Singapore home loans are now primarily benchmarked to SORA (Singapore Overnight Rate Average) — the official replacement for SIBOR, which was phased out in December 2024.

As at May 2026, the 3-month compounded SORA is approximately 2.55%, down from its 2023 peak of above 3.7%.

Major banks offer two main packages: SORA-pegged floating rates (typically SORA + 0.85–0.90%) and fixed rates (typically 2.45–2.65% for a 2-year fixed term).

The HDB Concessionary Loan is pegged at CPF OA + 0.1%, currently 2.60%; it is available only for HDB flats and requires no lock-in period.

The Total Debt Servicing Ratio (TDSR) cap of 55% and Mortgage Servicing Ratio (MSR) cap of 30% remain in force and directly limit how much you can borrow.

Fixed rates offer payment certainty but come with a lock-in penalty (typically 1.5% of outstanding loan) if you refinance early.

SORA-pegged loans offer transparency and flexibility, but your repayment will move with rates — currently favourable as SORA trends down from its 2023 highs.

Understanding Singapore Home Loan Interest Rates in 2026

When you take out a home loan in Singapore, the single most consequential variable is the interest rate. On a S$1 million loan over 25 years, the difference between a 2.45% and a 3.40% rate translates to roughly S$470 more per month — or over S$140,000 in additional interest over the life of the loan. Yet many buyers in Singapore choose their home loan based on convenience, the advice of a mortgage broker with a vested interest, or simply whatever their bank’s relationship manager recommends at point of sale.

This guide explains how Singapore home loan interest rates are structured in 2026, what SORA is and why it replaced SIBOR and SOR, how to read bank package offers correctly, and how to decide between a floating rate and a fixed rate package given the current interest rate environment. It is written for Singaporean and Permanent Resident property buyers — the same principles apply to foreigners but their ABSD liability fundamentally alters the financing calculus.

Monetary Authority of Singapore (MAS) regulates home lending in Singapore under the Monetary Authority of Singapore Act and the Notice MAS 632 on Residential Property Loans. HDB administers the Concessionary Loan under the Housing and Development Act.

Figure 1: SORA 3-Month Compounded Average vs 2-year Fixed Rate — Major Singapore Banks, 2020–2026. Data: MAS, bank publications.

What Is SORA and Why Did It Replace SIBOR?

SORA — the Singapore Overnight Rate Average — is the volume-weighted average rate of all overnight unsecured Singapore dollar interbank transactions brokered in Singapore between 08:00 and 18:15 each business day. It is published daily by MAS and is calculated retrospectively, which makes it a backward-looking, transaction-based benchmark rather than a quote-based one like SIBOR was.

SIBOR (Singapore Interbank Offered Rate) was phased out on 31 December 2024 following a global reform of interest rate benchmarks prompted by the 2012 LIBOR manipulation scandal. SOR (Swap Offer Rate), which was partly based on USD LIBOR, was discontinued even earlier. MAS and the Steering Committee for SOR & SIBOR Transition to SORA (SC-STS) oversaw the transition, which required all existing SIBOR-pegged mortgages to be converted to SORA-linked packages by end-2024.

SORA is now used in three primary forms for home loans:

1-Month Compounded SORA (1M SORA) — reflects the past 30 days of overnight rates. More reactive to short-term rate changes.

3-Month Compounded SORA (3M SORA) — reflects the past 90 days. More commonly used by banks for home loans; provides a slightly smoother signal.

SORA Board Rates — some banks (notably UOB) have internal board rates that are partially informed by SORA movements but give the bank more discretion over repricing.

SORA-Pegged Floating Rate Packages

A SORA-pegged floating rate package ties your home loan to the prevailing 3M Compounded SORA, plus a fixed spread set by the bank. As at May 2026, spreads across major banks range from +0.85% to +0.90%:

DBS: 3M Compounded SORA + 0.85%

OCBC: 3M Compounded SORA + 0.88%

UOB: 3M Compounded SORA + 0.90%

Maybank: 3M Compounded SORA + 0.85%

With 3M SORA at approximately 2.55% in May 2026, an all-in floating rate works out to roughly 3.40–3.45%. This is broadly similar to the prevailing 2-year fixed rate, which sits at 2.45–2.65% for Year 1–2 before typically reverting to a board rate or SORA-linked rate from Year 3.

The key characteristics of a SORA floating package are:

No lock-in period — you can refinance or reprice at any time without a penalty clause.

Transparent repricing — your rate changes as SORA moves, typically with a 1-month lag for 1M SORA packages or a 3-month lag for 3M packages.

Currently in a declining environment — if MAS and the Federal Reserve continue rate normalisation through 2026, SORA is expected to drift toward 2.2–2.4% by end-2026, which would bring all-in floating rates to around 3.05–3.30%.

Figure 2: Singapore Home Loan Package Comparison — DBS, OCBC, UOB, HDB Concessionary Loan and others, May 2026. Rates indicative; verify with lender.

Fixed Rate Packages

Fixed rate packages lock in an interest rate for a specified period — typically 2 years — after which the loan reverts to a floating rate, usually SORA-linked or a bank board rate. As at May 2026, major banks are offering:

Bank

Year 1

Year 2

Year 3+

Lock-in

DBS

2.45%

2.55%

FHR8 (board rate)

2 years

OCBC

2.50%

2.60%

OHR+ (SORA-linked)

2 years

UOB

2.45%

2.55%

SORA + spread

2 years

Standard Chartered

2.48%

2.60%

Board rate

2 years

Maybank

2.50%

2.65%

SORA + spread

2 years

The 2-year fixed period provides payment certainty — you know exactly what you will pay every month for the fixed term, which makes household budgeting straightforward. The risk is that if you need to refinance during the lock-in window — for example, because you sell the property, or a better package becomes available — you will typically pay a penalty of 1.50% of the outstanding loan amount at the time of early redemption.

On a S$1 million loan, that penalty is S$15,000. This is not an insignificant sum, and it is the primary reason experienced property investors often prefer no-lock-in floating packages despite the slightly higher all-in rate today.

The HDB Concessionary Loan — A Third Option

Buyers purchasing an HDB flat have access to a third option: the HDB Concessionary Loan, currently at a flat 2.60% per annum. This rate is set at CPF Ordinary Account interest rate (currently 2.5%) plus 0.1%, and is reviewed quarterly. It has remained at 2.60% since January 2023 when the CPF OA rate was last adjusted.

The HDB Concessionary Loan is notable for several reasons:

No lock-in — you can switch to a bank loan at any time without penalty.

LTV up to 80% — the maximum Loan-to-Value for an HDB loan is 80% of the purchase price or valuation (whichever is lower), versus 75% for a bank loan.

No cash down payment requirement — the 20% down payment can be funded entirely from CPF Ordinary Account (unlike bank loans, which require at least 5% in cash).

Eligibility conditions — all owners must not own any other residential property; income ceiling of S$14,000 household income applies for most flat types (no ceiling for HDB resale). You must obtain an HDB Flat Eligibility (HFE) Letter before exercising an OTP.

TDSR and MSR — How Much Can You Borrow?

MAS introduced the Total Debt Servicing Ratio (TDSR) framework in June 2013 to ensure borrowers do not over-leverage. TDSR limits total monthly debt obligations (including the new mortgage, car loans, personal loans, credit card minimum payments and all other credit facilities) to 55% of gross monthly income. Banks apply a stress-test rate of 4.0% per annum when assessing TDSR — meaning they calculate your hypothetical monthly payment at 4.0% regardless of the prevailing rate, to ensure you can afford the loan even if rates rise.

For HDB flat purchases (both BTO and resale), the additional Mortgage Servicing Ratio (MSR) cap applies: your monthly mortgage payment must not exceed 30% of gross monthly income. MSR applies to the actual servicing payment, not a stress-tested figure.

These rules mean that on a gross household income of S$10,000 per month, the maximum monthly mortgage payment you can qualify for (under MSR for HDB) is S$3,000; and the maximum all-debt obligation under TDSR is S$5,500. Practically, if you have a car loan of S$800/month, your maximum mortgage under TDSR is reduced to S$4,700/month.

Figure 3: Monthly Repayment by Rate Scenario — S$1M Loan, 25-Year Tenure. Illustrative; based on standard annuity formula.

Worked Example — The Tan Family’s Loan Decision

Mr and Mrs Tan are Singapore Citizens purchasing a S$1.4 million OCR condominium in Tampines in June 2026. They are first-time buyers with no outstanding home loans. Their gross combined household income is S$14,000 per month. They have S$180,000 in CPF OA (combined) and S$100,000 in cash savings.

Loan quantum: 75% LTV on S$1.4M = S$1.05M bank loan. Down payment = S$350,000 (25%), of which at least S$70,000 (5%) must be in cash. The Tans comfortably clear this with S$70,000 cash + S$280,000 CPF.

BSD: S$24,600 on S$1.4M (first S$180k at 1%, next S$180k at 2%, next S$640k at 3%, remaining S$400k at 4% — total S$1,800 + S$3,600 + S$19,200 = wait, let me compute correctly: BSD on S$1.4M = 1%×S$180k + 2%×S$180k + 3%×S$640k + 4%×S$400k = S$1,800 + S$3,600 + S$19,200 + S$16,000 = S$40,600). ABSD: S$0 (first purchase, SC).

Rate comparison:

Option A — 2-year fixed at 2.45%/2.55%: Monthly in Year 1 = S$4,634; Year 2 = S$4,706. Reverts to SORA + spread from Year 3 (est. ~S$4,500–4,800 depending on SORA trajectory). Lock-in penalty if exit before 24 months: ~S$15,750 (1.5% × S$1.05M).

Option B — SORA float at SORA+0.85% ≈ 3.40%: Monthly = ~S$5,161. No lock-in. If SORA falls to 2.2% by end-2026, rate drops to ~3.05%, monthly ~S$4,956.

Option C — If they were buying an HDB resale (for illustration): HDB Concessionary Loan at 2.60% → monthly ~S$4,748 on S$1.05M, 80% LTV available.

TDSR check (Option A, Year 1): Monthly payment S$4,634. With no other debts, TDSR = S$4,634 ÷ S$14,000 = 33.1%. Well within 55%. Stress-tested at 4.0%: hypothetical monthly = S$5,534; TDSR = 39.5%. PASS.

Recommendation: Given the declining SORA environment in 2026, the Tans opt for Option A (2-year fixed) to lock in payment certainty during the early years of ownership when their cash position is most stretched. They set a calendar reminder to review and refinance in Month 20, before the lock-in expiry.

Fixed vs Floating — How to Decide in 2026

With fixed and floating rates now converging at around 3.35–3.50% all-in, the classic argument — “floating is cheaper, fixed is certain” — no longer cleanly applies. The decision framework for 2026 hinges on three questions:

How long will you hold the property? If you plan to sell within 3 years (e.g., you are buying a resale flat as a stepping stone and expect to MOP a BTO), a floating package with no lock-in avoids the exit penalty. If you plan to hold for 10+ years, the 2-year fixed-then-float cycle is largely a moot point — both packages will track the same rates over the long run.

How sensitive is your monthly budget to rate moves? If a S$300–500 increase in monthly repayment would significantly stress your household, a fixed rate gives you a planning buffer. If you have comfortable headroom under TDSR, floating is fine.

What is the SORA outlook? As at May 2026, MAS and market consensus lean toward SORA continuing a gradual decline through 2026–2027 as the global rate cycle normalises. In a declining rate environment, locking in at today’s fixed rate means you may pay slightly more than the eventual SORA level. However, the gap is likely to be narrow (0.10–0.30%) and the certainty premium may be worth it for first-time buyers.

What Might Come Next — Singapore Loan Rate Outlook

Several factors will shape Singapore home loan rates through end-2026 and into 2027. MAS operates a unique monetary policy framework — it manages the Singapore dollar nominal effective exchange rate (S$NEER) rather than directly setting an overnight rate, meaning SORA is market-determined rather than policy-set. However, SORA is strongly correlated to the US federal funds rate through Singapore’s open capital account.

The US Federal Reserve has signalled two 25-basis-point cuts in the second half of 2026, which, if executed, would likely push 3M SORA from ~2.55% toward ~2.05–2.15% by year-end. This would bring SORA-pegged all-in rates to around 2.90–3.05% — meaningfully below today’s fixed rates of 2.45–2.65% over a 2-year view. Whether banks adjust their fixed rate offerings in anticipation remains to be seen; historically, fixed rates tend to reprice down with a 1–2 quarter lag.

Summary — Home Loan Rate Comparison at a Glance

Feature

SORA Float

Fixed Rate (2yr)

HDB Concess.

