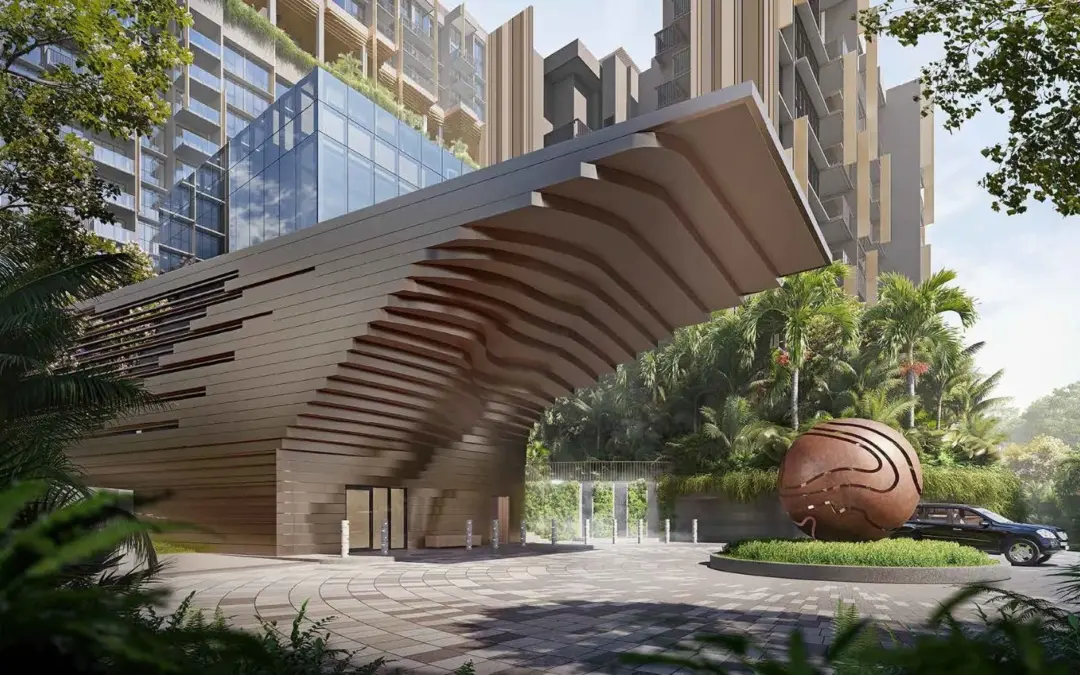

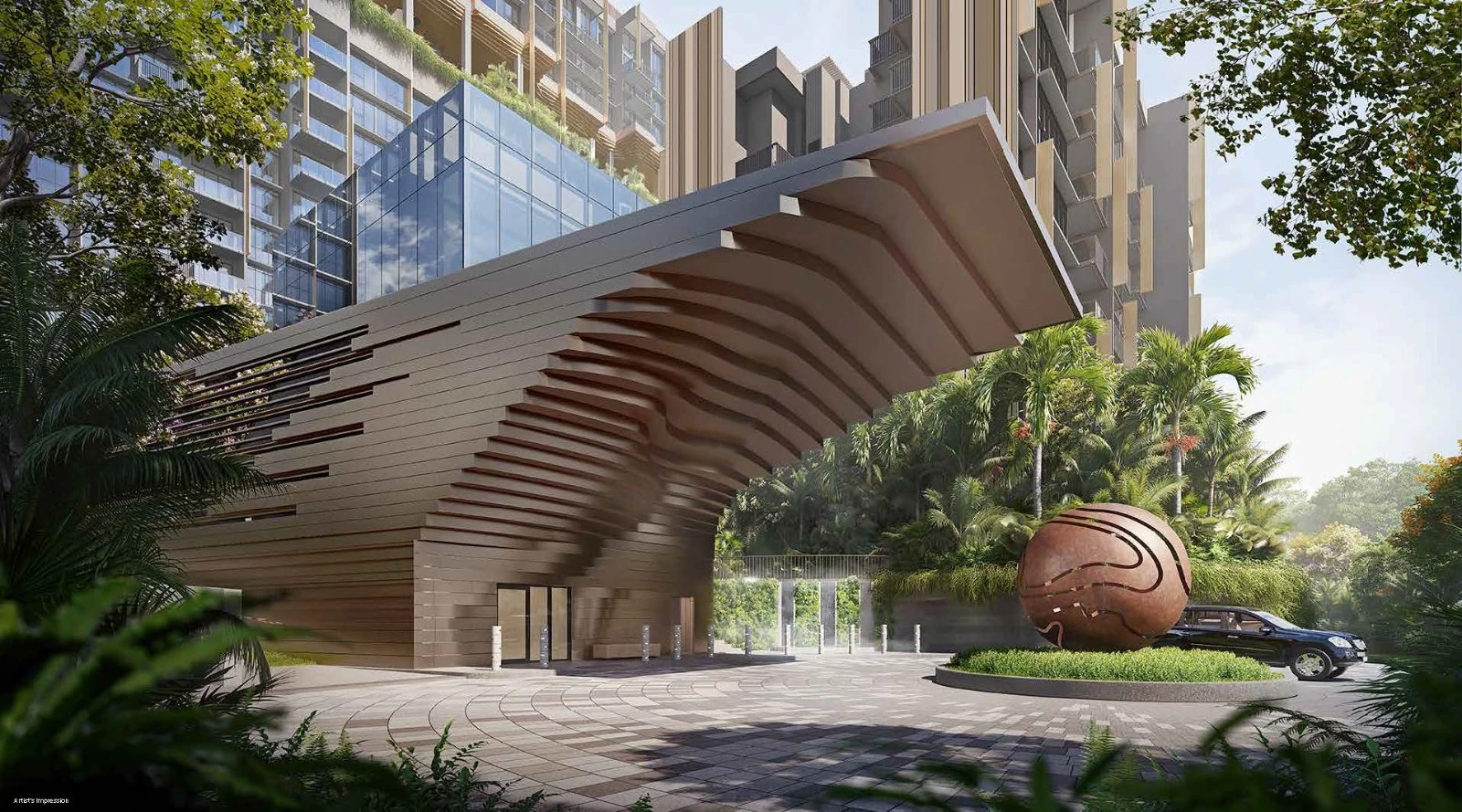

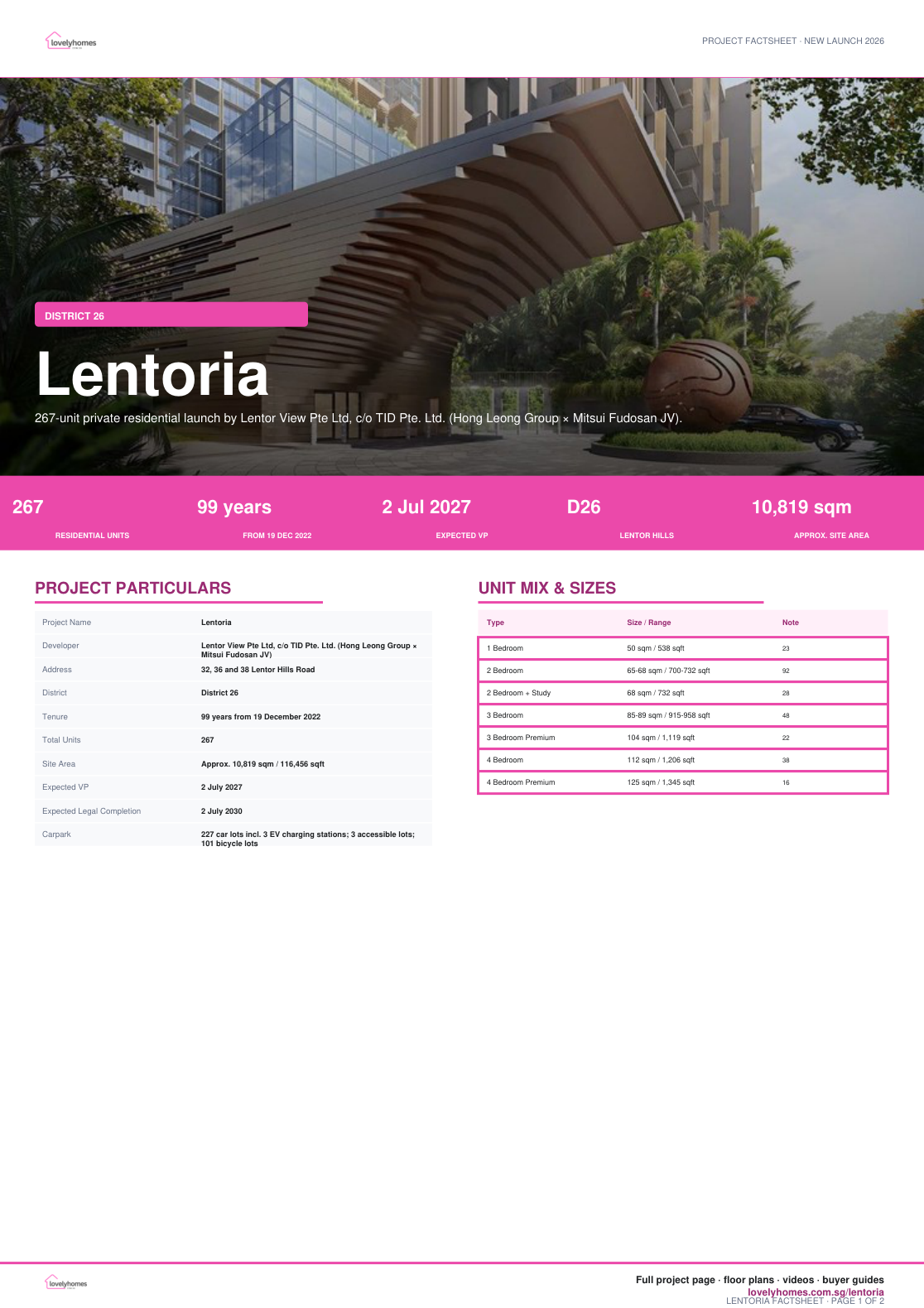

Lentoria is a 267-unit private residential development at Lentor Hills Road, planned as two 17-storey blocks and one 8-storey block with two basement carpark levels and communal facilities.

01 · Location

Lentor Hills address

Near Lentor MRT on the Thomson-East Coast Line, Lentor Modern and the established Ang Mo Kio / Upper Thomson residential corridor.

02 · Concept

Private park home

Project document positions Lentoria around lush landscaping, water features, a 50m lap pool and Level 14 sky terrace facilities.

03 · Mix

1BR to 4BR Premium

Bedroom options range from 50 sqm 1-bedroom units to 125 sqm 4-bedroom premium layouts.

Project At-a-Glance

Project Name

Lentoria

Developer

Lentor View Pte Ltd, c/o TID Pte. Ltd. (Hong Leong Group × Mitsui Fudosan JV)

Address

32, 36 and 38 Lentor Hills Road

District

District 26

Tenure

99 years from 19 December 2022

Total Units

267

Site Area

Approx. 10,819 sqm / 116,456 sqft

Expected VP

2 July 2027

Expected Legal Completion

2 July 2030

Carpark

227 car lots incl. 3 EV charging stations; 3 accessible lots; 101 bicycle lots

Unit Mix and Sizes

Bedroom Type

Size

Units

% of Total

1 Bedroom

50 sqm / 538 sqft

23

8.6%

2 Bedroom

65-68 sqm / 700-732 sqft

92

34.5%

2 Bedroom + Study

68 sqm / 732 sqft

28

10.5%

3 Bedroom

85-89 sqm / 915-958 sqft

48

18.0%

3 Bedroom Premium

104 sqm / 1,119 sqft

22

8.2%

4 Bedroom

112 sqm / 1,206 sqft

38

14.2%

4 Bedroom Premium

125 sqm / 1,345 sqft

16

6.0%

Unit mix is taken from the available project factsheet. Download the full floor-plan PDF below for individual type layouts.

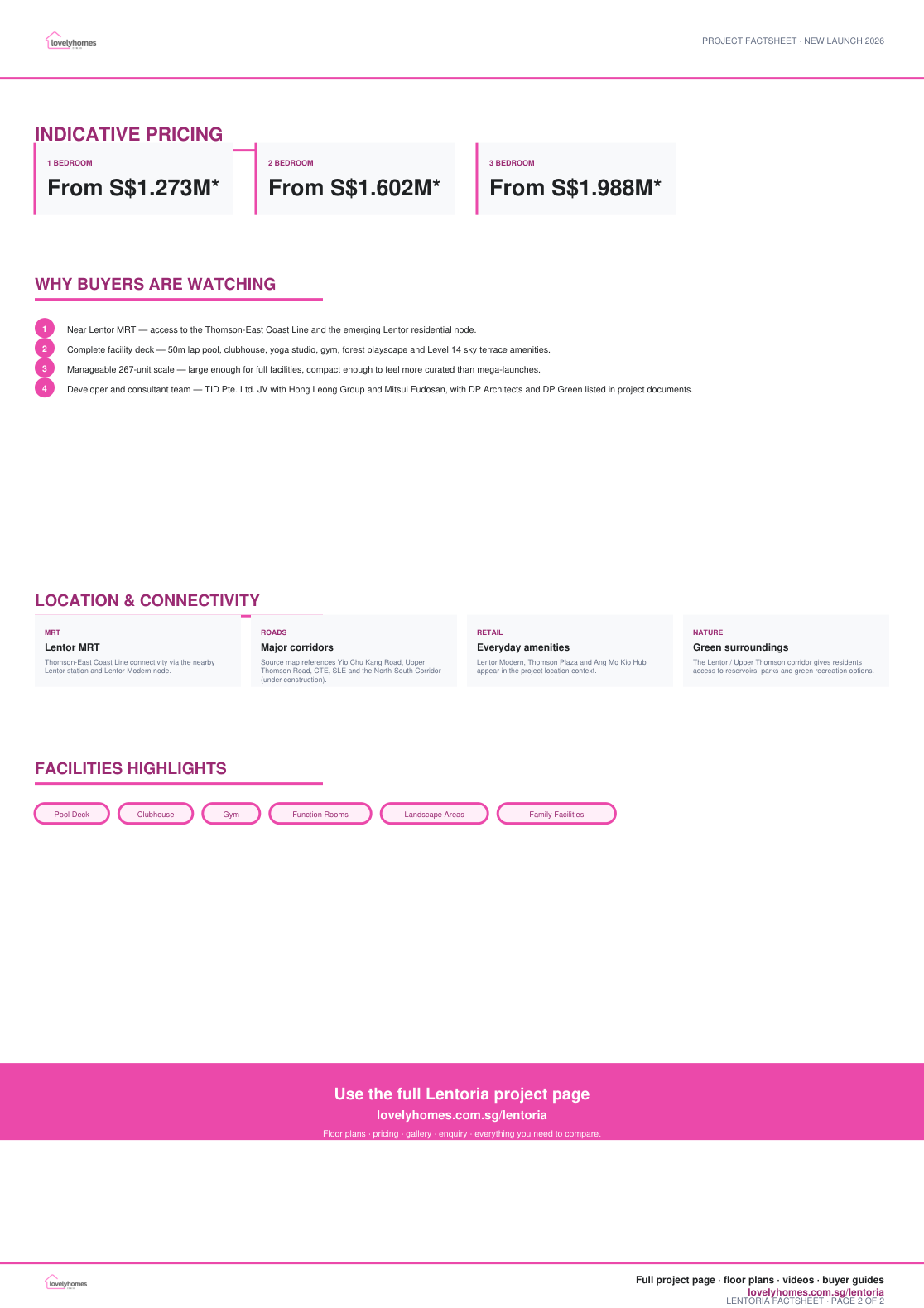

Indicative Pricing

1 Bedroom

From S$1.273M*

2 Bedroom

From S$1.602M*

3 Bedroom

From S$1.988M*

4 Bedroom

From S$2.598M*

*Indicative figures are extracted from the available source price matrix dated 18 August 2024 and may be outdated. Verify current developer availability, discounts and stamp-duty exposure before committing.

