Quick Answer — Home Insurance Singapore 2026 in 60 Seconds

HDB Fire Insurance: mandatory if you have an outstanding HDB loan; ~S$5/yr via HDB/Etiqa; covers structure, not contents

Home Contents Insurance: optional but strongly recommended; ~S$100–S$400/yr; covers furniture, renovations, appliances, valuables

Home Protection Plan (HPP): mandatory mortgage insurance for HDB loans, paid via CPF; discharges loan if owner dies or suffers total permanent disability

Private condo owners: building insurance is managed by the Management Corporation Strata Title (MCST); you need your own contents coverage

Common claim scenarios: water damage from burst pipes (most frequent), fire damage, theft, accidental breakage

Premium sweet spot: a S$80,000 sum-insured contents policy for a 4-room HDB costs approximately S$165–S$210 per year

Do not confuse: fire insurance ≠ home contents insurance ≠ HPP — they cover entirely different risks

Most Singapore homeowners assume they are fully covered once they buy fire insurance and sign up for the Home Protection Plan. In reality, standard HDB fire insurance covers only the shell of the flat — the walls, floors, ceilings, and fittings that HDB installed. The sofa you bought from IKEA, the custom kitchen carpentry, the television, the washing machine, and your children’s laptops are all entirely outside its scope. This guide walks you through all three layers of home insurance that every Singapore homeowner should understand in 2026, who administers each, what it costs, and how to structure your coverage without over-insuring.

The Three Layers of Singapore Home Insurance

Singapore’s home insurance landscape comprises three distinct products that most homeowners need to understand, even if they do not buy all three. Each is administered by a different body, covers a different risk, and carries a different cost structure.

Figure 1: Singapore home insurance — three key coverage types and approximate annual premiums. Sources: HDB, CPF Board, SingSaver, MoneySmart (2026).

HDB Fire Insurance — What It Is and Why It Falls Short

The HDB Fire Insurance Scheme, administered by HDB and currently underwritten by Etiqa Insurance Pte Ltd, is mandatory for all HDB flat owners with an outstanding HDB loan that commenced on or after 1 September 1994. The scheme is renewed every five years and costs approximately S$4.50–S$7.50 per year depending on flat type — widely regarded as the most affordable insurance product in Singapore.

What it covers is specifically defined by HDB: the cost of reinstating the physical structure of the flat, HDB-installed internal fittings, and any items that form part of the flat as originally constructed. This means walls, ceilings, floors, doors, window frames, electrical wiring, and sanitary fittings are covered. What it explicitly does NOT cover: renovations you have carried out after purchase, any furniture, appliances, electronics, clothing, valuables, or personal belongings. For most Singaporean households, where renovation costs alone can run S$40,000–S$80,000 for a 4-room flat, this is a significant gap.

Flat owners who have fully paid off their HDB loan are not required to maintain fire insurance, though HDB recommends it as basic prudence. Private property owners — condominiums and landed houses — are not covered by the HDB scheme at all.

Home Contents Insurance — The Essential Add-On

Home contents insurance is the product that fills the gap between what the HDB fire insurance covers and what you actually own inside your flat. It is entirely optional but strongly recommended by the Monetary Authority of Singapore (MAS) and the CPF Board. A standard home contents policy for a Singapore HDB flat covers furniture, appliances, electronics, clothing, jewellery (up to a sub-limit), cash, and improvements or renovations made by the owner. Most policies also include a liability component — if a visitor trips over your rug and sues you, the policy responds.

Figure 2: Singapore home insurance — what each policy covers. Sources: HDB, CPF Board, NTUC Income, MSIG, AXA (2026 policy documents).

The annual premium for home contents insurance varies with the sum insured, flat type, and optional add-ons. As a practical benchmark, a sum insured of S$80,000 for a standard 4-room HDB flat will cost approximately S$165–S$210 per year depending on the provider. Adding optional extras — such as worldwide personal accident cover, alternative accommodation reimbursement (if your flat is uninhabitable post-damage), or enhanced jewellery sub-limits — typically adds S$30–S$60 to the annual premium. The most common claims on home contents policies in Singapore are water damage from burst pipes or flooding from upstairs neighbours, accidental damage to electronics, and minor theft.

Premium Comparison — Home Contents Insurance Providers 2026

Figure 3: Indicative home contents insurance annual premiums for S$80,000 sum insured, standard HDB 4-room flat (2026). Premiums are indicative — verify directly with each insurer before purchase. Sources: SingSaver, MoneySmart, insurer websites (May 2026).

Home Protection Plan (HPP) — Mortgage Insurance for HDB Owners

The Home Protection Plan (HPP) is administered by the CPF Board and is mandatory for all Singapore Citizens and Permanent Residents who use their CPF Ordinary Account (OA) savings to service an HDB housing loan. The HPP is a reducing-term insurance policy that mirrors your outstanding HDB loan balance — if you die, or suffer total permanent disability (TPD) before your loan is fully repaid, the HPP pays off the outstanding balance so your family retains the flat without the burden of a mortgage.

Unlike fire insurance and contents insurance, HPP premiums are paid directly from your CPF OA, not from cash. This makes the HPP effectively invisible to most homeowners day-to-day. Premiums vary by age at entry, coverage percentage, and outstanding loan amount — a 35-year-old covering 100% of an S$400,000 outstanding loan might pay approximately S$250–S$350 per year in CPF, while a 45-year-old covering the same loan would pay more due to higher mortality risk. The CPF Board publishes an online HPP premium calculator at cpf.gov.sg.

HDB loan borrowers who choose to opt out of the HPP (which is permissible under certain conditions, such as having a private life insurance or Mortgage Reducing Term Assurance with equivalent coverage) must satisfy the CPF Board that alternative coverage is in place.

Home Insurance for Private Property Owners

Condominium owners and landed property owners in Singapore face a different insurance landscape from HDB flat owners. For strata-titled condominiums, the Management Corporation Strata Title (MCST) is legally required under the Building Maintenance and Strata Management Act (BMSMA) to maintain building insurance covering the common property and the original structure of individual units. This means the concrete walls, slab floors, and structural elements of your condo unit are insured at the development level. Your own contents, renovations, and fixtures that you have installed are not.

Condo owners should therefore purchase a standalone home contents policy — available from the same suite of providers (NTUC Income, MSIG, AXA, Etiqa, AIG, OCBC, DBS) — and are advised to include a renovation replacement rider that matches their actual renovation expenditure. For a private condo with S$150,000 in renovation and S$100,000 in furnishings and appliances, a contents policy covering S$250,000 sum insured would cost approximately S$300–S$450 per year. Landed property owners (terrace houses, semi-detached, detached) need separate building insurance as there is no MCST to manage this — comprehensive home policies from providers such as NTUC Income’s Enhanced Home plan cover both structure and contents under a single policy.

Summary — Which Policies Do You Need?

Property Type

Fire Insurance

Contents Insurance

HPP / Mortgage Cover

Building Insurance

HDB flat (HDB loan outstanding)

Mandatory (Etiqa/HDB)

Optional but recommended

Mandatory (CPF HPP)

N/A — covered by HDB

HDB flat (loan paid off)

Optional (strongly recommended)

Optional but recommended

N/A

N/A — covered by HDB

Private condo

N/A

Required (own contents)

Private MRTA or life policy recommended

MCST handles structure

Landed property (own)

N/A

Included in comprehensive home policy

Private MRTA or life policy recommended

Required — owner’s responsibility

Rented flat / room

N/A (landlord’s responsibility)

Tenant’s contents policy (optional)

N/A

N/A (owner’s responsibility)

Worked Example — Calculating the Right Coverage for an HDB 4-Room Owner

Mdm Priya, 38, Singapore Citizen, owns a 4-room HDB flat in Ang Mo Kio which she purchased in 2021 for S$580,000 using an HDB loan. Outstanding HDB loan as at May 2026: S$370,000. Renovation cost at purchase: S$48,000. Current value of furniture and appliances: approximately S$35,000. Electronics (3 laptops, 2 televisions, home theatre): approximately S$12,000. Personal valuables (jewellery, watches): approximately S$8,000.

Step 1 — Fire Insurance: Mandatory since she has an outstanding HDB loan. Cost: ~S$5/yr via Etiqa. Already enrolled.

Step 2 — Home Contents: Sum insured should cover renovations (S$48,000) + furnishings (S$35,000) + electronics (S$12,000) + a partial allowance for valuables (S$8,000, subject to sub-limits) = S$103,000 recommended sum insured. Selecting NTUC Income Enhanced Home at S$100,000 sum insured costs approximately S$195/yr. Adding a home contents liability extension (S$250,000 third-party liability): +S$20/yr. Total: ~S$215/yr.

Step 3 — HPP: CPF Board auto-deducts HPP premium from Mdm Priya’s CPF OA at ~S$260/yr at her age and loan balance. She is already enrolled.

Total annual outlay: S$5 (fire) + S$215 (contents) + S$260 (HPP, from CPF) = S$480/yr or S$40/month for comprehensive coverage of a S$580,000 property and S$103,000 in contents. This represents 0.083% of the property value per year — among the most cost-effective forms of financial protection available to any Singapore homeowner.

Why Home Insurance Matters More Than Most Singaporeans Think

The General Insurance Association of Singapore (GIA) reports that home insurance penetration in Singapore remains below 40% for contents coverage — meaning more than half of Singapore homeowners have no protection against the loss of their household belongings. This is a structural gap that becomes painfully apparent in the event of a water damage incident (Singapore’s most common home insurance claim type, often caused by burst pipes in ageing HDB stock or flooding from an upstairs neighbour) or a kitchen fire. A single kitchen fire can result in S$20,000–S$50,000 in damage to the affected flat, of which the HDB fire insurance might cover only the reinstated fixtures — the custom cabinetry, hob, hood, and appliances that the owner installed after purchase are entirely on the owner’s account.

For property investors, the economics are even clearer. A landlord who has invested S$1.2 million in a private condo and spent S$80,000 on renovation should be spending less than S$400/yr on contents insurance to protect that investment. The alternative — self-insuring against fire, flood, theft, or water damage — is a material unhedged exposure that most financial advisers would classify as imprudent for a leveraged property portfolio.

What Might Change

The home insurance market in Singapore is competitive but evolving. MAS has been encouraging greater take-up of contents and comprehensive home policies through its MoneySense financial literacy programme. There has been industry discussion about whether the HDB Fire Insurance Scheme’s sum insured (which has not been substantially revised since 2014) should be updated to reflect rising reinstatement costs — an S$800 per square metre assumption for a 5-room flat, for instance, may no longer reflect the actual cost of reinstating a modern flat with high-grade finishes. HDB has not yet announced a revision to the scheme’s structure, but any update to the sum insured or premium would represent a positive development for flat owners currently relying on the scheme as their primary coverage.

Frequently Asked Questions — Home Insurance Singapore 2026

Is home insurance mandatory in Singapore?

The HDB Fire Insurance Scheme is mandatory for all HDB flat owners with an outstanding HDB loan that started on or after 1 September 1994. The Home Protection Plan (HPP) is mandatory for all CPF members using CPF OA savings to repay an HDB housing loan. Home contents insurance is not mandatory for any property type — it is optional but strongly recommended. For private property owners, there is no statutory requirement for individual building or contents insurance (the MCST manages building insurance for condominiums), though most mortgage lenders require proof of building insurance for landed property.

What is the difference between HDB fire insurance and home contents insurance?

HDB fire insurance covers the reinstatement of the physical structure of your HDB flat — the walls, ceilings, floors, doors, windows, and fittings that HDB installed when the flat was first built. It is a narrow, structure-only policy that does not cover anything you have added since taking ownership. Home contents insurance, by contrast, covers everything inside the flat that you own — furniture, appliances, electronics, clothing, valuables, and most importantly, the renovations you have carried out (custom carpentry, kitchen works, flooring, false ceilings, etc.). The two policies are completely separate products from different providers with different scope and different pricing.

