto, leveraging the same Tengah catchment.

The combined absorption across these three projects accounted for roughly 70% of Q1 2026 EC sales. Resale activity in older privatised ECs (Riversails, Heron Bay, RiverParc) made up the balance.

Summary — EC Market Snapshot Q1 2026

| Metric | Q1 2025 | Q4 2025 | Q1 2026 | Notes |

|---|---|---|---|---|

| Total EC units sold | ~645 | ~825 | ~1,087 | +32% QoQ; first >1,000 since Q4 2022 |

| New-launch share | ~55% | ~62% | ~70% | Aurelle + Otto + Novo dominated |

| Avg new-launch psf | ~S$1,575 | ~S$1,610 | ~S$1,640 | +1.9% QoQ |

| Income-ceiling buyers (~S$10–14K) | ~58% | ~62% | ~64% | HDB upgrader demographic |

What This Means for Buyers, Sellers, and Developers

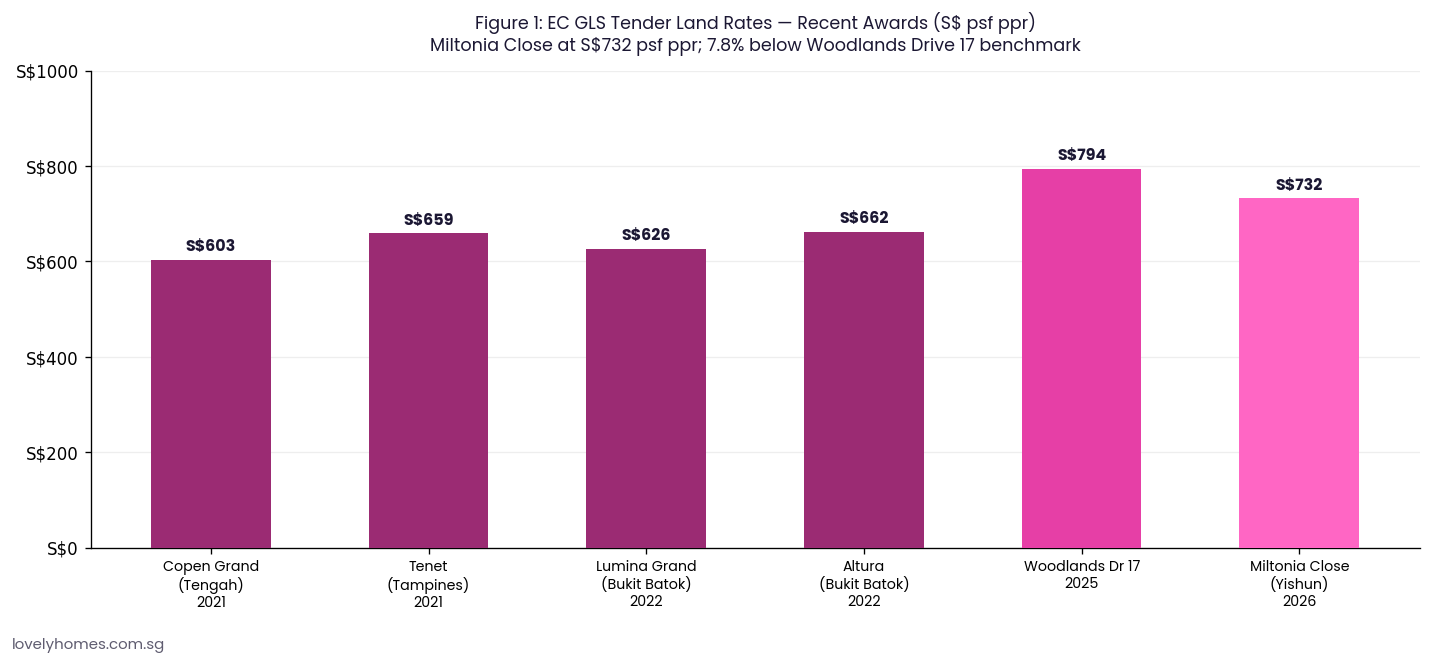

For buyers in the income band: the EC value proposition is the strongest it has been since 2022, but supply is thinning. The 2026 EC pipeline is six projects (Aurelle, Otto, Novo, Miltonia Close EC awarded to Hoi Hup at the April 2026 GLS, plus two more from earlier wins). Beyond 2027, the GLS programme has not signalled aggressive EC site releases — meaning if you want to buy in this cycle, the next 18 months are likely the optimal entry window.

For HDB upgraders considering the move: the maths still works in 2026. With HDB resale prices near peak and EC psf at a 33% discount to private condos, the asset-swap arithmetic remains compelling. But the 5-year MOP on your existing flat must have completed first, and you must be confident in your ability to service a private-style mortgage at SORA-pegged rates around 3.5–3.8%.