Why Buyers Are Watching

1

Near Lentor MRT — access to the Thomson-East Coast Line and the emerging Lentor residential node.

2

Complete facility deck — 50m lap pool, clubhouse, yoga studio, gym, forest playscape and Level 14 sky terrace amenities.

3

Manageable 267-unit scale — large enough for full facilities, compact enough to feel more curated than mega-launches.

4

Developer and consultant team — TID Pte. Ltd. JV with Hong Leong Group and Mitsui Fudosan, with DP Architects and DP Green listed in project documents.

Location and Connectivity

MRT

Lentor MRT

Thomson-East Coast Line connectivity via the nearby Lentor station and Lentor Modern node.

Roads

Major corridors

Source map references Yio Chu Kang Road, Upper Thomson Road, CTE, SLE and the North-South Corridor (under construction).

Retail

Everyday amenities

Lentor Modern, Thomson Plaza and Ang Mo Kio Hub appear in the project location context.

Nature

Green surroundings

The Lentor / Upper Thomson corridor gives residents access to reservoirs, parks and green recreation options.

Schools Nearby

Primary Schools

Check MOE SchoolFinder for the current registration year and exact home-school distance from 32/36/38 Lentor Hills Road.

Nearby Education Nodes

Ang Mo Kio, Upper Thomson and Yio Chu Kang education options are within the broader residential corridor.

Verification

Do not rely on marketing-distance claims without confirming distance bands and enrolment rules for the relevant year.

Lifestyle and Amenities

Water and wellness

50m lap pool, kid’s wading pool, hydrotherapy spa, cabana/sun deck, gymnasium and yoga studio.

Social spaces

Clubhouse, Garden Lounge, Forest Lounge, BBQ pavilions, dining pavilion and party deck.

Green living

Forest Playscape, Botanical Collection, dog run, jogging/walking trail, garden library and outdoor fitness.

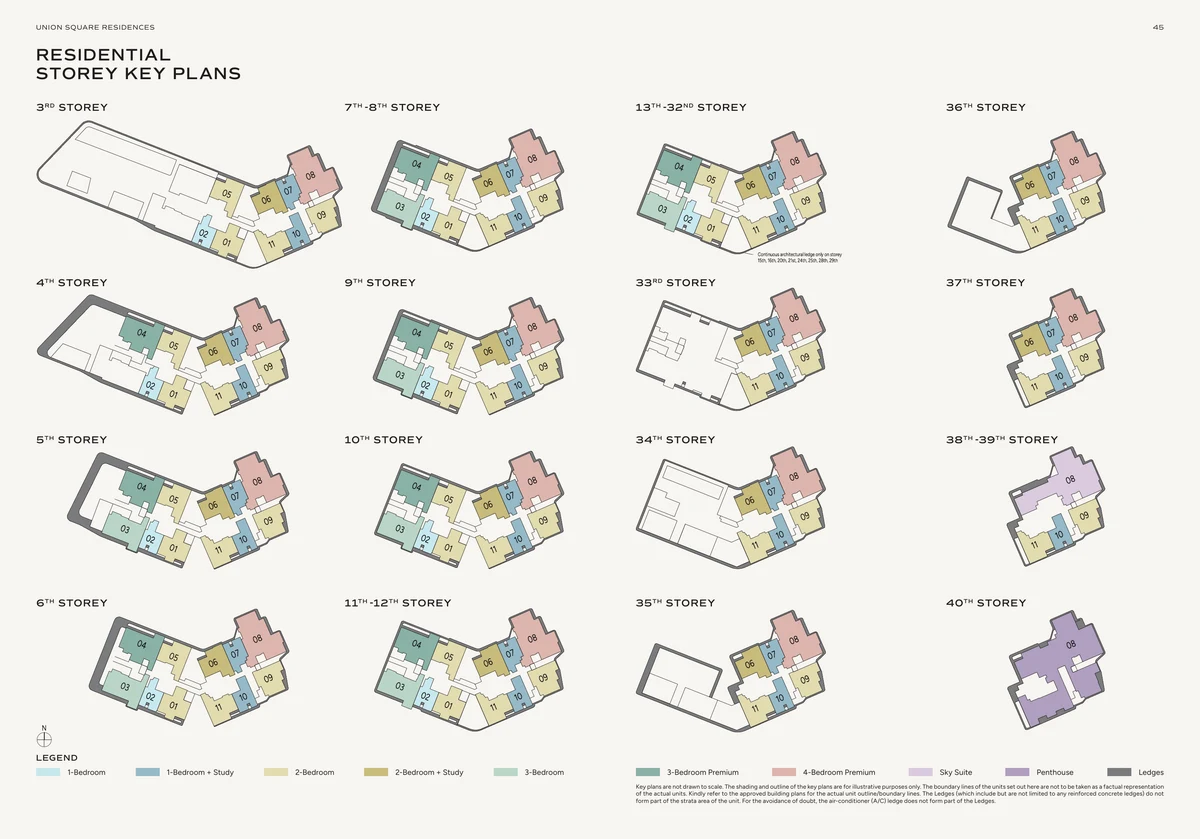

Site Plan

Actual site plan from Lentoria project documents · indicative and subject to developer confirmation

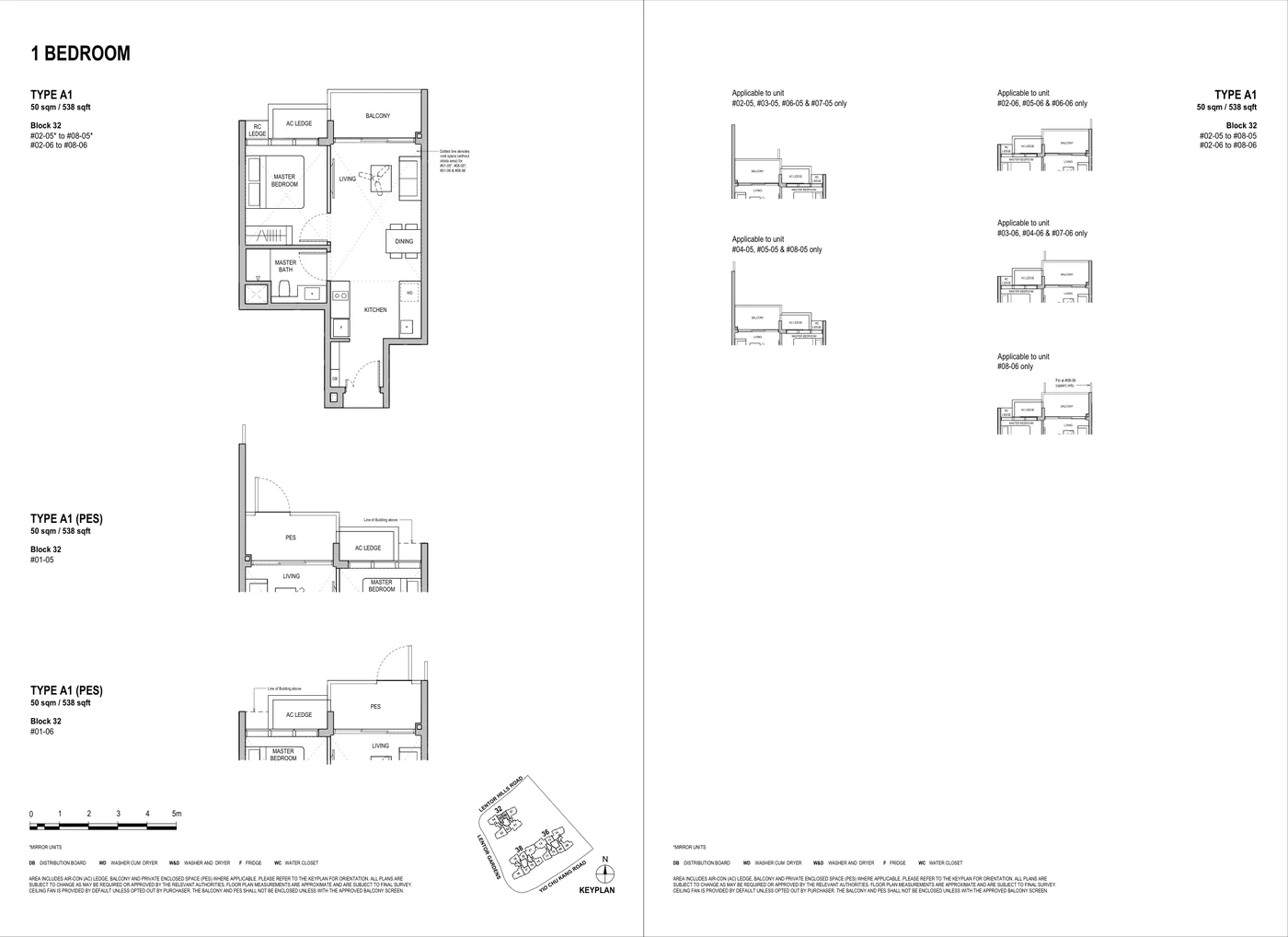

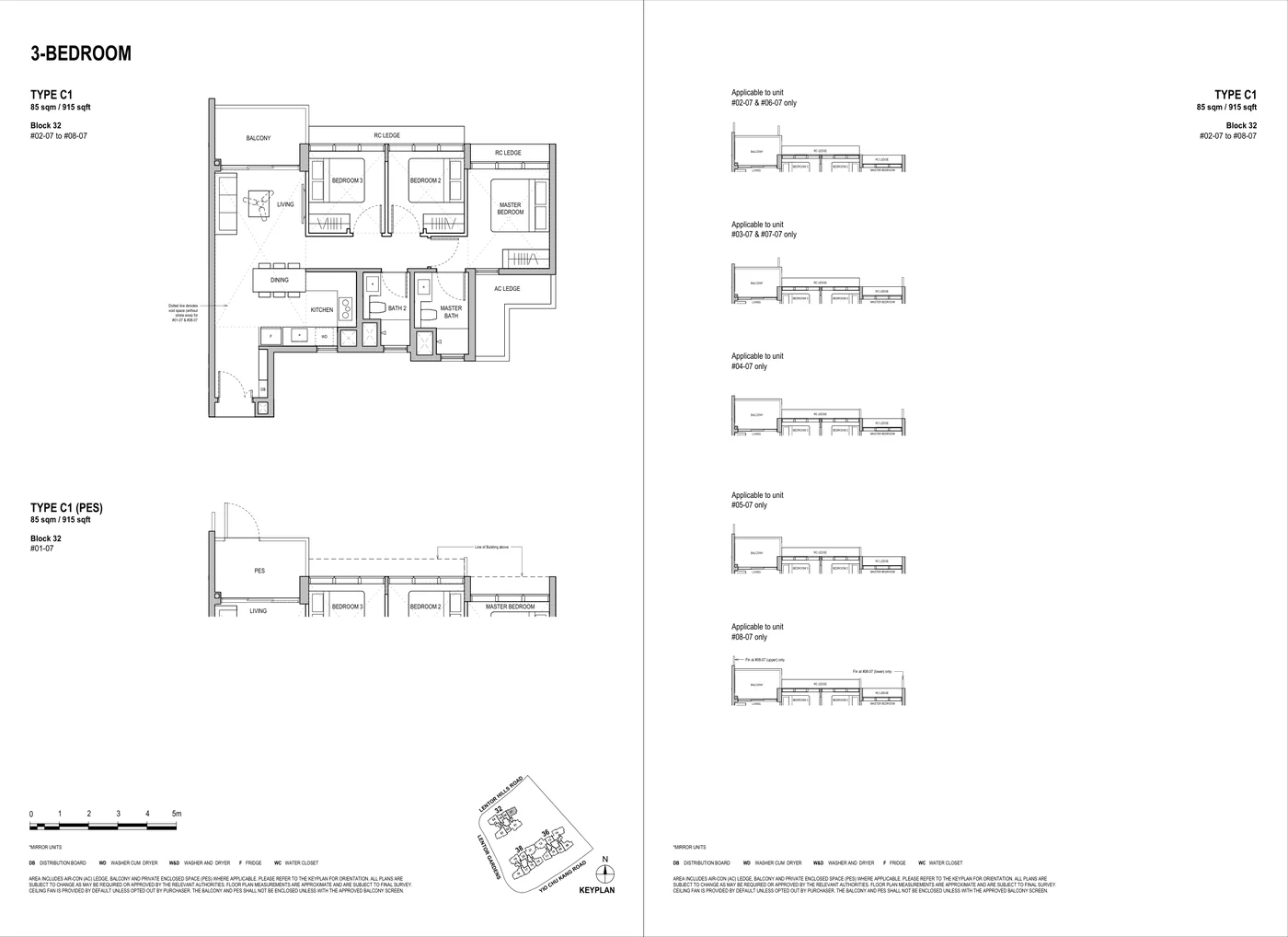

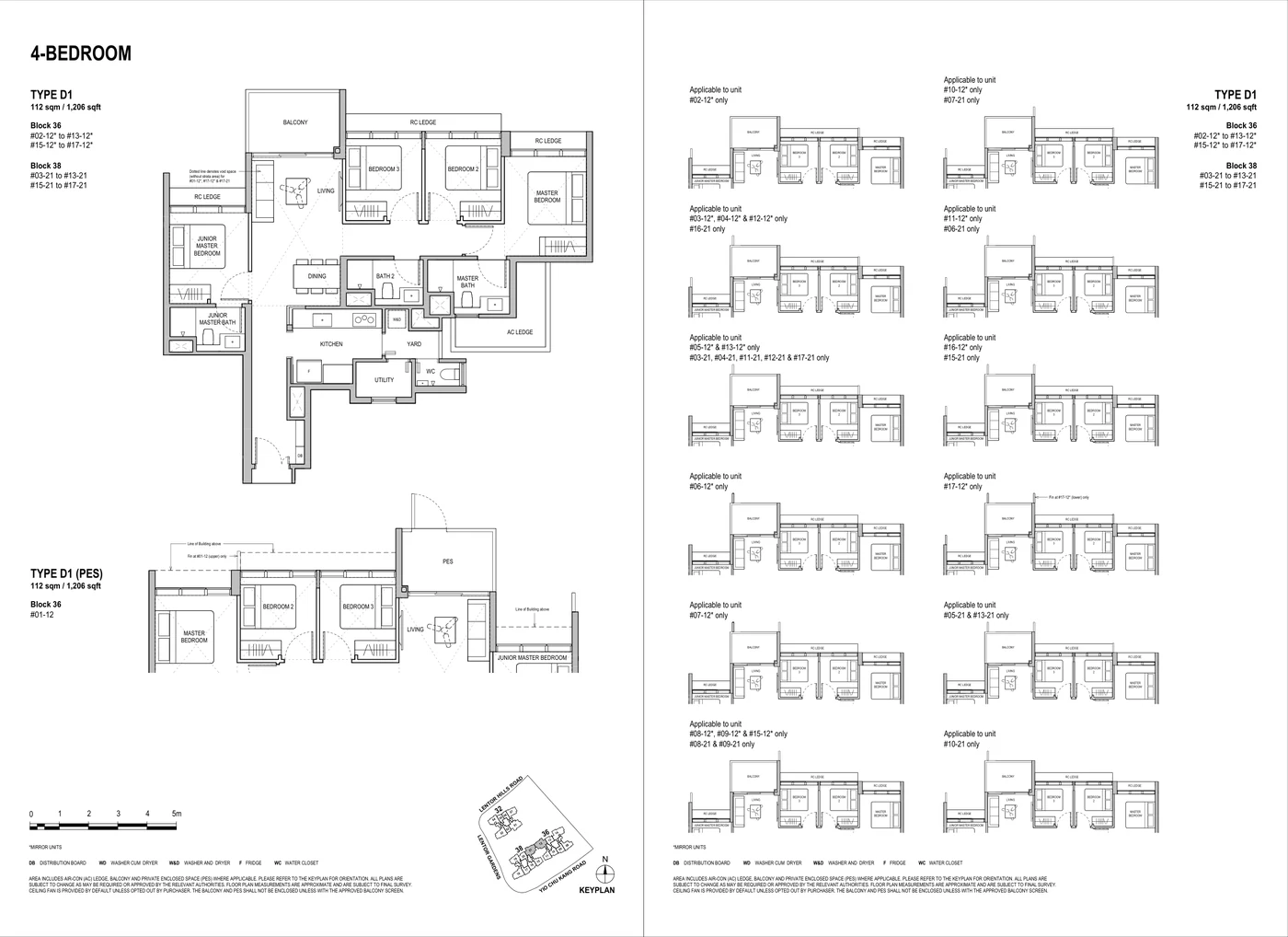

Floor Plans (Selected)

Representative actual plans by unit type. Download the full PDF below for all layouts, including 2BR + Study, 3BR Premium and 4BR Premium variants.