All-in Rate (May 2026)

~3.40%

2.45–2.65%

2.60%

Rate Certainty

None

2 years

Stable (CPF+0.1%)

Lock-in Period

None

2 years

None

Exit Penalty

None

~1.5% of loan

None

Max LTV

75%

75%

80%

Min Cash Down

5%

5%

0% (CPF ok)

Eligible Properties

All

All

HDB only

Best For

Flexible holders; declining rate bet

First-timers; budget certainty

HDB buyers; tight cash

Frequently Asked Questions

What is SORA and how is it different from SIBOR?

SORA (Singapore Overnight Rate Average) is the volume-weighted average of unsecured overnight interbank SGD transactions, published daily by MAS. SIBOR was a forward-looking rate based on bank submissions — susceptible to manipulation, as the 2012 LIBOR scandal revealed globally. SORA is transaction-based and backward-looking, making it more robust and harder to manipulate. SIBOR was fully discontinued on 31 December 2024; all SIBOR-pegged mortgages were converted to SORA or fixed-rate packages during 2023–2024.

Should I choose a fixed or floating rate home loan in 2026?

With SORA declining toward 2.2% by end-2026 and fixed rates at 2.45–2.65%, the all-in rates are converging. For first-time buyers who need budgeting certainty, a 2-year fixed rate is sensible — it protects against any short-term rate surprise and costs only marginally more than today’s floating all-in rate. For investors and experienced buyers who plan to hold long-term or who may sell within 3 years, a no-lock-in SORA floating package avoids exit penalties and will benefit as SORA falls further. In 2026 specifically, the edge is modest either way; the bigger decision is the property itself.

What is the current SORA rate in 2026?

As at May 2026, the 3-month compounded SORA is approximately 2.55% per annum, down from its peak of above 3.74% in mid-2023. It has been declining steadily as the US Federal Reserve began its rate normalisation cycle in late 2024. MAS publishes daily SORA rates on its website at mas.gov.sg/monetary-policy/sora.

What is TDSR and how does it affect how much I can borrow?

The Total Debt Servicing Ratio (TDSR) limits your total monthly debt obligations (including the home loan, car loans, personal loans and other credit facilities) to 55% of your gross monthly income. Banks stress-test your loan at 4.0% per annum when assessing TDSR eligibility — so even if the prevailing rate is 3.0%, the bank calculates whether you could afford the repayment at 4.0%. On top of TDSR, if you are buying an HDB flat, the Mortgage Servicing Ratio (MSR) limits your monthly home loan repayment to 30% of gross monthly income.

Can I use CPF to pay my home loan?

Yes. CPF Ordinary Account savings can be used to service monthly home loan repayments for both HDB flats and private properties, subject to the Valuation Limit (generally the lower of the purchase price or valuation) and the Withdrawal Limit (up to 120% of the Valuation Limit for private properties). Note that CPF monies withdrawn for property earn accrued interest at 2.5% per annum, which must be returned to your CPF account upon sale. This accrued interest does not represent an additional out-of-pocket cost but reduces the net cash proceeds you receive when you sell.

What is a lock-in period and what happens if I break it?

A lock-in period is a contractual commitment to maintain your loan with the same bank for a set duration — typically 2 years for fixed rate packages. If you refinance, prepay or redeem the loan in full before the lock-in expires, you pay a penalty usually equal to 1.5% of the outstanding loan amount at the time of early redemption. On a S$900,000 outstanding balance, that is S$13,500. No-lock-in packages (all SORA floating packages and HDB Concessionary Loans) allow you to exit or refinance at any time without penalty.

What is the difference between refinancing and repricing?

Repricing is when you switch to a different loan package within the same bank — typically cheaper (no legal or valuation fees) but limited to that bank’s available packages. Refinancing is when you move your loan to a different bank entirely. Refinancing typically offers access to sharper rates but incurs legal fees (S$2,000–3,500), valuation fees (S$300–800), and potentially a clawback of cashback incentives if you refinance within the clawback period (usually 3 years). Both options are typically considered when a fixed rate lock-in expires.

This article is for general informational purposes only and does not constitute financial or legal advice. Interest rates quoted are indicative as at May 2026 and are subject to change by individual lenders. The SORA rate is published daily by MAS and can be found at mas.gov.sg. TDSR and MSR rules are set by MAS and are subject to regulatory revision. For personalised advice on home loan selection and eligibility, consult a licensed financial adviser or mortgage specialist regulated by MAS. All stamp duty computations are based on IRAS published rates at iras.gov.sg. HDB Concessionary Loan eligibility criteria are set by HDB and available at hdb.gov.sg. CPF rules on property usage are administered by the CPF Board at cpf.gov.sg.

Foreigners (non-PR, non-SC) may purchase private residential property — condominiums, apartments, strata-titled units — in Singapore without restriction, subject to a 60% Additional Buyer’s Stamp Duty (ABSD) payable to IRAS.

Foreigners cannot buy HDB flats (resale or BTO) and cannot buy landed residential property (houses, semi-detached, bungalows) without prior approval from the Singapore Land Authority (SLA), which is rarely granted.

Executive Condominiums (ECs) become available to foreigners only after privatisation. For ECs from GLS sites tendered from 8 May 2026 onwards, privatisation occurs at 15 years from TOP; earlier ECs remain at 10 years.

The 60% ABSD applies to the entire purchase price and must be paid within 14 days of exercising the Option to Purchase (OTP).

Buyer’s Stamp Duty (BSD) is payable by all buyers regardless of nationality. On a S$2.5M purchase, BSD is approximately S$94,600.

Foreigners can obtain a mortgage from Singapore-licensed banks. LTV limit is 75% for a first property loan with no existing housing loans, subject to Total Debt Servicing Ratio (TDSR) of 55%.

Commercial and industrial property carries no ABSD — foreigners may purchase shophouses, office units, factories, and warehouses without the 60% surcharge.

Nationals of the USA, Iceland, Liechtenstein, Norway, and Switzerland are exempt from ABSD on their first residential purchase under Free Trade Agreement commitments.

What Is the ABSD and Who Administers It?

The Additional Buyer’s Stamp Duty (ABSD) is a surcharge levied by the Inland Revenue Authority of Singapore (IRAS) on the purchase or acquisition of residential property in Singapore, on top of the standard Buyer’s Stamp Duty (BSD). Introduced in December 2011 as a demand-side cooling measure, the ABSD has been adjusted multiple times. The most significant recent change for foreigners was on 27 April 2023, when the rate was doubled from 30% to 60%.

The policy objective is explicit: ABSD prioritises home ownership for Singaporeans and ensures that property remains affordable for residents. Non-resident buyers must bear a substantial additional cost — and this is intentional. Singapore’s Ministry of National Development has consistently maintained that residential property is primarily for citizens, and the 60% rate is designed to reflect that priority firmly.

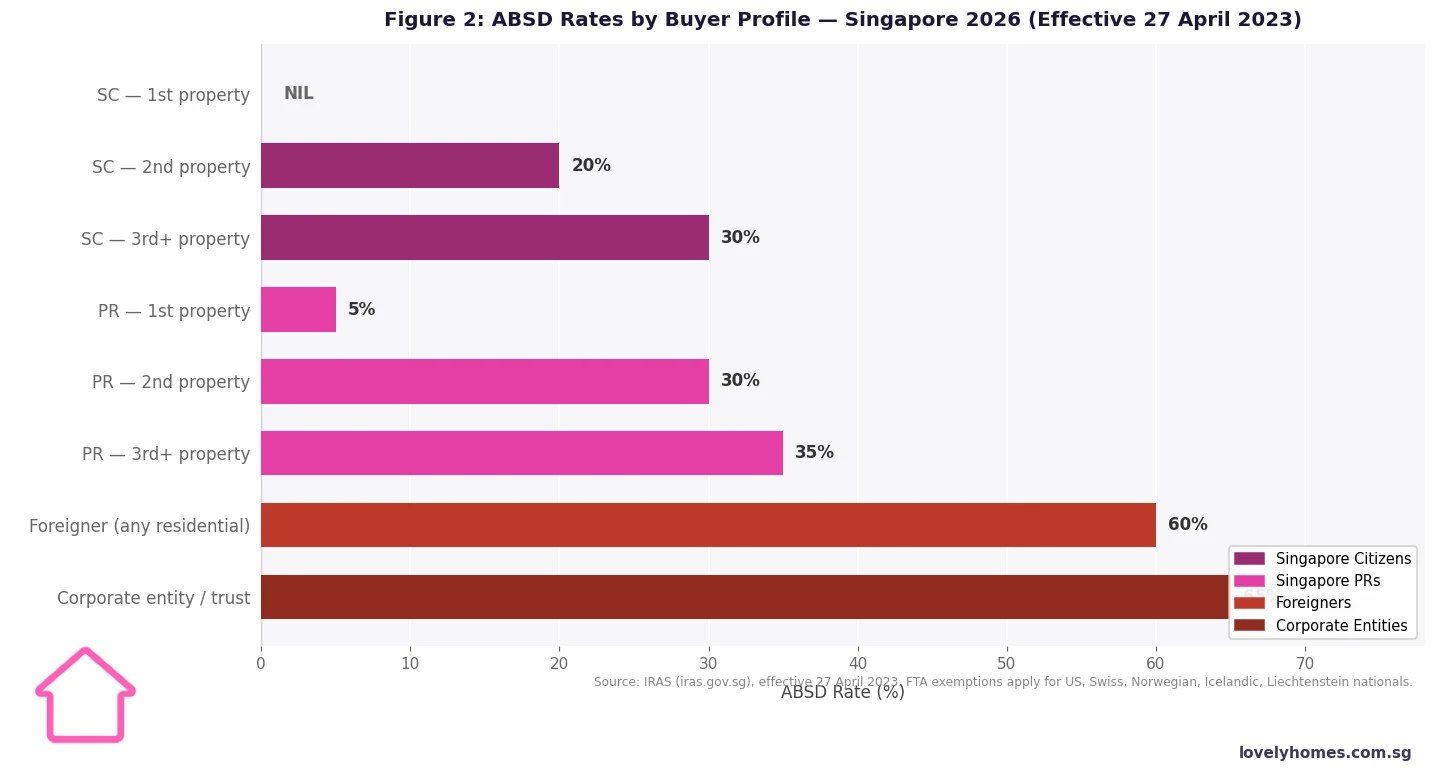

Figure 1: Property Eligibility by Buyer Type — Singapore 2026 | Source: HDB, URA, SLA, IRAS

ABSD Rates by Buyer Profile (Effective 27 April 2023)

ABSD is charged on the higher of the purchase price or the property’s market value. The table below shows the current rates, administered by IRAS, for residential property in Singapore:

Buyer Profile

1st Property

2nd Property

3rd+ Property

Singapore Citizen

0%

20%

30%

Singapore Permanent Resident (PR)

5%

30%

35%

Foreigner (non-PR, non-SC)

60% — flat rate, regardless of how many properties held in Singapore

Corporate entity / trust

65% — flat rate on residential property

Source: IRAS, effective 27 April 2023. FTA exemptions apply for nationals of the USA, Switzerland, Iceland, Liechtenstein, and Norway.

Figure 2: ABSD Rates by Buyer Profile — Singapore 2026 | Source: IRAS, effective 27 April 2023

Free Trade Agreement (FTA) Exemptions

Under Singapore’s FTA commitments, nationals of the USA, Iceland, Liechtenstein, Norway, and Switzerland are treated on par with Singapore Citizens for ABSD on their first residential property purchase. This means a US national buying their first Singapore condo pays 0% ABSD. On second and subsequent purchases, the SC schedule applies. The exemption is for individuals only; US-incorporated companies do not benefit. IRAS requires passport proof of nationality when claiming the FTA exemption.

What Foreigners Can Buy — and Cannot Buy

Permitted (60% ABSD where residential): Private condominiums, private apartments, strata-titled units, SOHO units with residential classification. ECs after privatisation (15 years from TOP for new GLS-launched ECs from 8 May 2026; 10 years for earlier ECs). Sentosa Cove landed property. Commercial shophouses, strata office units, retail units, industrial factories, warehouses — all without residential ABSD.

Not permitted without special approval: Landed residential property outside Sentosa Cove (houses, semi-detached, bungalows, terraced houses). The SLA may grant approval under the Residential Property Act in exceptional circumstances, but approvals are rare.

Strictly prohibited: HDB flats (both new BTO and resale). HDB housing is reserved for Singapore citizens and permanent residents under the Housing and Development Act. ECs during their MOP and privatisation period are also off-limits to foreigners.