Do I need home insurance if I rent out my flat?

If you are an HDB flat owner subletting your entire flat or individual rooms, your fire insurance obligation as owner remains unchanged (you must still maintain it if you have an outstanding HDB loan). For contents left in the flat (furniture, appliances provided to tenants), it is prudent to maintain a landlord-specific contents policy — these are available from providers such as NTUC Income and MSIG at a modest additional premium over the standard residential policy. Your tenant, however, is personally responsible for insuring their own belongings — their contents are not covered by your policy. Tenants who are concerned about their personal property should purchase a separate renter’s insurance or home contents policy, which typically costs S$80–S$150 per year for a room or shared flat arrangement.

Does home contents insurance cover renovation costs?

Yes — most home contents insurance policies in Singapore include a renovation replacement rider as part of the base or as an add-on. This covers the cost of reinstating or replacing renovations you have installed — custom kitchen carpentry, flooring, false ceilings, built-in wardrobes, and similar works — in the event of a covered loss (fire, water damage, accidental damage). It is important to declare the actual renovation sum when taking out the policy; under-declaring the renovation value is a common mistake that leads to underinsurance and a proportionally reduced payout at claim time. The renovation sum insured should be updated whenever you undertake significant works.

Can I use CPF to pay for home contents insurance?

No. Home contents insurance premiums must be paid in cash or by GIRO. CPF cannot be used to pay for any type of home insurance except the Home Protection Plan (HPP), whose premiums are deducted directly from the CPF Ordinary Account by the CPF Board. Fire insurance premiums under the HDB scheme are also paid in cash (typically via GIRO or internet banking). This is a common point of confusion — while CPF can be used extensively for the property purchase itself (down payment, BSD, monthly loan instalments), it cannot be used for insurance premiums other than HPP.

What happens to my home insurance if I sell my HDB flat?

The HDB Fire Insurance Scheme is tied to the flat (not the owner) and lapses upon sale or transfer of the flat — you do not need to formally cancel it, as it will not be renewed by the new owner’s HDB loan cycle. The HPP lapses when the CPF loan is fully discharged. Home contents insurance is a separate policy that you take out in your personal name — you should formally cancel it upon completion of the sale (your insurer will pro-rate any unused premium for refund). When purchasing your new property, you will need to arrange new policies appropriate to the new property type and your new loan arrangement. The CPF Board website and HDB’s My HDBPage both have guidance on reviewing insurance obligations when transacting.

Disclaimer: This article is provided for general information purposes only and does not constitute financial, insurance, legal, or property advice. Insurance product details, premium estimates, and policy terms referenced are indicative and based on publicly available information from the Housing and Development Board (HDB), CPF Board, Monetary Authority of Singapore (MAS), and insurer websites as at 18 May 2026, and may change without notice. Premium figures in Figure 3 are indicative illustrations only — actual premiums will vary based on individual circumstances, sum insured, add-ons, and insurer assessment. Readers should obtain formal quotations directly from licensed insurers and seek advice from a MAS-licensed financial adviser before purchasing any insurance product. LovelyHomes.com.sg does not endorse any specific insurer or insurance product.

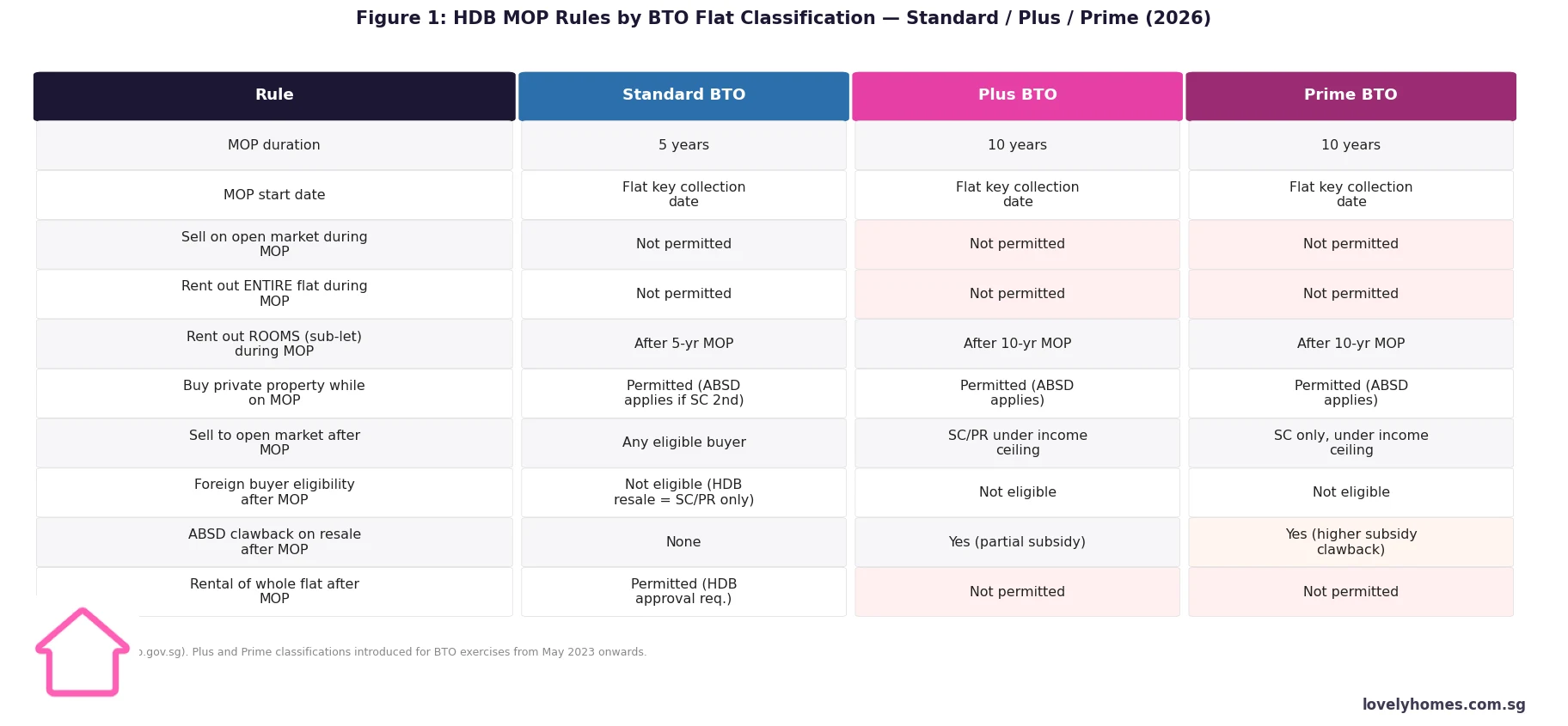

The HDB Minimum Occupation Period (MOP) is the mandatory period you must physically occupy your HDB flat before you can sell it on the open market, rent out the entire flat, or purchase a second private residential property without incurring the full ABSD burden. MOP is administered by HDB (Housing and Development Board).

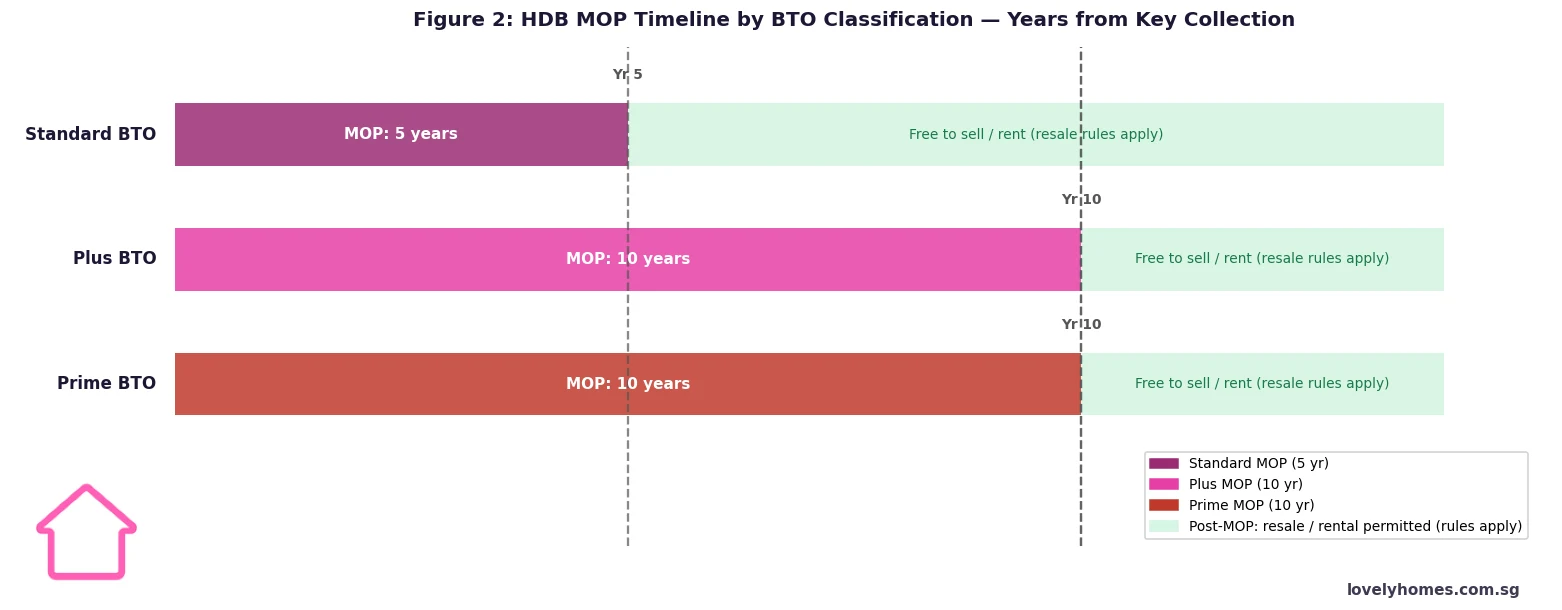

For Standard BTO flats, the MOP is 5 years from the date of key collection. For Plus and Prime BTO flats (introduced for BTO exercises from May 2023), the MOP is 10 years.

During the MOP, you cannot sell the flat, rent out the entire unit, or transfer ownership. You can, however, rent out individual rooms with HDB approval, and you may purchase private property (subject to ABSD).

After the MOP, Standard flat owners may sell to any eligible HDB buyer (SC or SPR). Plus flat owners must sell to SC or SPR buyers whose household income is within the prevailing income ceiling. Prime flat owners may only sell to Singapore Citizens whose household income is within the income ceiling.

Whole-flat rental after MOP is permitted for Standard flats (subject to HDB approval). It is not permitted at any time for Plus or Prime flats.

A subsidy clawback applies when Plus and Prime flats are sold on the open market — HDB recovers a portion of the housing grant and pricing subsidy. The clawback amount is higher for Prime flats.

The MOP clock starts from the date of key collection — not the date of BTO application, booking fee payment, or Temporary Occupation Permit (TOP). A flat collected in June 2024 has its Standard MOP expiry in June 2029.

What Is the MOP and Who Administers It?

The Minimum Occupation Period (MOP) is a statutory requirement under the Housing and Development Act, administered by the Housing and Development Board (HDB). It requires owners of HDB flats to physically occupy their flat for a minimum period before certain rights become available — primarily the right to sell on the open market, rent out the entire unit, or purchase a second private residential property.

The MOP exists for two complementary policy reasons. First, it ensures that subsidised HDB flats are used as genuine owner-occupied homes rather than short-term investment instruments. Second, it moderates the supply of resale HDB flats that enter the market at any one time, which helps to stabilise resale prices. The requirement has been part of Singapore’s public housing policy for decades, and HDB enforces it through its ownership records, which are cross-referenced against the buyer’s NRIC address for SC/SPR buyers.