1 Bedroom Type A150 sqm / 538 sqft

2 Bedroom Type B165 sqm / 700 sqft

3 Bedroom Type C185 sqm / 915 sqft

4 Bedroom Type D1112 sqm / 1,206 sqft

4 Bedroom Premium Type D3P125 sqm / 1,345 sqft

Full Floor Plans PDF

Official Lentoria floor-plan PDF with all selected bedroom types and keyplan references.

Lentoria is located at 32, 36 and 38 Lentor Hills Road in District 26.

Who is the developer of Lentoria?

The project developer is Lentor View Pte Ltd, c/o TID Pte. Ltd., described in the project factsheet as a joint venture between Hong Leong Group and Mitsui Fudosan.

How many units does Lentoria have?

Lentoria has 267 residential units across two 17-storey blocks and one 8-storey block.

When is the expected TOP?

The source factsheet states expected vacant possession on 2 July 2027 and expected legal completion on 2 July 2030.

Are prices current?

The displayed figures are indicative and extracted from an available source price matrix dated 18 August 2024. Latest availability and discounts must be verified before purchase.

Ready to see Lentoria in person?

Request the latest availability, current pricing and viewing slots before relying on older source price matrices.

Progressive payment, ABSD timing, and rental income.

Disclaimer. Prices, unit mix, specifications, site plans, floor plans and facility lists on this page are indicative only and subject to change by the developer without notice. Information has been compiled from available developer materials and verified for this LovelyHomes page update on 27 April 2026. LovelyHomes.com.sg is not the project developer. Prospective buyers should verify the latest developer sales kit, availability and pricing before committing to any purchase. Artist impressions are for illustrative purposes only and may differ from the final built product.

Union Square · District 01/02 · CCR · Mixed-Use Integrated

Union Square Residences

CDL’s 40-storey luxury residential tower at the heart of Clarke Quay — 366 homes integrated with premium office, co-living, retail, and dining at Singapore’s most vibrant riverside address.

Union Square Residences is City Developments Limited’s (CDL) landmark mixed-use development at the historic intersection of Clarke Quay, the Singapore River, and the CBD — an address that puts residents at the centre of Singapore’s cultural, commercial, and culinary life simultaneously. Rising 40 storeys with 366 luxury residences, Union Square Residences is integrated within Union Square Central, a dynamic precinct combining a 20-storey premium Grade A office tower, a new co-living concept, conservation heritage shophouses, and an activated Central Plaza with ground-floor retail, dining, and community programming.

What was once the gateway to Singapore is now the most coveted urban address: where the CBD’s financial might meets Clarke Quay’s nightlife, Fort Canning Park’s greenery meets Singapore River’s heritage, and Raffles Place MRT meets the Thomson-East Coast Line — all within walking distance.

01 · Address

Clarke Quay — Singapore’s Most Vibrant Riverside Precinct

Walking distance from Raffles Place MRT, Clarke Quay MRT, Fort Canning Park, the National Gallery, and Singapore River’s iconic dining and entertainment strip. Between everywhere that matters.

02 · Integrated Living

One Development. Boundless Possibilities.

Residences integrated with a Grade A office tower, co-living, retail, F&B, and a new Central Plaza for events, performances, and community — a true live-work-play ecosystem rarely available at this price point.

03 · Developer Pedigree

CDL — 60+ Years of Premium Delivery

City Developments Limited is one of Singapore’s largest listed developers with over 60 years of residential and commercial delivery across Singapore and 26 countries. BCA Green Mark Platinum Super Low Energy certification.

Project At-a-Glance

Project Name

Union Square Residences

Developer

City Developments Limited (CDL)

Address

Union Square, Clarke Quay / Singapore River, District 01/02

Activated plaza with food trucks, performances, community events

Unit Mix and Sizes

Bedroom Type

Unit Type

Size (sqft)

Size (sqm)

Notes

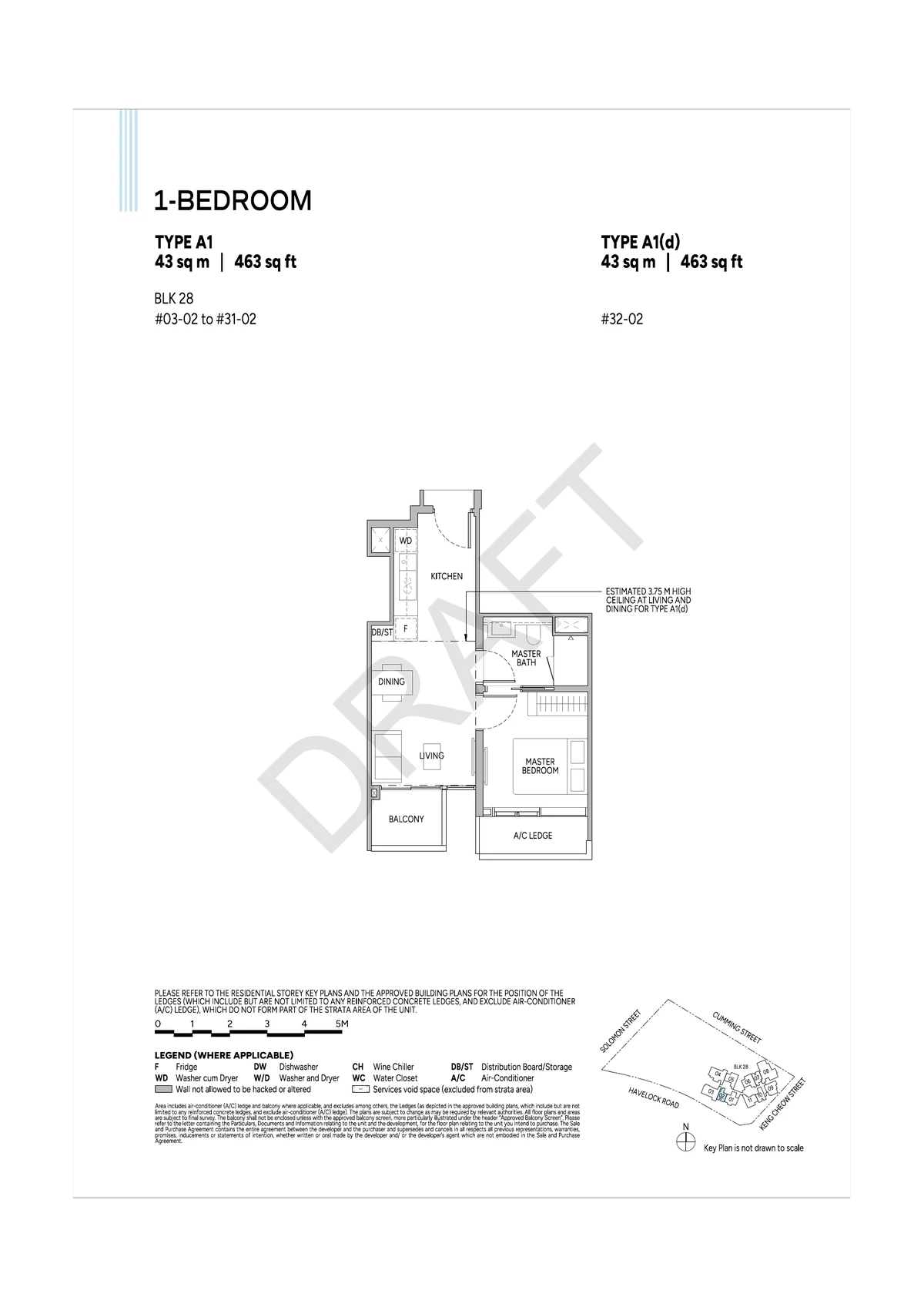

1-Bedroom

Type A1 / A1(d)