Buyer’s Stamp Duty (BSD) — Payable by Everyone

BSD is levied by IRAS on every property purchase in Singapore, regardless of nationality. For residential property, the tiered rates are: 1% on the first S$180,000; 2% on the next S$180,000; 3% on the next S$640,000; 4% on the next S$500,000; 5% on the next S$1,500,000; and 6% on amounts above S$3,000,000. On a S$2.5M purchase, total BSD = S$94,600.

Purchase Price Tier

BSD Rate

BSD on This Tier

First S$180,000

1%

S$1,800

Next S$180,000 (up to S$360,000)

2%

S$3,600

Next S$640,000 (up to S$1,000,000)

3%

S$19,200

Next S$500,000 (up to S$1,500,000)

4%

S$20,000

Next S$1,500,000 (up to S$3,000,000)

5%

Up to S$75,000

Remainder above S$3,000,000

6%

Variable

Sellers’ Stamp Duty (SSD) — The Anti-Flip Tax

SSD is administered by IRAS and applies to all sellers who dispose of residential property within three years of purchase, regardless of nationality. The rates are: 12% within 1 year; 8% within 2 years; 4% within 3 years; nil thereafter. For a foreigner who has paid 60% ABSD, an SSD liability on a short-term resale would be a severe additional burden. Foreign buyers must plan for a meaningful long-term holding horizon.

Holding Period

SSD Rate

Up to 1 year

12%

1 to 2 years

8%

2 to 3 years

4%

More than 3 years

Nil

Financing — LTV, TDSR, and Mortgage Options

Foreigners may borrow from Singapore-licensed banks subject to MAS macro-prudential rules identical to those applied to residents. The LTV limit is 75% for a first property loan with no existing housing loans (reducing to 55% for a second and 35% for a third). The TDSR cap is 55% of gross monthly income. Loan tenors run up to 35 years, typically reduced by age exceeding 65. Most major Singapore banks lend to foreigners — DBS, OCBC, UOB, Standard Chartered, and HSBC all do so, subject to enhanced documentation requirements including overseas income proof and a valid work pass or Long-Term Visit Pass.

The Buying Process — Step by Step

Arrange in-principle approval: Approach at least two Singapore banks before making offers. Allow 5–10 working days.

Engage a CEA-licensed agent: For new launches, no buyer commission is payable; for resale, co-broking arrangements vary.

Option to Purchase (OTP): On resale, the seller grants an OTP valid for 21 days; a 1% option fee is paid. For new launches, a 5% booking fee is paid directly to the developer.

Pay BSD and ABSD: Both due within 14 days of OTP exercise. On a S$2.5M purchase, this means wiring S$94,600 (BSD) + S$1,500,000 (ABSD) to IRAS — a total of S$1,594,600 within a fortnight of signing.

Engage a conveyancing solicitor: A Singapore-qualified solicitor handles title searches, mortgage documentation, and lodgement with SLA’s eConveyancing portal.

Completion: For resale, typically 8–12 weeks. For new launches, completion occurs at TOP/CSC, which may be 3–5 years away.

Worked Example: Mr David Harrington Buys a S$2.5M CCR Condo

Mr David Harrington, 42, is a British national on an Employment Pass earning S$25,000/month gross. He purchases a two-bedroom unit in District 9 at S$2,500,000, with no existing property loans in Singapore.

Monthly mortgage at 3.30% p.a. over 20 years on S$1,875,000 ≈ S$10,633/month. TDSR check: S$10,633 ÷ 55% = S$19,333 minimum monthly gross income required. Mr Harrington’s S$25,000/month comfortably qualifies. However, stamp duties alone represent 63.8% of the purchase price — the property must appreciate significantly for the investment to make financial sense on a net basis.

What This Means for Foreign Buyers

Despite the 60% ABSD headline rate, Singapore continues to attract foreign buyers for structurally sound reasons. Singapore offers secure freehold and 99-year leasehold titles with one of the most transparent property title systems in Asia. There is no capital gains tax, no inheritance tax, and no wealth tax. The SGD has historically been stable and appreciating against most major currencies, and Singapore’s rule of law is consistently ranked among the best globally.

For high-net-worth buyers from jurisdictions with currency risk, political instability, or restricted capital mobility — particularly from certain parts of Southeast Asia, China, and the Middle East — paying 60% ABSD is the premium for a stable, internationally recognised store of value. For US nationals, who pay 0% ABSD on their first purchase thanks to the FTA, Singapore offers one of the most favourable entry points into any developed-market property system globally.

What Might Come Next

The 60% ABSD rate for foreigners is unlikely to be reduced in the near term. Singapore’s government has consistently adjusted rates upward when demand has been firm, and the April 2023 doubling was a clear statement of direction. The EC policy changes of 8 May 2026 — extending MOP to 10 years and privatisation to 15 years, abolishing the Deferred Payment Scheme — further indicate a tightening trajectory. Foreign buyers should plan their acquisitions assuming the 60% rate will persist for the foreseeable future and structure their financial planning accordingly.

Can a foreigner on an Employment Pass buy a condo in Singapore?

Yes. Holding an Employment Pass does not confer Singapore PR status, so the buyer is classified as a foreigner for ABSD purposes — meaning 60% ABSD applies. There is no minimum residency duration requirement to purchase private residential property. The buyer must satisfy the bank’s TDSR requirements using their Singapore employment income (fully counted) and any overseas income (subject to a bank haircut, typically around 30% on variable income).

Are there properties foreigners can buy without the 60% ABSD?

Yes. Commercial and industrial properties do not attract the residential ABSD. Strata office units, retail units, commercial shophouses, industrial factories, and warehouses can all be purchased by foreigners without the 60% surcharge. Many foreign investors therefore channel their Singapore property exposure through commercial assets or Singapore REITs listed on SGX, which provide property-linked returns without the ABSD burden.

Can a foreigner married to a Singapore Citizen pay lower ABSD?

Not directly on a joint purchase. If the property is purchased in the Singapore Citizen spouse’s name alone (sole ownership) and it is the SC’s first property, no ABSD is payable. However, if both names appear on the title, the foreigner’s inclusion triggers 60% ABSD. Many cross-nationality couples place the first property in the SC’s sole name. On subsequent purchases in joint names, ABSD at the SC second-property rate of 20% applies. Seek independent legal and tax advice before structuring ownership this way, as there are CPF, mortgage liability, and estate planning implications.

When exactly must the ABSD be paid?

ABSD must be paid within 14 days of the date on which the liability arises — typically the date of exercising the OTP or the date of the Sale and Purchase Agreement, whichever is earlier. Late payment attracts a 5% per annum penalty interest plus potential IRAS prosecution under the Stamp Duties Act. There is no grace period. The full ABSD amount must be available on or before the deadline, not merely committed in a loan facility.

Is ABSD refundable if the purchase falls through after the OTP is exercised?

Generally, no. Once the ABSD liability arises, it is payable regardless of whether the transaction completes. IRAS may consider a remission application in exceptional circumstances if a transaction is aborted, but this is not guaranteed. The ABSD Married Couple Remission — which allows one SC/PR spouse to sell their existing property within six months of a joint purchase and claim a refund — does not apply to foreigners. Always consult a licensed conveyancing solicitor before exercising any OTP if there is uncertainty about financing, as the ABSD liability is triggered on signing.

Can a foreigner buy a shophouse and occupy the upper residential floor?

This depends on the shophouse’s URA zoning and approved use. If the upper floors are classified as residential under the Residential Property Act, a foreigner cannot purchase without SLA approval (rarely granted). Some shophouses are zoned entirely commercial or approved for mixed use with the upper floors treated as non-residential. The correct approach is to check the URA Master Plan zoning and the specific approved use with a conveyancing solicitor before making any offer, as the legal classification is significant and not always obvious from the building’s physical appearance.

Does a foreigner pay ABSD on a privatised Executive Condominium?

Yes. Once an EC is privatised, it is treated as private residential property and all standard ABSD rules apply — including the 60% rate for foreigners. For ECs launched under GLS tenders from 8 May 2026, privatisation occurs at 15 years from TOP; earlier ECs privatise at 10 years from TOP. Buyers purchasing privatised ECs in the secondary market should verify the specific EC’s TOP date and calculate the privatisation milestone accordingly before making an offer.

Disclaimer: This article is for general information only and does not constitute legal, tax, or financial advice. Stamp duty rates, eligibility rules, and financing guidelines are subject to change by IRAS, MAS, HDB, SLA, and URA. Always verify current rates at iras.gov.sg and consult a licensed Singapore conveyancing solicitor, a CEA-registered real estate professional, and a licensed mortgage adviser before committing to any property transaction. All figures are illustrative based on publicly available data as at 16 May 2026.

Loan-to-Value (LTV) is the single most important number in a Singapore home-purchase budget. It tells you, before anything else, the maximum slice of the property price the bank is willing to lend — and therefore the cash and CPF you need to bring yourself. Misread it by even five percentage points and you may find yourself short by tens of thousands of dollars on completion day.

This guide walks you through the LTV framework as it stands in 2026 — the rate ladder by housing-loan count, how tenure and age cut into the cap, how LTV interacts with TDSR and MSR, and the practical decisions buyers face. The framework is set by the Monetary Authority of Singapore (MAS) Notice 645 and reinforced by HDB’s own concessionary loan rules.

Quick Answer — LTV at a glance

Bank loan, first housing loan: up to 75% LTV, tenure up to 30 years for private (25 years for HDB).

Second housing loan: up to 45% LTV; third or more: up to 35%.

If tenure exceeds 30 years OR runs past borrower age 65: caps drop to 55% / 25% / 15%.

HDB Concessionary loan: up to 75% LTV, 25-year max tenure.

The cash component of the down-payment is at least 5% (private) or 10% (HDB Concessionary).

LTV is one of three gates — you must also pass TDSR (55%) and, for HDB/EC, MSR (30%).

What Is Loan-to-Value — and Why Does It Exist?

LTV is the ratio of the housing loan amount to the property’s purchase price or market value, whichever is lower. Banks use it as a first-pass risk control: a higher LTV means thinner equity from the borrower, which means less cushion if property prices fall.

MAS sets the LTV ceiling industry-wide. The ceiling has been progressively tightened since the cooling-measure era began in 2013, as the regulator’s priority shifted from supporting first-time owner-occupiers to discouraging investment-driven leverage. The most recent recalibration was December 2021, which lowered LTV on second housing loans from 50% to 45% and on third loans from 40% to 35%. That framework remains in force in 2026.

LTV limits Singapore 2026 — the cap that sets the size of your loan.

The 2026 LTV Ladder — Bank Housing Loans

The headline number you have heard — “75% LTV” — only applies to first-time housing-loan borrowers under standard tenure. Once you have an existing housing loan or stretch the tenure beyond the conservative limit, the cap falls sharply.

Figure 1: LTV ladder for bank housing loans, by housing-loan count and tenure.

Borrower scenario

Standard LTV

If tenure > 30 yrs OR runs past age 65

No outstanding housing loan

75%

55%

One outstanding housing loan

45%

25%

Two or more outstanding loans

35%

15%

Two practical points are worth flagging. First, the 30-year tenure rule does not mean a 30-year loan is always available — banks themselves often cap tenure earlier for older borrowers. Second, the “outstanding housing loan” count includes loans for properties you co-own as a guarantor or as a second name on the title; the regulator does not look only at your primary mortgage.

Cash Component — The Mandatory Minimum

LTV defines the maximum the bank will lend; the rest must come from the buyer. But of that “rest”, a minimum portion must be in cash and cannot be funded from CPF Ordinary Account.

Loan type

Minimum cash

Balance from CPF or cash

Bank loan, 75% LTV

5% of price

20% of price

Bank loan, 55% LTV (long tenure)

10% of price

35% of price

Bank loan, 45% LTV (2nd loan)

25% of price

30% of price

HDB Concessionary loan

10% of price

15% of price (CPF or cash)

The cash floor is the practical constraint that catches most upgraders by surprise. A buyer with a S$1.5M target and 75% LTV needs S$75,000 cash on the table at exercise day — on top of BSD, ABSD, and legal fees. CPF Ordinary Account balances cannot substitute for this minimum.

