MOP first: You must complete a 5-year Minimum Occupation Period (MOP) before subletting your whole HDB flat. For Plus and Prime flats, the MOP is 10 years.

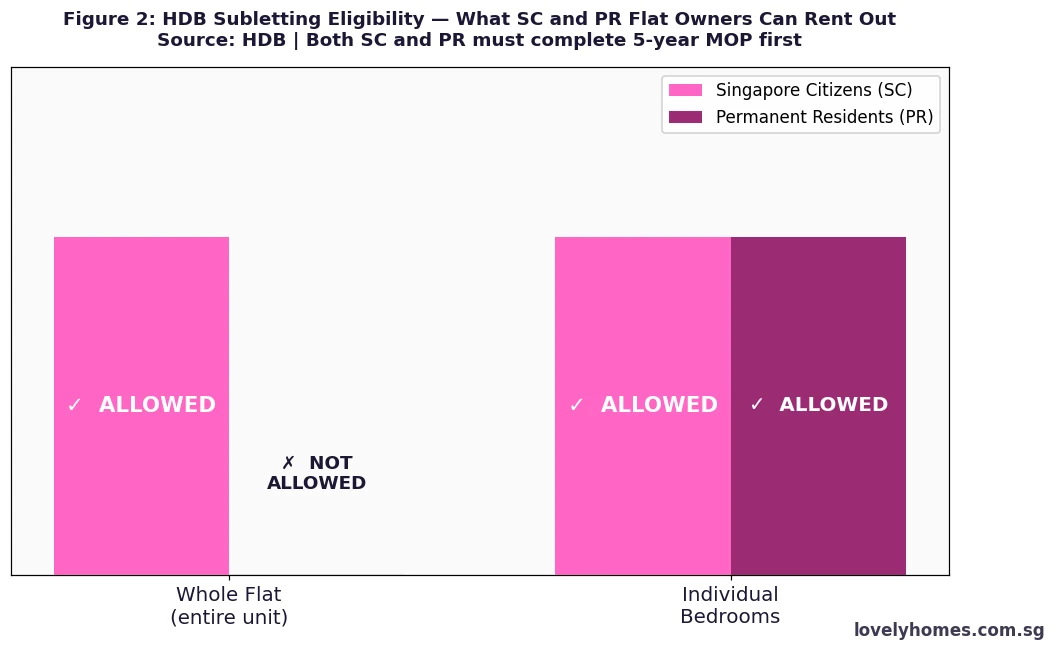

SC only for whole flat: Only Singapore Citizens (SCs) may sublet the entire flat. Singapore Permanent Residents (SPRs) may only rent out individual bedrooms — and must continue living in the flat.

HDB portal approval is mandatory: You must obtain written approval from HDB before the tenant moves in. Apply via SingPass at the HDB e-Services portal. Fee: S$20.

Non-Citizen Quota (NCQ): If your tenant is a non-Malaysian non-citizen, your flat is subject to a quota of 8% (neighbourhood) and 11% (block). Malaysians are exempt.

Subletting duration: Maximum 3 years per approved term for SG/Malaysian tenants; 2 years for other non-citizens. You must re-apply for each renewal.

Income tax: All rental income is taxable. Deductible expenses include mortgage interest, property tax, maintenance fees, and the HDB S$20 subletting fee.

Violation penalties: Subletting without approval or exceeding NCQ can result in fines up to S$5,000 and — in serious cases — compulsory flat acquisition by HDB.

Subletting your HDB flat is one of the most powerful financial options available to Singapore homeowners — but it is also one of the most regulated. The Housing & Development Board (HDB) administers a detailed set of rules under the Housing and Development Act (Cap 129) that govern who can sublet, to whom, for how long, and under what conditions.

This guide explains the regulatory framework for HDB subletting in 2026, from the Minimum Occupation Period (MOP) and the Non-Citizen Quota (NCQ) to the portal approval process, income tax obligations, and penalty regime. It complements our HDB Rental Landlord Guide 2026, which covers the practical experience of finding and managing tenants.

Who Can Sublet an HDB Flat — and What?