463

43

Type A1(d) features 3.75 m high ceiling at living & dining

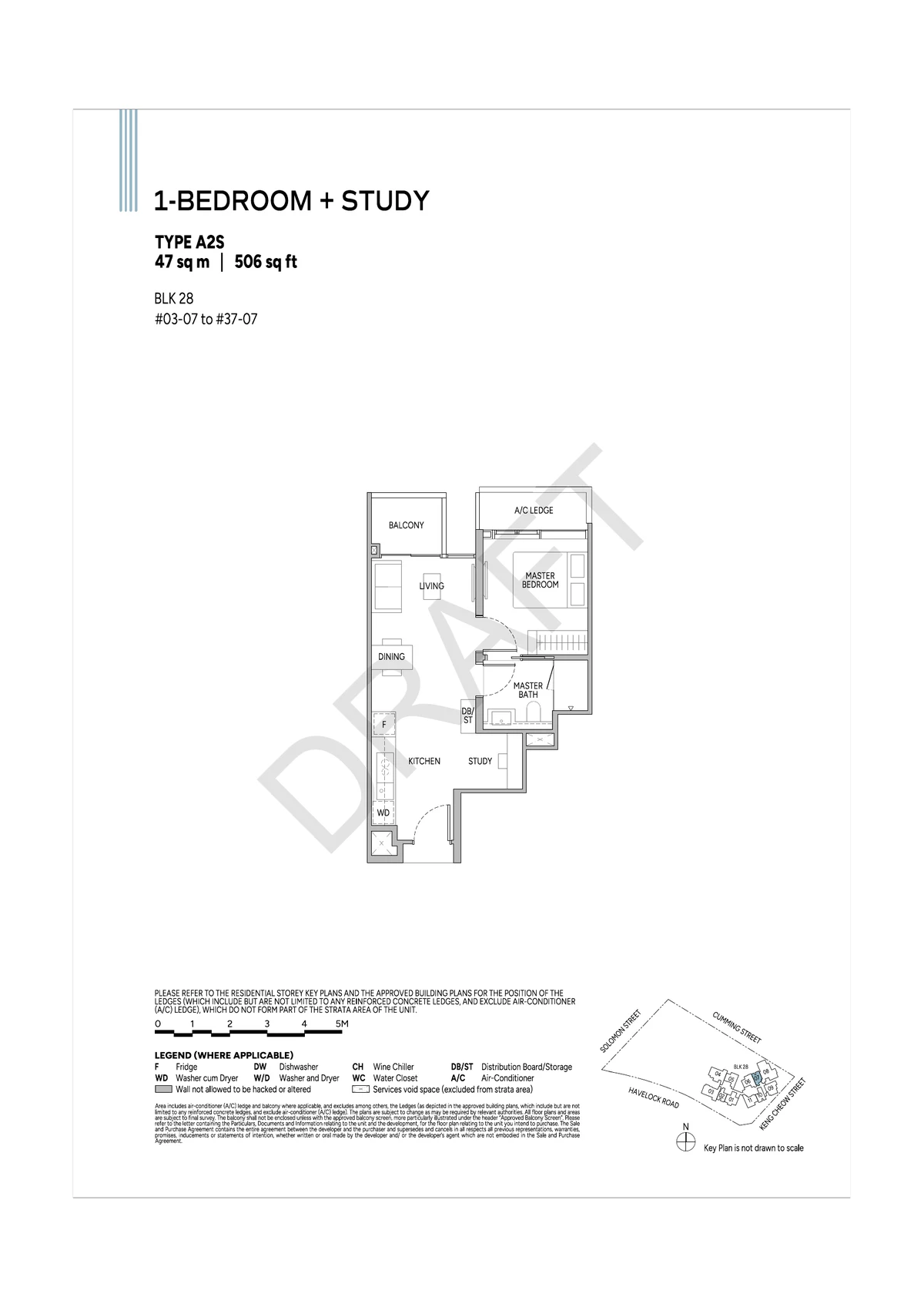

1-Bedroom + Study

Type A2S

506

47

Study adjacent to master bedroom

1-Bedroom + Study

Type A3S

506

47

Alternate layout

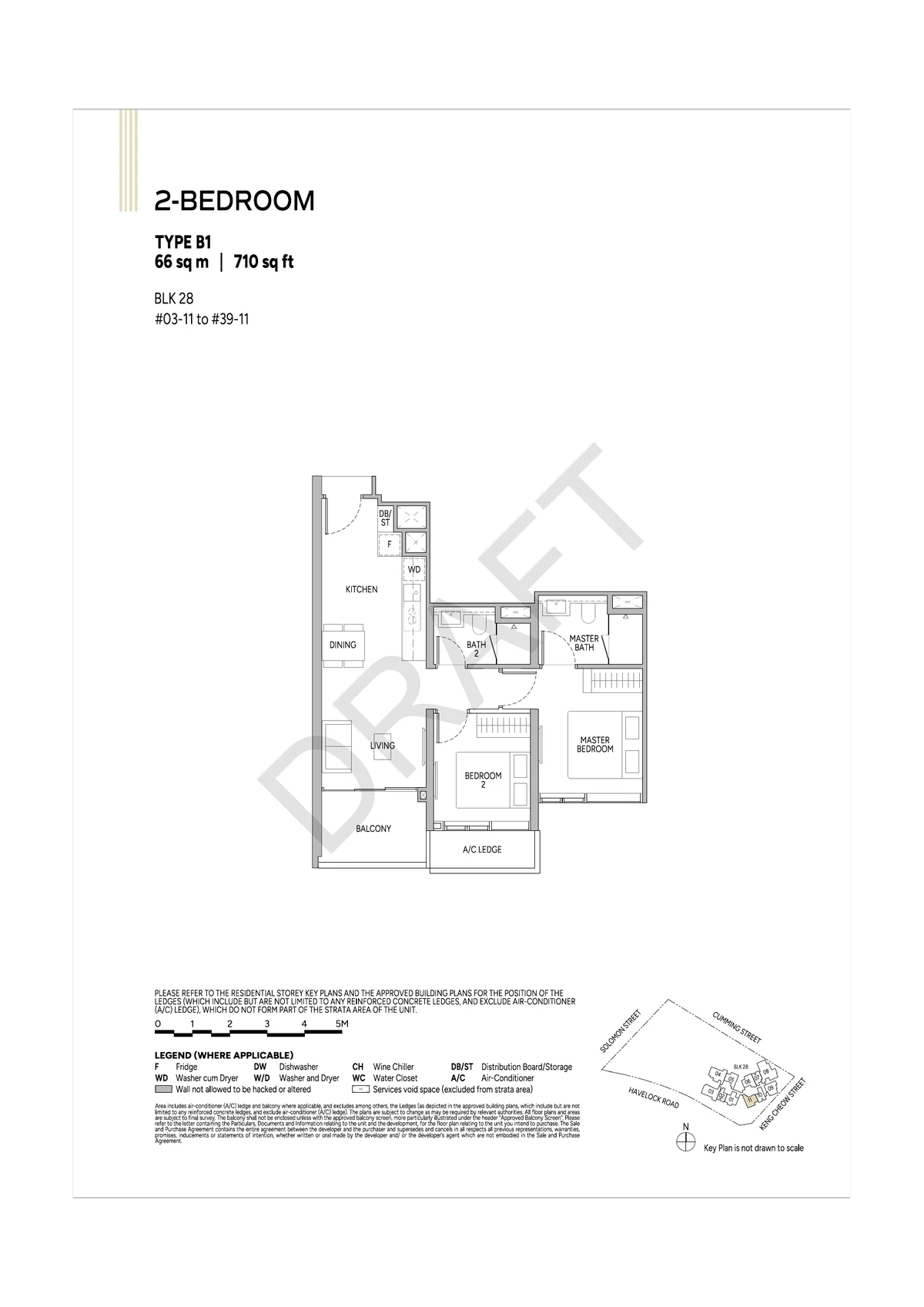

2-Bedroom

Type B1

710

66

2 bedrooms, 2 bathrooms

2-Bedroom

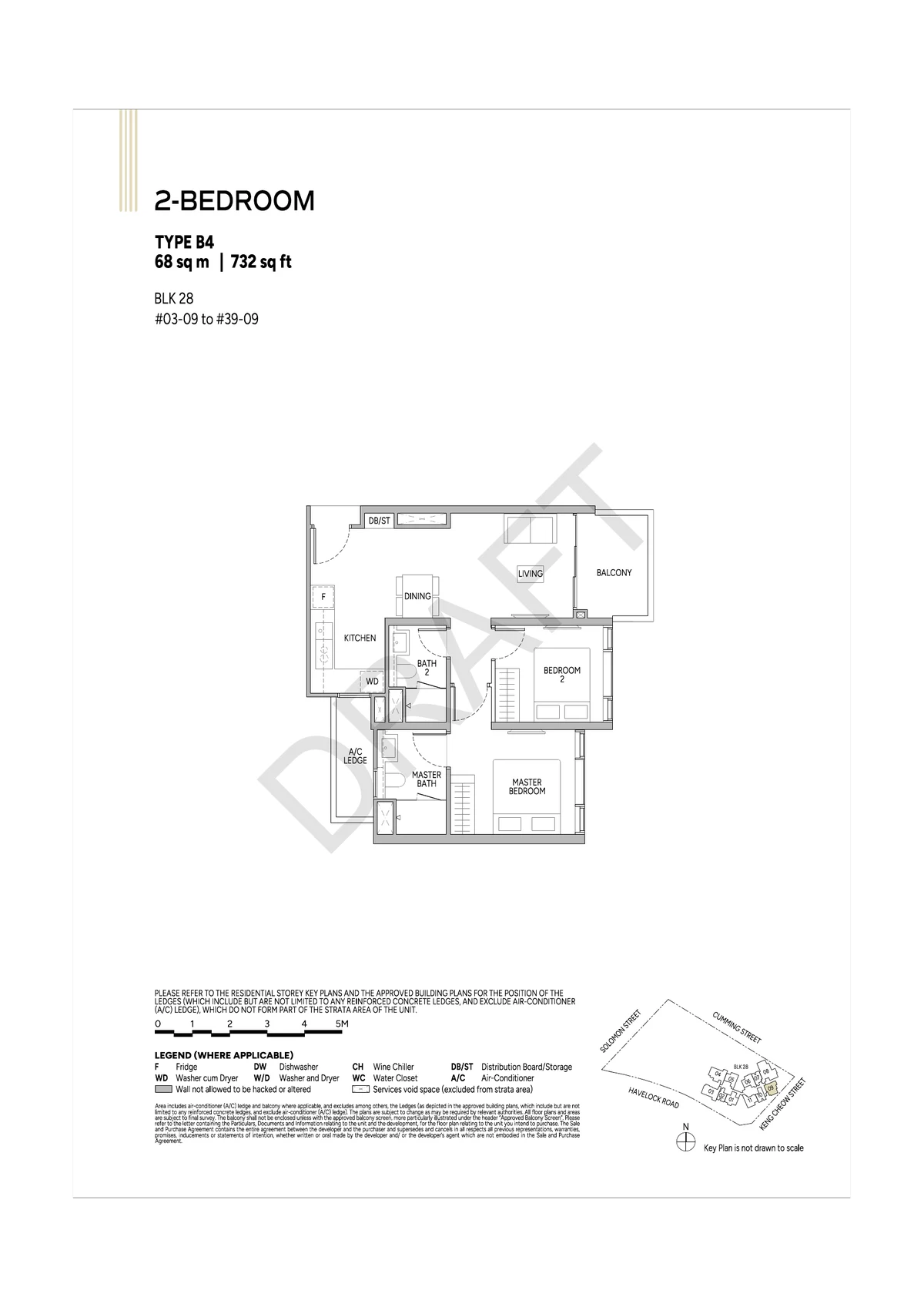

Type B4

732

68

Larger 2-bedroom configuration

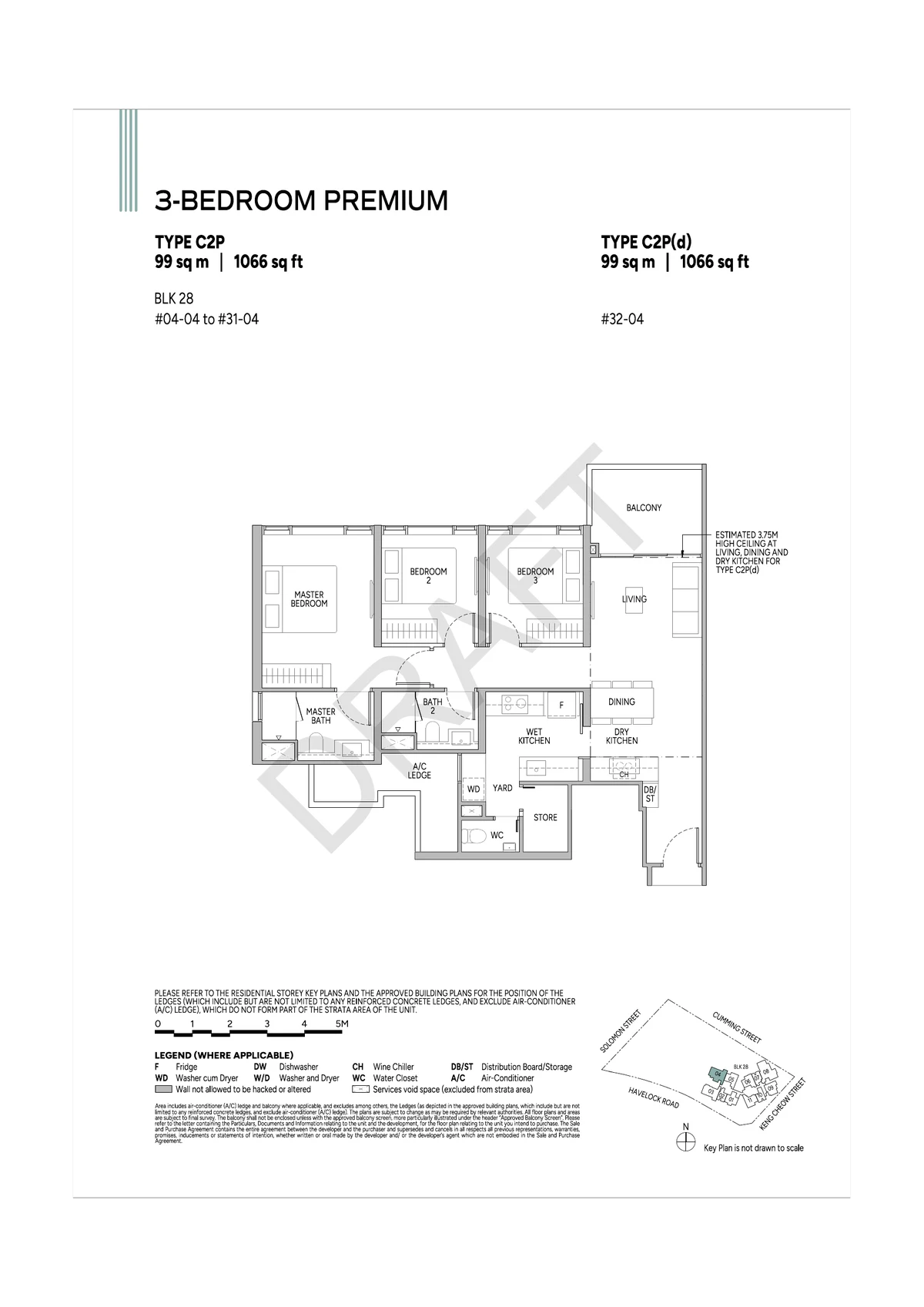

3-Bedroom Premium

Type C2P / C2P(J)

1,066

99

Junior master bedroom option available

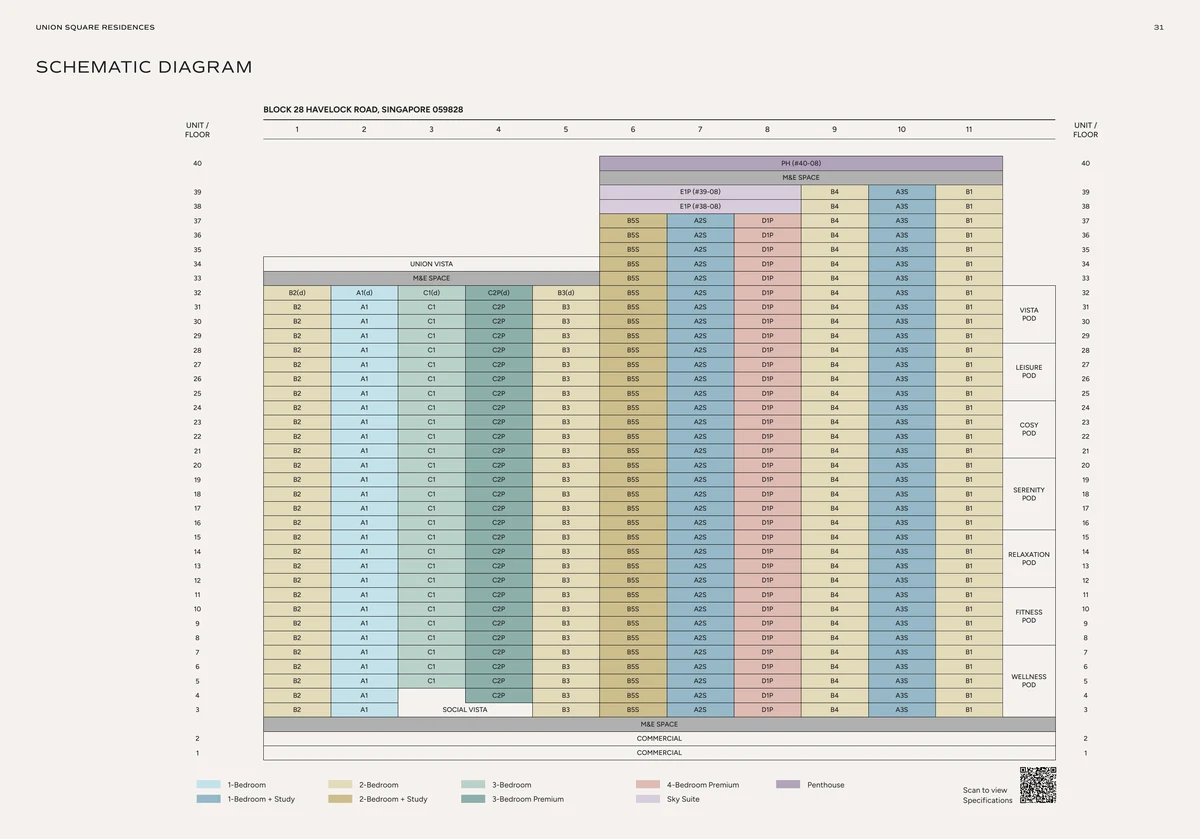

Total: 366 residential units across 40 storeys. Unit availability and exact counts are indicative — refer to the developer’s official sales materials. Download the factsheet for the complete storey key plans.