Figure 1: HDB MOP Rules by BTO Classification — Standard, Plus and Prime (2026) | Source: HDB

Standard, Plus and Prime: The Three BTO Classifications

From the May 2023 BTO exercise onwards, HDB classifies all new BTO flats into one of three tiers based on location and subsidy level. This classification directly determines MOP length, post-MOP resale eligibility, rental rights, and subsidy clawback:

Standard flats are located in non-central, typically suburban estates (such as Tengah, Woodlands, Sembawang, and Punggol). They carry the lowest subsidies relative to market value and have the most permissive rules: 5-year MOP, resale to any eligible SC/SPR buyer, and whole-flat rental allowed after MOP with HDB approval.

Plus flats are located near transport nodes or commercial hubs, in estates that would otherwise be too pricey for first-timer buyers without additional subsidy. They come with a 10-year MOP, resale restricted to SC/SPR buyers within the prevailing income ceiling, and no whole-flat rental at any time.

Prime flats are located in the choicest sites — city-fringe, waterfront, or mature central estates like Kallang, Toa Payoh, and Marina South — where HDB provides the heaviest subsidies. They carry a 10-year MOP, SC-only resale (SPR buyers are ineligible), income ceiling restrictions, no whole-flat rental at any time, and the highest clawback rate.

Buyers are told which classification a flat falls under at the time of BTO application. The classification is permanently attached to the flat and does not change over time, even after resale. A Prime flat remains a Prime flat in every subsequent transaction.

Figure 2: HDB MOP Timeline by BTO Classification — Years from Key Collection (Singapore 2026)

What You Can and Cannot Do During the MOP

The MOP does not mean you are locked away from all activity — it specifically restricts disposal and whole-unit rental. The table below summarises key permitted and prohibited actions:

Activity

During MOP

After MOP (Standard)

After MOP (Plus/Prime)

Sell flat on open market

Not permitted

Permitted (SC/SPR buyers)

SC/PR (Plus); SC only (Prime); income ceiling applies

Rent out entire flat

Not permitted

Permitted (HDB approval)

Not permitted (ever)

Rent out rooms (sub-let)

Not permitted during MOP

Permitted (HDB approval)

Permitted (HDB approval)

Buy private property

Permitted (ABSD applies if SC 2nd property: 20%)

Permitted

Permitted

Transfer ownership (gift / divorce / death)

HDB approval case-by-case

Yes

Yes (subject to Plus/Prime resale rules)

Renovate / alter the flat

Permitted (HDB renovation permit)

Permitted

Permitted

Buying Private Property During the MOP

One of the most common questions from HDB flat owners is whether they can buy a private condominium before their MOP is up. The answer is yes — you are allowed to purchase private residential property in Singapore while your MOP is running. However, there are important financial consequences to consider.

If you are a Singapore Citizen owning an HDB flat (which counts as your first residential property) and you buy a private condo during the MOP, you are buying a second property. This means you pay 20% ABSD on the private property purchase. If you are an SPR, your second-property ABSD is 30%. The HDB flat itself remains subject to the MOP and cannot be sold until the MOP expires.

This means you will be servicing two housing loans simultaneously until the HDB can be sold — which requires careful TDSR planning. The TDSR cap of 55% applies across all outstanding loans. HDB loans (from HDB directly) and bank loans on HDB flats are both counted in TDSR. If the combined debt servicing ratio exceeds 55% when adding the private mortgage, financing for the private property may be declined.

What Happens When You Sell After the MOP

Once the MOP is fulfilled, the key restrictions are lifted — but resale rules still apply, especially for Plus and Prime flats:

Standard flats: May be sold to any eligible HDB resale buyer — SC or SPR, subject to standard HDB eligibility criteria (Ethnic Integration Policy quotas, family nucleus requirements, etc.). No income ceiling on the buyer.

Plus flats: May only be sold to buyers whose household income does not exceed the prevailing income ceiling (currently S$14,000/month for families, S$7,000 for singles). SPR buyers are eligible. A subsidy clawback is deducted from the sale proceeds on the first open-market resale.

Prime flats: May only be sold to Singapore Citizen buyers (SPR buyers are not eligible) whose household income does not exceed the income ceiling. The subsidy clawback rate is higher than for Plus flats and is also deducted from the first open-market resale proceeds.

The subsidy clawback is calculated as a percentage of the resale price (or market value, whichever is higher) and is paid to HDB at the point of resale. HDB has not publicly released a fixed clawback percentage table; the exact rate is determined and communicated at the time of application. This is intended to recover some of the subsidy advantage enjoyed by Plus/Prime buyers while still allowing them a fair profit on genuine capital appreciation.

The MOP and CPF Accrued Interest

When you sell an HDB flat after the MOP, any CPF funds used to purchase the flat (including the option fee, downpayment, and monthly mortgage instalments paid from your CPF Ordinary Account) must be refunded to your CPF accounts — along with accrued interest at the CPF OA interest rate (currently 2.5% per annum). This accrued interest represents what your CPF savings would have earned had they not been used for housing. On a long MOP (10 years), accrued interest can be substantial and reduces the net cash proceeds from the sale.

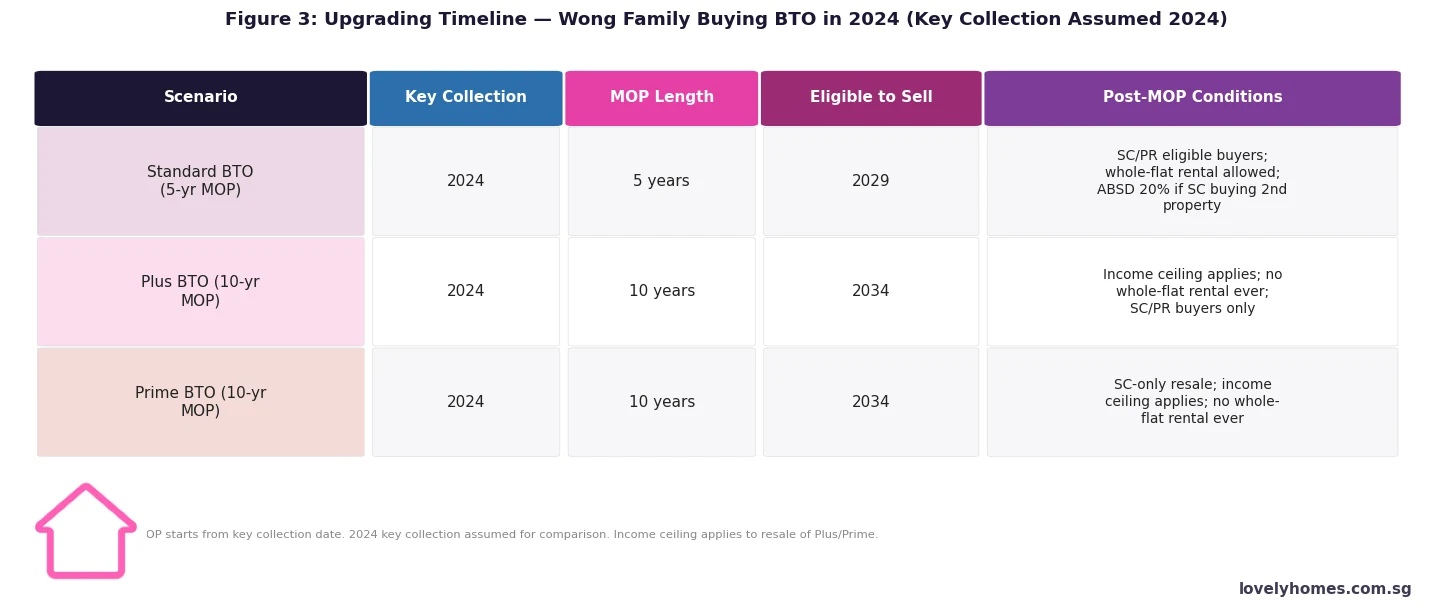

Worked Example: The Wong Family and the MOP Decision

Mr and Mrs Wong, both Singapore Citizens, purchase a 4-room BTO flat in Bishan (classified as a Plus flat) in June 2024. Key collection is in June 2024. Their household income is S$9,000/month. The purchase price is S$550,000.

Over the 10-year MOP, if the flat appreciates from S$550,000 to S$800,000 (a not unreasonable assumption for a Plus-classified Bishan flat), the Wongs would make a nominal gross gain of S$250,000. From this, HDB deducts the clawback (amount TBD at point of sale), plus CPF refund with accrued interest. On a S$550,000 purchase with 25% CPF downpayment (S$137,500) at 2.5% CPF OA rate over 10 years, accrued interest alone would be approximately S$38,700 — reducing net cash-in-hand from the sale. This is still a solid return, but buyers should model it carefully before factoring in the Plus flat subsidy as pure profit.

What This Means for HDB Buyers in 2026

The 10-year MOP for Plus and Prime flats is a significant commitment. A buyer collecting keys in 2026 cannot sell their Plus or Prime flat until 2036 at the earliest. Over that decade, Singapore’s property market will go through multiple cycles, interest rate shifts, and policy changes. Buyers who select Plus or Prime flats primarily because of the lower purchase price — and not because they genuinely intend to occupy the flat for 10 years — may find themselves in a difficult position if circumstances change (job relocation overseas, family expansion, divorce).

For those who do plan to stay, the Plus and Prime schemes deliver real value. A Prime flat in a central location at a subsidised price, occupied for 10 years with a no-rental restriction, is likely to appreciate meaningfully in absolute terms even after clawback. The restriction is the price of the subsidy.

What Might Come Next

The May 2023 introduction of Plus and Prime classifications represented a significant shift from the old Mature/Non-Mature estate binary. The April 2023 announcement also removed the ability of EC buyers to use the Deferred Payment Scheme from May 2026 — suggesting the government continues to tighten across all public and quasi-public housing tiers. Any further changes to MOP duration are unlikely in the near term given that the 10-year Plus/Prime MOP is relatively new and the government will want to assess its impact before adjusting. The resale income ceiling may, however, be revised upwards over time to track median income growth in Singapore.

When does the MOP start — from key collection or from BTO ballot application?

The MOP starts from the date of key collection — not the date of BTO application, not the ballot exercise date, and not the date you pay the option fee or sign the lease agreement. The key collection date is when you physically receive the keys to your flat and formally take possession. This date is recorded by HDB and serves as the MOP commencement date. For a Standard flat collected in July 2024, the MOP expires in July 2029. For a Plus or Prime flat collected in the same month, it expires in July 2034.

Can I rent out rooms in my HDB flat while the MOP is running?

No. During the MOP, you may not rent out any part of your flat — neither the entire unit nor individual rooms. Room rental (sub-letting) is only permitted after the MOP has been fulfilled and only with HDB’s prior written approval. After the MOP, Standard flat owners may rent out rooms or the entire flat (with HDB approval); Plus and Prime flat owners may rent out rooms after the MOP but may never rent out the entire flat under any circumstances.

What happens if I need to move overseas for work during the MOP?

If you need to work overseas temporarily, you must continue to maintain your HDB flat as your Singapore residence — meaning a family member must continue to reside in the flat, and you must return periodically. You cannot rent out the flat during the MOP even if you are overseas. If your overseas stint is long-term and the flat will genuinely be unoccupied, you should consult HDB directly. Abandoning the occupancy requirement during the MOP can result in HDB compulsorily acquiring the flat at a below-market price under the Housing and Development Act — a severe consequence that buyers should be aware of.

Can I buy a private condo while my HDB MOP is still running?

Yes. Purchasing a private residential property while your HDB MOP is outstanding is permitted. However, since your HDB flat counts as your first residential property, the private condo purchase is classified as a second property for ABSD purposes. A SC pays 20% ABSD on the private condo. An SPR pays 30%. You must also have the financial capacity to service both housing loans simultaneously and remain within the 55% TDSR cap. Many HDB owners choose to exercise this option a year or two before their MOP expires, so the HDB can be sold shortly after the MOP milestone — reducing the period of dual-loan exposure.

