Singapore Property Market Outlook H2 2026: Supply Wave, Rate Easing and What to Watch

Quick Answer: Singapore Property Market H2 2026

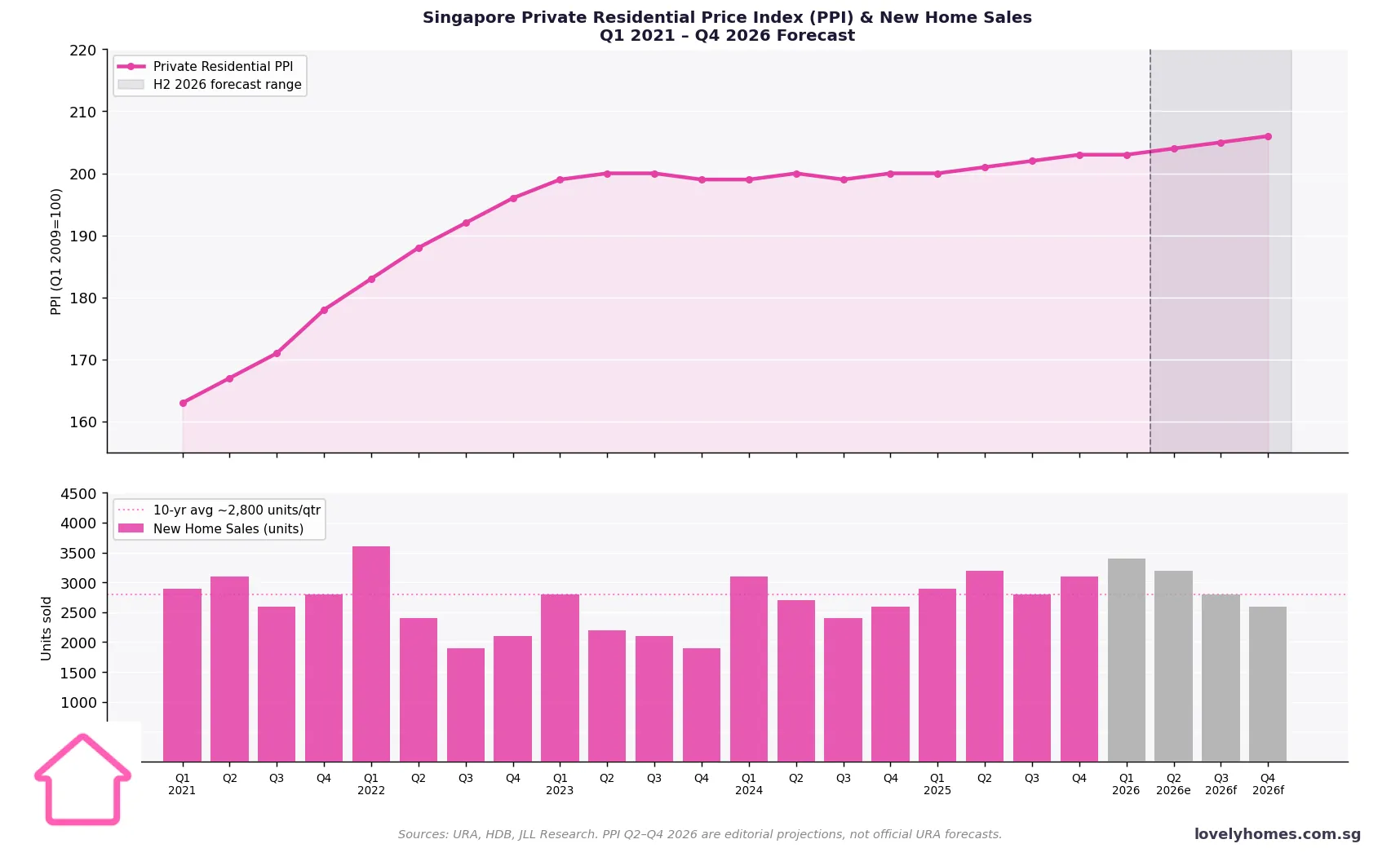

- Q1 2026 private residential prices (URA PPI) rose an estimated 0.8–1.2% quarter-on-quarter — a continued moderation from the 2021–2022 peak, consistent with the government’s stated aim of sustainable growth.