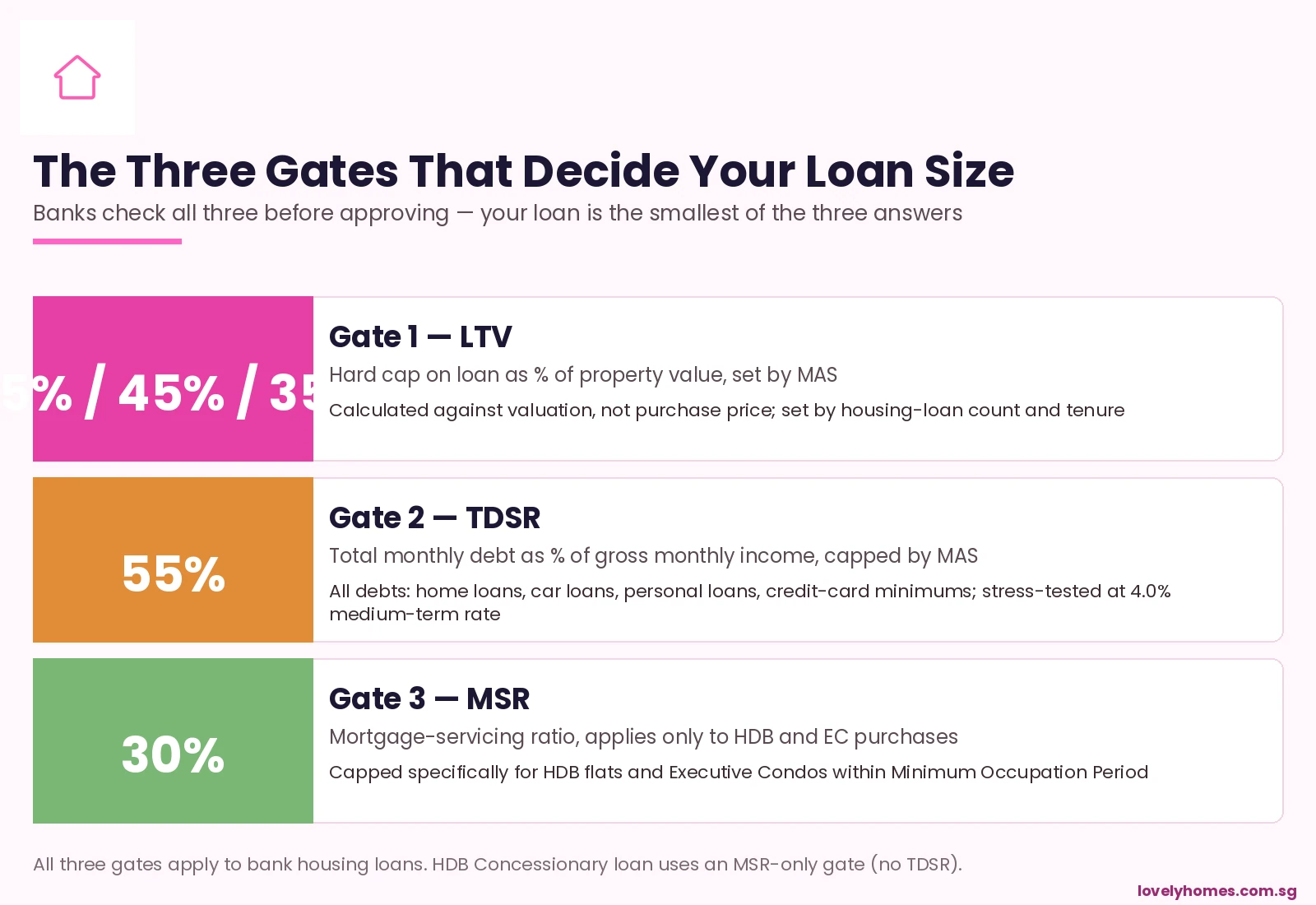

The Three Gates — LTV, TDSR, and MSR

LTV is only one of three caps. Banks must also satisfy:

Figure 2: The three gates — your loan is the smallest of the three answers.

LTV — absolute % of property value, set by MAS as above.

TDSR (Total Debt Servicing Ratio) — total monthly debt repayments capped at 55% of gross monthly income, stress-tested against a 4.0% medium-term interest rate even though current bank rates are well below that. All debts count: home loans, car loans, education loans, personal loans, credit-card minimum repayments.

MSR (Mortgage Servicing Ratio) — only for HDB flats and Executive Condos within MOP, capped at 30% of gross monthly income.

The bank computes the maximum loan under each rule and lends you the smaller of the three. A buyer at 75% LTV but with a heavy car loan can find their actual loan capped by TDSR rather than LTV; an HDB buyer with no other debts often finds MSR — not LTV — is the binding constraint.

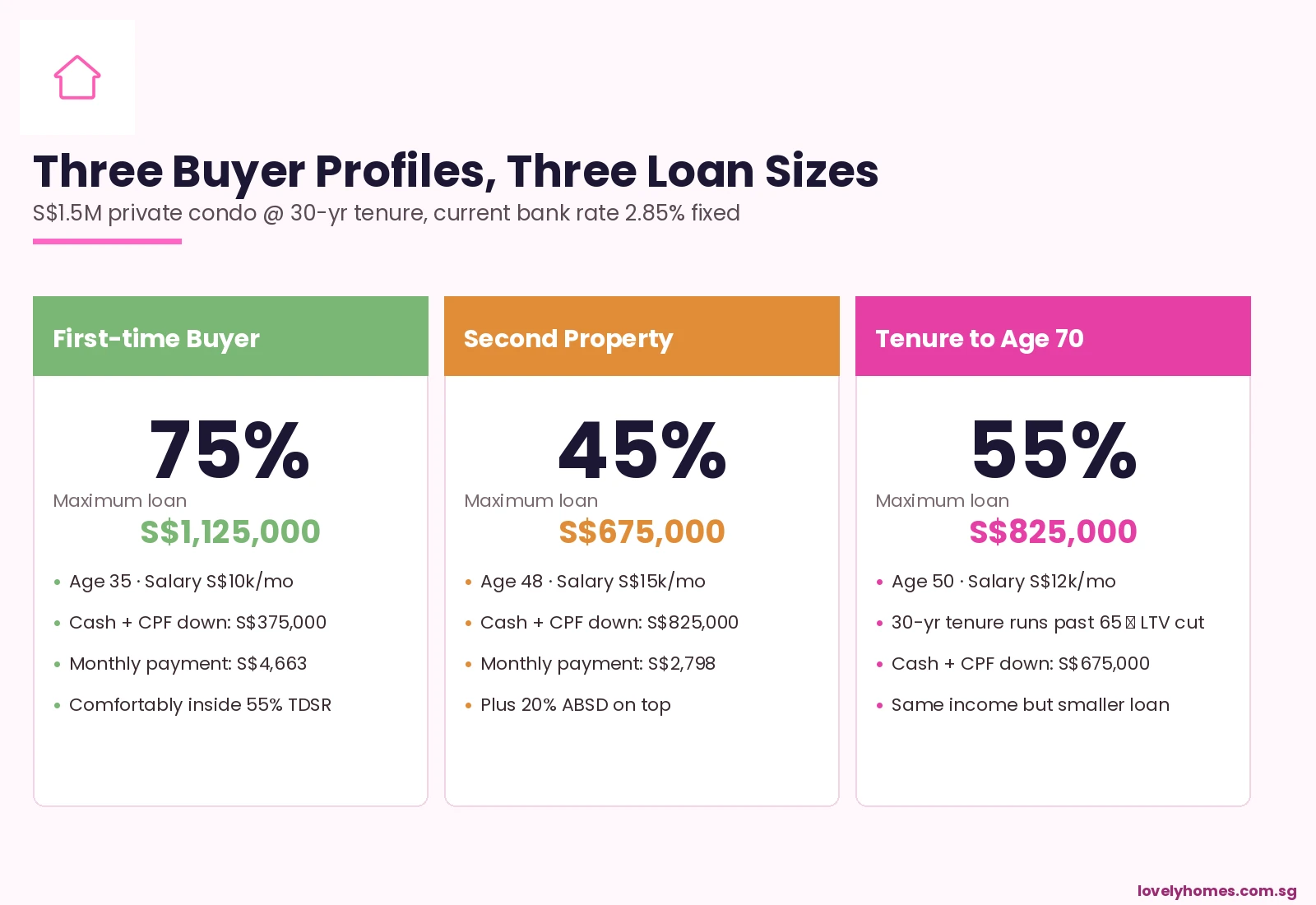

Worked Example — Three Buyer Profiles, Three Loan Sizes

Consider three buyers all looking at the same S$1.5M private condo, taking a 30-year loan at 2.85% fixed:

Figure 3: Three buyer profiles compared on identical S$1.5M condo.

The first-time buyer at age 35, salary S$10k/month, no other loans, gets the textbook 75% LTV: S$1,125,000 loan, S$375,000 down (5% cash + 20% CPF/cash). Monthly payment S$4,663 — comfortably inside 55% of S$10k.

The second-property buyer at age 48 with one outstanding home loan is capped at 45% LTV: S$675,000 loan only, S$825,000 down. This buyer also pays 20% ABSD on the new property — an additional S$300,000.

The upgrader to a tenure that runs past age 65 at age 50 is capped at 55% LTV (because the 30-year tenure runs to age 80, well past 65): S$825,000 loan only. Same income as the second buyer, but bigger loan because no existing housing loan; still smaller than the first-time buyer because of the tenure rule.

HDB Concessionary Loan — A Different Beast

The HDB Concessionary loan, available to buyers of new and resale HDB flats meeting income and ownership criteria, runs on its own framework:

LTV: up to 75% of valuation, identical to first-time bank loan.

Tenure cap: 25 years for new flats, 25 or 30 years for resale depending on age.

Interest rate: pegged to CPF Ordinary Account rate plus 0.1% — currently 2.60% (CPF OA at 2.5% + 0.1% spread, rate-locked).

MSR-only gate: 30% of gross income, no separate TDSR overlay.

Rule of two: Singapore households are limited to two HDB Concessionary loans across a lifetime, with a five-year wait between the first and second.

For comparable risk profiles, the Concessionary loan typically beats bank loans on cost; the trade-off is the more rigid tenure cap and the requirement to deplete CPF OA balances above S$20,000 first.

What This Means for You as a Buyer in 2026

The 2026 environment is the tightest LTV regime Singapore has had in two decades. Combined with stress-tested TDSR at 4.0% and ABSD at 20% on second properties for citizens, the effective leverage available to a typical buyer is materially below where it sat pre-2018.

Three practical conclusions:

Plan around the binding gate, not around LTV alone. Run all three checks before committing — ask your banker to model TDSR with all your debts, and MSR if you are buying HDB or EC.

Tenure is now a real lever for older buyers. Choosing a 25-year tenure that ends before 65 can keep you on the 75% LTV track even at age 40. Stretching to 30 years past 65 cuts to 55%.

Reserve capital, not just cash. The 5% mandatory-cash floor is the headline; in practice you also need BSD, ABSD, legal fees, and a six-month reserve buffer. A S$1.5M purchase typically requires S$120,000 in cash on the table at exercise.

Frequently Asked Questions

Is LTV calculated on the purchase price or the valuation?

The lower of the two. If a property is bought at S$1.5M but the valuation is S$1.45M, the bank applies LTV to S$1.45M. The remaining S$50,000 must be covered in cash — this is the dreaded “valuation gap” that catches buyers in rising markets.

Does selling my existing property before buying a new one reset my LTV count?

Yes — provided the existing housing loan is fully discharged before the OTP date on the new purchase. Banks check the credit bureau records on the day of credit assessment, and a discharged loan no longer counts as outstanding. This is why “sell-then-buy” buyers can access the 75% LTV track that “buy-then-sell” buyers cannot.

Can I take a 35-year loan if I am only 30 years old?

The MAS framework permits it, but bank policies vary. Most banks prefer to cap tenure at 30 years even for young borrowers. Even where 35 years is permitted, the over-30 tenure rule kicks in and reduces the LTV cap to 55% on the first loan — usually a poor trade-off.

Does my spouse’s housing loan affect my LTV count?

If you co-borrow on a single property, you are counted as one applicant for LTV purposes. If your spouse has a separate property in their sole name with an outstanding loan, that does not count against you when you buy in your sole name — this is the basis of decoupling strategies that release ABSD allowance.

What happens if my loan application is approved but my income drops before completion?

Banks reserve the right to re-underwrite at completion. A material income drop (typically more than 20%) between approval and completion can lead to a loan reduction or, in extreme cases, withdrawal. Buyers facing this should engage their banker proactively rather than wait for completion day.

Are there any loans that bypass LTV?

Not for residential property. Some private banks offer “lombard” or asset-backed lending against shares, bonds, or insurance policies, which sit outside the housing-loan framework, but these are not housing loans and the security is the financial portfolio, not the property. They are an option mainly for high-net-worth borrowers with substantial liquid investments.

