Singapore EC Buying Guide 2026: Complete Guide to Executive Condominiums

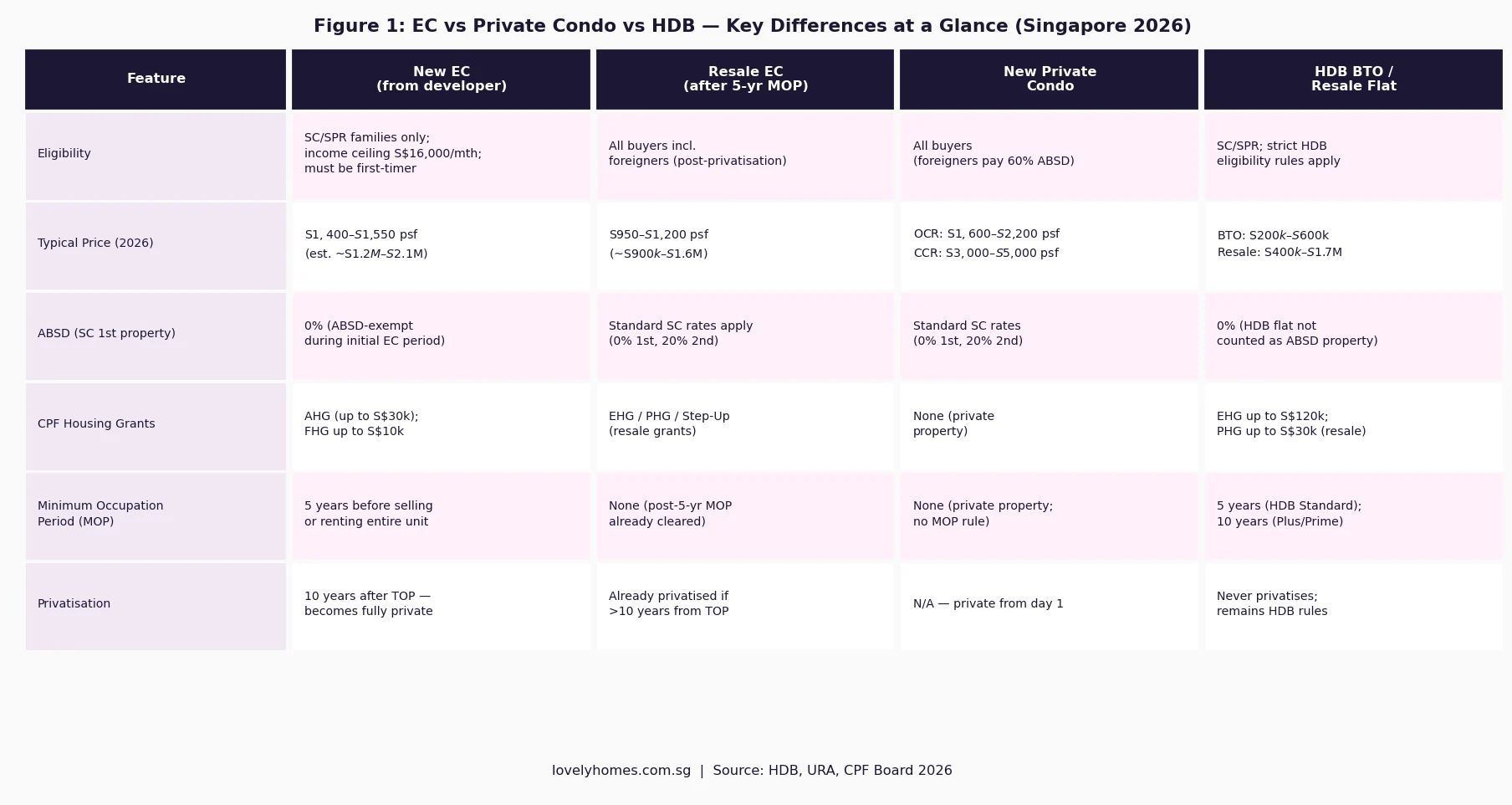

For Singapore’s “sandwich class” — households who earn too much to qualify for subsidised HDB flats but find new private condominiums financially out of reach — the Executive Condominium (EC) remains the most important rung on the property ladder. Priced typically S$400–S$700 per square foot lower than comparable private condominiums at launch, ECs are purpose-built by private developers on government land, sold to eligible buyers with CPF grants, and eventually privatised ten years after their Temporary Occupation Permit (TOP) date. At that point, they trade freely on the open market like any private condominium.