What is the subsidy clawback for Plus and Prime flats, and when is it paid?

The subsidy clawback for Plus and Prime flats is paid to HDB at the point of the first open-market resale (i.e., the first resale transaction after the MOP). It is deducted from the sale proceeds before any balance is paid to the seller. The clawback is calculated as a percentage of the resale price or market valuation (whichever is higher). HDB has not published a fixed percentage table publicly; the exact rate is communicated in the flat purchase document at the time of BTO booking and is specific to the flat’s classification and location. The clawback only applies to the first open-market resale — subsequent owners of a Plus or Prime flat do not face an additional clawback when they eventually sell.

Do MOP rules apply to HDB flats purchased on the open resale market?

Yes. When you purchase an HDB resale flat — whether Standard, Plus, or Prime — the MOP requirement applies afresh from the date you collect the keys. A Standard resale flat has a 5-year MOP from your key collection date; a Plus resale flat has a 10-year MOP; and a Prime resale flat has a 10-year MOP. The classification (Standard, Plus, Prime) of the flat follows it through all transactions. You cannot shorten the MOP on a resale flat because the previous owner already fulfilled their MOP.

Can an SPR buyer purchase a Plus or Prime HDB flat on the open resale market?

For Plus flats: yes, subject to the income ceiling (S$14,000/month household income) and standard SPR eligibility criteria. For Prime flats: no — Prime flats may only be resold to Singapore Citizens (not SPR). This restriction applies to every resale of a Prime flat in perpetuity, not just the first resale. SPR buyers wishing to purchase Plus flats must also form an eligible family nucleus (e.g., SC/SPR family or SPR household of two or more) to qualify under HDB’s resale eligibility framework.

Disclaimer: This article is for general information only and does not constitute legal or financial advice. HDB rules, MOP durations, clawback rates, and eligibility criteria are subject to change by HDB and the Ministry of National Development. Always verify the latest requirements at hdb.gov.sg and consult HDB directly or a licensed HDB resale agent for guidance specific to your situation. All figures and scenarios are illustrative and based on publicly available data as at 16 May 2026.

Foreigners (non-PR, non-SC) may purchase private residential property — condominiums, apartments, strata-titled units — in Singapore without restriction, subject to a 60% Additional Buyer’s Stamp Duty (ABSD) payable to IRAS.

Foreigners cannot buy HDB flats (resale or BTO) and cannot buy landed residential property (houses, semi-detached, bungalows) without prior approval from the Singapore Land Authority (SLA), which is rarely granted.

Executive Condominiums (ECs) become available to foreigners only after privatisation. For ECs from GLS sites tendered from 8 May 2026 onwards, privatisation occurs at 15 years from TOP; earlier ECs remain at 10 years.

The 60% ABSD applies to the entire purchase price and must be paid within 14 days of exercising the Option to Purchase (OTP).

Buyer’s Stamp Duty (BSD) is payable by all buyers regardless of nationality. On a S$2.5M purchase, BSD is approximately S$94,600.

Foreigners can obtain a mortgage from Singapore-licensed banks. LTV limit is 75% for a first property loan with no existing housing loans, subject to Total Debt Servicing Ratio (TDSR) of 55%.

Commercial and industrial property carries no ABSD — foreigners may purchase shophouses, office units, factories, and warehouses without the 60% surcharge.

Nationals of the USA, Iceland, Liechtenstein, Norway, and Switzerland are exempt from ABSD on their first residential purchase under Free Trade Agreement commitments.

What Is the ABSD and Who Administers It?

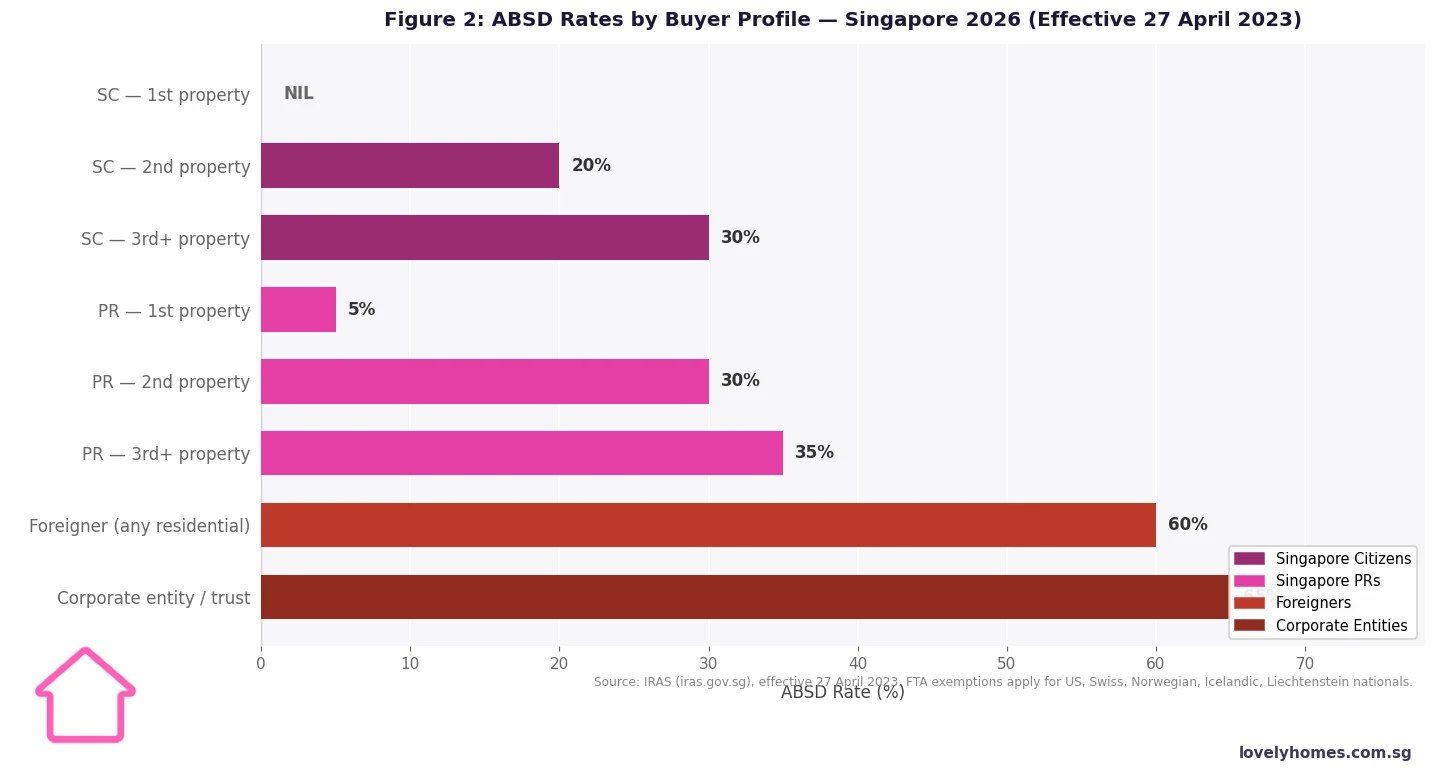

The Additional Buyer’s Stamp Duty (ABSD) is a surcharge levied by the Inland Revenue Authority of Singapore (IRAS) on the purchase or acquisition of residential property in Singapore, on top of the standard Buyer’s Stamp Duty (BSD). Introduced in December 2011 as a demand-side cooling measure, the ABSD has been adjusted multiple times. The most significant recent change for foreigners was on 27 April 2023, when the rate was doubled from 30% to 60%.

The policy objective is explicit: ABSD prioritises home ownership for Singaporeans and ensures that property remains affordable for residents. Non-resident buyers must bear a substantial additional cost — and this is intentional. Singapore’s Ministry of National Development has consistently maintained that residential property is primarily for citizens, and the 60% rate is designed to reflect that priority firmly.

Figure 1: Property Eligibility by Buyer Type — Singapore 2026 | Source: HDB, URA, SLA, IRAS

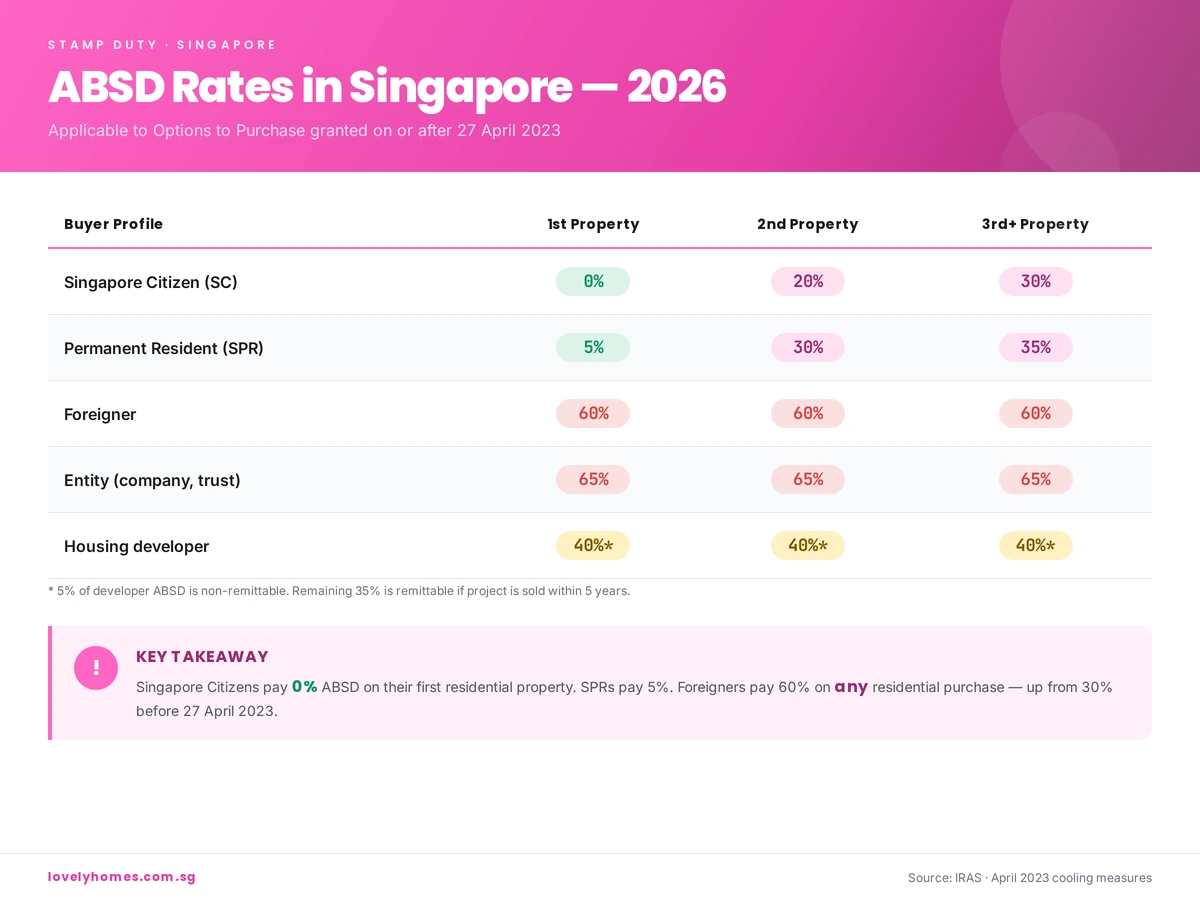

ABSD Rates by Buyer Profile (Effective 27 April 2023)

ABSD is charged on the higher of the purchase price or the property’s market value. The table below shows the current rates, administered by IRAS, for residential property in Singapore:

Buyer Profile

1st Property

2nd Property

3rd+ Property

Singapore Citizen

0%

20%

30%

Singapore Permanent Resident (PR)

5%

30%

35%

Foreigner (non-PR, non-SC)

60% — flat rate, regardless of how many properties held in Singapore

Corporate entity / trust

65% — flat rate on residential property

Source: IRAS, effective 27 April 2023. FTA exemptions apply for nationals of the USA, Switzerland, Iceland, Liechtenstein, and Norway.