Does SORA-pegged versus fixed-rate make a difference to LTV?

No. LTV is set by the housing-loan count and tenure, regardless of the rate type. Fixed and floating loans face the same LTV cap. Choice between fixed and SORA is a separate decision driven by rate outlook and personal risk preference.

This article provides general information about LTV and related housing-loan rules in Singapore as at May 2026. It is not financial, tax, or legal advice. LTV ceilings, cash-component rules, TDSR and MSR are set by the Monetary Authority of Singapore, the Inland Revenue Authority of Singapore, and the Housing & Development Board, and may be amended at any time. For authoritative figures, consult MAS, HDB, CPF Board, the Urban Redevelopment Authority, and SingStat. Before signing an Option to Purchase, engage a licensed Singapore mortgage banker, conveyancing solicitor, and where relevant a financial planner to model your situation specifically.

The HDB upgrader guide Singapore 2026 is your complete, step-by-step resource for navigating the most financially significant move many Singaporeans will ever make: selling your Housing Development Board flat and purchasing a private condominium. Whether you are a Singapore Citizen approaching Minimum Occupation Period, or a permanent resident re-evaluating your property portfolio, understanding the full financial, regulatory, and timing picture is essential before you commit to either transaction.

Quick Answer — HDB Upgrade at a Glance

You must meet a Minimum Occupation Period (MOP) of 5 years before selling your HDB flat (resale) or renting it out entirely

Singapore Citizens buying a private condo while retaining their HDB pay 20% ABSD on the private property purchase

The sell-first strategy eliminates ABSD and is used by the majority of upgraders; the buy-first strategy preserves housing continuity but incurs ABSD upfront

Minimum cash component for a private condo: 5% of purchase price (beyond what CPF can cover)

Your Total Debt Servicing Ratio (TDSR) must not exceed 55% of gross monthly income on all loans combined

CPF Ordinary Account savings used for the HDB must be refunded with accrued interest of 2.5% per annum upon sale

Full upgrade process (sell HDB + buy private): 7–9 months on a sell-first strategy; legal completion to collect keys adds 3–5 months for new launches

A Singapore Citizen household with S$800K HDB equity upgrading to a S$1.5M condo typically needs S$350K–$420K in additional cash/CPF

What Is the HDB-to-Private Upgrade Path?

Singapore’s dual-tier housing market — public HDB flats and private residential properties — creates a well-trodden upgrade path that the Housing Development Board and Urban Redevelopment Authority have both shaped through policy. An HDB flat is built on land sold to the HDB by the State under a 99-year lease; the HDB flat grant system, CPF usage rules, and MOP together form a structured subsidy framework designed to support first-time homeownership. The private condominium market, regulated separately by the URA, operates without the same direct subsidies, but also without income ceilings, nationality restrictions (for citizens and PRs), or MOP constraints once purchased.

The “HDB upgrade” is the act of monetising the subsidised first-home equity — essentially converting the benefit of below-market pricing and CPF grants into cash proceeds — and reinvesting those proceeds into the private market. The CPF Housing Grant for resale HDB flats, administered by the Housing Development Board, can total up to S$80,000 for eligible first-time buyer households; this grant accrues interest at 2.5% per annum and must be returned to CPF upon sale. Upgraders therefore need to account for this accrued interest deduction before calculating usable equity.

MOP: When Can You Sell?

The Minimum Occupation Period is the single most important gating rule. Under HDB regulations, resale HDB flat owners must physically occupy the flat for five years from the date of possession (for resale) or five years from the date of key collection (for new BTO flats purchased directly from the HDB). During the MOP you cannot sell your flat on the open market, rent out the entire flat, or own any private residential property in Singapore.

The five-year MOP was first introduced in 2010 and has remained stable since. For Prime Location Public Housing (PLH) flats announced from October 2021, the MOP is 10 years — a significant constraint for buyers in mature estates like Bishan, Queenstown, or the Pearl’s Hill development announced by MND in March 2026. Always verify the applicable MOP from your HDB letter of offer.

ABSD and the Simultaneous-Ownership Question

The single most expensive decision in the upgrade process is whether to sell your HDB flat before or after buying the private property. The difference is the Additional Buyer’s Stamp Duty, which is administered by the Inland Revenue Authority of Singapore (IRAS).

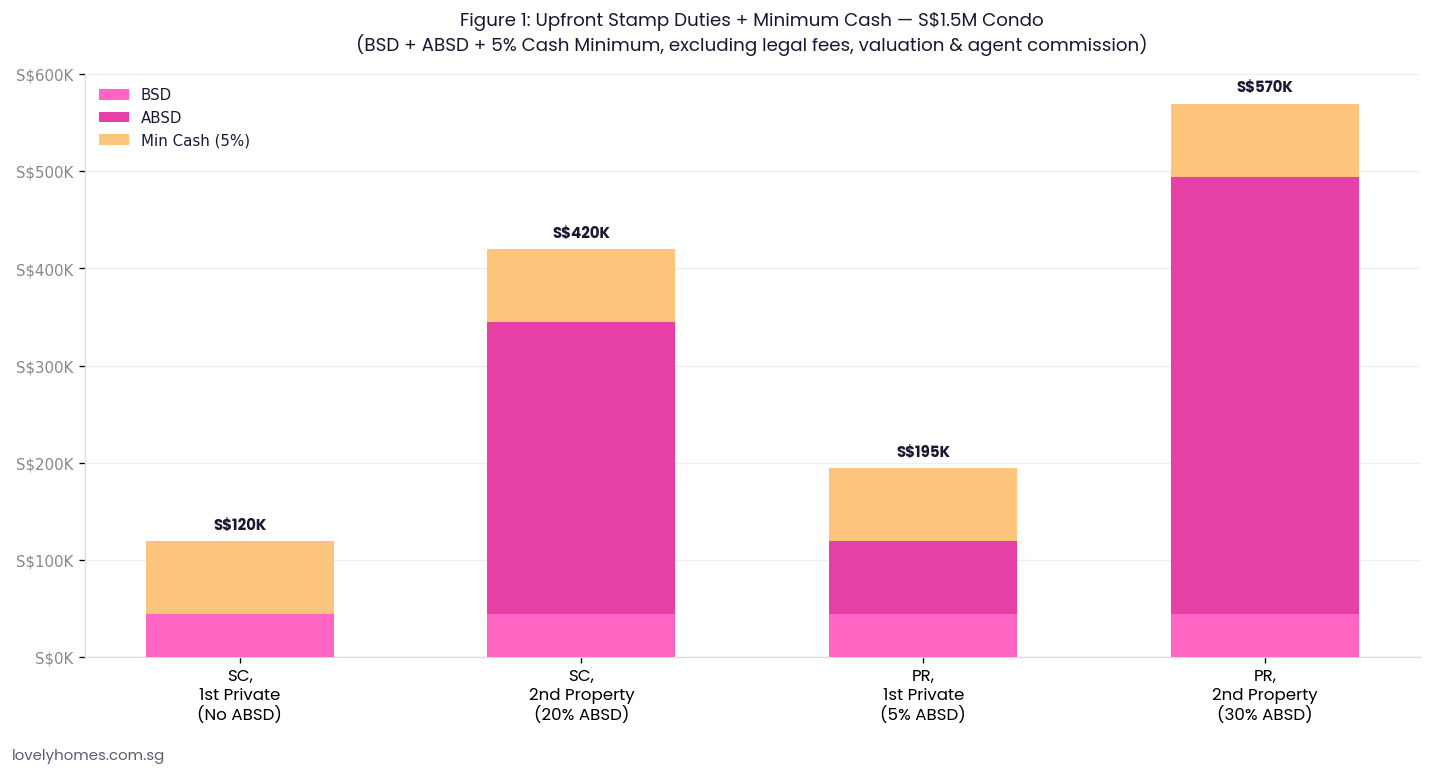

Figure 1: Upfront stamp duties + minimum cash for a S$1.5M private condo purchase by buyer profile. ABSD is administered by IRAS and is based on the purchase price or market value, whichever is higher.

At the current rates (effective 27 April 2023), a Singapore Citizen buying a second residential property pays 20% ABSD on the purchase price. On a S$1.5M condominium that is S$300,000 payable within 14 days of exercising the Option to Purchase. Permanent Residents buying their first private residential property pay 5% ABSD; their second attracts 30%.

The sell-first strategy means completing the HDB sale (and receiving the full proceeds) before exercising the OTP for the private property. As long as no private residential property is in your name at the point of exercising the OTP, the ABSD charge is 0% for a Singapore Citizen’s first private purchase. This is the financially dominant path for the majority of HDB upgraders and accounts for the bulk of upgrade transactions recorded in URA caveats each year. The downside is an interim period — typically 1–4 months — between HDB completion and private condo collection, during which the family must rent or stay with relatives.

The buy-first strategy preserves residential continuity and is preferred by households with school-age children needing school proximity, or families who cannot face temporary displacement. However, ABSD is payable in full at OTP exercise. IRAS does offer a Remission Scheme for Married Couples: if at least one buyer is a Singapore Citizen and the couple sells the first property within six months of the private purchase date (resale) or key collection date (new launch), IRAS will refund the ABSD on the second property. The refund is not automatic — the couple must apply via the IRAS MyTax Portal within the six-month window.

CPF Usage, Accrued Interest, and Usable Equity

Understanding your actual usable equity from the HDB sale requires two deductions many sellers underestimate. First, the outstanding HDB loan balance (typically financed at the CPF Ordinary Account interest rate of 2.6% per annum) or bank loan must be fully repaid upon completion. Second, all CPF Ordinary Account monies used for the purchase — including the principal plus accrued interest at 2.5% per annum compounded annually — must be refunded to your CPF OA before you receive any cash proceeds. The CPF Board, as custodian of the national retirement savings scheme, enforces this return to ensure retirement adequacy is not eroded by property liquidation.

Practical example: a flat purchased in 2016 for S$500,000 where S$150,000 was used from CPF over nine years will have accrued approximately S$38,000 in interest, meaning S$188,000 must be refunded to CPF. This refunded amount is not lost — it returns to your CPF OA for future use, including towards the new private property — but it does reduce the cash-in-hand proceeds from the HDB sale.

TDSR, MSR, and How Much You Can Borrow

Private property mortgage lending in Singapore is governed by the Total Debt Servicing Ratio framework, administered by the Monetary Authority of Singapore (MAS). Under TDSR rules, the monthly repayment on all outstanding credit facilities — including the new mortgage — must not exceed 55% of the borrower’s gross monthly income. MAS also applies a stress-test rate: variable-rate loans are assessed at the prevailing rate plus a floor, and fixed-rate loans are assessed at the actual fixed rate or 3.5% (whichever is higher, as of the most recent MAS guidance). This means that even if actual SORA-pegged mortgage rates are below 3.5% today, the bank will calculate affordability as if they were 3.5%.

The Mortgage Servicing Ratio — which caps HDB loan repayments at 30% of income — does not apply to private property. However, banks typically retain their own internal MSR-equivalent underwriting floors. For a household with S$12,000 monthly gross income, the maximum monthly debt service across all credit lines is S$6,600 (55%), and after deducting any car loan or personal loan obligations, the remaining capacity determines the maximum mortgage quantum.