This guide covers everything you need to know about buying an EC in Singapore in 2026 — who is eligible, how much you can borrow, which CPF grants apply, the full cost breakdown, and how the new cooling measures announced on 8 May 2026 change the landscape. Where relevant, we cross-reference the EC rule changes in our separate article Singapore EC Rule Changes May 2026: 10-Year MOP, No DPS and 90% First-Timer Quota Explained.

- ECs are built by private developers but sold under HDB rules — eligibility, income ceiling (S$16,000/month for families), and a 5-year MOP apply.

- New ECs in 2026 are launching at an estimated S$1,400–S$1,550 psf — roughly S$400–S$600 psf lower than comparable OCR private condominiums.

- Eligible buyers can access the CPF Additional Housing Grant (AHG) of up to S$30,000 and the Family Housing Grant (FHG) of up to S$10,000.

- As of 8 May 2026, new EC rules include: 10-year MOP before an EC unit can be rented out in its entirety, 15-year privatisation period (up from 10), 90% first-timer priority ballot, and abolition of the Deferred Payment Scheme (DPS).

- ABSD is not payable on a first EC purchase from the developer; standard ABSD rates apply if buying a fully privatised EC on the open market.

- You cannot own any private property for 30 months before applying, and must not own another HDB flat at the time of EC application.

- The Minimum Occupation Period is 5 years for selling; the unit cannot be rented out in its entirety during this 5-year period (and now 10 years for full-unit rental under the new rules).

- At privatisation (15 years from TOP under the new rules), the EC may be purchased by foreigners at standard ABSD rates.

What Is an Executive Condominium?

An Executive Condominium is a hybrid residential property type unique to Singapore, introduced by the Housing and Development Board (HDB) in 1995. It is developed by private developers on land sold by HDB under the Government Land Sales (GLS) programme, and comes with private condominium facilities — swimming pool, gymnasium, clubhouse, security, and landscaped grounds — at a price point made accessible through an eligibility framework similar to HDB flats.

Unlike a standard HDB flat, an EC is sold under a hybrid legal framework: it is a private strata-title property governed by the Building Maintenance and Strata Management Act (BMSMA), but for the first ten to fifteen years (depending on the vintage), it is subject to HDB ownership rules including the Minimum Occupation Period (MOP) and eligibility requirements. After the privatisation date, these HDB rules fall away entirely and the property trades as a full private condominium.

HDB administers the EC scheme. The Singapore Land Authority (SLA) maintains the land register. The Urban Redevelopment Authority (URA) tracks EC transaction data under the same REALIS system that covers private condominiums. Applications for new EC launches are made through the HDB portal at hdb.gov.sg.

EC Eligibility in 2026 — Who Can Buy?

Eligibility for purchasing a new EC from the developer is strictly governed by HDB. The primary eligibility schemes are the Public Scheme (family nucleus), Fiance/Fiancee Scheme, Orphans Scheme, and Joint Singles Scheme. The overwhelming majority of EC buyers purchase under the Public Scheme: a Singapore Citizen applicant forms a family nucleus with a spouse, children, or parents.

| Eligibility Criterion | Requirement |

|---|---|

| Citizenship | At least one applicant must be a Singapore Citizen. The other occupier may be a Singapore Citizen or Permanent Resident. |

| Age | At least 21 years old (18 years old for orphans scheme) |

| Income ceiling | Monthly household gross income ≤ S$16,000 (families); ≤ S$8,000 (singles — Joint Singles Scheme only, age 35+) |

| First-timer status | Must not have previously owned a private residential property in the 30 months before the EC application. Both applicant and occupier must not currently own an HDB flat (unless selling within 6 months of EC key collection). |

| Previous subsidies | If previously purchased an HDB flat with CPF grants or sold an HDB flat with HDB loan, there are waiting periods or resale levy implications. Check HDB’s eligibility calculator. |

| 30-month private property rule | Neither the applicant nor any listed occupier may have disposed of a private residential property within 30 months before the EC application date. |

| Ownership of HDB flat | Must not own an HDB flat unless you commit to sell within 6 months of EC TOP (for existing HDB owners upgrading). |