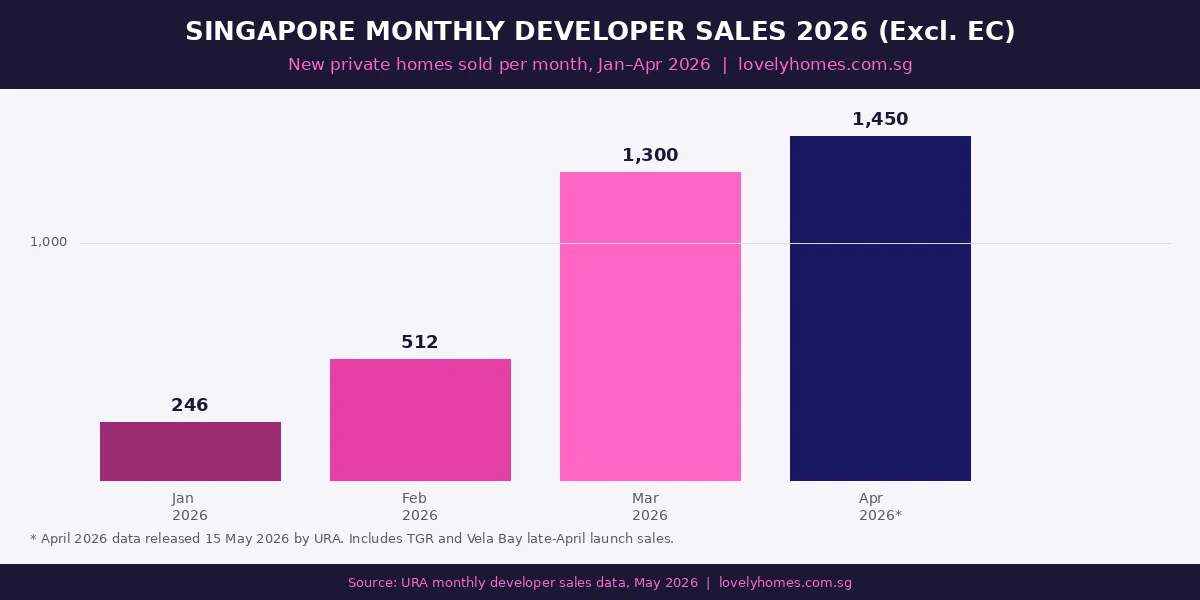

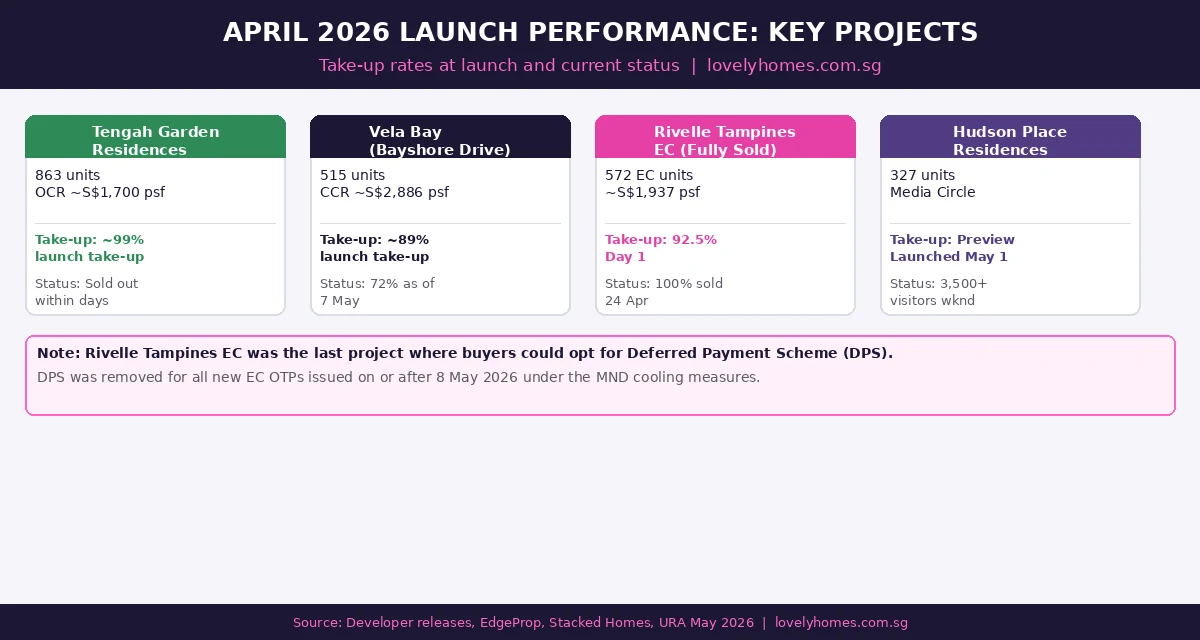

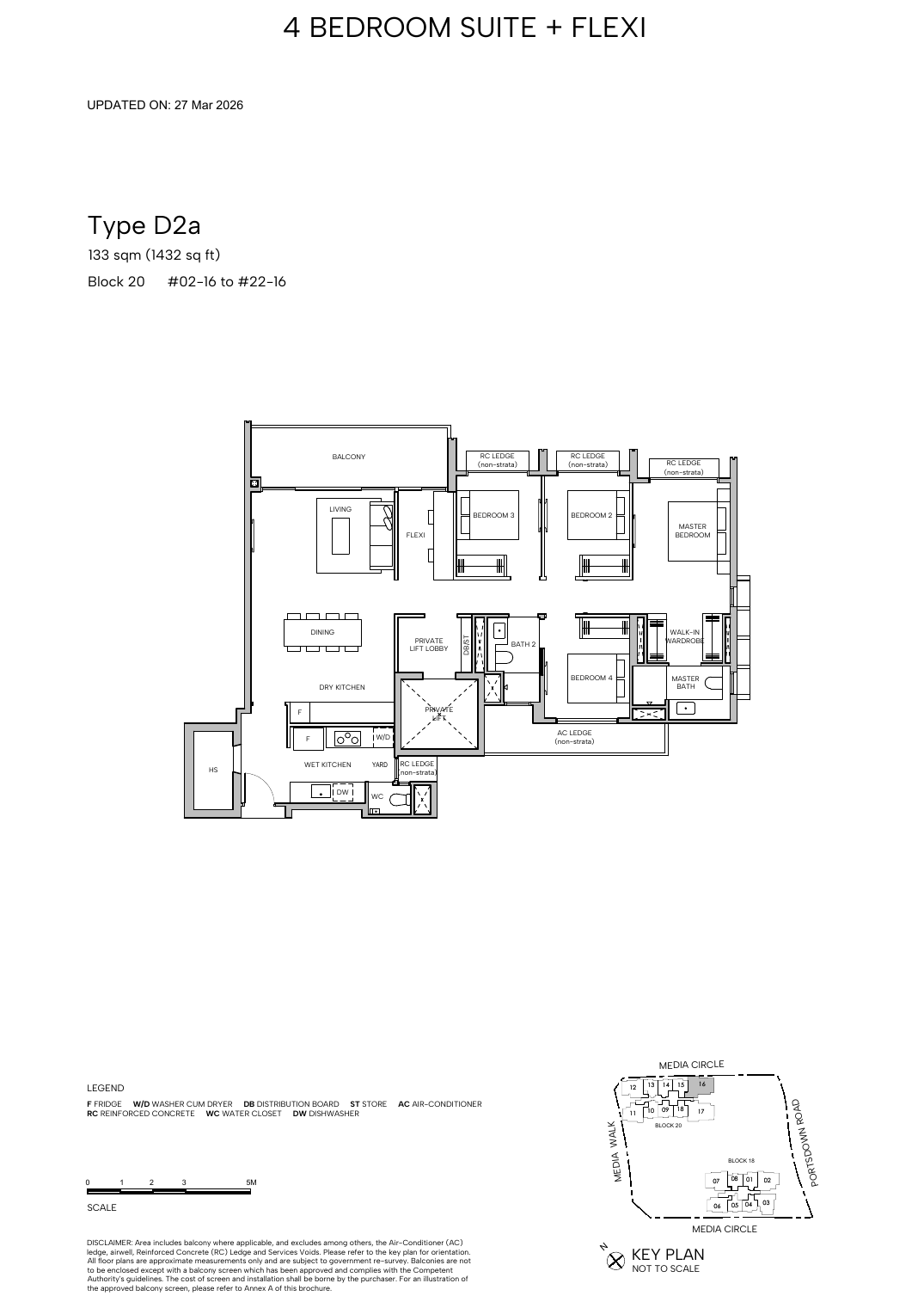

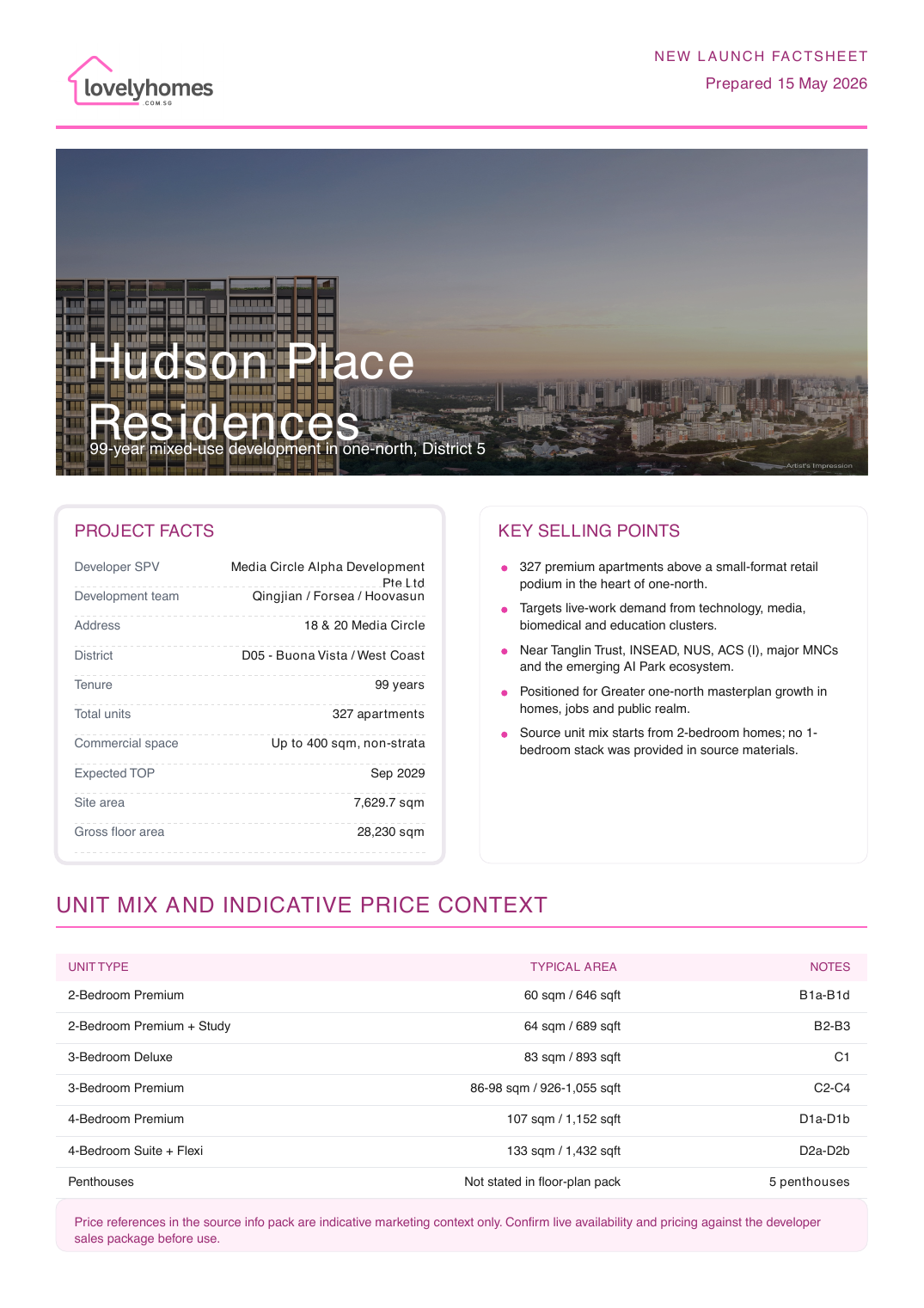

- New home sales rebounded to roughly 3,400 units in Q1 2026 — the strongest quarter since late 2022 — driven by launches including Hudson Place Residences and a pipeline of OCR projects attracting HDB upgraders.