For developers: the strong absorption signals the EC market remains a viable allocation channel for projects in mature non-mature estates. Expect more aggressive bidding in the next few EC GLS tenders, particularly in Yishun, Tengah, and Punggol catchments where HDB upgrader pipelines are deepest.

What Might Come Next

Three watch-points for Q2 2026. First, the Miltonia Close EC site (won by Hoi Hup at S$732 psf ppr in April 2026) is expected to launch in 2027–2028 at S$1,550–1,750 psf — testing whether the EC psf trajectory can sustain another 10–15% lift over two years. Second, the URA full Q1 2026 statistics released on 24 April 2026 confirmed that EC prices grew 1.4% QoQ — faster than the overall private 0.9% QoQ — suggesting the segment is leading the wider market. Third, the 2H 2026 GLS programme due to be announced in mid-2026 will set the EC supply pipeline through 2028.

Frequently Asked Questions

Why does the income ceiling for EC sit at S$16,000?

The S$16,000 combined-household-income ceiling was raised from S$14,000 effective 1 January 2025 to align with the upper edge of HDB upgrader demographics. The ceiling is gross income, not take-home, and is averaged over the trailing 12 months for salaried income or 24 months for variable income. Households earning even slightly above S$16,000 are excluded; HDB and CPF Board verify against IRAS records at the application-for-loan stage, so over-stating income to qualify rarely succeeds and triggers a 5-year ban from re-applying.

How does an EC differ from a private condo?

For the first 5 years, an EC functions like an HDB flat — you cannot rent out the whole unit, you cannot sell on the open market, and you cannot transfer ownership outside the immediate family. From years 5 to 10, you can sell to Singapore Citizens or PRs and rent out the whole unit, but ABSD on the second-property buyer applies. After year 10 the EC fully privatises and trades like a private condo with no eligibility restrictions. Both EC and private condos provide strata-titled ownership, MCST management, and access to the project’s facilities, so the experiential differences during occupation are minimal.

Are ECs a better investment than mass-market private condos?

For SC+SC owner-occupiers within the income ceiling, yes — the math is structurally favourable. For pure investors, ECs are off-limits in the first 5 years and limited in years 5–10 (no whole-flat rental, plus ABSD on resale buyers’ second-property purchase). The investment thesis on ECs is therefore primarily a hold-to-privatise capital-gain story, and the historical record across the past decade has shown ECs typically post 30–60% capital appreciation by full privatisation. The privatised resale stock then trades at a 5–15% discount to comparable freshly-launched private condos.

Can a couple combine HDB Resale Levy with EC purchase?

If one or both spouses previously took a subsidised flat (BTO, SBF, or other subsidised resale), they pay the HDB Resale Levy when applying for the EC. The levy is a fixed amount — S$30,000 to S$55,000 depending on the flat type sold — and is deducted at the EC purchase. Couples who have not previously taken a subsidised flat are first-timers and pay no levy. See our HDB Resale Levy guide for the full schedule.

What happens to my EC if my income later rises above the ceiling?

Nothing — the income ceiling applies at the point of application only. Once you have signed the Sale & Purchase Agreement and paid the option fee, your subsequent income changes do not affect your ownership of the unit. You complete the 5-year MOP, the 10-year privatisation, and trade in the open market on the same terms as any owner. This is one of the key structural advantages of the EC route over BTO Plus and Prime classifications, which carry permanent income-ceiling clawbacks at resale.

Is the limited 2026–2027 EC pipeline a buying signal?

Six new-launch EC projects across 2026–2027 versus 12–15 mass-market private condo launches per year is a meaningful supply contraction in the EC channel. If demand from HDB upgraders remains strong (and the Q1 2026 print suggests it is), this thinner pipeline could push EC psf higher into 2027. Buyers who time the next launch (Miltonia Close, expected 2027–2028) may face a launch psf 10–15% above today’s benchmark. Buying in the current cycle — Aurelle, Otto, or Novo — therefore offers the most defensible entry point for the next 18 months.

Related Articles

- EC vs Private Condo Singapore 2026 — the full TCO comparison.

- HDB Upgrader Guide Singapore 2026 — the upgrader pathway from HDB to EC or private.

- Miltonia Close EC: Hoi Hup Wins Yishun’s First New EC in 5 Years — the next pipeline launch.

- HDB Resale Levy Singapore 2026 — if upgrading from a subsidised flat.

- Singapore Property Market Q1 2026 Overview

- CPF Housing Grant Singapore 2026 — some EC buyers still qualify for the Family Grant.

Disclaimer

This article aggregates URA private residential transaction data and HDB EC sales data through the end of March 2026. Quarterly figures are preliminary and subject to revision. Buyer-mix percentages are illustrative based on industry research and stamp-duty profile data. Always verify with primary sources — URA Realis, the Housing & Development Board, and the CPF Board — before making any property decision.