Under the new rules effective 8 May 2026, 90% of units in each EC launch are balloted exclusively to first-timer families in the initial launch phase. This is a significant increase from the previous 70% first-timer priority, and is designed to ensure that ECs continue to serve their target demographic — upgraders who have not previously benefited from a subsidised property. Second-timer families (who have previously owned an HDB flat) are permitted to ballot only for the remaining 10% allocation during the first month of launch, and gain unrestricted access from the second month.

EC Pricing, CPF Grants, and Affordability in 2026

The pricing advantage of an EC over a comparable OCR private condominium has been the scheme’s defining attraction since its introduction. In the 2026 launch pipeline, new ECs are expected to price at S$1,400–S$1,550 per square foot, against OCR private condominiums averaging S$1,900–S$2,200 psf. For a 1,000 sq ft three-bedroom unit, that translates to a launch price of approximately S$1.4M–S$1.55M for the EC versus S$1.9M–S$2.2M for a comparable private condo — a saving of S$450,000–S$700,000 before grants.

On top of the pricing discount, eligible EC buyers may apply for CPF housing grants. The two principal grants for new EC purchases are the CPF Additional Housing Grant (AHG) and the Family Housing Grant (FHG), both administered by the CPF Board and HDB:

| Grant | Maximum Amount | Income Ceiling to Qualify | Notes |

|---|---|---|---|

| CPF Additional Housing Grant (AHG) | S$30,000 | ≤ S$10,000/month (family) | Tiered based on income; only first-timers eligible; credited to CPF OA |

| Family Housing Grant (FHG) | S$10,000 | ≤ S$16,000/month (family) | Available to all eligible EC first-timer families; credited to CPF OA |

| Step-Up CPF Housing Grant | S$15,000 | ≤ S$7,000/month (2nd-timer) | For 2nd-timer families who previously lived in a 2-room or smaller HDB flat; not stacked with AHG |

CPF grants for ECs are credited to your CPF Ordinary Account (OA) and may be used to offset the purchase price or reduce the mortgage. Unlike HDB resale grants, EC grants do not require you to hold the property for the MOP before they are “used up” — but CPF OA funds used are subject to the standard CPF accrued interest rules on eventual sale.

Financing an EC: Bank Loans, CPF, and the TDSR/MSR Framework

ECs may only be financed via bank loans — HDB concessionary loans are not available for EC purchases. The loan is subject to the standard Monetary Authority of Singapore (MAS) framework: Total Debt Servicing Ratio (TDSR) of 55% and, for EC purchases, the Mortgage Servicing Ratio (MSR) of 30% of gross monthly income. The MSR applies because ECs are treated as HDB-type properties for the purposes of borrowing limits during the initial eligibility period.

Under the prevailing LTV rules, a buyer with no outstanding property loans may borrow up to 75% of the purchase price (or market valuation, whichever is lower) from a financial institution. With the new 2026 rules abolishing the Deferred Payment Scheme (DPS), buyers are required to service the loan from the point of purchase or from when construction milestones are reached under the Normal Progressive Payment scheme.

| Financing Parameter | Applicable Rule |

|---|---|

| Loan type | Bank loan only (no HDB concessionary loan for ECs) |

| Maximum LTV | 75% of purchase price / valuation (whichever is lower), assuming no existing property loans |

| Minimum cash payment | 5% in cash; remaining 20% downpayment may come from CPF OA |

| TDSR (total debt) | All monthly debt obligations ≤ 55% of gross monthly income |

| MSR (mortgage only) | EC mortgage repayment ≤ 30% of gross monthly income |

| Maximum loan tenure | 30 years (capped such that loan maturity does not exceed age 65 of youngest borrower) |

| DPS (Deferred Payment Scheme) | Abolished effective 8 May 2026 — all purchases use Normal Progressive Payment |

EC Cooling Measures 2026: What Changed on 8 May 2026?