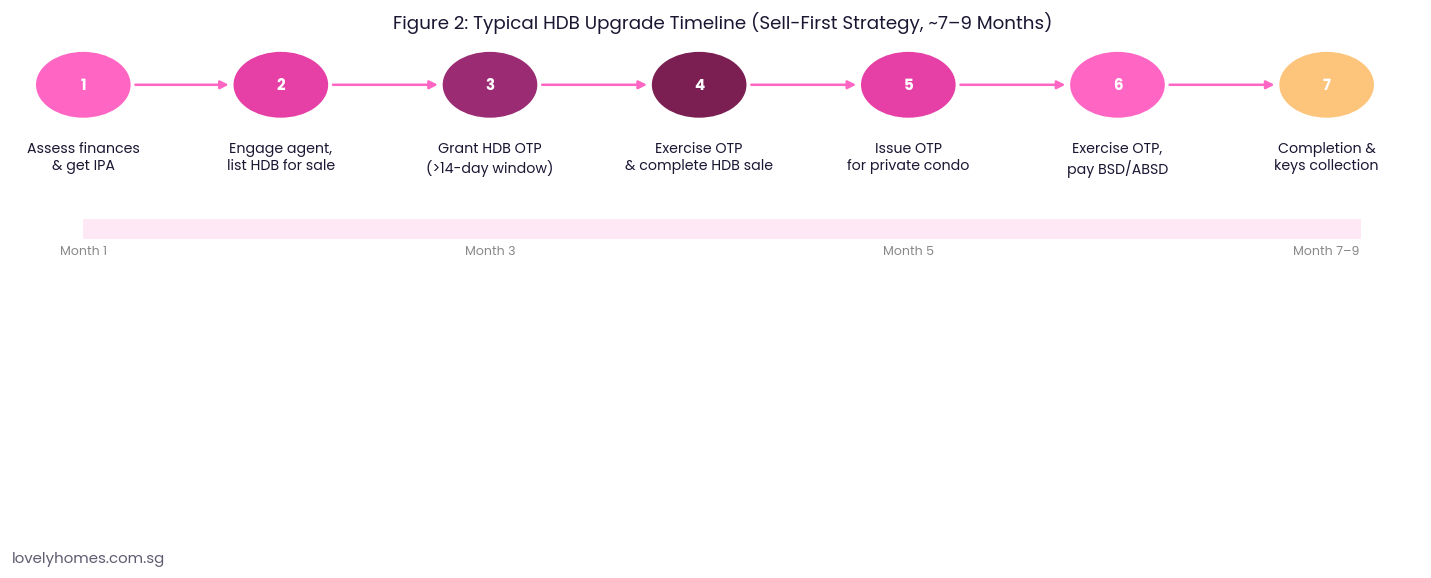

Figure 2: The typical sell-first upgrade timeline. Steps 1–4 cover the HDB sale; Steps 5–7 cover the private condo purchase. Total elapsed time is approximately 7–9 months for a resale private condo; add 2–5 years for a new launch.

The Loan-to-Value Framework for Private Property

Under MAS Notice 632, the maximum Loan-to-Value (LTV) ratio for a first housing loan from a financial institution is 75% of the lower of purchase price or market value, provided the loan tenure does not exceed 30 years and the borrower does not exceed 65 years of age at loan maturity. If either condition fails, the LTV drops to 55% or 45%. For upgraders who have fully repaid their HDB loan, the higher 75% LTV applies on the private condo purchase. For those with an outstanding HDB bank loan at the time of application (buy-first strategy), the LTV for the new loan may be reduced to 45%, further increasing the cash component required.

Summary Table: Key Upgrade Figures at a Glance

Parameter

Sell-First (No ABSD)

Buy-First (ABSD Remission)

ABSD (SC, 2nd property)

0% (sold HDB first)

20% upfront; refundable if HDB sold within 6 months

BSD (on S$1.5M)

~S$44,600 (both strategies)

~S$44,600

Min Cash Required

5% of purchase price

5% + 20% ABSD (cash or financing)

Max LTV

75% (no outstanding loan)

45% (outstanding HDB bank loan retained)

TDSR Limit

55% of gross income

55% of gross income

Typical Timeline

7–9 months (resale condo)

6 months from OTP exercise to sell HDB

CPF OA Accrued Interest

2.5% p.a., must refund to CPF upon HDB sale

Same

Worked Example: The Tans Upgrade from Tampines to Condo

Mr and Mrs Tan are a Singapore Citizen couple in their late thirties. They purchased a Tampines HDB 5-room resale flat in 2019 for S$620,000, using S$180,000 from CPF OA and taking an HDB bank loan for S$440,000 at 2.6% per annum. As of April 2026 — seven years into the loan — their outstanding loan balance is approximately S$360,000, and their CPF refund obligation (principal S$180,000 + accrued interest ~S$33,000) totals S$213,000. The flat is valued at S$750,000 on the open market.

Proceeds calculation (sell-first):

Sale price: S$750,000

Less: outstanding HDB loan repayment: −S$360,000

Less: CPF refund obligation: −S$213,000

Net cash-in-hand: S$177,000

CPF OA balance after refund: S$213,000 (available for new purchase)

New condo purchase at S$1.5M (sell-first, no ABSD):

BSD payable to IRAS: ~S$44,600

ABSD: S$0 (HDB sold first)

5% minimum cash: S$75,000

Loan quantum (75% LTV): S$1,125,000

CPF usable (OA): S$213,000 (can cover remaining 20% − 5% cash = S$225,000; short by ~S$12,000 in CPF — top up from cash or savings)

Combined gross household income for TDSR: S$14,000/month. Monthly mortgage on S$1,125,000 at 3.5% stress rate over 25 years ≈ S$5,630. TDSR = 40.2% — within the 55% cap. The upgrade is financially feasible.

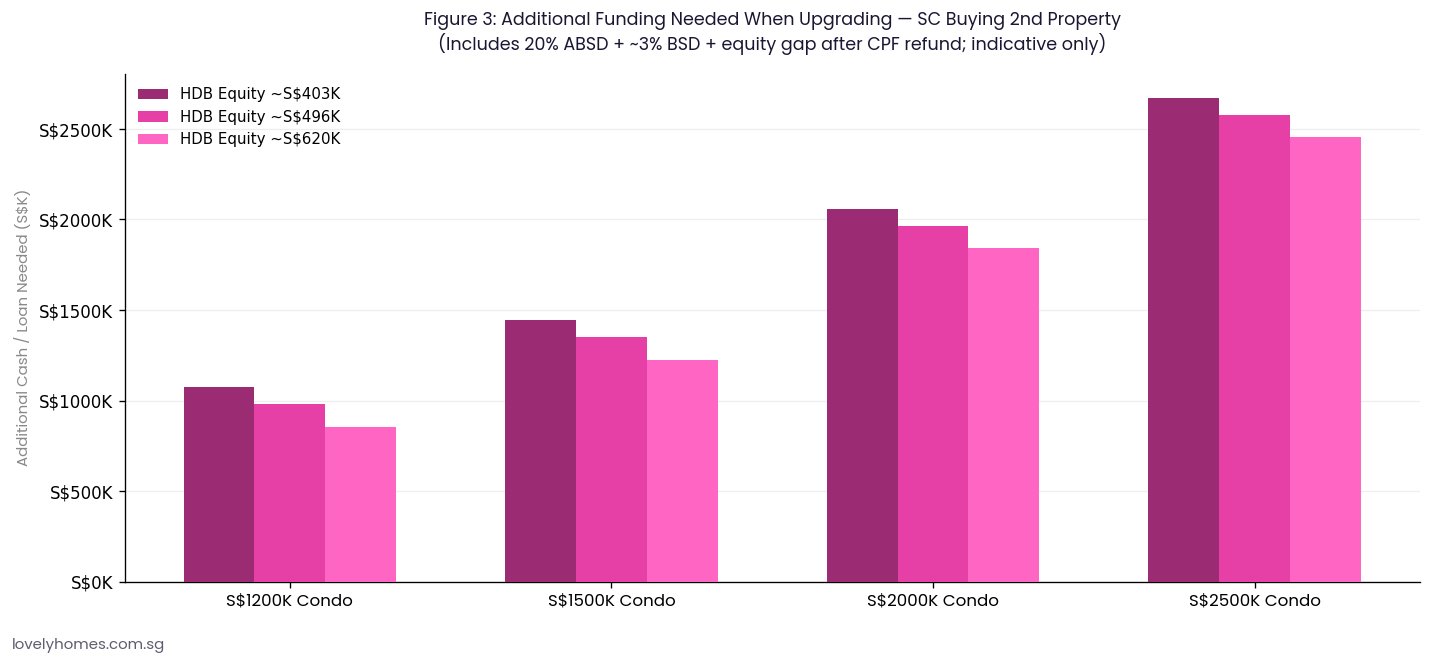

Figure 3: Additional cash or loan funding needed above HDB equity proceeds, by condo price point and usable equity level. All figures assume 20% ABSD (SC 2nd property) and 3% BSD; sell-first scenario removes the ABSD bar entirely.

Why the Upgrade Matters for Singapore Wealth Building

The HDB-to-private upgrade has historically been Singapore’s most reliable individual wealth-building step. URA transaction data consistently shows that private residential prices in the Rest of Central Region (RCR) and Core Central Region (CCR) have outpaced HDB resale price appreciation over 10-year rolling periods, particularly in proximity to MRT interchanges and integrated developments. The 2016–2026 decade saw HDB resale values rise approximately 40–55% in prime estates, while comparable private freehold or 99-year leasehold condos in the same districts appreciated 60–90%.

That said, the upgrade decision is not purely about capital appreciation. Private condo ownership typically involves higher monthly outgoings — management fees, sinking fund contributions, higher property tax under the non-owner-occupier progressive rate (administered by IRAS), and higher mortgage quantum — which compress monthly cash flow for the first 5–10 years. Households should model the cash-flow impact carefully using the actual mortgage rate (SORA + spread, typically 3.4–3.8% as of April 2026 for new floating-rate packages) rather than the stress-test rate.

What Might Come Next: Policy Watch for Upgraders

The current ABSD framework (20% for SC second property) has been in place since April 2023 and shows no sign of immediate revision. MAS and MND have both signalled that macroprudential tools will remain elevated as long as private property prices continue to rise. The URA reported a 0.9% quarter-on-quarter increase in private residential prices in Q1 2026 (full statistics released 25 April 2026), on top of a 0.6% gain in Q4 2025, suggesting sustained upward pressure that gives authorities little reason to ease ABSD. Upgraders planning their move in 2026–2027 should assume the 20% SC ABSD rate persists for the foreseeable future, and should build the sell-first timeline around that assumption.

One area to watch is the Lease Buyback Scheme and CPF use rules for older HDB upgraders (aged 55+), where CPF Retirement Account obligations create a different equity-release calculus. MND’s Committee of Supply 2026 speech hinted at ongoing reviews of CPF Retirement Sum drawdown rules for older owner-occupiers — any loosening could marginally improve equity available for the upgrade among this cohort.

Frequently Asked Questions

Can I buy a private condo before selling my HDB flat?

Yes, but as a Singapore Citizen you will be liable for 20% ABSD on the private condo purchase price, payable within 14 days of exercising the OTP. IRAS provides a Remission Scheme for married couples where at least one is a Singapore Citizen: if you sell your HDB within six months of the private condo’s key collection date (new launch) or OTP exercise date (resale), you may apply to IRAS for a refund of the ABSD paid. The refund is not automatic and requires a formal application within the stipulated window. Note that the 5% cash down payment for the private condo is still required upfront and is not refunded.

What happens to the CPF money I used for my HDB flat?

Upon selling your HDB flat, all CPF Ordinary Account monies used for the purchase — including the initial down payment, subsequent monthly instalments drawn from CPF, and any CPF Housing Grants received — must be refunded to your CPF OA with accrued interest at 2.5% per annum compounded annually. This refunded amount re-enters your CPF OA and can be used immediately for the down payment on your private condo purchase (subject to the CPF Withdrawal Limit and Valuation Limit rules). You do not lose this money — it simply remains within the CPF system rather than being paid out as cash. The CPF Board’s property portal at cpf.gov.sg provides a withdrawal calculator to estimate your exact refund obligation.

How much cash do I actually need to upgrade?

The minimum cash component for any private property purchase in Singapore is 5% of the purchase price. This must be paid in cash — CPF OA funds or bank loans cannot cover this component. For a S$1.5M condominium that is S$75,000. On top of this, you will need cash or CPF for the Buyer’s Stamp Duty (approximately S$44,600 on S$1.5M), legal fees (~S$3,000–$5,000), and a valuation fee (~S$300–$600). If you are using the sell-first strategy and have no ABSD to pay, total cash and CPF outlay to exercise the OTP is approximately S$120,000–$130,000 for a S$1.5M property, with the remainder funded by your mortgage and CPF OA balance.

Can I retain my HDB flat and buy a private condo?

Singapore Citizens and Permanent Residents are not prohibited from simultaneously owning an HDB flat and a private property, but the financial cost is high: as an SC you will pay 20% ABSD on the private property purchase, and as a PR you will pay 30% ABSD on your second property. Additionally, while you own both, the HDB flat remains subject to HDB rules including the restriction on fully subletting the flat until MOP is met (unless you are above 35, divorced, a single with the right to sublet under HDB’s rules, or have specific HDB approval). If you proceed with this dual-ownership approach, you must ensure your TDSR covers both your HDB loan instalments and the new private mortgage simultaneously.

What is the Temporary Housing Solution during the gap between HDB completion and condo collection?