Figure 2: ABSD Rates by Buyer Profile — Singapore 2026 | Source: IRAS, effective 27 April 2023

Free Trade Agreement (FTA) Exemptions

Under Singapore’s FTA commitments, nationals of the USA, Iceland, Liechtenstein, Norway, and Switzerland are treated on par with Singapore Citizens for ABSD on their first residential property purchase. This means a US national buying their first Singapore condo pays 0% ABSD. On second and subsequent purchases, the SC schedule applies. The exemption is for individuals only; US-incorporated companies do not benefit. IRAS requires passport proof of nationality when claiming the FTA exemption.

What Foreigners Can Buy — and Cannot Buy

Permitted (60% ABSD where residential): Private condominiums, private apartments, strata-titled units, SOHO units with residential classification. ECs after privatisation (15 years from TOP for new GLS-launched ECs from 8 May 2026; 10 years for earlier ECs). Sentosa Cove landed property. Commercial shophouses, strata office units, retail units, industrial factories, warehouses — all without residential ABSD.

Not permitted without special approval: Landed residential property outside Sentosa Cove (houses, semi-detached, bungalows, terraced houses). The SLA may grant approval under the Residential Property Act in exceptional circumstances, but approvals are rare.

Strictly prohibited: HDB flats (both new BTO and resale). HDB housing is reserved for Singapore citizens and permanent residents under the Housing and Development Act. ECs during their MOP and privatisation period are also off-limits to foreigners.

Buyer’s Stamp Duty (BSD) — Payable by Everyone

BSD is levied by IRAS on every property purchase in Singapore, regardless of nationality. For residential property, the tiered rates are: 1% on the first S$180,000; 2% on the next S$180,000; 3% on the next S$640,000; 4% on the next S$500,000; 5% on the next S$1,500,000; and 6% on amounts above S$3,000,000. On a S$2.5M purchase, total BSD = S$94,600.

Purchase Price Tier

BSD Rate

BSD on This Tier

First S$180,000

1%

S$1,800

Next S$180,000 (up to S$360,000)

2%

S$3,600

Next S$640,000 (up to S$1,000,000)

3%

S$19,200

Next S$500,000 (up to S$1,500,000)

4%

S$20,000

Next S$1,500,000 (up to S$3,000,000)

5%

Up to S$75,000

Remainder above S$3,000,000

6%

Variable

Sellers’ Stamp Duty (SSD) — The Anti-Flip Tax

SSD is administered by IRAS and applies to all sellers who dispose of residential property within three years of purchase, regardless of nationality. The rates are: 12% within 1 year; 8% within 2 years; 4% within 3 years; nil thereafter. For a foreigner who has paid 60% ABSD, an SSD liability on a short-term resale would be a severe additional burden. Foreign buyers must plan for a meaningful long-term holding horizon.

Holding Period

SSD Rate

Up to 1 year

12%

1 to 2 years

8%

2 to 3 years

4%

More than 3 years

Nil

Financing — LTV, TDSR, and Mortgage Options

Foreigners may borrow from Singapore-licensed banks subject to MAS macro-prudential rules identical to those applied to residents. The LTV limit is 75% for a first property loan with no existing housing loans (reducing to 55% for a second and 35% for a third). The TDSR cap is 55% of gross monthly income. Loan tenors run up to 35 years, typically reduced by age exceeding 65. Most major Singapore banks lend to foreigners — DBS, OCBC, UOB, Standard Chartered, and HSBC all do so, subject to enhanced documentation requirements including overseas income proof and a valid work pass or Long-Term Visit Pass.

The Buying Process — Step by Step

Arrange in-principle approval: Approach at least two Singapore banks before making offers. Allow 5–10 working days.

Engage a CEA-licensed agent: For new launches, no buyer commission is payable; for resale, co-broking arrangements vary.

Option to Purchase (OTP): On resale, the seller grants an OTP valid for 21 days; a 1% option fee is paid. For new launches, a 5% booking fee is paid directly to the developer.

Pay BSD and ABSD: Both due within 14 days of OTP exercise. On a S$2.5M purchase, this means wiring S$94,600 (BSD) + S$1,500,000 (ABSD) to IRAS — a total of S$1,594,600 within a fortnight of signing.

Engage a conveyancing solicitor: A Singapore-qualified solicitor handles title searches, mortgage documentation, and lodgement with SLA’s eConveyancing portal.

Completion: For resale, typically 8–12 weeks. For new launches, completion occurs at TOP/CSC, which may be 3–5 years away.

Worked Example: Mr David Harrington Buys a S$2.5M CCR Condo

Mr David Harrington, 42, is a British national on an Employment Pass earning S$25,000/month gross. He purchases a two-bedroom unit in District 9 at S$2,500,000, with no existing property loans in Singapore.

Monthly mortgage at 3.30% p.a. over 20 years on S$1,875,000 ≈ S$10,633/month. TDSR check: S$10,633 ÷ 55% = S$19,333 minimum monthly gross income required. Mr Harrington’s S$25,000/month comfortably qualifies. However, stamp duties alone represent 63.8% of the purchase price — the property must appreciate significantly for the investment to make financial sense on a net basis.

What This Means for Foreign Buyers

Despite the 60% ABSD headline rate, Singapore continues to attract foreign buyers for structurally sound reasons. Singapore offers secure freehold and 99-year leasehold titles with one of the most transparent property title systems in Asia. There is no capital gains tax, no inheritance tax, and no wealth tax. The SGD has historically been stable and appreciating against most major currencies, and Singapore’s rule of law is consistently ranked among the best globally.

For high-net-worth buyers from jurisdictions with currency risk, political instability, or restricted capital mobility — particularly from certain parts of Southeast Asia, China, and the Middle East — paying 60% ABSD is the premium for a stable, internationally recognised store of value. For US nationals, who pay 0% ABSD on their first purchase thanks to the FTA, Singapore offers one of the most favourable entry points into any developed-market property system globally.

What Might Come Next

The 60% ABSD rate for foreigners is unlikely to be reduced in the near term. Singapore’s government has consistently adjusted rates upward when demand has been firm, and the April 2023 doubling was a clear statement of direction. The EC policy changes of 8 May 2026 — extending MOP to 10 years and privatisation to 15 years, abolishing the Deferred Payment Scheme — further indicate a tightening trajectory. Foreign buyers should plan their acquisitions assuming the 60% rate will persist for the foreseeable future and structure their financial planning accordingly.

Can a foreigner on an Employment Pass buy a condo in Singapore?

Yes. Holding an Employment Pass does not confer Singapore PR status, so the buyer is classified as a foreigner for ABSD purposes — meaning 60% ABSD applies. There is no minimum residency duration requirement to purchase private residential property. The buyer must satisfy the bank’s TDSR requirements using their Singapore employment income (fully counted) and any overseas income (subject to a bank haircut, typically around 30% on variable income).

Are there properties foreigners can buy without the 60% ABSD?

Yes. Commercial and industrial properties do not attract the residential ABSD. Strata office units, retail units, commercial shophouses, industrial factories, and warehouses can all be purchased by foreigners without the 60% surcharge. Many foreign investors therefore channel their Singapore property exposure through commercial assets or Singapore REITs listed on SGX, which provide property-linked returns without the ABSD burden.

Can a foreigner married to a Singapore Citizen pay lower ABSD?

Not directly on a joint purchase. If the property is purchased in the Singapore Citizen spouse’s name alone (sole ownership) and it is the SC’s first property, no ABSD is payable. However, if both names appear on the title, the foreigner’s inclusion triggers 60% ABSD. Many cross-nationality couples place the first property in the SC’s sole name. On subsequent purchases in joint names, ABSD at the SC second-property rate of 20% applies. Seek independent legal and tax advice before structuring ownership this way, as there are CPF, mortgage liability, and estate planning implications.

When exactly must the ABSD be paid?

ABSD must be paid within 14 days of the date on which the liability arises — typically the date of exercising the OTP or the date of the Sale and Purchase Agreement, whichever is earlier. Late payment attracts a 5% per annum penalty interest plus potential IRAS prosecution under the Stamp Duties Act. There is no grace period. The full ABSD amount must be available on or before the deadline, not merely committed in a loan facility.

Is ABSD refundable if the purchase falls through after the OTP is exercised?

Generally, no. Once the ABSD liability arises, it is payable regardless of whether the transaction completes. IRAS may consider a remission application in exceptional circumstances if a transaction is aborted, but this is not guaranteed. The ABSD Married Couple Remission — which allows one SC/PR spouse to sell their existing property within six months of a joint purchase and claim a refund — does not apply to foreigners. Always consult a licensed conveyancing solicitor before exercising any OTP if there is uncertainty about financing, as the ABSD liability is triggered on signing.

Can a foreigner buy a shophouse and occupy the upper residential floor?

This depends on the shophouse’s URA zoning and approved use. If the upper floors are classified as residential under the Residential Property Act, a foreigner cannot purchase without SLA approval (rarely granted). Some shophouses are zoned entirely commercial or approved for mixed use with the upper floors treated as non-residential. The correct approach is to check the URA Master Plan zoning and the specific approved use with a conveyancing solicitor before making any offer, as the legal classification is significant and not always obvious from the building’s physical appearance.

Does a foreigner pay ABSD on a privatised Executive Condominium?

Yes. Once an EC is privatised, it is treated as private residential property and all standard ABSD rules apply — including the 60% rate for foreigners. For ECs launched under GLS tenders from 8 May 2026, privatisation occurs at 15 years from TOP; earlier ECs privatise at 10 years from TOP. Buyers purchasing privatised ECs in the secondary market should verify the specific EC’s TOP date and calculate the privatisation milestone accordingly before making an offer.

Disclaimer: This article is for general information only and does not constitute legal, tax, or financial advice. Stamp duty rates, eligibility rules, and financing guidelines are subject to change by IRAS, MAS, HDB, SLA, and URA. Always verify current rates at iras.gov.sg and consult a licensed Singapore conveyancing solicitor, a CEA-registered real estate professional, and a licensed mortgage adviser before committing to any property transaction. All figures are illustrative based on publicly available data as at 16 May 2026.

Rental yield measures annual rental income as a percentage of property value. Gross yields in Singapore range from roughly 2.2% (landed, CCR) to 5.0% (OCR condos, non-mature HDB). Net yield after tax, maintenance, and vacancy is typically 1–1.5 percentage points lower.

Capital gain is the appreciation in property value over the holding period. Singapore private residential prices rose roughly 30% between 2020 and 2022, but growth has moderated to 1–3% per annum post-cooling measures.

At current mortgage rates of ~3.5–4.2% per annum (SORA-pegged and fixed), most Singapore investment properties produce neutral to negative cash flow — the investor is effectively subsidising the mortgage in exchange for capital appreciation.

HDB flats as investment properties produce the highest net yields (4–5%) but are subject to owner-occupier rules — you cannot buy an HDB resale flat purely as an investment while owning other property.

The correct choice depends on your liquidity needs, tax position, holding period, and leverage tolerance.

The 60% ABSD on foreigners and 20% on Singapore Permanent Residents for second property purchases fundamentally reshape yield maths for those cohorts.

A Singapore Citizen paying 20% ABSD on a second property raises the effective entry cost by S$300,000 on a S$1.5M condo — requiring a higher yield or longer hold to break even.

Diversification into Singapore REITs offers yield exposure with no ABSD, no management burden, and far lower minimum capital.