The Government announced a package of EC-specific cooling measures on 8 May 2026 — the most significant changes to the EC framework in over a decade. The changes are designed to reinforce the EC’s role as a subsidised housing product for genuine owner-occupiers and to curtail speculative demand. The four key changes are:

- 10-year full-unit rental restriction: EC owners may not rent out their entire unit for 10 years from the unit’s TOP date (up from the previous 5-year restriction). During this period, individual rooms may still be rented to authorised occupants. This effectively extends the owner-occupier commitment period significantly.

- 15-year privatisation period: An EC is now privatised 15 years from its TOP date (up from 10 years previously). Until privatisation, the HDB ownership rules continue to apply. From the privatisation date, the EC becomes a full private condominium and may be sold to foreigners and entities without restriction.

- 90% first-timer priority ballot: In the first month of each EC launch, 90% of units are reserved for first-timer families — up from 70%. This ensures that the primary beneficiaries of the EC subsidy are those who have not previously owned a subsidised property.

- Abolition of the Deferred Payment Scheme (DPS): Buyers can no longer defer mortgage repayments until TOP. All EC purchases from 8 May 2026 onwards use the Normal Progressive Payment scheme, which ties payments to construction milestones. This is consistent with the progressive payment rules that already apply to most new launches.

For a detailed analysis of these changes and their implications, read our companion article: Singapore EC Rule Changes May 2026: 10-Year MOP, No DPS and 90% First-Timer Quota Explained.

EC Minimum Occupation Period (MOP) — What You Can and Cannot Do

The EC Minimum Occupation Period is 5 years, measured from the date of key collection (i.e., from the date the unit is physically occupied, not from TOP or purchase date). During the 5-year MOP, the EC owner must live in the unit and cannot sell or sublet the entire unit to a third party. Individual rooms may be rented to authorised occupants, subject to HDB’s prevailing subletting rules.

After completing the 5-year MOP, the EC may be sold on the open market to Singapore Citizens and PRs (but not yet foreigners or entities, as the privatisation has not yet occurred). After the 15-year privatisation milestone (under the new rules), the EC may be sold to any buyer worldwide including foreigners and companies — at which point standard ABSD rates apply to the buyer based on their profile and property count.

EC vs Private Condo: Price Gap and Value Proposition (2016–2026)

The persistent price gap between EC new launches and comparable OCR private condominiums has historically closed over time as the EC approaches and then passes privatisation. Buyers who purchased ECs at launch in 2014–2017 have typically seen capital appreciation of 25–45% by the time of privatisation around 2024–2027, in many cases outperforming comparable OCR condominiums on a per-unit basis given the lower entry price.

The 2026 EC launch pipeline includes several projects across the OCR and RCR, including Altura EC (Bukit Batok West Avenue 8) and Novo Place (Tengah Garden Avenue), which are near-completion or recently TOP’d, as well as upcoming launches in Tampines, Tengah, and Bedok areas. Under the new 15-year privatisation rule, buyers of 2026 ECs should note that the privatisation milestone does not arrive until approximately 2040–2041, extending the HDB-rule period compared with earlier vintages.

Worked Example: The Lim Family Buying a 2026 EC Launch

Mr and Mrs Lim are a Singapore Citizen couple, both aged 34. Their combined gross monthly income is S$12,000. They are first-time buyers who have never owned any private property or subsidised HDB flat. They are applying for a new EC launch at Tengah, priced at S$1.45M for a 1,000 sq ft three-bedroom unit.