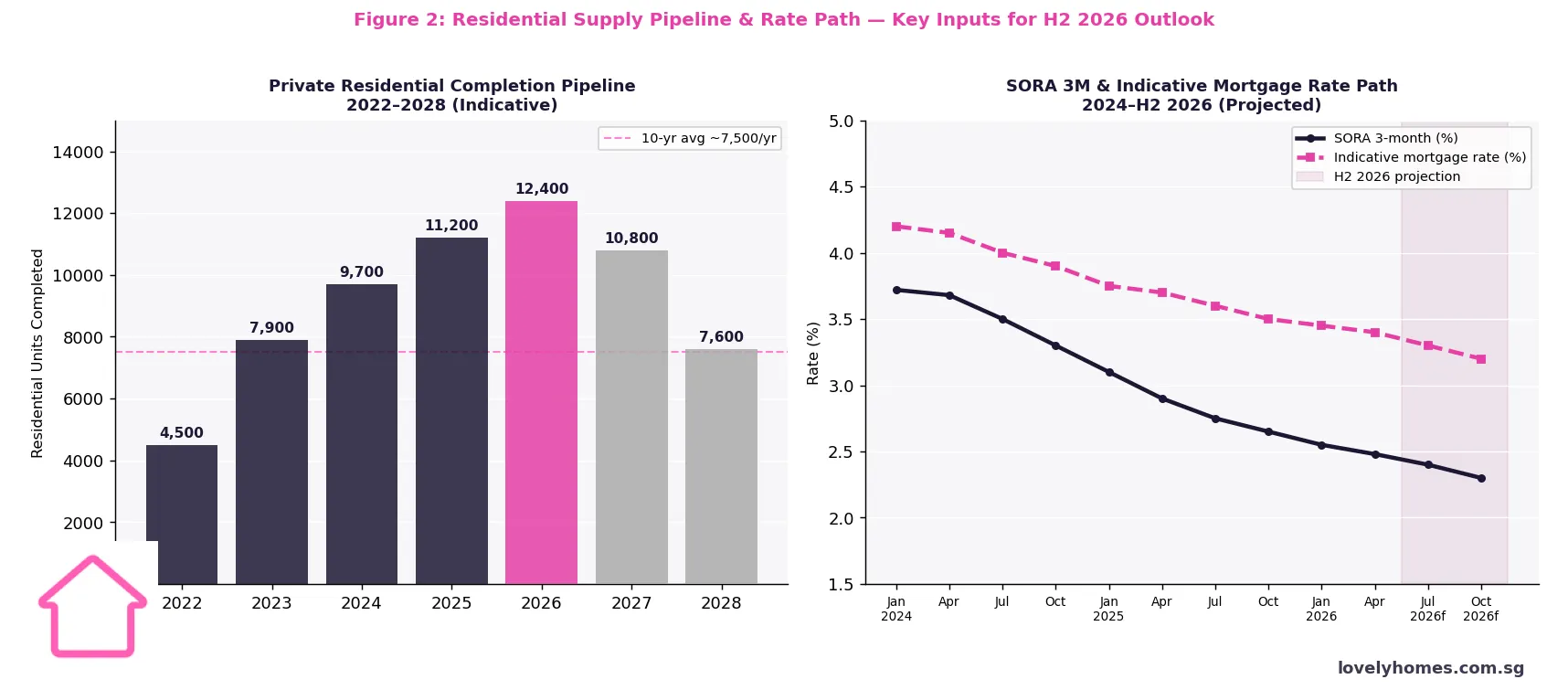

- Record supply wave: an estimated 12,400 private residential units are projected to complete in 2026, nearly 65% above the 10-year average. This is the largest single-year pipeline in over a decade.

- SORA 3-month has declined from a peak of ~3.72% in early 2024 to approximately 2.48% in April 2026, and is forecast to ease further to 2.30–2.40% by year-end as the US Federal Reserve continues its gradual easing cycle.

- The May 2026 EC cooling measures (raising the EC income ceiling to S$16,000 and extending EC MOP) may boost near-term EC demand but reduce second-hand private condo demand at the upgrader tier.