Most sell-first upgraders experience a 1–6 month gap between HDB legal completion and moving into the new private property. The most common approach is a deferred completion arrangement negotiated with the HDB buyer at the point of signing the OTP — you agree to stay in the flat for a fixed rental period (typically 2–3 months at a market rate) after legal completion while your new home is prepared. Alternatively, families rent a unit in the open market at prevailing rates, or stay with extended family. Factoring rental costs of S$2,000–$4,500 per month (depending on unit size and district) into your upgrade budget is essential, particularly for the east and central regions where new launch condo waiting periods can extend to 3–5 years.

Are there specific private condos I cannot buy with my HDB equity?

There are no restrictions on which private condominium an HDB upgrader may purchase. However, two practical constraints often apply. First, Restricted Residential Properties under the Residential Property Act — Good Class Bungalows and most landed housing in Singapore — require Ministerial approval for Singapore Permanent Residents and are unavailable to foreigners entirely; Singapore Citizens may purchase without restriction. Second, if your usable CPF OA balance is below the Valuation Limit (the lower of purchase price and market value), your CPF usage will be capped; you must fund the shortfall from cash. Always check the CPF Board’s updated Valuation Limit rules at cpf.gov.sg before committing to a price point.

What happens if I cannot sell my HDB within the 6-month ABSD remission window?

If you purchased a private condo while retaining your HDB flat (buy-first strategy) and are unable to sell the HDB within six months of the private condo’s key collection date or OTP exercise date, the ABSD remission is forfeited — the 20% ABSD you paid upfront is not refunded. In practice, HDB resale transactions in Singapore typically complete within 8–16 weeks of listing, so the six-month window is generally achievable if you list the HDB promptly after exercising the condo OTP. The risk is greatest when buying a resale condo (shorter completion timeline) while your HDB is slow to sell. If you are uncertain, the sell-first strategy eliminates this risk entirely.

This article is intended for general informational purposes only and does not constitute financial, legal, or property advice. Stamp duty rates, CPF rules, HDB regulations, and MAS lending guidelines are subject to change; always verify current figures directly with the Inland Revenue Authority of Singapore (IRAS), the CPF Board, the Housing Development Board, and the Monetary Authority of Singapore. Consult a licensed property agent, bank mortgage specialist, and solicitor before making any property transaction decision. Nothing in this article should be treated as a solicitation to buy or sell any property.

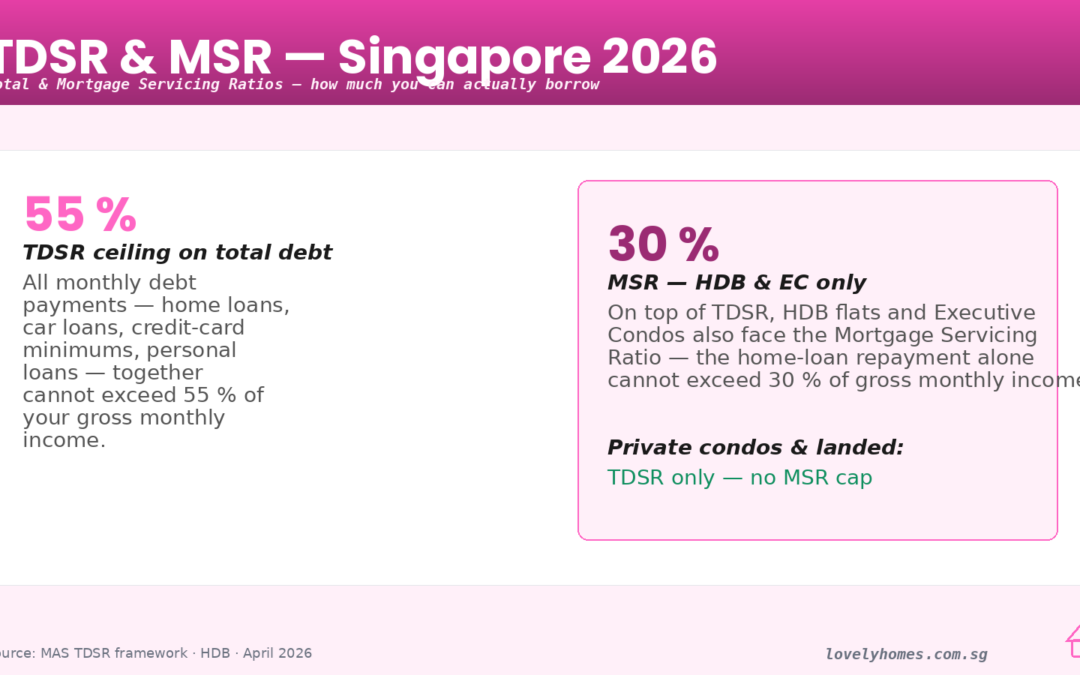

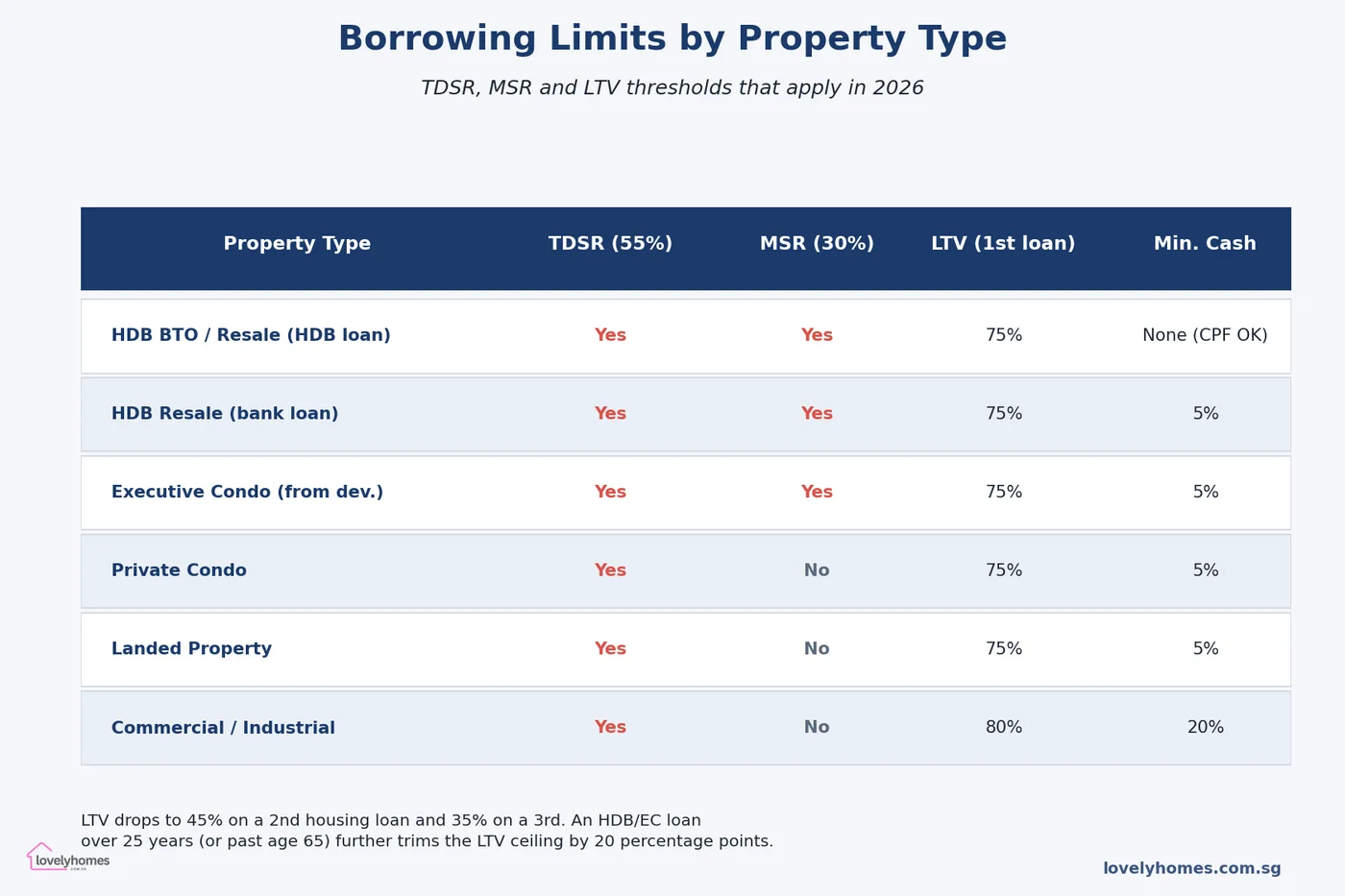

Figure 1: The two numbers that decide every Singapore home loan — TDSR at 55% of income and MSR at 30% for HDB and EC purchases.

If you have ever wondered why the bank’s pre-approval letter gave you a smaller loan than you budgeted for — or why a friend on the same salary can borrow noticeably more than you — the answer almost always comes down to two acronyms: TDSR and MSR. These are the two borrowing limits the Monetary Authority of Singapore (MAS) bakes into every residential mortgage, and in 2026 they are the single biggest determinants of how much home you can actually finance.

This guide is the 2026 edition. It covers exactly how TDSR and MSR are calculated, how they interact with the loan-to-value (LTV) cap, where the 4.0% stress-test rate comes from, what counts as income, what doesn’t, and — crucially — how to game the numbers in your favour without breaking any rules. We walk through a fully-worked Singapore example end-to-end and finish with the policy trajectory so you know what to watch for next.

Quick Answer: The 10 Things Every Singapore Borrower Should Know

TDSR is 55%. Total monthly debt repayments — including the new mortgage — cannot exceed 55% of your gross monthly income. Applies to every residential property loan.

MSR is 30%. Mortgage repayments on an HDB flat or Executive Condominium (EC) bought from the developer cannot exceed 30% of gross monthly income. Private condos and landed property have no MSR.

Stress-test rate is 4.0%. TDSR and MSR are calculated at a medium-term interest rate of 4.0% for residential loans, regardless of the rate you actually pay today.

LTV caps layer on top. First housing loan: up to 75% of purchase price. Second housing loan: up to 45%. Third and beyond: up to 35%.

Age and tenure matter. If the loan tenure pushes past age 65, or exceeds 30 years (25 for HDB), the LTV cap drops by 20 percentage points.

Variable income is haircut by 30%. Commission, bonus, rental and freelance earnings are only counted at 70% of the proven figure.

Existing debts eat into headroom. Car loans, credit-card minimum payments, student loans, and other mortgages all hit your TDSR ceiling before the new home loan does.

Guarantors are counted too. If you guarantee a sibling’s loan, it may sit in your TDSR — not theirs.

Cash down-payment rules mirror LTV. The first 5% (25% at higher LTV tiers) must be paid in cash; the balance can be CPF Ordinary Account funds.

Refinancing carve-out. Borrowers refinancing an owner-occupied property with no cash-out may be exempted from TDSR — a narrow but useful escape hatch.

What Is TDSR — The Framework That Underpins Every Home Loan

The Total Debt Servicing Ratio was introduced in June 2013 as part of MAS’s cooling-measures programme (see our full cooling measures timeline for the wider context). Its purpose is simple: to stop households from levering up to a level where a modest rise in interest rates would push them into negative cash flow. The 2010s saw Singapore’s household debt-to-GDP ratio climb past 70%, and MAS wanted a circuit-breaker that worked the same way regardless of which bank a buyer walked into.

TDSR caps all monthly debt obligations at 55% of gross monthly income. “All debt” is deliberately broad: it includes the prospective home-loan instalment (calculated at the stress-test rate), existing mortgages, car loans, personal loans, renovation loans, student loans, credit-card minimum repayments and any loans you have personally guaranteed. Even a dormant credit card with a S$20,000 limit is counted if the bank uses the 3% minimum-payment convention.

The ratio was originally set at 60% in 2013 and tightened to 55% in December 2021, where it remains in 2026. That three-percentage-point shave looks small on paper but at a typical Singapore household income removes roughly S$150,000–S$200,000 of borrowing capacity.

What Is MSR — The Second Ratio You Cannot Ignore for HDB and EC Buyers

The Mortgage Servicing Ratio is narrower but stricter. Introduced for HDB loans in 2011 and extended to bank loans on HDB flats in 2013, MSR caps the mortgage portion alone at 30% of gross monthly income for purchases of HDB flats and Executive Condominiums bought directly from the developer.

MSR is a subset of TDSR, not a substitute. HDB and new-EC buyers must clear both ratios — the tighter of the two binds. In practice MSR is almost always the binding constraint for HDB buyers because existing debt rarely adds up to the 25-percentage-point gap between MSR (30%) and TDSR (55%). For EC buyers the numbers narrow as the project moves through its 10-year maturation period — after the five-year minimum occupation period and the ten-year privatisation, a resale EC is treated like a private condo for borrowing-limit purposes, so TDSR alone applies.