| Item | Amount | Notes |

|---|---|---|

| Purchase price | S$1,450,000 | 1,000 sq ft, 3-bedroom EC at ~S$1,450 psf |

| CPF AHG (income S$12,000 — no AHG; AHG requires ≤S$10,000) | S$0 | Income S$12,000 exceeds AHG S$10,000 ceiling |

| CPF Family Housing Grant (FHG) | S$10,000 | First-timer family; income ≤ S$16,000 — fully eligible |

| Effective purchase price after grant | S$1,440,000 | Grant applied against CPF OA balance |

| ABSD | S$0 | First EC purchase from developer — ABSD-exempt |

| BSD | S$43,400 | On S$1.45M: 1%×180k + 2%×180k + 3%×640k + 4%×450k |

| Bank loan (75% LTV) | S$1,087,500 | Based on purchase price S$1.45M × 75% |

| Minimum cash downpayment (5%) | S$72,500 | Must be paid in cash |

| CPF OA (remaining 20% downpayment) | S$290,000 | From CPF OA (including FHG S$10,000) |

| Monthly mortgage (25 years @ 3.5%) | ~S$5,440/month | MSR = 45.3% — EXCEEDS 30% MSR; must increase downpayment or reduce loan |

| Adjusted: loan S$800,000 (55.2% LTV), 30 yrs @ 3.5% | ~S$3,593/month | MSR = 29.9% — within 30% MSR limit. Requires additional S$287,500 in CPF/cash. |

This worked example illustrates a critical affordability tension: the MSR of 30% cap on the EC mortgage can force buyers with a combined income of S$12,000 to make a larger downpayment than the minimum 25% required by LTV rules. At S$1.45M and a 3.5% bank rate, a 75% LTV loan of S$1.0875M requires monthly repayments of approximately S$5,440 — an MSR of 45.3%, far above the 30% limit. The Lim family would need to either reduce the loan amount (by increasing their downpayment to approximately 44.8%), buy a smaller or lower-priced unit, or wait until their income increases. This is a common challenge for buyers in the S$11,000–S$16,000 income band looking at 3-bedroom ECs in 2026.

EC Buying Summary — Key Rules at a Glance (2026)

| Rule / Parameter | Current Position (Post–8 May 2026) |

|---|---|

| Income ceiling (family) | S$16,000/month |

| Income ceiling (singles, age 35+) | S$8,000/month (Joint Singles Scheme) |

| First-timer priority at launch | 90% of units — raised from 70% on 8 May 2026 |

| ABSD on new EC purchase | Nil (ABSD-exempt for eligible buyers under EC scheme) |

| Minimum Occupation Period | 5 years (from key collection date) |

| Full-unit rental restriction | 10 years from TOP (new rule from 8 May 2026) |

| Privatisation period | 15 years from TOP (new rule; previously 10 years) |

| Deferred Payment Scheme | Abolished — Normal Progressive Payment only (8 May 2026) |

| CPF AHG (max) | S$30,000 (income ≤ S$10,000/month) |

| CPF FHG (max) | S$10,000 (income ≤ S$16,000/month) |

| Loan type | Bank loan only (no HDB concessionary loan) |

| MSR cap | 30% of gross monthly income |

| TDSR cap | 55% of gross monthly income |

| Maximum LTV | 75% (no existing property loans) |

What Might Come Next for the EC Scheme?

The 8 May 2026 cooling measures signal a clear policy intent: the Government views the EC as a genuine first-home product for middle-income Singaporeans, not a short-to-medium-term investment vehicle. The extension of the rental restriction to 10 years and the privatisation period to 15 years both reduce the speculative premium that early-privatisation buyers have historically captured.

Going forward, it is possible that: the income ceiling is revised upward to keep pace with nominal wage growth; additional GLS sites are released to increase EC supply given strong demand from HDB upgraders; or that the 30-month private property wait-out period for EC applicants is extended further. These are speculative scenarios — any changes would be announced by HDB and take effect from the announcement date.

For buyers evaluating ECs in the 2026 pipeline, the longer privatisation horizon means a re-pricing of the “privatisation premium” into the expected hold period. Buyers who are genuinely owner-occupiers over a 15-year horizon are largely unaffected — but those who were banking on a 10-year exit into the private market will need to revise their investment thesis.