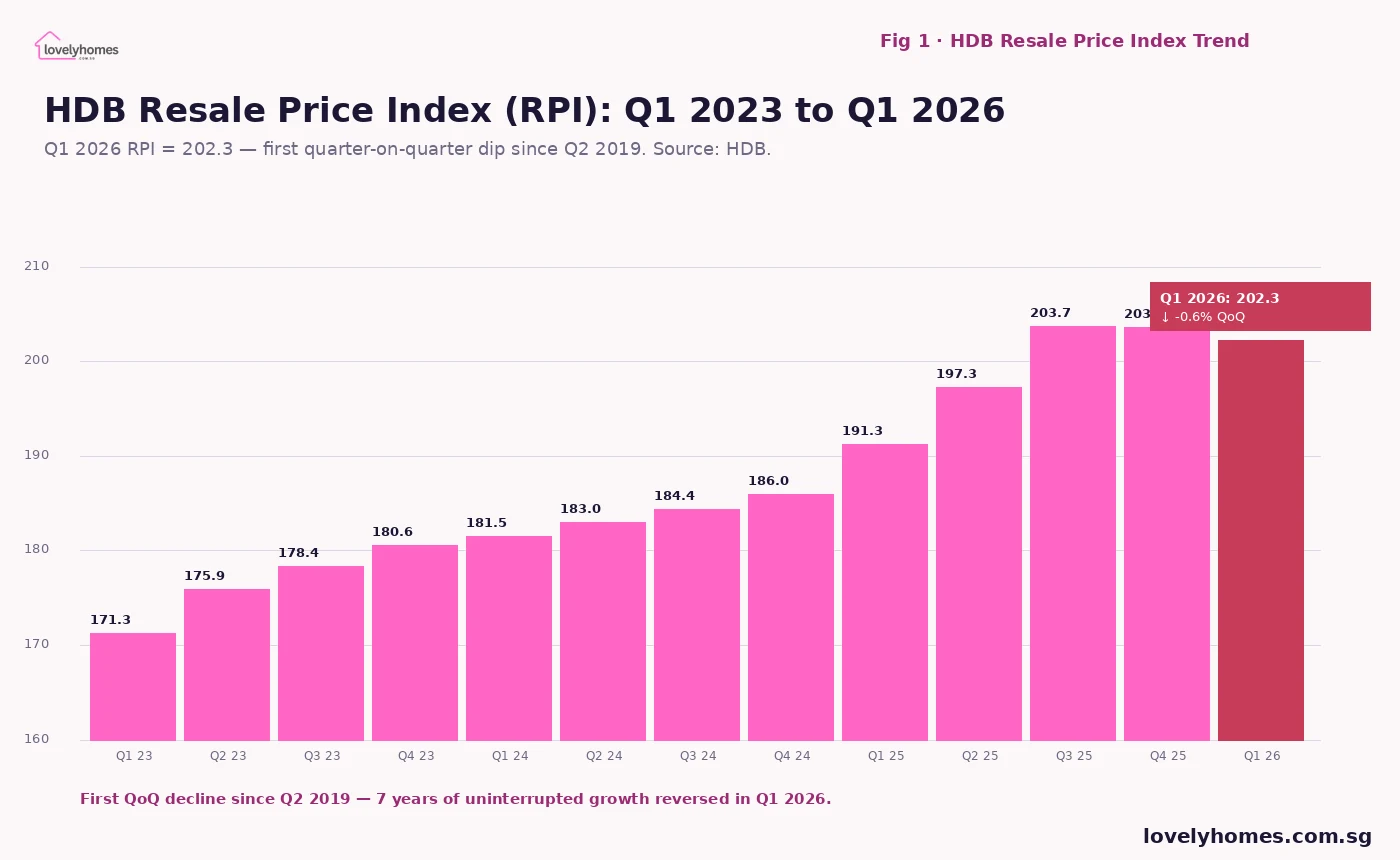

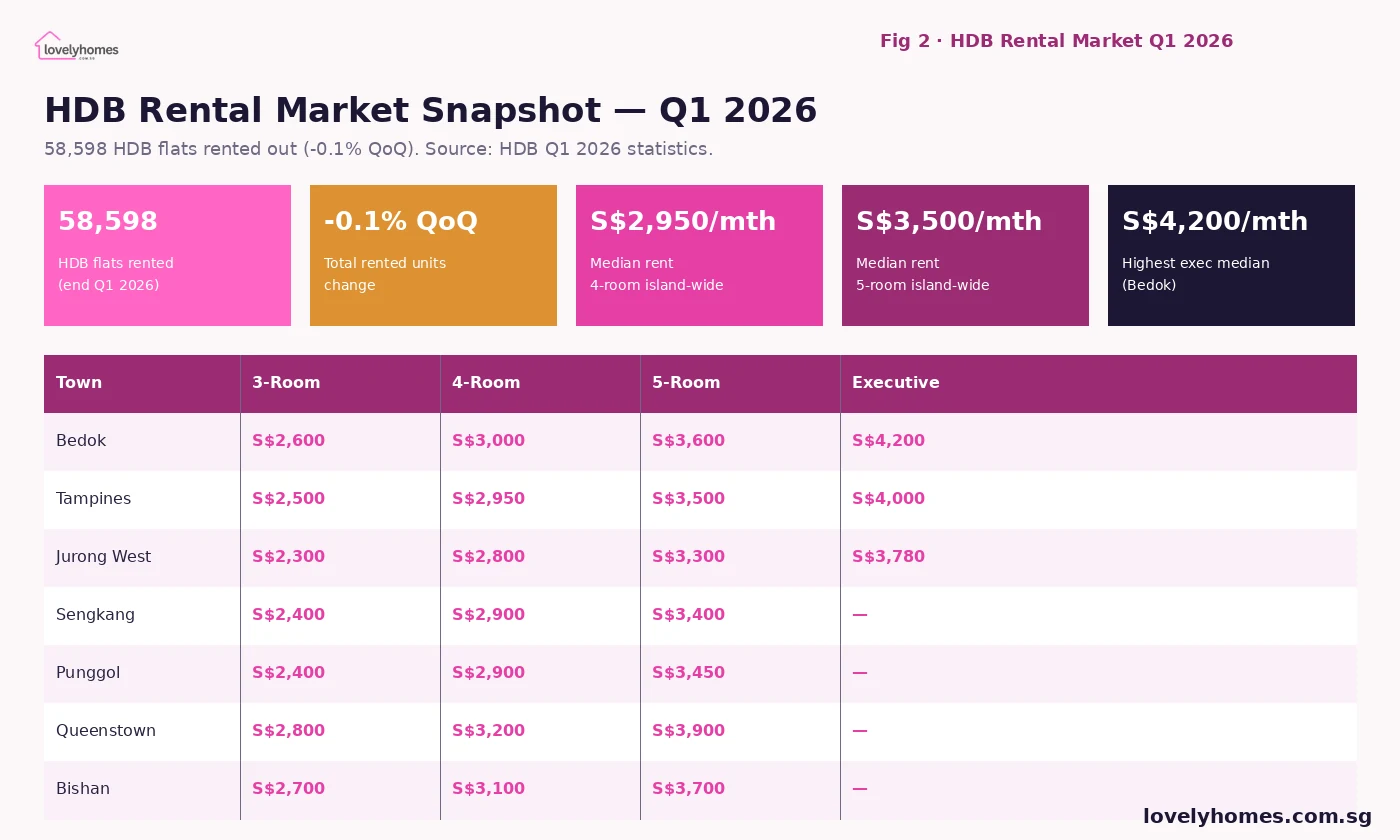

- The HDB resale market remains supported by the large MOP cohort (13,484 units in 2026) but faces price headwinds from higher supply and more stringent HDB Plus/Prime resale restrictions.

- Investment property outlook: continued compression of gross yields toward the mortgage rate makes leveraged residential investment increasingly return-dependent on capital appreciation rather than income.

- Key risk for H2 2026: any reversal of US Federal Reserve easing (e.g., re-acceleration of inflation) that pushes SORA back above 3% would materially increase holding costs and could trigger price corrections in the upper-OCR / RCR segments.

Where Singapore Property Stands at Mid-2026

Singapore’s private residential market enters the second half of 2026 in a state of controlled equilibrium. Prices are stable but not falling; transaction volumes have recovered from the 2023–2024 trough; and the government has maintained its full suite of demand-side cooling measures without any signal of relaxation. The Urban Redevelopment Authority (URA) Q1 2026 flash estimate (released 1 April 2026) showed the Private Residential Property Price Index up approximately 0.8–1.2% quarter-on-quarter — consistent with the 1.0–1.5% per-quarter trend observed since cooling measures were tightened in April 2023.

The headline stability, however, masks significant divergences by segment. Mass-market OCR condominiums have outperformed CCR and RCR on both price growth and transaction volumes, driven by HDB upgrader demand from the record MOP cohort documented in our guide to the HDB MOP Supply Bumper 2026. CCR properties, weighed by the 60% foreigner ABSD and a narrowing pool of domestic investors at current yields, have shown minimal price movement since 2023.

The Supply Wave: A Record 12,400 Completions in 2026

The single most consequential factor for the H2 2026 outlook is supply. As a result of the government’s aggressive Government Land Sales (GLS) programme from 2021 to 2023, an estimated 12,400 private residential units are slated for completion in 2026 — approximately 65% above the 10-year average of around 7,500 units per year. The pipeline remains elevated in 2027 at roughly 10,800 units before reverting toward average in 2028. This sustained supply injection is the primary mechanism the government is relying upon to contain price inflation without deploying further demand-side cooling measures.