Understanding Rental Yield: Gross vs Net

Rental yield is the simplest metric for property investors — it tells you how much income the property generates relative to its cost. However, the headline gross yield figure can mislead. Gross yield divides annual rental income by the property price. Net yield, which is far more meaningful, deducts all recurring ownership costs: property tax (at the non-owner-occupier rate), maintenance fees, agent commissions and vacancy allowance, insurance, and any management costs.

In Singapore’s high-tax environment for investment properties, the gap between gross and net yield is substantial. Investment-rate property tax for a non-owner-occupied residential unit is assessed on the Annual Value (AV) — which the Inland Revenue Authority of Singapore (IRAS) estimates at market rent — at rates of 11% on the first S$30,000 AV and up to 27% on AV above S$90,000 (effective 2024). This alone can reduce your gross yield by 0.8–1.2 percentage points. See our guide to capital gains and rental income tax for the full deduction analysis.

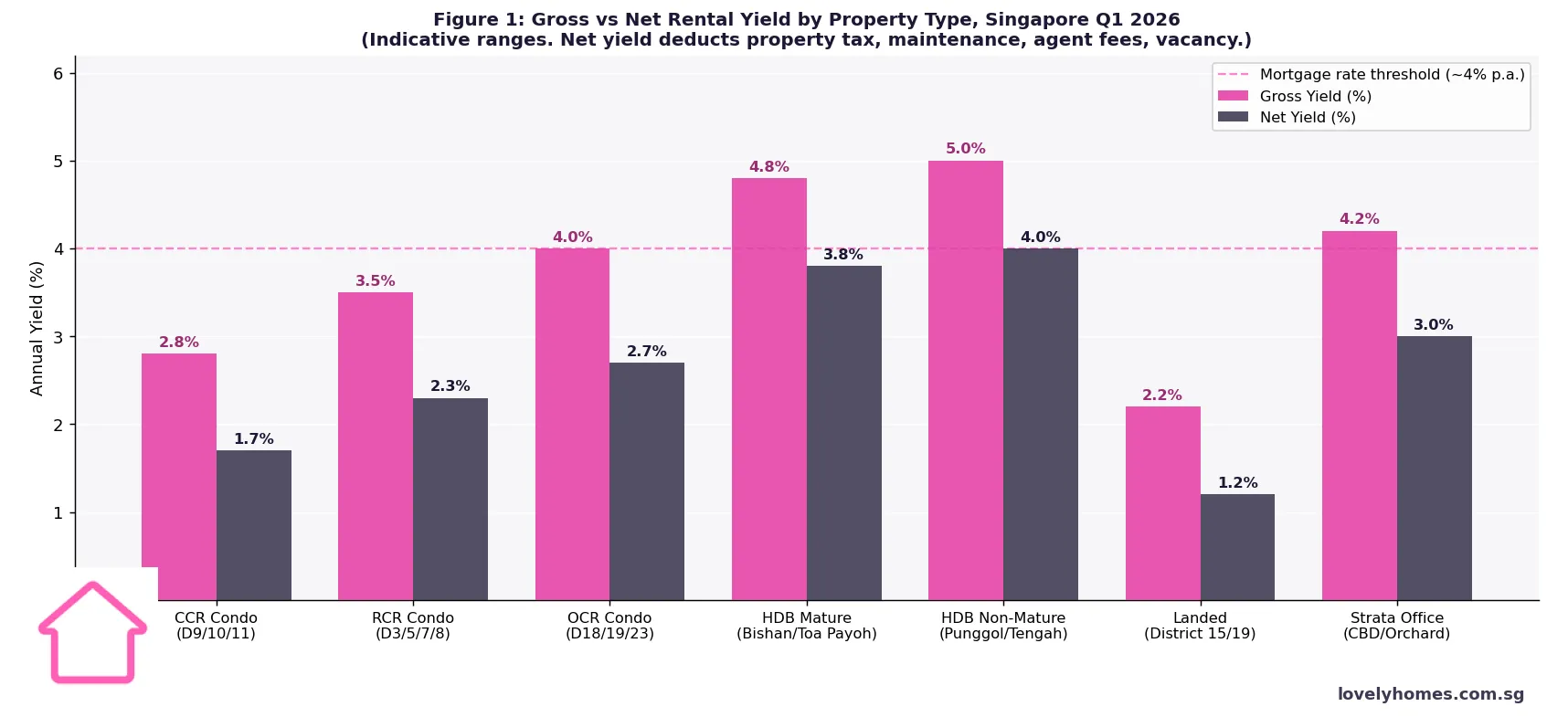

Figure 1: Gross vs Net Rental Yield by Property Type, Singapore Q1 2026. Sources: URA, HDB, IRAS. Figures are indicative market averages; individual properties will vary.

The yield picture in Q1 2026 tells a clear story. OCR condominiums and non-mature HDB flats offer the most attractive net yields (2.7–4.0%) for Singapore Citizen investors who own no other residential property. CCR condominiums, where purchase prices have risen fastest, show compressed net yields of 1.7% — well below the prevailing mortgage rate of 3.5–4.2%. A CCR investor at current prices is implicitly betting on capital appreciation rather than income.

The mortgage-rate threshold line on Figure 1 is critical: any property with a net yield below the investor’s mortgage rate produces negative cash flow. The investor’s equity is being drawn down each month until either (a) rental rates rise, (b) the mortgage is refinanced to a lower rate, or (c) the property is sold. For most CCR and landed investments at current prices, this is the reality.

Understanding Capital Gain: The Singapore Track Record

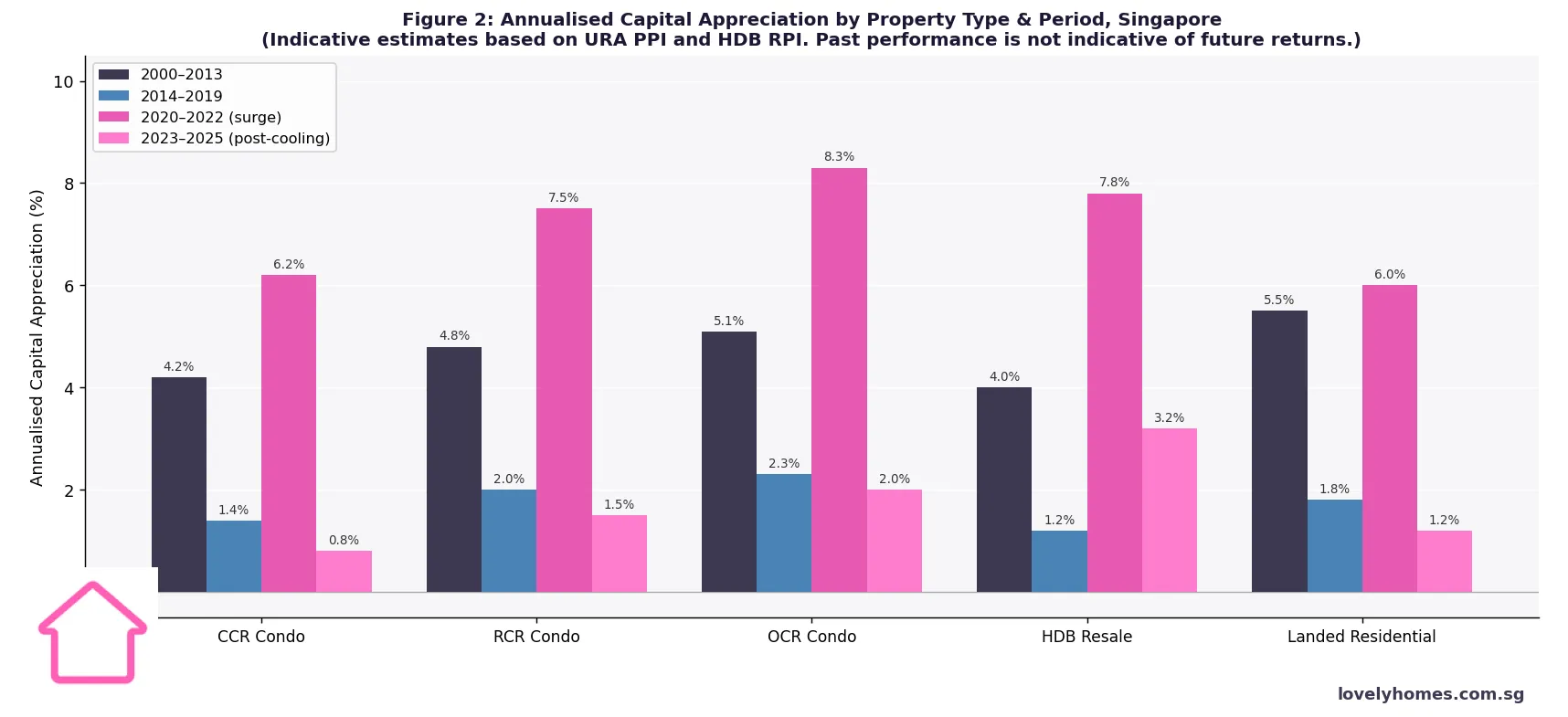

Figure 2: Annualised Capital Appreciation by Property Type & Period, Singapore. Sources: URA Private Residential Property Price Index, HDB Resale Price Index. Past performance is not indicative of future returns.

Singapore residential property delivered strong long-run capital appreciation — particularly the 2000–2013 period, which included the post-SARS recovery, two rounds of quantitative easing, and robust population growth. OCR condos and landed property produced annualised gains of 5–6% over that period. However, the 2014–2019 period — dominated by progressive rounds of cooling measures, the Total Debt Servicing Ratio (TDSR) framework, and population growth moderation — saw annualised gains compress to 1.2–2.3% across all property types.

The 2020–2022 surge was exceptional: the pandemic-era ultra-low interest rate environment (SORA briefly fell to 0.22% in 2021), pent-up demand, and a structurally undersupplied resale market drove annualised gains of 6–8% across OCR and HDB. This period is unlikely to repeat in the near term given current mortgage rates of 3.5–4.5% and the government’s demonstrated willingness to deploy cooling measures.

The 2023–2025 post-cooling stabilisation shows OCR condos and HDB resale at 2–3.2% per annum — more sustainable but insufficient to justify a leveraged investment at current LTV and mortgage rate assumptions unless the investor has a 10+ year horizon.

The ABSD Factor: How Stamp Duty Reshapes the Calculus

Singapore Citizens purchasing a second residential property pay 20% ABSD on the purchase price, effective from 27 April 2023. On a S$1.5M OCR condo, this amounts to S$300,000 — an additional upfront cost that must be recovered before the investment breaks even. At a net yield of 2.7% (post all costs), the investor earns approximately S$40,500 per annum in net rental income. At that rate, it takes over seven years of rental income alone to recover the ABSD cost — before accounting for mortgage interest subsidisation.

This is why the property-vs-REIT comparison has become increasingly compelling. Singapore REITs attract zero ABSD, no property tax, no maintenance fees, and no tenant management burden, with gross distributions of 5–8% in many sectors. The trade-off is that REITs do not offer the leverage of a mortgage-financed property and are subject to equity market volatility. See the dedicated S-REIT Investment Guide 2026 for a detailed comparison.

For Singapore Permanent Residents (SPR), the ABSD on a second residential property rises to 30%, making the break-even period even longer. For foreigners, the 60% ABSD renders residential property investment (as opposed to owner-occupation) economically untenable in most cases. Commercial property, which does not attract ABSD and where foreigners can invest freely, offers a structurally more favourable framework for non-citizen investors.