Related Articles

- Singapore EC Rule Changes May 2026: 10-Year MOP, No DPS and 90% First-Timer Quota Explained

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- TDSR and MSR Singapore 2026: Complete Guide to Property Borrowing Limits

- CPF Housing Grant for Resale Singapore 2026: Complete Guide to EHG, PHG and Step-Up Grant

- HDB BTO Application Process Singapore 2026: Step-by-Step Guide from Eligibility to Keys

- Conveyancing Fees Singapore 2026: Legal Costs for Buying and Selling Property

- Stamp Duty Calculator Singapore 2026: Complete BSD and ABSD Guide for Every Buyer

Frequently Asked Questions

Can a Singapore PR buy a new EC directly from the developer?

No. At least one applicant in the household must be a Singapore Citizen to buy a new EC from the developer. A Singapore PR may be listed as an occupier or co-applicant only if the primary applicant is a Singapore Citizen. After the EC completes its 5-year MOP, it may be sold to SC or SPR buyers. After privatisation (15 years from TOP under the new rules), it may be sold to foreigners and entities as well.

Do I pay ABSD when buying an EC from the developer?

No, ABSD is not payable on a first EC purchase from the developer under the EC eligibility scheme, provided you qualify under one of HDB’s approved eligibility schemes and the purchase is your first-ever subsidised property. However, if you already own a private residential property (and have not disposed of it within 30 months before applying), you are ineligible for the EC scheme entirely. ABSD applies normally if you purchase a fully privatised EC on the resale market after the 15-year privatisation milestone, as that is treated as a standard private property purchase.

What is the difference between an EC’s MOP and the rental restriction?

These are two distinct rules. The MOP (5 years from key collection) governs when you can sell the EC unit — you must hold and occupy it for 5 years before selling on the open market. The full-unit rental restriction (now 10 years from TOP under the 8 May 2026 rules) governs when you can rent out the entire unit to a third-party tenant. You can rent individual rooms at any time to authorised occupants, but cannot vacate the unit entirely and sublet it as a whole during the 10-year period. Both rules apply concurrently — you may therefore sell after 5 years, but the buyer cannot rent it out until the 10-year rental restriction expires.

Can I use CPF to buy an EC?

Yes. CPF Ordinary Account (OA) savings may be used to pay the downpayment (except the mandatory 5% cash portion), stamp duties, and monthly mortgage instalments for an EC, subject to the Valuation Limit and Withdrawal Limit rules. CPF housing grants (AHG and FHG) are credited to your CPF OA and can be applied against the purchase price. The standard CPF accrued interest rules apply — any CPF OA used must be returned with accrued interest (currently 2.5% per annum) when the property is eventually sold.

Is an EC a good investment in 2026?

The investment case for ECs has historically been strong for genuine owner-occupiers. The entry price discount (versus comparable private condominiums) combined with appreciation to private-market values at and after privatisation has generated solid capital gains for many EC buyers over 10–15-year hold periods. However, the new 15-year privatisation rule extends the investment horizon and reduces the liquid exit window. ECs are best regarded as a long-term owner-occupier decision with an embedded investment component, not a short-cycle flip. Gross rental yields for EC units approaching privatisation (around 3.5–4.5%) are competitive with OCR private condominiums. Buyers should factor in the MSR borrowing constraint, which can require a higher-than-minimum downpayment at today’s price levels, reducing their effective leverage and upfront capital efficiency compared with a similarly-sized HDB flat purchase.

What upcoming EC projects are launching in 2026?

The 2026 EC launch pipeline includes several projects across the OCR. Watch the LovelyHomes EC Launches page for the latest project information as details are confirmed. Key sites in the URA 1H2026 GLS Confirmed List include Tengah Garden Avenue (multiple phases), Tampines North, and a Bedok South site. Pricing at new launches has been in the S$1,400–S$1,550 psf range based on recent comparable awards; final prices depend on developer cost structures and market conditions at the time of launch.

Disclaimer: This article is for general information and educational purposes only. It does not constitute legal, financial, or investment advice. EC eligibility rules, income ceilings, CPF grant amounts, and cooling-measure parameters are set by HDB and the Singapore Government and may change at any time. Always verify the current position on the HDB website and consult a licensed property agent (CEA-registered), conveyancing lawyer, and/or licensed financial adviser before making any property decision. LovelyHomes is not a licensed property agent and does not represent any developer, agent, or financial institution.

Click anywhere or press Esc to close