Indicative Pricing

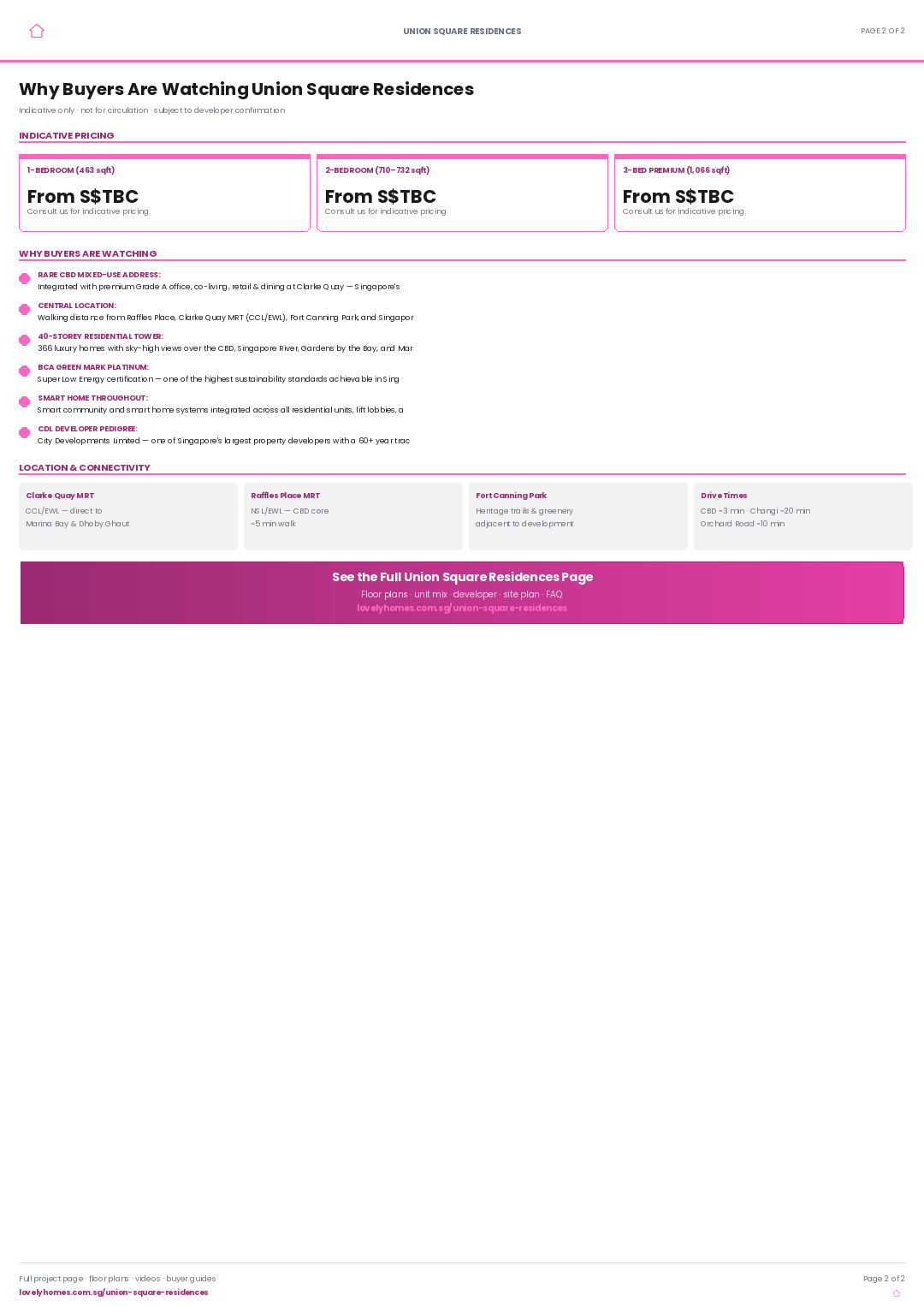

1-Bedroom (463 sqft)

From S$TBC

2-Bedroom (710–732 sqft)

From S$TBC

3-Bed Premium (1,066 sqft)

From S$TBC

Prices are indicative and subject to change. Before ABSD, BSD, and legal fees. Union Square Residences occupies a unique CCR mixed-use position that warrants independent pricing research. See our ABSD guide and BSD guide for stamp duty calculations on CCR purchases.

Why Buyers Are Watching

1

Singapore’s most central live-work-play address. Clarke Quay, Raffles Place, the Singapore River, Fort Canning Park, Gardens by the Bay, and Marina Bay are all reachable on foot or within one MRT stop — a convergence of connectivity that no standalone residential project in Singapore can replicate.

2

BCA Green Mark Platinum Super Low Energy certification. One of the highest sustainability certifications achievable for a Singapore new-launch residential development. Energy efficiency translates to lower utilities bills, higher environmental credentials, and future-proof long-term value.

3

Mixed-use integration amplifies rental demand. The adjacent Grade A office tower, co-living component, and retail/dining activation create a captive pool of tenant demand from professionals working within the Union Square precinct — a structural rental advantage few condo investments enjoy.

4

Clarke Quay rejuvenation is actively underway. The ongoing transformation of Clarke Quay — following major F&B reinvestment, event activations, and the upcoming Canninghill Square integration — structurally supports capital appreciation for all residential stock in the precinct over the medium term.

5

Conservation buildings add irreplicable heritage character. Union Square’s integration of original conservation shophouses within a modern mixed-use development creates a sense of place and aesthetic identity that cannot be replicated by any new GLS development — a permanent differentiator in the secondary market.

6

CDL developer track record is Singapore’s most documented. City Developments Limited has listed on SGX since 1963 and has delivered more than 50,000 homes globally. Past Singapore landmarks include South Beach Residences, Boulevard 88, Canninghill Piers, and The Sail.

7

Smart home and smart community systems are integrated across all units. Including smart access control, visitor management, smart locks, digital concierge, and energy monitoring — systems that contribute to operating cost savings and tenant convenience for investor-held units.

8

Type A1(d) high-ceiling variant is a value differentiator. The 3.75 m ceiling height in the 1-Bedroom Type A1(d) variant is unusual for a Singapore 1-bedroom product at this size — creating a sense of volume and light rarely available at 43 sqm.

Location and Connectivity

MRT Lines

Clarke Quay MRT (NE5)

North-East Line — direct to Dhoby Ghaut, Little India, Harbourfront. Walking distance from development.

MRT Lines

Raffles Place (EW14/NS26)

EW/NS interchange — CBD, Marina Bay, Jurong East, Changi Airport. Approximately 5–8 min walk from development.

Nature

Fort Canning Park

Singapore’s historic hilltop park with heritage trails, WWII tunnels, open-air events, and lush green canopy — adjacent to the development.

Drive Times

CBD & Key Destinations

Raffles Place ~3 min · Orchard Road ~10 min · Changi Airport ~20 min · Marina Bay Sands ~8 min · JB Checkpoint ~45 min

Cantonment Primary School · St Margaret’s Primary School · Outram Secondary School

Secondary Schools

Gan Eng Seng Secondary · Crescent Girls’ School · River Valley High School · Outram Secondary

Tertiary / JC

School of the Arts (SOTA) · Singapore Management University (SMU) · Lasalle College of the Arts

International Schools

Overseas Family School · Stamford American International School · ISS International School

Lifestyle and Amenities

Clarke Quay & Singapore River

Singapore’s most iconic riverside entertainment precinct — Clarke Quay, Boat Quay, and Robertson Quay are all walking distance. Michelin-starred restaurants, heritage shophouses, and waterfront bars are part of daily life at Union Square.

Cultural & Heritage Belt

National Gallery Singapore, Asian Civilisations Museum, Fort Canning Park, Chinatown Heritage Centre, and Singapore River’s conservation shophouses — the highest concentration of arts, culture, and heritage within walking distance of any Singapore new launch.

In-Development Activation

Union Square Central’s Central Plaza will host food truck events, outdoor performances, community workouts, and placemaking activations — creating a vibrant, hotel-lobby-quality ground floor experience for residents every day.

Site Plan

Level 1 — Arrival plaza, Grand Stand, retail & F&B · Levels 3–29 — Recreational pods with swimming pools, gymnasium, and sky gardens · Level 40 — Penthouse residences · Indicative only

Residential storey key plans — 3rd to 40th storey unit distribution · indicative only · subject to developer confirmation

Floor Plans (Selected)

One representative plan per bedroom type. Download the full floor plans PDF for all stack-by-stack layouts, balcony dimensions, and AC ledge specifications.

1-Bedroom (Type A1) · 43 sqm / 463 sqft · Type A1(d) features 3.75 m ceiling height

Union Square Residences — Schematic chart · unit distribution across 40 storeys · indicative only · refer to developer’s official stack chart for confirmed positions

Facilities (30+)

Infinity PoolRecreational Pods (Levels 3–29)Sky GardensGymnasiumFunction RoomsCentral Plaza (Events)Grand StandConcierge ServicesCo-Working FacilitiesSmart Home SystemSmart Community Platform24-Hour SecurityCCTV SurveillanceEV ChargingBicycle BaysGrade A Office Tower (20-storey)Co-Living (3-storey)Conservation ShophousesGround Floor Retail & F&BRooftop RestaurantPneumatic Waste SystemBCA Green Mark Platinum SLE

Gallery

Developer and Consultant Team

City Developments Limited (CDL)

City Developments Limited is one of Singapore’s largest listed property developers, with a global portfolio spanning residential, commercial, hospitality, and industrial assets across 26 countries. SGX-listed since 1963, CDL has delivered more than 50,000 homes globally, with landmark Singapore residential projects including South Beach Residences, Boulevard 88, Canninghill Piers, The Sail @ Marina Bay, and One Shenton. For Union Square Residences, CDL is delivering a full mixed-use precinct — an ambition that reflects the company’s integrated development expertise accumulated across Marina Bay, Clarke Quay, and the CBD corridor over several decades.

Developer

City Developments Limited (CDL)

Mixed-Use Concept

Union Square Central — Residences + Grade A Office + Co-Living + Retail & F&B

Sustainability

BCA Green Mark Platinum Super Low Energy

Smart Systems

Smart home + smart community platform across all residential units

Location

Clarke Quay / Singapore River, District 01/02 (CCR)

Sustainability and Specifications

BCA Green Mark Platinum Super Low Energy: Union Square Residences has been awarded Singapore’s most demanding sustainability certification — Green Mark Platinum Super Low Energy (SLE). This designation requires demonstrable reductions in building energy intensity far beyond standard Green Mark requirements, translating directly to lower energy bills for residents and a future-proof environmental footprint.

Smart Home System: Every unit is equipped with a smart home platform covering access control, smart door locks, digital concierge, lighting management, and remote monitoring — accessible via smartphone from anywhere.

Smart Community Platform: Building-wide smart community systems covering visitor management, lift access control, smart security, and facility booking at common areas, basement, and lift lobbies.

EV Charging Infrastructure: Electric vehicle charging provisions in the basement carpark, supporting Singapore’s national EV rollout target.

Conservation Heritage Integration: The existing conservation shophouses within the Union Square precinct are retained and sensitively restored — reducing embodied carbon impact and preserving Singapore’s heritage built environment as a community asset.

Project Timeline

2023

Land Award & Licence

2024–2025

Sales Launch

2025–2027

Construction Phase

Est. 2028

TOP (Vacant Possession)

Est. 2031

Legal Completion

Project Factsheet

A shareable 2-page LovelyHomes factsheet — bring it to viewings, share with family.

Union Square Residences is located at Union Square, Clarke Quay / Singapore River, in Districts 01/02 (Core Central Region). The development is within walking distance of Clarke Quay MRT (NE5, North-East Line) and Raffles Place MRT (EW14/NS26, interchange). Fort Canning Park is immediately adjacent. Full address details are available in the project factsheet.

Who is the developer of Union Square Residences?

Union Square Residences is developed by City Developments Limited (CDL), one of Singapore’s largest listed property developers. CDL has been SGX-listed since 1963 and has delivered more than 50,000 homes globally, with past Singapore landmarks including South Beach Residences, Boulevard 88, Canninghill Piers, and The Sail @ Marina Bay.

What is the tenure of Union Square Residences?

Union Square Residences is a 99-year leasehold development. Full lease commencement date and remaining tenure details are available in the developer’s official project documentation.

How many residential units does Union Square Residences have?

Union Square Residences comprises 366 residential units across 40 storeys. Bedroom types range from 1-Bedroom (463 sqft) through to 3-Bedroom Premium (1,066 sqft), including 1-Bedroom + Study variants. A special Type A1(d) variant features a 3.75 m high ceiling at the living and dining area.

What is Union Square Central?

Union Square Central is the integrated mixed-use precinct within which Union Square Residences sits. It comprises: (1) the 40-storey residential tower with 366 homes; (2) a 20-storey premium Grade A office tower with retail and dining on the 1st storey and a rooftop restaurant; (3) a new co-living concept in a 3-storey building plus existing conservation shophouses; and (4) an activated Central Plaza with placemaking events including food trucks, performances, and community workouts. The precinct integrates new-build towers with heritage conservation buildings from Singapore’s colonial era.

What MRT stations are near Union Square Residences?

Union Square Residences is served by two major MRT stations within walking distance: Clarke Quay MRT (NE5, North-East Line) connects to Dhoby Ghaut, Little India, Serangoon, and Harbourfront; Raffles Place MRT (EW14/NS26, East-West/North-South interchange) connects to Marina Bay, Orchard, Jurong East, Changi Airport, and Tuas. The walking time to Raffles Place MRT is approximately 5–8 minutes.

Is Union Square Residences subject to ABSD?

Yes. Union Square Residences is a private residential development in the CCR and ABSD applies at prevailing rates. Singapore Citizens pay 0% on first property, 20% on second; Permanent Residents pay 5% on first, 30% on subsequent; foreigners pay 60%. See our complete ABSD guide.

Can foreigners buy Union Square Residences?

Yes. Union Square Residences is an unrestricted private residential condominium and is available to Singapore Citizens, PRs, foreigners, and corporate entities. Foreigners are subject to 60% ABSD as of 27 April 2023. See our foreigners’ property guide.

What sustainability features does Union Square Residences have?

Union Square Residences has been awarded BCA Green Mark Platinum Super Low Energy certification — Singapore’s highest sustainability standard for buildings. This requires significant reductions in building energy intensity. Additionally, the development features smart home management, smart community systems, EV charging infrastructure, and integrates the existing conservation shophouses to reduce embodied carbon.

What financing is available for Union Square Residences?

Buyers may take a bank loan of up to 75% LTV for a first property. The Total Debt Servicing Ratio (TDSR) cap of 55% applies. The progressive payment scheme means loan interest is only paid on drawn amounts — see our Progressive Payment guide and TDSR guide for details. CPF OA savings can be used subject to Withdrawal Limit rules.

Ready to see Union Square Residences in person?

Register your interest for a complimentary project briefing and showflat tour from our editorial team.

Where CCR mixed-use developments rank for gross yields — and why Clarke Quay commands above-average rents.

DISCLAIMER: All information on this page is compiled from publicly available sources and developer-issued marketing materials for informational purposes only. Prices, unit mix, specifications, and timelines are indicative and subject to change without notice. The floor plans shown are marked DRAFT by the developer and are for reference only. This page does not constitute an offer or solicitation to buy or sell any property. Buyers should conduct their own due diligence and seek advice from a licensed property consultant and legal counsel before any purchase decision. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

Rental yield is the single metric that separates a property bought to rent out from a property bought to live in. In Singapore in 2026, gross rental yields on residential property have settled into a tight 2.5%–5.0% band, with the upper end reserved for suburban three-bedroom condominiums and smaller one-bedroom units in fringe micro-markets. This guide explains exactly how rental yield is calculated, which Singapore districts are delivering 4%+ gross yields in 2026, and the unit-type and tenure trade-offs that determine whether your rental yield translates into meaningful net cash flow after costs, taxes, and leverage.

Figure 1: Gross rental yield is the headline, net yield is what pays the bills.

Quick Answer

Gross yield = annual rent ÷ purchase price × 100.

Singapore average (private condo, 2026): 3.5% gross.

Best yielding sub-markets: Woodlands, Jurong East, Sembawang, Tampines and selected OCR one-beds at 4.2%–4.8%.

Lowest yielding: CCR luxury freehold (Orchard, River Valley) at 2.2%–2.7%.

Net yield after costs is typically 30%–40% lower than gross — budget for maintenance, property tax, agent fees, income tax and vacancy.

Smaller units yield more: 1BR beats 3BR on gross yield by 60–120 bps.

HDB resale yield is not directly comparable — subletting rules apply (MOP, subletting-of-whole-flat rules).

How Rental Yield Works in Singapore

Rental yield has two forms: gross and net. Gross yield is simply the annual rent divided by the purchase price. Net yield deducts all the carrying costs — property tax, maintenance fees, agent commission, minor repairs, vacancy provision, income tax on rental income — and shows you the actual return before financing.