Summary Table: Rental Yield vs Capital Gain at a Glance

Factor

Rental Yield Focus

Capital Gain Focus

Best property type

OCR condo, non-mature HDB

CCR / RCR condo, landed

Typical gross yield

3.5–5.0%

2.2–3.5%

Monthly cash flow

Near break-even to positive

Typically negative (subsidised)

Ideal hold period

3–7 years

7–15 years

Liquidity risk

Lower (OCR wider buyer pool)

Higher (CCR narrower pool)

Key risk

Vacancy, yield compression

Cooling measures, rate rises

ABSD impact (2nd property, SC)

Significant — 7+ yr payback

Significant — 10+ yr payback

Alternative

S-REITs (5–8% distributions)

Growth REITs / commercial

Worked Example: Ms Tan’s S$1.5M OCR Condo

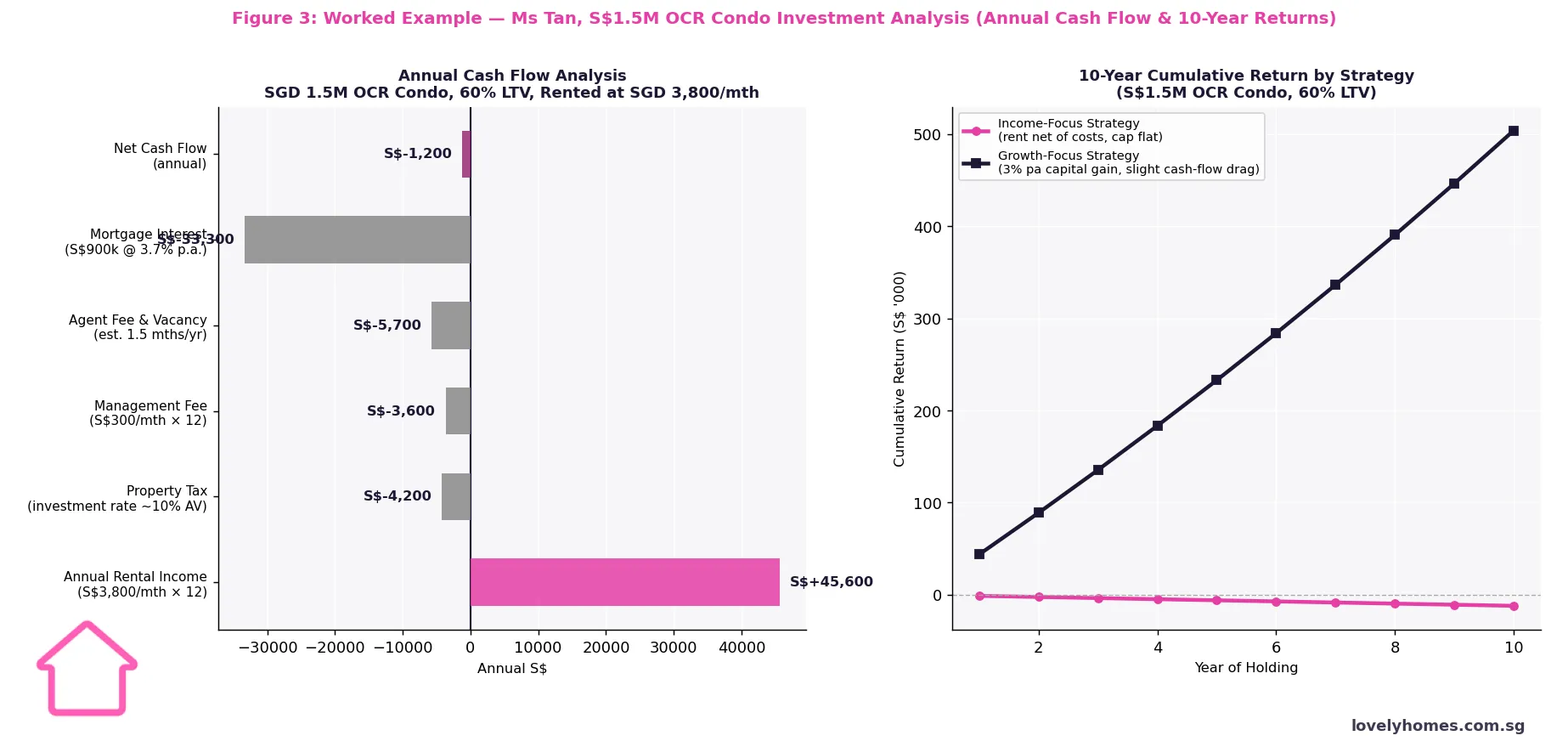

Figure 3: Ms Tan — S$1.5M OCR Condo Annual Cash Flow & 10-Year Returns. Figures are indicative. Consult a licensed adviser before investing.

Ms Tan, 42, is a Singapore Citizen with one HDB flat (fully paid). She wishes to invest S$1.5M in a second residential property — a 2-bedroom OCR condo in Tampines. She pays 20% ABSD (S$300,000) plus 5% BSD (S$44,600), bringing the total acquisition cost to S$1,844,600. She finances 60% of the purchase price (S$900,000) via a bank loan at 3.7% per annum (SORA spread, 25-year tenure) after satisfying the TDSR Singapore 2026 constraint at her household income of S$18,000/month.

Annual cash flow breakdown:

Rental income: S$3,800/month × 12 = S$45,600

Property tax (investment rate, estimated AV S$33,600): ~S$4,200

Management fee (S$300/month): S$3,600

Agent and vacancy allowance (1.5 months/year): S$5,700

Mortgage interest (S$900k × 3.7%): S$33,300

Net annual cash flow: approximately –S$1,200 (slightly negative)

The gross yield on the purchase price is 3.04%. The net yield (after all costs, before mortgage principal) is approximately 2.72% — below the mortgage rate of 3.7%. Ms Tan is effectively subsidising the mortgage by about S$1,200 per annum, plus the opportunity cost of the S$300,000 ABSD (foregone investment return at 3% = S$9,000/year).

Capital appreciation scenario: If the property appreciates at 3% per annum over 10 years, the gross capital gain is approximately S$515,000. After selling costs (BSD on seller side N/A — no SSD after 3 years), agent commission (~1%), and assuming no further Seller’s Stamp Duty (the Seller’s Stamp Duty applies for 3 years post-purchase per the property’s holding period), the net gain before tax is approximately S$495,000. Over 10 years, total net return (rental income net + capital gain) is approximately S$483,000 — an annualised return on total equity deployed of roughly 5.5% per annum.

By comparison, the same S$300,000 ABSD + S$600,000 downpayment (S$900,000 total equity) invested in a diversified S-REIT portfolio at a conservative 6% gross distribution yield with 2% capital growth would yield approximately S$690,000 over 10 years — a meaningfully higher outcome with no tenant management, no maintenance, and no mortgage. The direct property route wins primarily if capital appreciation exceeds 3% per annum or if rental rates rise materially.

Why This Matters for Singapore Investors in 2026

The investment property thesis in Singapore has always rested on three pillars: land scarcity, population growth, and government commitment to maintaining a stable housing market. All three remain broadly intact, but the near-term environment is more challenging than the 2020–2022 peak. Mortgage rates have risen from near-zero to 3.5–4.5%, vacancy rates in the private rental market have crept up from sub-5% to 7–10% in CCR and RCR, and the government has maintained or tightened cooling measures (most recently the EC cooling measures of May 2026).

Investors entering the market in 2026 should model conservatively: assume net yields of 2.5–3.5% for OCR condos, capital appreciation of 2–3% per annum (not the 7–8% of 2021–2022), a mortgage rate of 3.5–4.0%, and a 10+ year hold period for the investment to produce an acceptable risk-adjusted return. The ABSD payback period must be factored into the break-even analysis.

What Might Come Next

Several factors could materially shift the yield/growth calculus in the medium term. On the positive side: a sustained decline in Singapore Overnight Rate Average (SORA) benchmarks (linked to US Federal Reserve easing) would reduce mortgage rates and improve cash flows; continued strong foreign talent attraction supporting rental demand; and the progressive unveiling of the Greater Southern Waterfront and Jurong Lake District transformations creating new capital appreciation pockets. On the negative side: an expansion of the pipeline of private residential completions from the record 1H 2026 Government Land Sales programme could compress rents; any tightening of the foreign talent inflow policy would reduce rental demand; and a deterioration in the global economic environment could dampen transaction volumes and prices.

Investors are encouraged to treat property as one component of a diversified portfolio, weigh the liquidity and ABSD constraints explicitly, and consult a licensed financial adviser before committing capital at these price levels.

Frequently Asked Questions

What is the difference between gross yield and net yield in Singapore property?

Gross yield divides annual rental income by the property’s market value or purchase price — it gives you a quick comparison benchmark. Net yield deducts all recurring ownership costs: property tax (charged by IRAS at the investment rate, not the lower owner-occupier rate), maintenance fees, sinking fund contributions, agent commission for finding tenants (typically half a month’s rent per year), vacancy allowance, and insurance. For Singapore condominiums, the gap between gross and net yield is typically 1.0–1.5 percentage points, meaning a property with a 4% gross yield might deliver only 2.5–3.0% net. When evaluating a property for investment, always use net yield as the baseline for comparison against mortgage costs and alternative investments.

Is rental income from Singapore property taxable?

Yes. Rental income from a Singapore property is subject to personal income tax at your marginal rate, which can be as high as 24% for high-income individuals. However, the income is assessed on a net basis — you may deduct allowable expenses including mortgage interest (the interest component, not principal), property tax, maintenance fees, agent commissions, and a deemed 15% allowance on gross rent as an alternative to tracking actual expenses. A property generating S$45,600 gross rent with actual deductible expenses of S$46,800 would produce a taxable loss — which can offset other income in some circumstances. See our guide to capital gains and rental income tax for a full worked example of both the actual-expense and deemed-expense paths.

Can I use CPF to fund an investment property in Singapore?

Yes, you can use CPF Ordinary Account (OA) funds to fund the downpayment and monthly instalments for a second residential property, subject to certain conditions. The CPF usage limit is generally 120% of the property’s valuation limit, and the property must have a remaining lease of at least 20 years. However, all CPF funds used — plus accrued interest at 2.5% per annum — must be refunded to your CPF account from the sale proceeds when you sell. This accrued interest effectively reduces your net profit from the investment. Many investors underestimate this cost; a property held for 20 years could have an accrued interest liability of 65% or more of the original CPF amount used.

How does Seller’s Stamp Duty affect my investment exit strategy?

Seller’s Stamp Duty (SSD) applies to private residential properties sold within 3 years of purchase: 12% in year 1, 8% in year 2, and 4% in year 3. If you purchase a S$1.5M condo and sell within 12 months, SSD is S$180,000 — a massive cost that eliminates most short-term investment gains. SSD does not apply after the 3-year holding period. This means the effective minimum hold for a leveraged property investment is at least 3 years; most investors target 5–10 years to allow the ABSD, SSD, and acquisition costs to be absorbed into a meaningful capital gain. The ABSD guide contains a full table of stamp duty rates by buyer profile and property type.

What are the best alternatives to direct property investment in Singapore?

Singapore offers several liquid alternatives to direct residential property investment. Singapore REITs (S-REITs) trade on SGX and offer diversified exposure to commercial, industrial, retail, healthcare, and data-centre real estate with gross distributions of 5–8% and no ABSD, no management burden, and high liquidity. Freehold strata offices in the CBD carry no ABSD for foreigners and offer yields of 3.5–5%. CPF Investment Scheme (CPFIS) products allow some CPF OA and SA funds to be invested in REITs and property-linked instruments. For investors who want Singapore property exposure without the capital outlay, some private funds and family-office structures offer fractional exposure to residential or commercial portfolios. The commercial property guide and REITs guide provide detailed comparisons.

Should I prioritise yield or growth when buying an investment property?

The correct priority depends on your financial profile. If you have high monthly cash commitments and cannot sustain a negative-cash-flow property for an extended period, yield should take priority — an OCR condo or resale HDB (if eligible) provides a better income cushion. If you have substantial savings, a long investment horizon (10+ years), and a high income that covers any monthly shortfall, a CCR or prime-location property may deliver superior absolute capital gains over the long run, even if the annual cash flow is negative. In the current rate environment (mortgage rates 3.5–4.2%), properties with gross yields below 4% are cash-flow negative even without accounting for ABSD, so ensure you model both the yield and the capital appreciation case explicitly before committing.