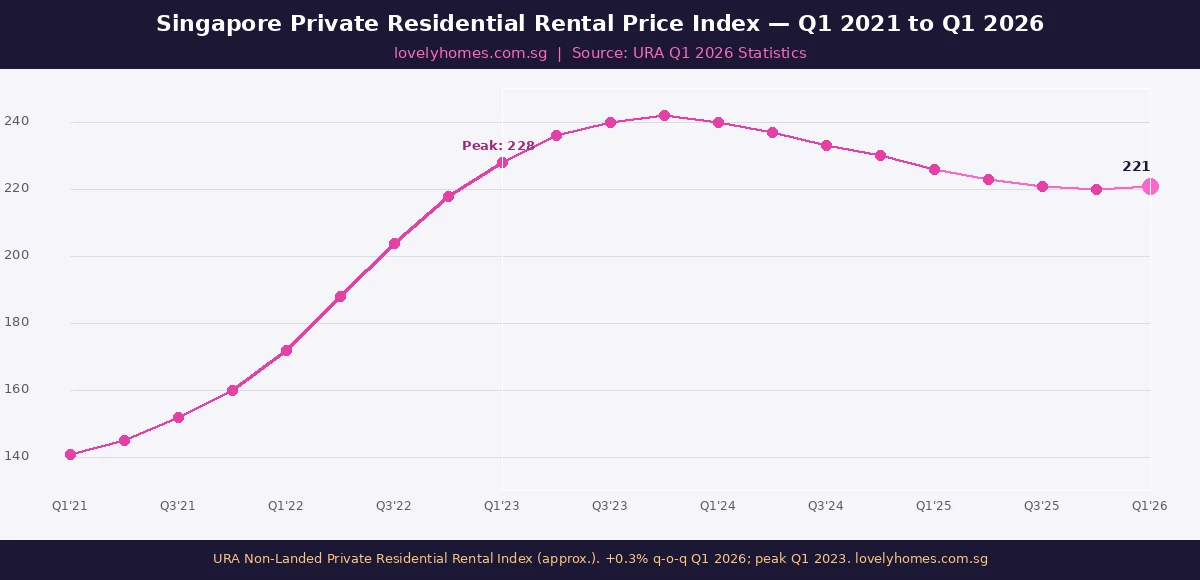

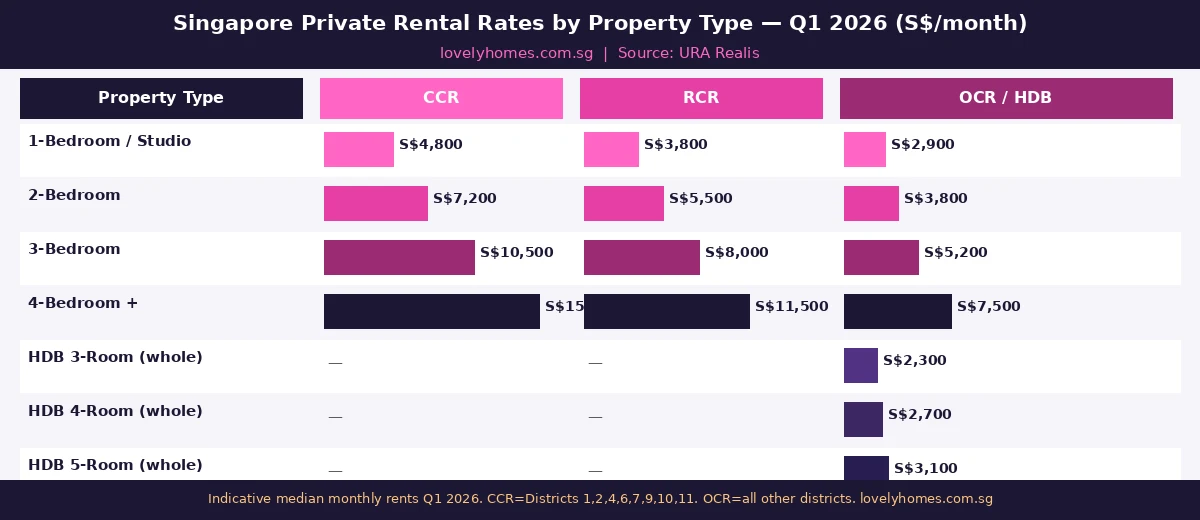

For renters and rental investors, the supply wave is already visible in the data. As reported in our analysis of the Singapore Private Rental Market Q1 2026, the URA non-landed rental index rose just 0.3% quarter-on-quarter in Q1 2026 — a near-plateau after three years of double-digit annual rental growth. CCR vacancy rates have risen above 10%, and RCR vacancy is approaching that level. OCR remains tighter at 7–9%, supported by HDB upgrader demand and expat families seeking suburban accommodation near international schools.

For owner-occupiers purchasing new launches in H2 2026, the supply wave is a neutral-to-positive factor: more choice, potentially more negotiating power on developer pricing, and a broader resale comparables base when they eventually sell. For investors relying on capital appreciation, the supply headwind is real — historically, periods of above-average residential completions in Singapore have correlated with softer PPI growth in the 12–24 months following peak supply.

The Rate Path: SORA Easing Creates Affordability Tailwind

The Singapore Overnight Rate Average (SORA) — the benchmark for most floating-rate home loans since the phase-out of SIBOR — has fallen from approximately 3.72% (3-month compounded) in early 2024 to around 2.48% as of May 2026. Most analysts project a further decline to 2.30–2.40% by end-2026, contingent on the US Federal Reserve executing two additional 25-basis-point cuts in the second half of the year.

For borrowers on SORA-pegged mortgages (the majority of floating-rate borrowers), this translates into indicative all-in mortgage rates declining from around 3.9–4.2% in early 2024 toward 3.2–3.4% by Q4 2026 — a reduction of roughly 60–80 basis points from peak. On a S$900,000 mortgage over 25 years, this corresponds to monthly instalment savings of approximately S$280–360, meaningfully improving affordability and reducing the cash-flow subsidy required for investment properties.

Borrowers considering whether to refinance or reprice in H2 2026 should weigh the remaining lock-in period and clawback provisions against the declining rate environment. With SORA continuing to ease, there is an argument for delaying a fixed-rate lock-in and remaining on SORA until rates stabilise.

EC Cooling Measures and the Upgrader Pipeline

The Ministry of National Development (MND) announced adjustments to Executive Condominium (EC) rules on 8 May 2026, raising the household income ceiling to S$16,000 (from S$14,000) and extending the EC resale MOP. Our analysis of the EC Cooling Measures May 2026 examined the demand implications in detail. The income ceiling increase is expected to draw some households who previously opted for private condos into the EC segment — a market segment that combines public housing pricing with private amenities — potentially softening demand for the lower end of the OCR private condo market in the S$1.3–1.8M range.

At the same time, the extended MOP for ECs means that the supply of EC units coming to the open market will be deferred — a modest support factor for OCR private prices in the medium term. The net effect on private condo prices is likely to be a modest negative for the S$1.3–1.8M tier but neutral for higher price points.

HDB Resale: Supported by MOP Wave, Restrained by Plus/Prime Rules

The HDB resale market has performed strongly in the first half of 2026, with transaction volumes elevated by the largest MOP cohort on record and the continued million-dollar flat phenomenon (with City Vue @ Henderson setting a S$1.728M record in April 2026). However, the introduction of the HDB Plus and Prime classification (effective from the February 2023 BTO exercise) introduces a structural change in the resale market that will become more visible from 2033 onwards: Plus and Prime flats, when they come to the open resale market, will face income-ceiling restrictions and (for Prime) Singapore-Citizen-only buyer eligibility, which may compress price discovery versus unrestricted Standard resale flats.

In the near term (H2 2026), the HDB resale market remains supported. Demand from buyers priced out of the private market, the continuing Proximity Housing Grant (PHG) of up to S$30,000, and a sustained supply of Standard-classified resale flats from the 2021 MOP cohort all point to stable transaction volumes at 25,000–27,000 transactions per year.