A condominium renting at S$4,500/month on a S$1.5M purchase looks like a 3.6% gross yield. But after you subtract property tax (S$3,600), maintenance (S$4,200), agent commission on a 2-year lease (S$4,500), minor repairs (S$2,000), 1-month annual vacancy provision (S$4,500) and income tax at 22% on taxable rent (approximately S$8,800) — you are looking at a net yield of 1.8%, roughly half the headline number. That is before interest on your mortgage, which would push a leveraged investor into negative cash flow territory unless rents outperform or rates fall.

Key takeaway

Always underwrite to net yield. Singapore investors frequently overestimate returns by anchoring on gross yield figures and ignoring 1.5–2.0 percentage points of carrying costs.

Singapore Rental Yield Map 2026 — By Region

Core Central Region (CCR)

The CCR — Districts 1, 2, 4, 9, 10, 11 and parts of 6 and 7 — is Singapore’s prestige market. It houses the bulk of freehold stock, luxury condominiums, and branded residences. CCR has the lowest gross yields of the three regions:

Sub-Market

Tenure

Gross Yield Range

Orchard / Tanglin (D10)

Freehold / 99-yr

2.3% – 2.8%

River Valley (D9)

Freehold / 99-yr

2.4% – 2.9%

Sentosa Cove (D4)

99-yr

2.2% – 2.6%

Newton / Novena (D11)

Freehold / 99-yr

2.8% – 3.3%

Tanjong Pagar CBD (D2)

Freehold / 99-yr

2.8% – 3.2%

Rest of Central Region (RCR)

The RCR — the districts ringing the CCR — has become Singapore’s sweet spot for balanced yield and capital growth:

Sub-Market

Tenure

Gross Yield Range

Queenstown / Alexandra (D3)

99-yr

3.2% – 3.8%

Science Park / Pasir Panjang (D5)

99-yr

3.0% – 3.6%

Toa Payoh / Bishan (D12 / D20)

99-yr

3.3% – 3.9%

Marine Parade / East Coast (D15)

Freehold / 99-yr

2.9% – 3.5%

Bukit Merah / HarbourFront (D4 fringe)

99-yr

3.1% – 3.7%

Outside Central Region (OCR)

OCR — the suburbs — delivers the highest gross yields in Singapore, driven by cheaper acquisition costs, stable suburban rents and high tenant demand from upgrading locals and middle-management expats:

Sub-Market

Tenure

Gross Yield Range

Woodlands (D25)

99-yr

4.2% – 4.8%

Jurong East (D22)

99-yr

4.0% – 4.6%

Tampines (D18)

99-yr

3.9% – 4.5%

Sembawang / Yishun (D27)

99-yr

4.1% – 4.7%

Punggol / Sengkang (D19)

99-yr

3.8% – 4.3%

Clementi / West Coast (D5 West)

99-yr

3.5% – 4.0%

Unit-Size Effect: Why One-Bedders Lead the League Table

Within any single sub-market, smaller units yield more — a consistent pattern across OCR, RCR and CCR. The reason is mechanical: rent per square foot falls more slowly than purchase price per square foot as units grow. A 500 sqft 1BR in Jurong East might transact at S$930 psf and rent at S$3.80 psf/month (4.9% gross). The same project’s 1,100 sqft 3BR trades at S$1,150 psf and rents at S$3.20 psf/month (3.3% gross).

Unit Type

Region

Gross Yield

1-Bedroom (500–550 sqft)

OCR

4.3% – 4.9%

2-Bedroom (700–750 sqft)

OCR

3.8% – 4.3%

3-Bedroom (950–1,050 sqft)

OCR

3.3% – 3.8%

4-Bedroom + (1,250 sqft+)

OCR

2.8% – 3.3%

1-Bedroom (500–550 sqft)

RCR

3.5% – 4.0%

3-Bedroom (950–1,050 sqft)

RCR

2.8% – 3.3%

The trade-off: 1-bed demand is narrower — single tenants, young couples without children, international postings — meaning vacancy risk is higher in a downturn. Our shoebox unit guide dives deeper into the investment case.

Worked Example: OCR 1-Bedroom vs CCR 2-Bedroom

Consider two investors each deploying S$1.2M of equity:

Metric

Investor A — OCR 1BR (Cash)

Investor B — CCR 2BR (Leveraged)

Purchase Price

S$1,200,000

S$2,400,000 (75% LTV ⇒ S$1.2M equity)

Location

D22 Jurong East, 1BR 517 sqft

D09 River Valley, 2BR 732 sqft

Monthly Rent

S$4,000

S$5,800

Gross Yield

4.0%

2.9%

Annual Property Tax (non-owner)

S$4,440

S$8,700

Annual Maintenance

S$4,200

S$4,800

Annual Insurance

S$600

S$800

Annual Agent Fees (avg)

S$2,000

S$2,900

Vacancy Provision (1 month)

S$4,000

S$5,800

Gross Rent p.a.

S$48,000

S$69,600

Net Rent p.a. (pre-tax, pre-interest)

S$32,760

S$46,600

Net Yield on Price

2.7%

1.9%

Mortgage Interest p.a. (4% on S$1.2M)

S$0 (cash buyer)

S$48,000

Pre-tax Net Cashflow

S$32,760

−S$1,400

Investor A’s unleveraged OCR 1-bed generates positive cash flow of S$32,760 a year. Investor B’s leveraged CCR 2-bed is marginally cash-flow negative — which is fine if the strategy is capital appreciation on freehold tenure, but devastating if the investor miscalculated TDSR headroom. Stress-test using our TDSR/MSR guide.

The Six Factors That Drive Singapore Rental Yield

1. Transport Connectivity

Walk-to-MRT (within 400m) commands a 5%–8% rent premium over non-MRT peers, but also a price premium — so net yield effect is marginal. However, developments that are MRT-adjacent with a line upgrade coming (e.g. Cross Island Line or Jurong Region Line stations) see yields compress post-opening as prices re-rate faster than rents.

2. School Proximity

Tenants with Primary 1 registration imperatives pay a premium for the 1km and 2km catchment zones of sought-after primary schools. This is a tenant-pool effect, not a rent-per-sqft effect — it reduces vacancy rather than raising headline rents.

3. Unit Size and Facing

North-south facing with unblocked views, high-floor > 20th storey, and natural cross-ventilation all contribute 3–8% rent premium. Low-floor pool-facing units can underperform by 5%+.

4. Tenure

Contrary to popular belief, freehold commands a price premium but not a rent premium — tenants do not pay more for freehold because they are not buying. This directly compresses freehold yields below 99-year leasehold yields for otherwise-equivalent stock.

5. Age of Development

New launches rent at a premium in year 1–3 post-TOP, tapering towards market norms by year 5. 10–20 year old developments trade at the stable mid-range. 30+ year old freeholds often underperform on rent (dated finishes) but beat on yield (low purchase price).

6. Macro Cycle

Rental growth in Singapore tracks non-resident inflows (EP/PR approvals, multinational relocations). Expect outperformance during policy easing and underperformance when ICA and MOM tighten approvals. Check MAS Financial Stability Review annually.

Yield vs Capital Growth: The Eternal Trade-off

Singapore investors historically face a stylised choice:

OCR 1BR: 4.5% gross yield, 3% capital growth p.a. ⇒ 7.5% total return.

CCR freehold 2BR: 2.5% gross yield, 6% capital growth p.a. ⇒ 8.5% total return.

CCR wins on total return, OCR wins on cashflow. If you need the property to service its own mortgage, choose yield. If you can fund the shortfall from employment income and are playing for long-term wealth preservation, capital growth wins.

Tax Treatment of Rental Income

Singapore residents (citizens and PRs) are taxed on rental income at their marginal rate (up to 24% in 2026), with deductible expenses. Non-residents are taxed at a flat 24% without expense deductions (unless they elect to be taxed as tax-residents subject to the 183-day rule). Deductible expenses include mortgage interest, property tax, fire insurance, repairs, agent commission, and in certain cases, a 15% deemed rental expense in lieu of itemised receipts.

Furnish strategically. A S$20,000 furnishing package typically boosts monthly rent by S$300–S$500 — payback in 4–6 years, not 10+.

Optimise vacancy. List at market, not above. Every month of vacancy is 8.3% of annual income lost.

Frequently Asked Questions

What is a good rental yield in Singapore?

Anything above 3.5% gross for a condominium in 2026 is above market average. Above 4.0% gross is considered strong. Above 4.5% is exceptional and usually limited to OCR shoebox units or distressed stock.

Why is my CCR condo’s yield so low?

CCR prices are elevated due to freehold tenure, land scarcity, and aspirational demand. Rents do not scale at the same rate as price because tenants are indifferent between freehold and 99-year leasehold for the same product. Result: headline yields of 2.3%–2.9% in prime Orchard, Tanglin, Sentosa.

Is HDB subletting a better yield play than condo rentals?

HDB subletting yields can be strong (3.5%–4.5%) but come with strict rules: minimum occupation period (5 years), subletting-of-whole-flat approvals, citizenship mix limits. See our HDB subletting guide.

What is a typical agent commission on a lease?

Standard market practice: 0.5 months’ rent for a 1-year lease, 1 month’s rent for a 2-year lease, 1.5 months for a 3-year lease, payable by the landlord.

Can I claim mortgage interest as a deductible expense?

Yes — mortgage interest on the rented property is deductible against rental income, as are property tax, fire insurance, repairs (not improvements) and agent commission.

How does the 15% deemed rental expense rule work?

IRAS allows landlords to claim 15% of gross rental as a deemed expense in lieu of itemised deductions, on top of mortgage interest and property tax. This simplifies tax filing for small landlords.

What is cash-on-cash return?

Net annual cashflow divided by total cash equity (downpayment + stamp duty + legal + furnishing). This is the number you actually experience in your bank account. Often divergent from net yield when leverage is high.

Can foreigners earn rental income in Singapore?

Yes — foreigners who own Singapore residential property can let it and earn rental income, subject to 24% non-resident tax rate.

Disclaimer: Rental yields are indicative and compiled from URA rental contract data, public transaction records, and market-survey estimates current at the time of writing. Individual yields vary by unit facing, floor, tenant profile and macro cycle. Nothing on this page is financial, tax, or investment advice — consult a qualified advisor before committing to a purchase.

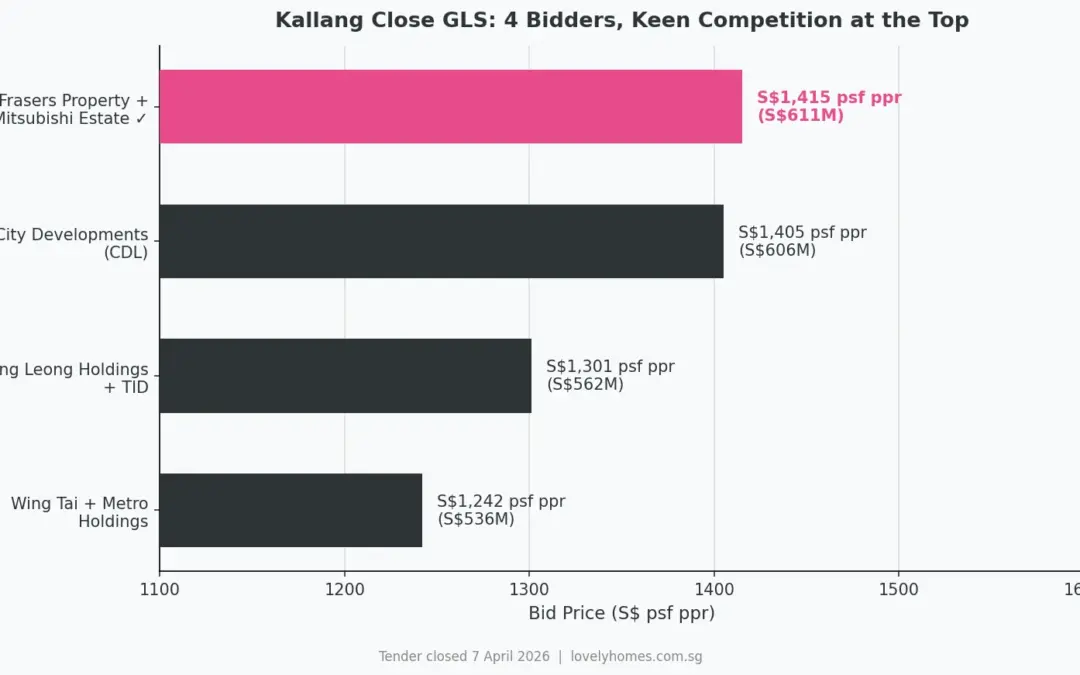

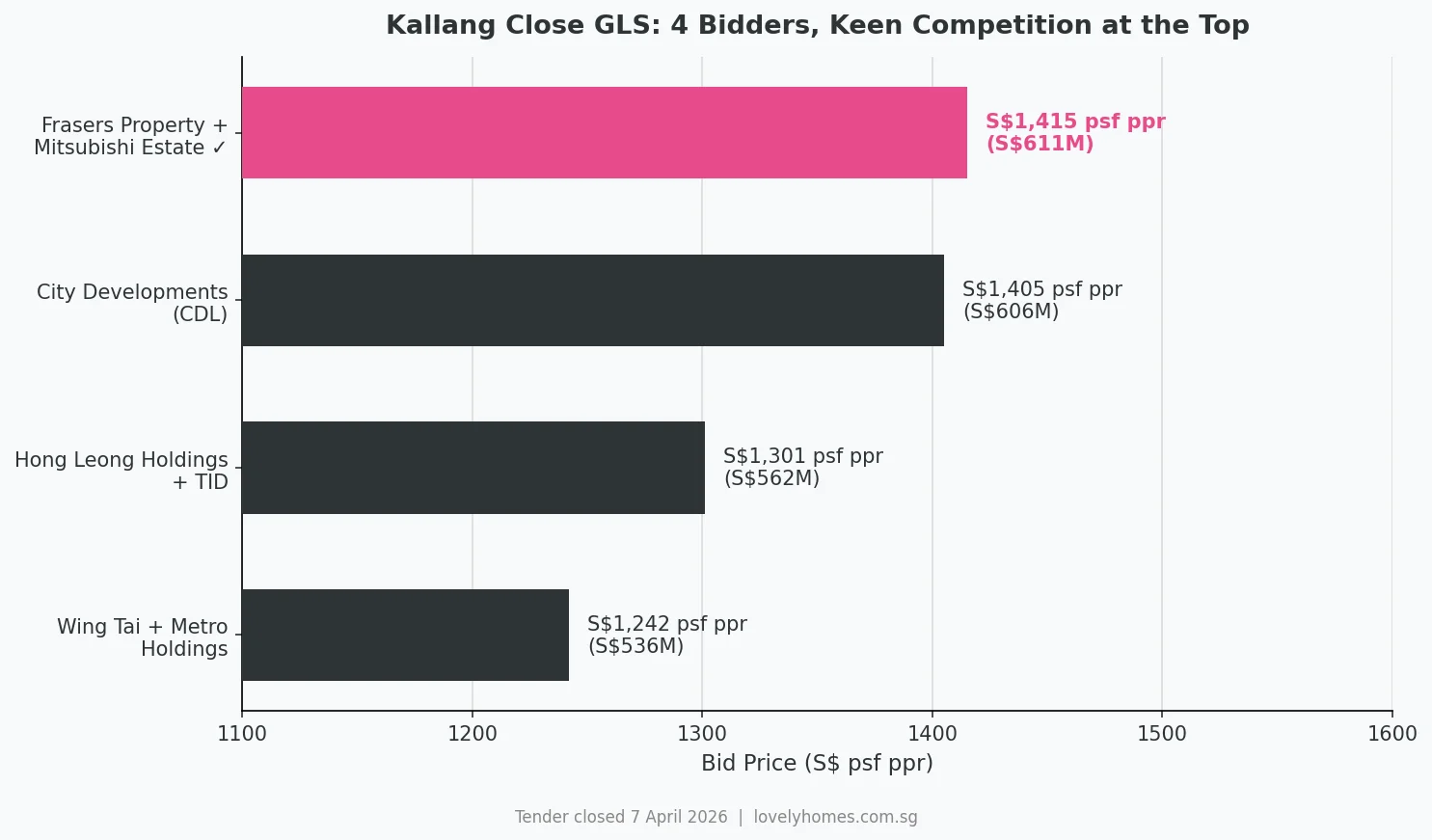

Quick Answer: The GLS tender for Kallang Close closed on 7 April 2026. A joint venture between Frasers Property and Mitsubishi Estate submitted the winning bid of S$610.75 million (S$1,415 psf ppr), the highest psf ppr for a city-fringe residential GLS site in recent years. The site can yield approximately 470 homes and will be the first private residential development in the Kallang Close industrial enclave in 12 years.