For a side-by-side look at which ratios hit which property type, the matrix below summarises 2026 rules.

Figure 2: 2026 borrowing limits by property type. HDB flats and ECs face both MSR and TDSR; private condos, landed property and commercial assets only face TDSR.

How the 4.0% Stress-Test Rate Works — And Why It Matters More Than Your Actual Rate

Here is the trap that catches most first-time buyers: banks must calculate your monthly instalment using an assumed rate of 4.0% for residential mortgages, even if your actual rate is 2.5% or 3.0%. This is the medium-term interest rate, set by MAS and reviewed from time to time. It was revised upward from 3.5% to 4.0% in September 2022 and has not moved since.

Why 4.0%? The rate is designed to approximate the long-run average that Singapore floating-rate loans have oscillated around over a 30-year horizon. It is deliberately punitive — regulators would rather have borrowers told “you qualify for less” at origination than have the same borrowers go into arrears when rates spike. Anyone who lived through the 2022–2023 rate cycle, when three-month SORA went from 0.2% to 3.8% in 18 months, will appreciate the logic.

The mechanic: the bank plugs a 4.0% rate into the standard amortisation formula using your chosen loan tenure, derives an assumed monthly instalment, and tests that figure against your TDSR (55%) and, if applicable, MSR (30%). Your actual repayment — calculated at whatever rate the bank is offering — will be lower in most cases, leaving you with a margin of safety that MAS consciously engineered.

What Counts as Income — And Why Variable Pay Is Penalised

Income for TDSR/MSR purposes is not what you see on your IRAS tax statement. MAS prescribes a structured treatment:

Fixed salary. Counted at 100%. Evidenced by payslips (usually three to six months) and the latest CPF contribution history.

Variable income. Commission, bonus, overtime, and freelance earnings are haircut by 30%, so only 70% of the verified average is recognised. The haircut applies to the entire variable component, even if you can show multiple years of steady track record.

Rental income. Counted at 70% of the gross rent receivable, net of void periods. A two-year tenancy agreement is strong evidence; month-to-month leases are viewed more sceptically.

Self-employed / business income. Two years of Notice of Assessment (NOA) are the default evidentiary bar, with the 30% haircut applied.

Allowances and AWS. Typically 100% if contractual and evidenced; otherwise haircut.

This is where the seemingly simple 55% number becomes surprisingly individual. A banker earning S$12,000 monthly but with 40% of that as variable gets assessed on S$7,200 fixed + S$3,360 post-haircut variable = S$10,560 — so the TDSR ceiling drops to S$5,808 per month rather than the nominal S$6,600.

What Counts as Debt — The Items Borrowers Miss

The other half of the equation is debt. The headline items — the new home loan instalment, existing mortgages, and car loans — are obvious. Less obvious items often catch borrowers out:

Credit-card minimum payments. Banks use a 3% minimum convention on the outstanding balance (or sometimes on the total credit limit). If you carry S$30,000 revolving credit across cards, that is a S$900 monthly hit on your TDSR — shaving S$192,000 off your loan ceiling at a 4.0% stress rate over 30 years.

Renovation and personal loans. Unsecured loan instalments count in full.

Student loans. Included in TDSR from the date repayments begin.

Guarantor obligations. If you have co-signed a relative’s loan and there is no formal debt-transfer, some banks will count the full instalment against you. Others use 50%. Ask the relationship manager explicitly.

Outstanding ABSD remission obligations. If you are on a remission schedule (e.g. from selling a prior property to claim remission on a new purchase), the existing loan remains in TDSR until the sale completes.

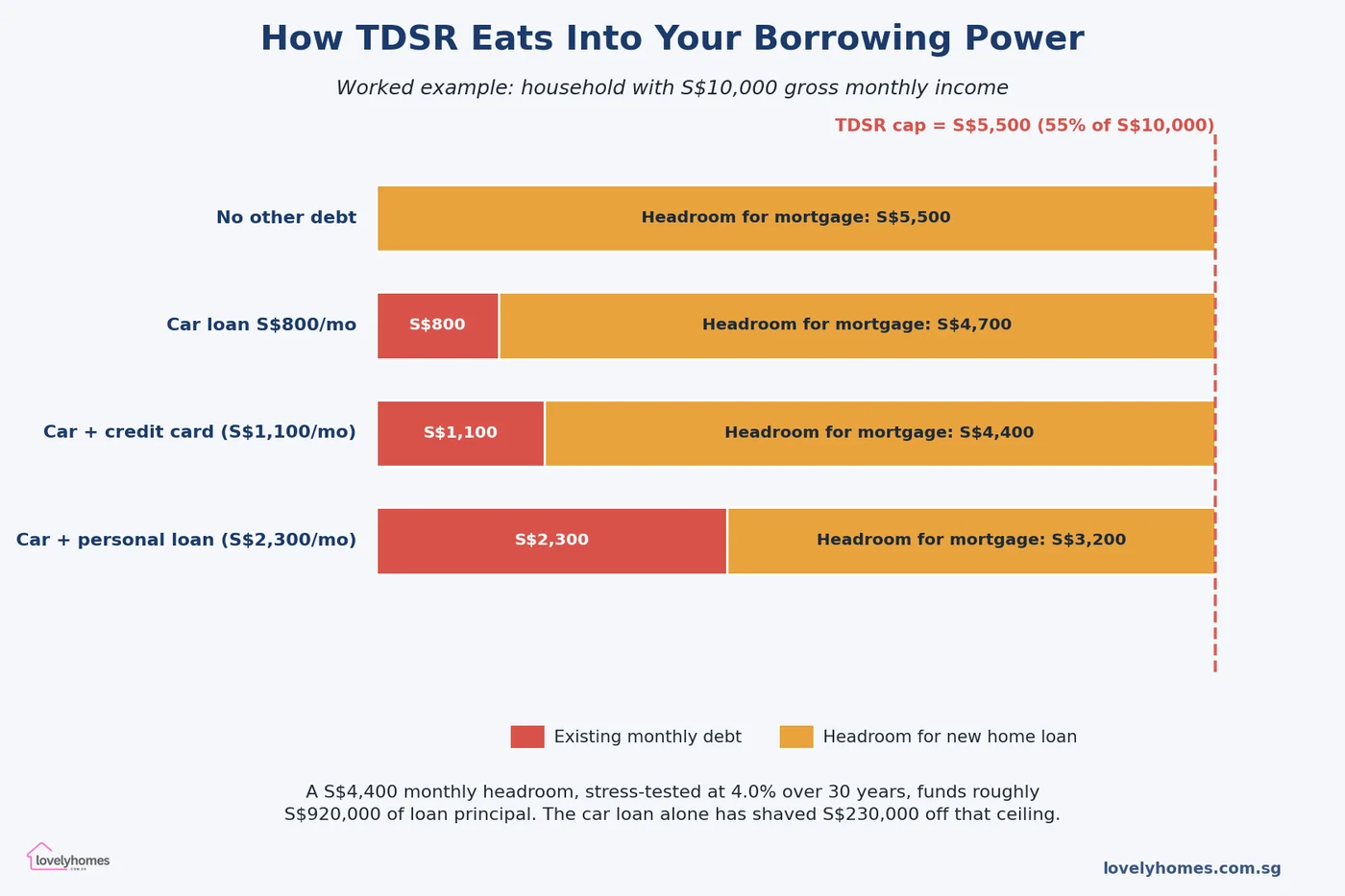

A Fully-Worked Example: A S$10,000-a-Month Household Buying a Private Condo

Figure 3: How different existing-debt profiles crater the monthly headroom available for a new mortgage, given a household earning S$10,000 gross.

Consider a dual-income couple: combined gross monthly salary S$10,000, both on fixed pay, no variable component. They are looking at a S$1.8 million resale private condo in District 15.

Step 1 — TDSR cap. 55% × S$10,000 = S$5,500. No MSR applies because this is a private condo.

Step 2 — Existing debts. One car loan at S$800/month and revolving credit balances generating a S$300/month minimum payment. Total existing obligations: S$1,100.

Step 3 — Headroom for the new mortgage. S$5,500 − S$1,100 = S$4,400 per month available for the new home loan instalment.

Step 4 — Maximum loan principal. At the 4.0% stress rate over a 30-year tenure, S$4,400 monthly funds approximately S$922,000 of loan principal (standard amortisation formula: P = M × [(1 − (1 + r)^(−n)) / r]).

Step 5 — LTV cap. At 75% LTV on an S$1.8m purchase, the bank could lend up to S$1,350,000 — but TDSR limits them to S$922,000 here, so TDSR binds, not LTV. The couple needs S$878,000 of combined cash and CPF equity.

Flip the same household to an HDB flat at S$700,000: now MSR binds first. 30% × S$10,000 = S$3,000 maximum mortgage instalment. That fundamentally funds roughly S$628,000 — well below the 75% LTV ceiling of S$525,000… wait. In this case the 75% LTV actually binds below MSR, because S$525,000 of loan needs only about S$2,500/month at 4.0% over 25 years, comfortably inside MSR. So the couple’s CPF-plus-cash needs to fill the remaining S$175,000.

These two scenarios show the recurring pattern: for HDB/EC buyers, MSR or LTV usually binds; for private/landed buyers, TDSR usually binds. The flow of the calculation matters, and every added dollar of existing debt has a disproportionate impact through the 30-year amortisation lever.

How to Legitimately Maximise Your Borrowing Ceiling

Nothing below involves gaming the system — each lever is recognised by banks and MAS. Together they can add S$200,000–S$400,000 to a buyer’s loan ceiling.

Close dormant credit facilities. A S$50,000 unused overdraft or a clutch of credit cards still hits TDSR via the 3% minimum rule. A week of admin before you apply for pre-approval can move the needle.

Pay down the car loan. High-instalment vehicle finance is the single most common TDSR killer. A S$1,000 monthly car note costs you roughly S$210,000 of home-loan capacity at 4.0%/30yr.

Lengthen the tenure (cautiously). A 30-year tenure beats a 25-year one on headline TDSR because the stress-rate instalment is lower — but watch the age-65 and 30-year triggers that knock the LTV down 20 points.

Co-apply with a higher earner. Joint applications aggregate income and debt. If spouses have different debt loads, consider which combination maximises the pooled headroom.

Formalise variable income. A commissioned sales professional with one year of written contracts may be haircut more heavily than one with two years of NOAs. Waiting one tax cycle can unlock meaningful capacity.

Use a Loan Assessment before committing. Banks in Singapore offer in-principle approval (IPA) at no cost. Three IPAs from different banks let you benchmark the figure.

How Singapore’s Framework Compares Globally

Singapore is not alone in prescribing debt-service ratios, but its combination is unusually strict. Hong Kong applies a 50% debt-service ratio with a 70% LTV cap for first-time owner-occupiers — broadly comparable but no separate MSR for public housing. The United Kingdom uses a 4.5× income loan-to-income ratio at most lenders (soft cap), with affordability stress-tested at 3 percentage points over the reversion rate. Australia’s prudential regulator APRA applies a serviceability buffer of 3 percentage points over the contracted rate — a rule-of-thumb approach rather than a hard ratio.

The common thread in all four jurisdictions is a stress-test mechanism designed to withstand a rate spike. Singapore’s 4.0% medium-term rate is higher (more conservative) than the contracted-rate buffers used in the UK and Australia, which is one reason Singaporean household debt has been more resilient through recent cycles than peers. MAS has been explicit that this is by design: household leverage is viewed as a systemic risk, not purely a consumer-protection issue.

What Might Come Next — The Forward View

The 4.0% stress rate has held since September 2022. Three scenarios could prompt a revision in the next 12–18 months:

Sustained higher long-term rates. If three-month SORA settles above 3.5% on a durable basis, MAS may nudge the medium-term rate to 4.25% or 4.5% to preserve the buffer it represents.

Renewed leverage in the private condo segment. If luxury-segment TDSR headroom is being used aggressively to bid up prime-district prices, expect tighter LTV on second/third loans rather than a TDSR change.

Public housing affordability stress. If HDB resale prices outrun wage growth materially, MSR could tighten from 30% to 25%. This would be the single most consequential move for first-time buyers.

None of the above is signalled by MAS at the time of writing (April 2026) — but the Financial Stability Review due in November 2026 is the data release to watch. Historically MAS has adjusted TDSR and MSR in the December statement that accompanies the cooling-measures package.

Frequently Asked Questions

1. Does TDSR apply to refinancing my existing mortgage?