How do I calculate the net return on a Singapore investment property?

Total net return = (Net rental income over hold period) + (Sale price – Purchase price – Acquisition costs – Selling costs). Acquisition costs include BSD, ABSD, legal fees (roughly S$3,000–S$6,000 for a condo purchase), and agent commission. Selling costs include agent commission (1–2% of sale price), legal fees, and any SSD if sold within 3 years. If CPF was used, you must also account for CPF accrued interest repaid to the CPF account on sale. Divide total net return by the equity deployed (downpayment + ABSD + all upfront costs) and the number of years held to derive an annualised return on equity. For most S$1.5M OCR condos purchased in 2026 with 20% ABSD, you need a minimum 3.5% per annum capital appreciation and a 10-year hold to match a 6% p.a. REIT distribution on the same equity.

This article is for general informational purposes only and does not constitute financial, tax, or investment advice. Rental yields, capital appreciation figures, and return projections are illustrative estimates based on publicly available data and should not be relied upon for investment decisions. Past performance of Singapore property markets is not indicative of future returns. All investments carry risk, including the possible loss of principal. Consult a licensed financial adviser, MAS-licensed investment adviser, and IRAS for your specific circumstances. ABSD, SSD, and other stamp duty rates are subject to change without notice.

Tags: Rental Yield Singapore, Capital Gain Property Singapore, Singapore Property Investment 2026, Gross Net Yield, Investment Property Singapore, ABSD Second Property, Singapore Condo Investment, Property vs REITs, OCR Condo Yield, Singapore Property Returns

ABSD Singapore — short for Additional Buyer’s Stamp Duty — is the single largest upfront cost most buyers face when purchasing a second (or third, or fourth) residential property in Singapore. If you are buying as a foreigner, ABSD can add 60% of the purchase price to your cost. If you are a Singapore Citizen buying your second property, that figure is 20%. Get this number wrong in your budgeting, and you can very quickly wipe out years of planning.

This guide walks you through exactly how ABSD works in 2026 — who pays, how much, how it is calculated, what remissions are available, and the legitimate strategies property buyers use to manage it. All figures reflect the Government’s 27 April 2023 cooling measures, which remain the applicable framework. For the latest rates, always check the IRAS Additional Buyer’s Stamp Duty page.

Quick Answer — ABSD at a glance

Singapore Citizens: 0% on 1st property, 20% on 2nd, 30% on 3rd+

Singapore PRs: 5% / 30% / 35%

Foreigners: 60% on any residential property

Companies, trusts and other entities: 65%

ABSD is payable within 14 days of signing the Option to Purchase (OTP) or Sale & Purchase Agreement.

What is ABSD and Why Does It Exist?

ABSD is a transaction tax levied on the buyer when acquiring a residential property in Singapore. It sits on top of the regular Buyer’s Stamp Duty (BSD) that every buyer pays. Where BSD is progressive and maxes out at 6% for the portion of price above S$3 million, ABSD is a flat rate applied to the entire purchase price or market value (whichever is higher).

The tax was introduced in December 2011 as part of the Government’s suite of cooling measures — the tools Singapore uses to moderate speculative demand, manage affordability for owner-occupiers, and prevent the kind of runaway price inflation seen in other global cities. Because it targets second-and-subsequent-property buyers and non-citizens disproportionately, ABSD is the single most powerful lever in the cooling-measures toolbox. You can read more about the broader framework in our Property Cooling Measures section.

ABSD Rates in Singapore (2026)

The table below sets out the ABSD rates currently in force. Rates apply based on the profile of the buyer at the time the Option to Purchase (OTP) is granted.

ABSD rates by buyer profile — applicable to OTPs granted on or after 27 April 2023.

Buyer Profile

1st Residential Property

2nd Residential Property

3rd & Subsequent

Singapore Citizen (SC)

0%

20%

30%

Singapore Permanent Resident (SPR)

5%

30%

35%

Foreigner (non-PR individual)

60%

60%

60%

Entity (e.g. company, trustee for a trust)

65%

65%

65%

Housing developer

40%*

40%*

40%*

* 5% of a developer’s ABSD is non-remittable. The remaining 35% is remittable subject to conditions, including selling all units in a qualifying project within five years.

How ABSD is Calculated — A Worked Example

ABSD is applied to the higher of the purchase price or the market value of the property. It is not charged on a tiered basis — the full rate applies to the entire amount.

Example: A Singapore Citizen couple already owns their first home (a 4-room HDB flat). They decide to buy a S$2,000,000 resale condominium in District 15 as an upgrader investment. ABSD on the second property for a Singapore Citizen is 20%.

Purchase price: S$2,000,000

ABSD (20%): S$400,000

BSD (progressive, on S$2m): approximately S$64,600

Total stamp duty payable: S$464,600

That S$400,000 ABSD alone would consume most of the typical upgrader’s CPF and cash reserves. This is why many Singaporean couples take the ‘sell first, buy second’ upgrade route — selling the existing HDB or condo before buying the next home — which we cover later in this guide.

Who Pays ABSD? Exemptions and Special Cases

ABSD applies when you purchase an additional residential property. Commercial property, industrial property, and pure-land parcels are not within its scope. A property is counted toward your “property count” if:

You hold the title as a sole owner, joint tenant, or tenant-in-common;

You are a beneficial owner via a trust;

You are a beneficiary of an estate that holds residential property.

Properties not counted include: properties you merely reside in but do not own (e.g. as a tenant), inherited shares in a deceased estate within the administration period, and certain industrial/commercial units.

Executive Condominiums (ECs)

For new ECs bought directly from the developer during the minimum occupation period of the scheme, ABSD is not triggered because the buyer must commit to an owner-occupier arrangement. ABSD rules apply normally if an EC is purchased on the resale market after its 5-year MOP and 10-year privatisation milestones.

Free Trade Agreement (FTA) Nationals

Citizens and Permanent Residents of countries with which Singapore has an FTA extending National Treatment on stamp duty — namely Iceland, Liechtenstein, Norway, Switzerland, and United States citizens — are accorded the same ABSD treatment as Singapore Citizens. An eligible US citizen buying their first Singapore residential property therefore pays 0% ABSD, not 60%.

ABSD Remission Schemes — How to Get Some (or All) of It Back

Several remission schemes let qualifying buyers claim back part or all of the ABSD they initially pay. The big three to know are:

1. Married Couple Remission (Sale of First Residential Property)

If a Singapore Citizen (or mixed SC & SPR, SC & foreigner) couple buys a replacement home before selling their existing one, they can apply for ABSD remission provided they sell the first property within six months of the later of (a) the date of purchase of the replacement property, or (b) the TOP/CSC date if buying an uncompleted unit. This is effectively a “grace period” that allows upgraders to move without double-paying ABSD.

2. Mixed-Nationality Married Couples

An SC spouse married to a foreigner buying a matrimonial home jointly can enjoy SC rates (rather than foreigner rates) if the property will be used as their matrimonial home and conditions are met. Again, for a first joint home this means 0% ABSD.

3. Developer ABSD Remission

Licensed housing developers pay 40% ABSD upfront (5% non-remittable, 35% remittable) on land purchased for residential development. The 35% is remittable upon meeting development and sales conditions — typically completing the project and selling all units within 5 years.

Remissions must be applied for within strict timeframes (usually 14 days of the triggering event). We strongly recommend engaging a conveyancing lawyer who is experienced in stamp-duty remission applications before signing any OTP where remission will be relied upon.

ABSD vs BSD: What is the Difference?

Every property purchase in Singapore attracts Buyer’s Stamp Duty (BSD), which is a progressive tax on the purchase price:

1% on the first S$180,000

2% on the next S$180,000

3% on the next S$640,000

4% on the next S$500,000

5% on the next S$1,500,000

6% on the portion above S$3,000,000 (residential only)

BSD applies to every buyer; ABSD is the additional layer that may or may not apply depending on your citizenship status and property count. BSD and ABSD are payable together, within 14 days of signing the OTP.

The History of ABSD in Singapore (2011–2026)

Understanding how we arrived at today’s ABSD rates helps you anticipate where the Government may go next. The key milestones:

December 2011: ABSD introduced. Foreigners paid 10%; entities 10%; SPRs 3% on 2nd property; SCs 3% on 3rd+.

January 2013: First major hike. Foreigners to 15%, entities 15%, SPRs 5%/10%, SCs 7%/10% on 2nd/3rd.

July 2018: Rates raised again amid a reflating market. Foreigners to 20%, entities to 25%.

December 2021: Another round. Foreigners to 30%, entities to 35%, SPR 2nd property to 25%, SC 2nd to 17% / 3rd to 25%.

April 2023: The current regime. Foreigners doubled to 60%, entities to 65%, SPR 2nd to 30%, SC 2nd to 20%.

Each tightening has coincided with a period of accelerating private-residential price growth. For a full chronology including LTV, SSD and TDSR changes, see our comprehensive Property Cooling Measures archive.

How to Legally Minimise Your ABSD Bill

ABSD is not optional, but there are a handful of legitimate strategies buyers use to reduce the amount payable or to avoid triggering higher rates:

Sell first, then buy. For couples upgrading, timing the sale of your existing HDB or condo before the purchase of the next means you never hold two properties simultaneously and therefore pay 0% ABSD on the new first home (as an SC).

Use the matrimonial home remission. A mixed SC–foreigner couple buying their matrimonial home jointly enjoys SC rates if structured correctly.

Decouple responsibly. Where one spouse transfers their share of an existing property to the other, only the transferring spouse is freed to buy a second property as a “first” purchase. Decoupling has legal, CPF refund, and mortgage implications — always take specialist advice first.

Consider commercial or industrial property instead. Commercial and industrial properties do not attract ABSD. They have their own financing, GST, and tax considerations — but for investors focused on yield, they are worth analysing. See our Property Investment section for how commercial yields compare with residential.

Look offshore for second and third properties. Singaporeans investing in Malaysia (JB/Iskandar), Thailand, the UK, Australia, or Japan pay no ABSD to the Singapore Government for those purchases. Each destination has its own foreign-buyer regime, which we cover in our Foreign Property Investment guide.

Time your citizenship/PR application carefully. For families where PR or citizenship is in progress, the ABSD profile at the date the OTP is granted determines the rate. Moving the OTP date by a few weeks can, in edge cases, change the applicable rate by 15–25 percentage points.

Frequently Asked Questions

Is ABSD payable on the land value or the built-up value?

ABSD is calculated on the higher of the purchase price or the market value of the property at the time of acquisition. For new launches, this is typically the purchase price; for resale, IRAS may apply an independent market valuation.

When exactly is ABSD due?

Within 14 days from the date of the document triggering the duty — usually the signing of the Option to Purchase (for resale) or the Sale & Purchase Agreement (for new launches). Late payment attracts penalties.

Can CPF be used to pay ABSD?

No. ABSD (like BSD) cannot be paid from CPF directly at the point of purchase — it must be paid in cash. You can, however, apply for CPF reimbursement after the stamping is complete, drawing from your Ordinary Account against the purchase price.

Do I pay ABSD if I inherit a property?

No. A property acquired by way of inheritance is not a purchase and does not attract ABSD on the transfer itself. However, an inherited property does count toward your property count for future purchases.

I already own a commercial shophouse. Do I pay ABSD on my residential condo?

The residential-only count means commercial and industrial holdings are not included in your ABSD property count. If you are a Singapore Citizen buying your first residential property while owning commercial real estate, you still pay 0% ABSD.

How does ABSD affect an Executive Condominium purchase?

Buying a new EC from the developer under the EC scheme does not attract ABSD during the initial owner-occupation period. Once an EC is privatised (10 years after TOP) and traded on the open market, normal ABSD rules apply.

What to Do Next