Summary Table: H2 2026 Market Segment Outlook

| Segment | Price Momentum | Volume Outlook | Key Drivers / Risks |

|---|---|---|---|

| OCR Private Condo | +1–2% pa | Stable–Up | HDB upgrader demand; supply headwind; EC competition |

| RCR Private Condo | +0.5–1% pa | Stable | Vacancy rising; SORA easing helps; limited new launches |

| CCR Private Condo | 0–0.5% pa | Flat–Down | 60% foreign ABSD; yield compression; investor retreat |

| HDB Resale | +2–4% pa | Up | Large MOP cohort; million-dollar segment active; grants support |

| Executive Condo (new) | +1–3% pa | Up | Income ceiling raised to S$16k; 2 EC sites in 1H GLS |

| Landed Residential | +1–2% pa | Stable | Citizen-only buying; tight supply; limited investment demand |

| Private Rental Market | –1–2% pa | Stable | Supply wave landing; vacancy rising; rent-to-income limits |

Worked Example: What Easing Rates Mean for a H2 2026 Purchaser

Consider a Singapore Citizen family (the Tans) looking to buy a S$1.4M 3-bedroom OCR condo in Q3 2026 as their first private residential property. They have S$350,000 in downpayment funds (25% of purchase price) and will borrow S$1,050,000 at an indicative floating rate of 3.30% per annum (SORA + spread, as at Q3 2026 projection).

- Monthly instalment: S$5,098 (S$1.05M over 25 years at 3.30% pa)

- TDSR check: household income required at 55% cap = S$9,269/month minimum; Tan family income S$14,000/month → TDSR 36.4% — passes comfortably.

- BSD: S$37,600 on S$1.4M (first S$180k × 1% + next S$180k × 2% + next S$640k × 3% + remaining S$400k × 4%)

- ABSD: Nil (first property for Singapore Citizens)

- Total cash at completion: Downpayment S$350,000 + BSD S$37,600 + legal fees ~S$4,500 = approximately S$392,100

Compared to an equivalent purchase in Q1 2024 (mortgage rate ~4.1%), the lower rate saves approximately S$350/month — S$105,000 over 25 years in interest, all else equal. The rate tailwind is meaningful for first-time buyers; for investors, it reduces but does not eliminate the negative cash-flow problem at current CCR and RCR yield levels.

What Might Come Next: Key Signals to Watch in H2 2026

Several catalysts could shift the H2 2026 outlook materially in either direction. On the upside, a larger-than-expected US Federal Reserve rate cut cycle could bring SORA below 2% and re-stimulate investor demand that has been dormant since 2022; the launch of major integrated developments (including Sim Lian’s Holland Plain dual-parcel project and potential launches in the Greater Southern Waterfront) could drive a new round of price discovery in the S$2,500–3,500 psf range; and continued strong employment growth in financial services and tech could sustain rental demand at the upper end of the market.

On the downside, a re-acceleration of US inflation forcing the Fed to pause or reverse easing (which occurred briefly in Q1 2024) would push SORA back toward 3% and materially worsen affordability; the record completion pipeline landing simultaneously with rising vacancy could depress rental rates below what investors have modelled; and any policy signal from the government that it is considering further demand-side measures (such as tightening the ABSD for Singapore Citizens on second properties above 20%) would immediately dampen transaction volumes.

The most likely base case for H2 2026 is a continuation of the current equilibrium: private residential prices flat-to-up 1–2% per annum in OCR and HDB resale, moderate transaction volumes, and a gradual improvement in affordability as SORA eases. This is not a bull market for property investors, but it is a stable environment for genuine owner-occupiers looking to buy well.

Frequently Asked Questions

Will Singapore property prices fall in H2 2026?

A broad price correction in Singapore residential property in H2 2026 is not the base-case outlook. The government has consistently demonstrated its willingness to deploy cooling measures to prevent sharp price increases but has not historically used them as a tool to drive prices down. The supply wave and moderating rents create headwinds, but the sustained demand from HDB upgraders and first-time private buyers, combined with easing interest rates, provides a floor. The most vulnerable segments to modest price softening are high-end CCR condominiums (where investment demand has retreated) and rental-heavy RCR units where vacancy is rising. Broad OCR and HDB resale prices are expected to remain stable to modestly positive.

Is now a good time to buy a private condo in Singapore?

For genuine owner-occupiers buying their first or only property, H2 2026 offers a reasonable entry environment: interest rates are declining from their 2023–2024 peak, there is more supply choice than at any time since 2014, and developers are offering more flexible payment schemes and occasional price adjustments on slower-moving units. For investors buying a second residential property (attracting 20% ABSD for Singapore Citizens), the break-even analysis is less compelling — the ABSD alone requires 7+ years of net rental income to recover at current yield levels. The Rental Yield vs Capital Gain guide provides a detailed worked example for investment property decision-making.

How does the 2026 GLS supply wave affect new launch prices?

The 1H 2026 GLS Confirmed List (released December 2025) provides for approximately 4,575 private residential units across nine confirmed sites — 50% above the 10-year average. Historically, a surge in land supply has tempered developer bids (land prices), which in turn constrains the launch prices developers can profitably offer. The Holland Plain Parcel B tender result — where Sim Lian was the sole bidder at S$1,491 psf ppr — illustrates this dynamic: even for a prime District 10 site, developers are bidding cautiously when the land pipeline is generous. This suggests new launch prices in H2 2026 are unlikely to see the sharp upside surprises seen during the 2021–2022 supply drought period.

What is the rental market outlook for H2 2026?

Singapore’s private rental market is transitioning from a supply-deficit landlord’s market (2020–2023) toward a more balanced market as the completion pipeline lands. The URA non-landed rental index — which rose approximately 50% cumulatively between 2020 and 2023 — has essentially plateaued since Q3 2024. In H2 2026, the accelerating supply wave (12,400 completions projected for full year) is expected to increase vacancy further in CCR and RCR and keep rental growth near zero or mildly negative across most segments. OCR and HDB remain tighter, supported by the HDB upgrader cohort — families who have sold their HDB flat but are waiting for their new private purchase to complete often rent in the interim.

Should I lock in a fixed-rate mortgage now or wait for SORA to fall further?