Horizontal bar chart comparing the four bids for the Kallang Close GLS site, with Frasers Property and Mitsubishi Estate’s winning bid of S$1,415 psf ppr.

The government land sale (GLS) tender for the Kallang Close residential site closed on 7 April 2026 with four bids — and a result that underscores sustained developer confidence in city-fringe locations, even amid a broader market that posted its lowest transaction volume since Q2 2020.

The winning consortium, a joint venture between Frasers Property Singapore and Mitsubishi Estate, submitted a bid of S$610.75 million (S$1,415 per square foot per plot ratio) — just S$4.35 million, or 0.7%, above second-placed City Developments Ltd. The paper-thin margin between first and second illustrates how keenly both bidders valued the site, and gives a clear signal of where institutional capital believes city-fringe launch prices can go.

Site Factsheet

Detail

Information

Address

Kallang Close, Singapore

District

D08 — Kallang / Whampoa

Site Area

Approximately 11,456 sq m (123,320 sq ft)

Plot Ratio

3.5

Maximum GFA

Approximately 40,107 sq m (431,611 sq ft)

Estimated Units

~470 private residential homes

Tenure

99-year leasehold (from date of award, Apr 2026)

Retail Component

Capped at 115 sq m GFA

Childcare Centre

Minimum 500 sq m GFA (mandatory)

Winning Bid

S$610.75 million (S$1,415 psf ppr)

Joint Venture

Frasers Property Singapore × Mitsubishi Estate

Tender Closed

7 April 2026

The Four Bids: Near-Record Competition

Rank

Bidder

Total Bid

S$ psf ppr

1st (Winner)

Frasers Property + Mitsubishi Estate

S$610.75M

S$1,415

2nd

City Developments Ltd (CDL)

S$606.40M

S$1,405

3rd

Hong Leong Holdings + TID JV

~S$561.5M

S$1,301

4th

Wing Tai Holdings + Metro Holdings

~S$536.4M

S$1,242

The 0.7% gap between the top two bids is one of the narrowest in recent Singapore GLS tender history. CDL — which co-developed Norwood Grand in Woodlands with Frasers Property — was effectively beaten by its own partner on a different site. The spread between first and fourth bidders was 13.9%, indicating that all four consortia saw real value in the Kallang Close waterfront location, but had genuinely different views on achievable launch pricing and margins.

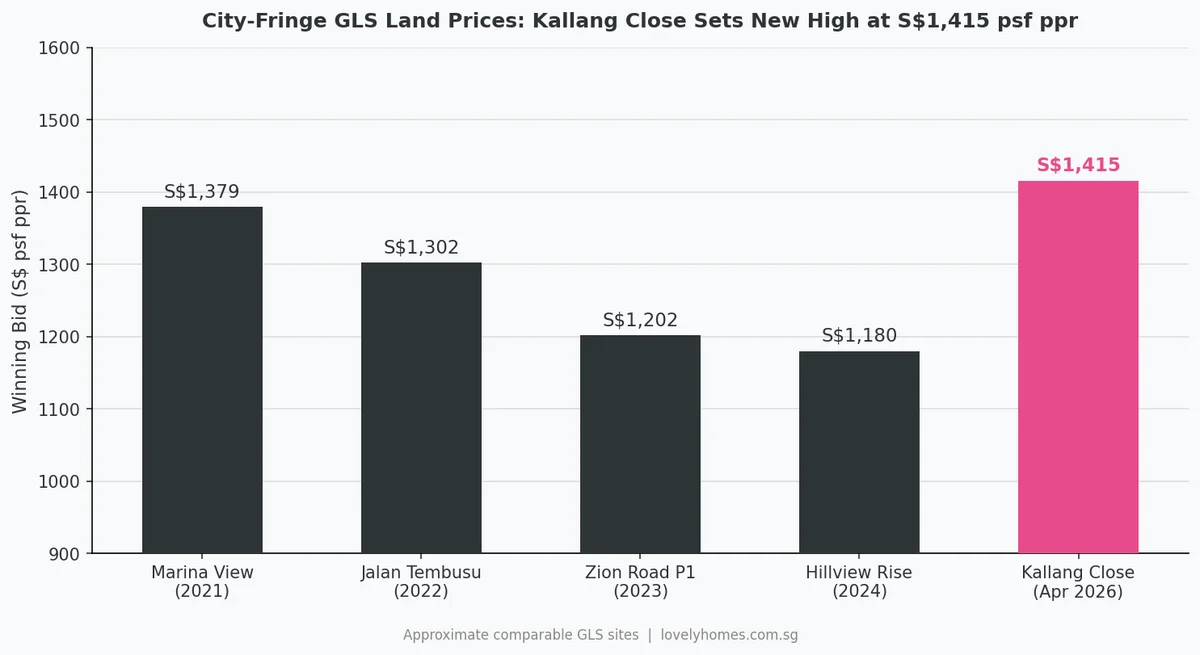

Why Kallang Close Commands a Premium

Bar chart comparing winning GLS bids for comparable city-fringe residential sites from 2021 to April 2026.

The site’s premium psf ppr reflects several structural advantages that are difficult to replicate in the GLS pipeline:

Kallang River waterfront frontage. The site sits adjacent to the Kallang River, and the consortium has committed to delivering a publicly accessible riverfront promenade. Waterfront residential sites are rare in Singapore’s land-scarce market; comparable waterfront addresses — Robertson Quay, Marina Bay, Harbourfront — consistently command significant price premiums.

First private homes in the precinct in 12 years. Kallang Close has been predominantly industrial. The last private residential development in the immediate vicinity launched over a decade ago. Buyers arriving at this project will be entering a precinct undergoing transformation, which historically has been a strong driver of early-adopter price appreciation.

Dual MRT accessibility. Kallang MRT (East-West Line) and Bendemeer MRT (Downtown Line) are both within walking distance, giving future residents cross-island connectivity without transfers.

Proximity to the city and Kallang planning transformation. The Kallang Area Master Plan envisions a sports and lifestyle precinct around the Singapore Sports Hub, Kallang Alive, and the future redevelopment of the National Stadium precinct. The broader area is also benefiting from the Geylang-to-Kallang urban renewal corridor.

Retail and childcare anchors. The mandatory childcare centre (minimum 500 sq m) and capped retail (115 sq m) will add day-to-day amenity value for residents without creating oversupply of commercial space.

What Will Launch Pricing Look Like?

At a land cost of S$1,415 psf ppr, industry analysts have modelled potential launch prices in the S$2,800–3,100 psf range, depending on:

Construction cost trajectory. Building costs in Singapore rose significantly in 2022–2024 and have moderated but remain elevated. A 99-year leasehold development on a 3.5 plot-ratio site with waterfront features and a childcare component will carry above-average construction costs.

Positioning relative to comparable launches. Recent city-fringe new launches — Robertson Opus (D09, ~S$3,150–3,360 psf), UPPERHOUSE (D10, ~S$3,350 psf) — provide a ceiling benchmark. Kallang Close, while waterfront, is in D08 which has historically priced at a modest discount to D09/D10.

Launch timing. The project is unlikely to launch before late 2027 or 2028, given the need for site clearing, design, and construction commencement. The market trajectory over the next 12–18 months will influence the eventual strategy.

A rough breakeven analysis, assuming a 20–22% developer margin over total project cost (land + construction + marketing), suggests a launch price of approximately S$2,900–3,100 psf is required for the project to pencil. Some analysts have modelled upside to S$3,300 psf if the waterfront premium commands a strong early take-up rate.

The Frasers × Mitsubishi Partnership

This is the first JV between Frasers Property Singapore and Mitsubishi Estate, Japan’s largest real estate company by market capitalisation. Frasers Property brings deep Singapore-market execution capability — it has developed One Canberra, Riverfront Residences, and North Park Residences, among others. Mitsubishi Estate brings global real estate expertise and balance sheet scale.

The partnership follows a trend of Japanese developers deepening their Singapore exposure: Sekisui House co-developed THE ORIE in Toa Payoh, MCL Land (a Jardine Matheson subsidiary with deep ties to the Japanese market) developed ELTA in Clementi alongside CSC Land. Japanese investors view Singapore freehold and 99-year leasehold assets as strategic long-term holdings with stable SGD returns.

What This Means for the Broader Market

The Kallang Close result has several read-throughs for Singapore property market observers:

Developer confidence in RCR/city-fringe pricing remains high. Despite Q1 2026 transaction volumes falling 39.7% QoQ, four major consortia competed vigorously for a single site. Developers are bidding for land they believe they can sell at S$2,900+ psf — a vote of confidence in demand fundamentals.

CDL’s near-miss is notable. CDL bid aggressively at S$1,405 psf ppr — its second near-miss in recent GLS tenders. The developer appears determined to rebuild its Singapore residential pipeline following a period of relative inactivity.

The GLS programme is working as a supply valve. The 1H 2026 GLS programme placed 9 sites on the Confirmed List. Kallang Close is the first to be awarded. The forthcoming sites at River Valley Green, Holland Plain, and Peck Hay Road will further test developer appetite in the CCR and RCR.

Waterfront as a permanent premium. Both the Frasers–Mitsubishi bid and CDL’s second-place bid exceeded S$1,400 psf ppr for a site with river frontage. This reinforces that waterfront views in Singapore command a structural premium that survives cooling measures and interest-rate cycles.

Timeline and What to Watch

Date / Period

Milestone

7 April 2026

GLS tender closed; Frasers × Mitsubishi named provisional winner

Q2/Q3 2026

URA formally awards site; conveyance and commencement of site works

Late 2026 – 2027

Architectural design, planning approval, showflat construction

2027 – 2028 (est.)

Showflat preview; public launch (subject to market conditions)

2030 – 2031 (est.)

Expected temporary occupation permit (TOP) based on 99-yr leasehold timeline

Frequently Asked Questions

Who won the Kallang Close GLS tender?

A joint venture between Frasers Property Singapore and Mitsubishi Estate, with a bid of S$610.75 million (S$1,415 psf ppr). The tender closed on 7 April 2026.

How many units will the Kallang Close development have?

Approximately 470 private residential homes, based on the site’s GFA of approximately 431,611 sq ft at a plot ratio of 3.5.

What is the expected launch price for the Kallang Close condo?

Industry analysts estimate a launch price in the range of S$2,900–3,100 psf, reflecting the land cost, construction expenses, waterfront premium, and comparable city-fringe launches. The project is unlikely to launch before late 2027 or 2028.

Is the Kallang Close site freehold or leasehold?

99-year leasehold, from the date of site award in April 2026.

Which MRT stations are near Kallang Close?

Kallang MRT Station (East-West Line) and Bendemeer MRT Station (Downtown Line) are both within walking distance of the Kallang Close site.

Why is this site significant?

It will be the first private residential development in the predominantly industrial Kallang Close precinct in approximately 12 years. The site has Kallang River waterfront frontage and sits within the broader Kallang Area Master Plan transformation zone, including the Kallang Alive sports and leisure precinct.

When will the Kallang Close condo be completed?

Based on typical construction timelines for a 99-year leasehold project of this scale, the estimated target for a Temporary Occupation Permit (TOP) is approximately 2030–2031. The official construction schedule will be confirmed after the site is formally awarded and planning approval obtained.

Interested in the Kallang Close launch? Register for early updates.

This article is for general informational purposes only and does not constitute financial or investment advice. Property prices are projections based on analyst estimates at the time of writing; actual launch prices will depend on market conditions at the time of launch. All figures cited are based on publicly available GLS tender results and URA data as at 20 April 2026. No marketing agency is named in connection with this development.

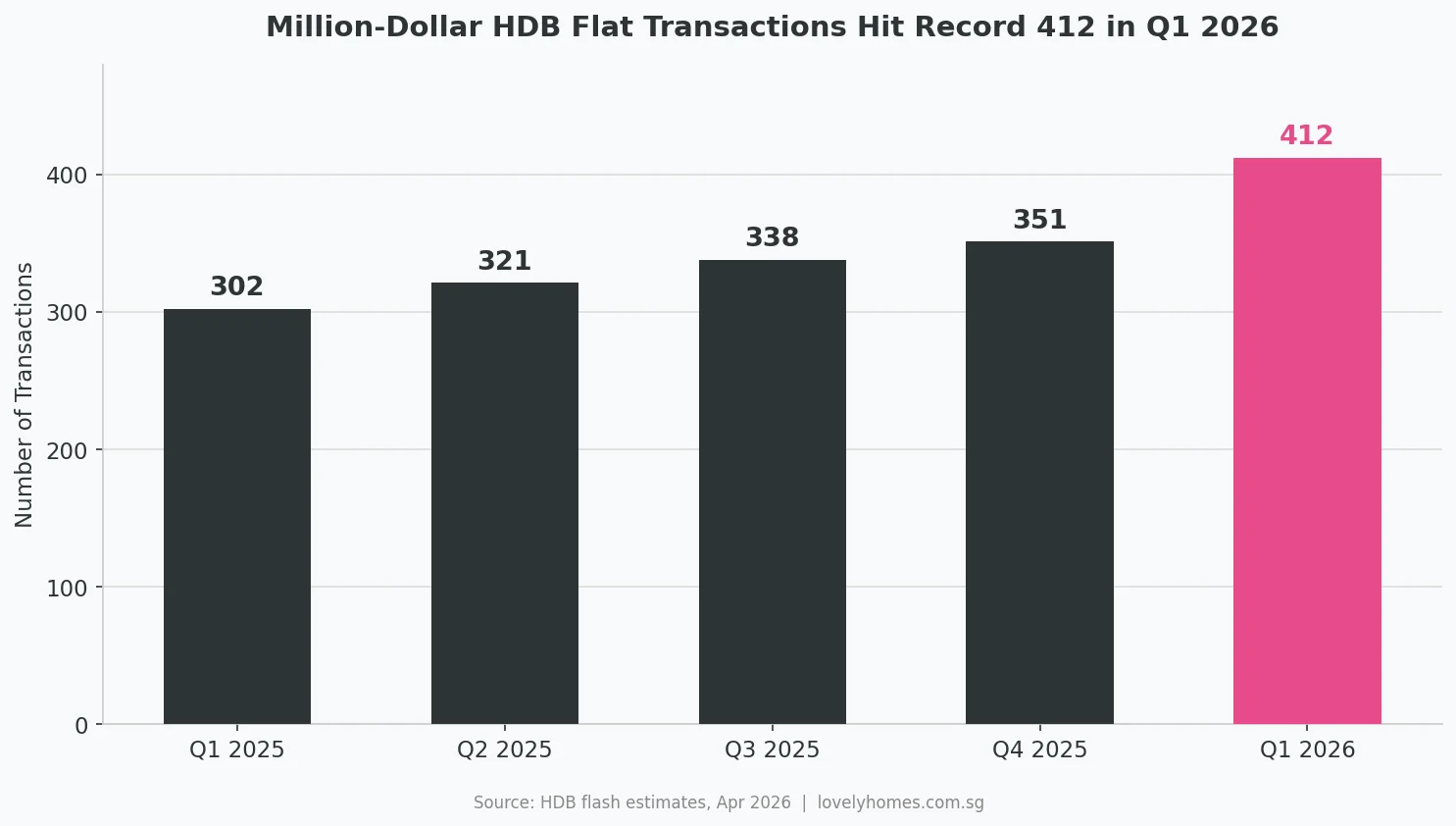

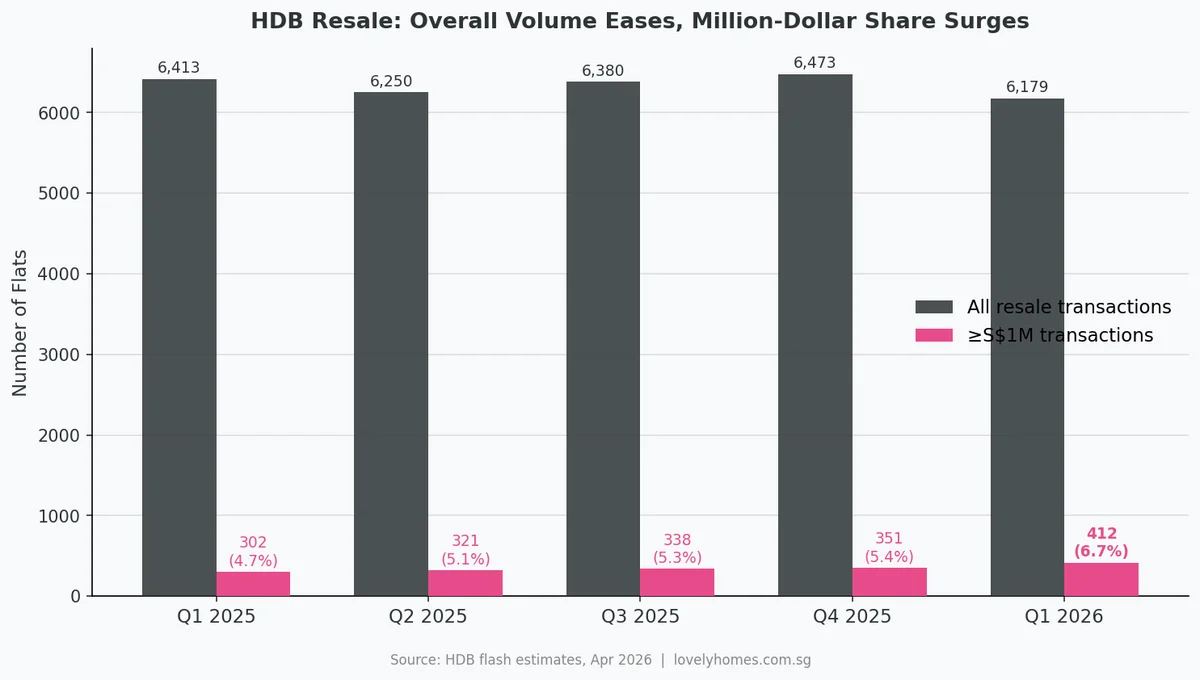

Quick Answer: In Q1 2026, HDB resale prices fell 0.1% — the first quarterly decline in seven years. Yet 412 flats changed hands at S$1 million or more, a new all-time quarterly record. The headline dip and the record premium sales are both real; they just reflect different segments of the same market.

Singapore’s HDB resale market delivered a headline that surprised many commentators on 1 April 2026: the Resale Price Index fell 0.1% quarter-on-quarter — the first decline since Q2 2019. In the same breath, the Housing and Development Board confirmed that 412 flats had sold for S$1 million or above in the same three months, eclipsing the prior record of 351 set in Q4 2025.

The juxtaposition is not a contradiction. It is a portrait of a two-speed resale market: broad price moderation driven by cooling-measure discipline, overlaid by an accelerating premium segment concentrated in a handful of mature estates.

The Numbers at a Glance

Metric

Q1 2026

Q4 2025

Change

HDB Resale Price Index (RPI)

203.4

203.6

−0.1% QoQ

Total resale transactions

6,179

6,473

−4.5% QoQ

Million-dollar transactions

412

351

+17.4% QoQ

Million-dollar share of total

6.7%

5.4%

+1.3 pp

S$1.7M all-time record

Dawson Rd 5-room (Feb 2026)

—

New benchmark

The overall RPI decline is technically modest — 0.1 percentage point — and should be understood in the context of seven consecutive quarters of price growth. Analysts at Knight Frank and JLL have characterised the dip as a “soft landing” rather than a structural correction, pointing to policy-driven affordability guardrails: the Mortgage Servicing Ratio (MSR) cap of 30%, Enhanced CPF Housing Grant (EHG) eligibility reviews, and the 15-month wait-out period for private downgraders.

Why Are Million-Dollar Transactions Still Rising?

Overall resale volume has eased while the share of million-dollar transactions has climbed steadily.

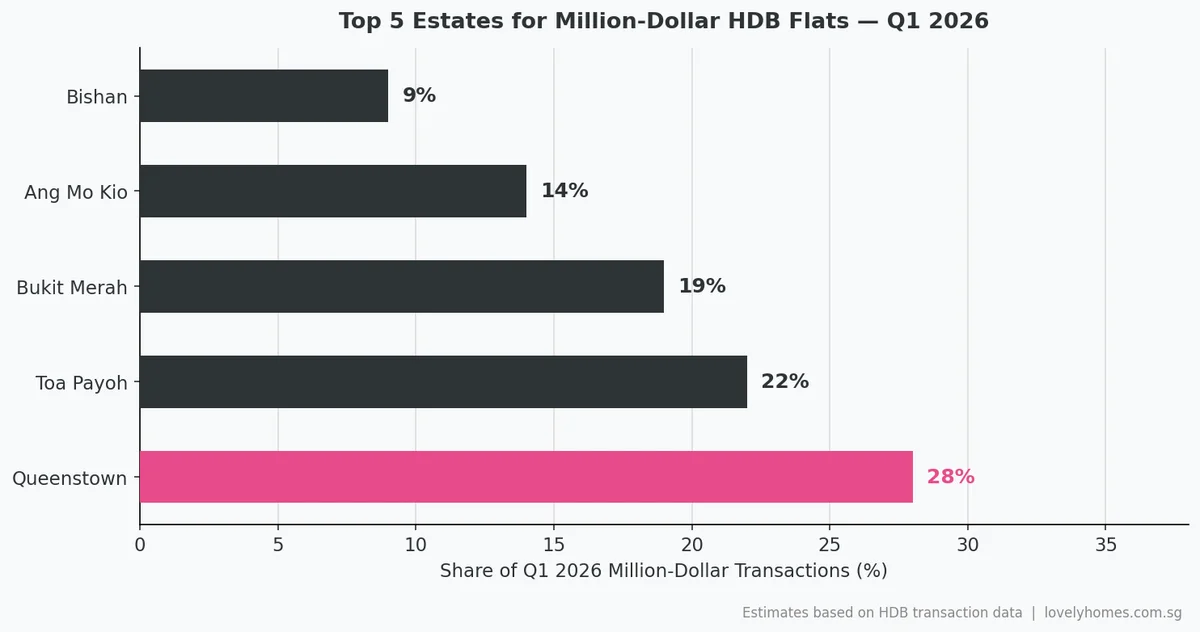

The premium segment operates on different fundamentals. Million-dollar HDB flats are almost entirely concentrated in a narrow band of mature estates — Queenstown, Toa Payoh, Bukit Merah, Ang Mo Kio and Bishan — where flat supply is structurally constrained, location premiums are well-established, and buyer profiles skew towards upgraders and cash-rich upsizers.

Several structural factors underpin the record:

Supply scarcity in mature estates. Large flats (5-room and executive) in central locations such as Queenstown and Toa Payoh are finite. As older owners pass on or move to assisted-living arrangements, each resale becomes a competition between multiple qualified buyers.

Private-market spillover. Buyers priced out of District 9–10 condos at S$2,500–3,500 psf are finding that a large, well-located HDB flat at S$1.0–1.4 million still represents value on a per-square-foot basis (often below S$900 psf).

The Dawson effect. The award-winning SkyParc @ Dawson and the broader Dawson precinct continue to set benchmarks. The S$1.7 million February 2026 transaction for a 5-room flat in Dawson Road is now the all-time national record for any HDB resale flat.

Diminished Alternative Housing Supply (DAHS) effect. New private condo launches fell ~60% QoQ in Q1 2026; with fewer new options, HDB upgraders are staying put or competing harder for premium resale flats.

The S$1.7 Million Record: Unpacking the Dawson Road Transaction

The record-setting flat is a 5-room unit along Dawson Road in Queenstown. At S$1.7 million, it surpasses the previous record of S$1.588 million set in 2023 and represents a premium of roughly 65–70% over the average 5-room flat price island-wide (approximately S$610,000–640,000). The buyer paid predominantly in cash above valuation, reflecting both the location’s scarcity value and the unit’s large floor area (approximately 113 square metres).

Queenstown holds a unique position: it was Singapore’s first public-housing satellite town, developed from the 1950s onwards, and retains some of the densest concentrations of MRT-accessible, well-maintained mature flats in the city. Its proximity to Alexandra, Buona Vista, and the upcoming Greater Southern Waterfront corridor ensures continued demand from professionals and dual-income households.

Top Estates Driving Million-Dollar Transactions

Queenstown, Toa Payoh, and Bukit Merah account for the majority of S$1M+ HDB resale flats in Q1 2026.

The concentration of premium transactions in five mature estates is a structural feature of the market, not a temporary anomaly. About 90% of million-dollar HDB transactions since 2021 have occurred in the core central and near-city estates, according to HDB transaction data. This geographic concentration has two implications:

Policy relevance: The data does not indicate broad HDB price inflation. The 90% of the market transacting below S$1 million is where the cooling measures are working as intended.

Buyer planning: Aspiring premium HDB buyers need to consider that million-dollar transactions in these estates are now the norm rather than the exception. Budget planning, CPF usage limits, and stamp duty calibration (BSD applies to HDB resale transactions too) are essential.

What the HDB Resale Price Dip Actually Means

The 0.1% dip in the RPI is historically significant — it is the first in 28 quarters — but it is marginal in absolute terms. It does not imply that HDB flat prices are about to fall sharply. Key counterpoints:

Volume decline, not distress: The 4.5% QoQ drop in transactions (6,179 vs 6,473) reflects seasonality and reduced new-flat completions, not seller distress or forced selling.

Full Q1 2026 data on 24 April 2026: URA and HDB will release complete Q1 2026 real estate statistics on 24 April 2026. The flash estimate (released 1 April) covers caveats lodged up to 30 March — the final data will capture some additional March transactions.

Policy signals are neutral: MAS and MND have not signalled any relaxation of cooling measures, nor any tightening. The market is operating within the intended guardrails.

June 2026 BTO exercise: HDB’s June 2026 sales exercise will offer approximately 6,900 flats across Ang Mo Kio, Bishan, Bukit Merah, Sembawang and Woodlands. Increased BTO supply provides an alternative for first-timers, which may further moderate resale volumes in the lower price bands.

Practical Implications for HDB Resale Buyers and Sellers

If you are buying a resale flat

The flat price dip provides a marginal negotiating advantage in the broad market, but this advantage does not extend to million-dollar premium flats in mature estates, where demand continues to outstrip supply. Buyers targeting Queenstown, Toa Payoh or Bukit Merah 5-room units should budget above S$1 million and ensure their CPF Ordinary Account balance and cash savings can cover cash-over-valuation (COV), which remains common in these sub-markets.

If you are selling a resale flat

Sellers in non-mature estates may find price expectations need modest recalibration, particularly for 3-room and smaller flats where supply from BTO completions is increasing. Sellers of large flats in prime mature estates remain in a strong position — Q1 2026 data confirms undiminished buyer appetite for well-located units.

If you are a private-property buyer watching the HDB market

The correlation between HDB premium prices and private OCR/RCR condo prices is real but lagged. The current HDB resale dip has not yet translated into private price weakness — private non-landed prices rose 0.4% QoQ in Q1 2026. Monitoring both indices over Q2 2026 will be instructive.

Frequently Asked Questions

How many HDB flats sold for S$1 million or more in Q1 2026?

412 flats, the highest quarterly total on record. This is up 17.4% from the previous quarter’s 351 transactions.

What is the most expensive HDB flat ever sold?

As of Q1 2026, a 5-room flat along Dawson Road in Queenstown that sold for S$1.7 million in February 2026. This surpassed the prior record and set a new national benchmark across all flat types.

Did HDB resale prices fall in Q1 2026?

Yes. The Resale Price Index (RPI) declined 0.1% quarter-on-quarter in Q1 2026, the first quarterly fall since Q2 2019 (seven years). The full Q1 2026 HDB data is scheduled for release by HDB on 24 April 2026.

Why are million-dollar HDB transactions rising even as prices dip?

The overall price dip reflects broad market moderation in non-mature estates and smaller flat types, while the million-dollar segment is driven by structurally scarce supply in mature estates such as Queenstown and Toa Payoh. The two trends coexist because they serve different buyer segments.

Which HDB estates have the most million-dollar transactions?

Queenstown, Toa Payoh, Bukit Merah, Ang Mo Kio, and Bishan account for the vast majority of million-dollar HDB resale transactions. Approximately 90% of all such transactions are in mature, centrally-located estates.

Are HDB cooling measures being relaxed?

No. As of April 2026, there has been no policy signal from MAS, MND or HDB indicating any relaxation of the Mortgage Servicing Ratio (MSR) cap, Additional Buyer’s Stamp Duty (ABSD) rates, or loan-to-value (LTV) limits applicable to HDB resale purchases.

How does the HDB price dip affect private property?

Private non-landed residential prices rose 0.3% QoQ in Q1 2026 despite the HDB dip, representing a divergence between the two markets for the first time since Q2 2019. Analysts regard this as a soft-landing scenario rather than a leading indicator of private price weakness.

Have questions about HDB resale prices or upgrading strategy?

This article is for general informational purposes only and does not constitute financial, legal or property advice. Property prices and market conditions change; readers should conduct their own due diligence or consult a licensed property professional before making any investment decision. All figures cited are based on HDB and URA flash estimates for Q1 2026 released 1 April 2026; full statistics will be published 24 April 2026.