The answer depends on your risk profile and how much further you expect SORA to fall. With SORA at approximately 2.48% (May 2026) and projected at 2.30–2.40% by year-end, most fixed-rate packages are currently priced at 3.0–3.3% per annum for a 2-year lock-in — which does not represent a compelling premium over a SORA-pegged floating package (currently 3.0–3.5% depending on the spread). If you believe SORA will fall below 2% within 12–18 months (which would require aggressive Fed easing), staying on a floating rate makes sense. If you prioritise payment certainty and are concerned about upside rate surprises, a 2-year fixed package at 3.0–3.2% provides a reasonable hedge. The Refinancing Singapore 2026 guide walks through the break-even analysis.

What are the biggest risks to Singapore property in H2 2026?

The three principal risks to the Singapore property outlook in H2 2026 are: (1) a re-acceleration of US inflation forcing the Federal Reserve to maintain or raise rates, which would push SORA back toward 3% and significantly worsen affordability for mortgaged households; (2) a sharper-than-expected vacancy increase in the private rental market causing rental income to fall below what investors have underwritten, triggering some forced selling; and (3) an unexpected government policy tightening — such as an increase in the ABSD for Singapore Citizens on second residential properties above the current 20%. None of these is the base case, but all are plausible tail risks that property investors should model into their downside scenarios.

How does the HDB Plus/Prime classification affect the resale market outlook?

In the near term (2026–2032), the impact is limited — the first Plus and Prime cohorts from the February 2023 BTO exercise will not MOP until around 2033. From 2033 onwards, however, the structural change becomes significant: Plus and Prime resale flats will only be buyable by income-ceiling-eligible households, and Prime resale flats are restricted to Singapore Citizens only. This narrows the effective buyer pool relative to unrestricted Standard resale flats. Property investors or upgraders holding Standard resale flats will be in a structurally stronger position than those whose eventual exit is via a Plus or Prime resale — a point that is often overlooked in discussions of the RFC framework’s impact on resale market dynamics.

Related Articles

- Singapore Developer Sales April 2026

- EC Cooling Measures May 2026

- HDB MOP Supply Bumper 2026

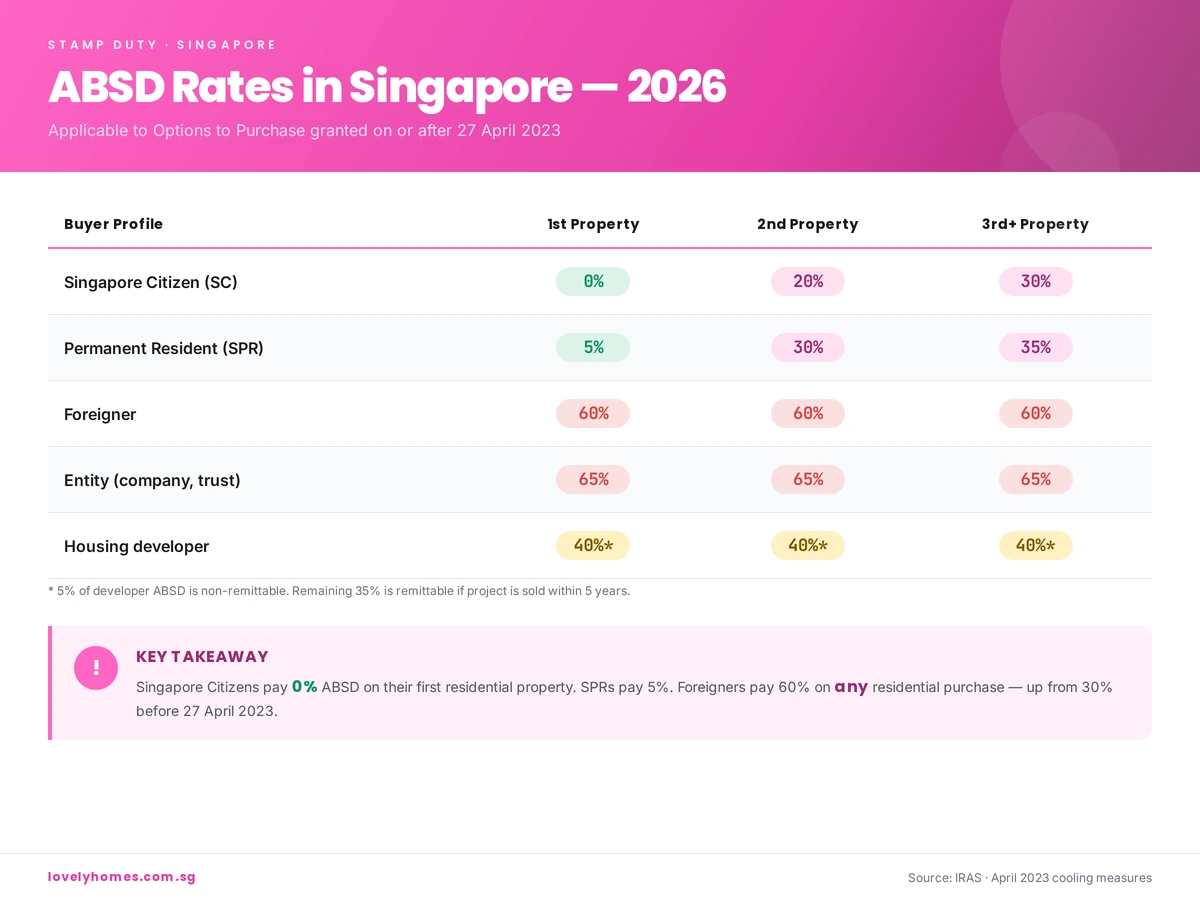

- ABSD Singapore 2026 — Complete Guide

- Singapore Private Rental Market Q1 2026

- Rental Yield vs Capital Gain Singapore 2026

- HDB Resale Market Q1 2026

Disclaimer

This article is a market analysis and commentary for informational purposes only. It does not constitute financial advice, investment advice, or a solicitation to buy or sell any property or financial instrument. All price indices, transaction volumes, SORA projections, and market forecasts are editorial estimates based on publicly available data from URA, HDB, and MAS, and are subject to significant uncertainty. Past market performance is not indicative of future results. Consult a licensed financial adviser and property professional before making any investment or purchase decision.

Tags: Singapore Property Market 2026, Property Outlook H2 2026, Singapore Real Estate Analysis, Private Residential Price Index, SORA Rate Path 2026, HDB Resale Market, GLS Supply Pipeline, Property Investment Singapore, Market Trends 2026, Singapore Condo Prices