HDB imposes a strict eligibility framework based on your citizenship status and how long you have owned the flat.

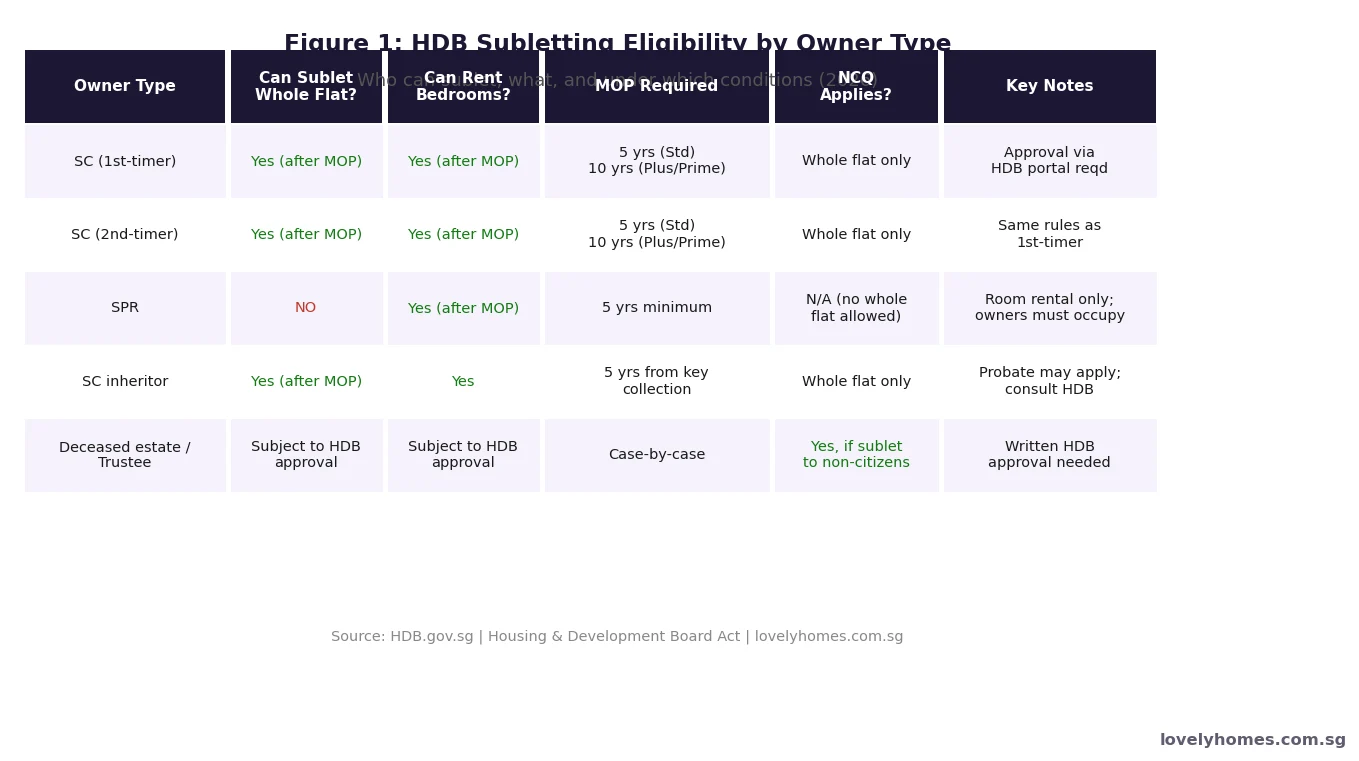

Figure 1: HDB Subletting Eligibility by Owner Type (2026). SC flat owners may sublet the whole flat after MOP; SPRs are restricted to bedroom rental only. Click to enlarge.

Singapore Citizens (SCs)

SC flat owners who have completed the MOP may sublet the entire flat or rent out individual bedrooms. When subletting the whole flat, HDB portal approval is required before the tenant moves in. When renting out bedrooms, no formal approval is needed — but you must continue to live in the flat, and you must notify HDB within 7 days of any new tenant commencing occupancy.

Singapore Permanent Residents (SPRs)

SPRs may not sublet the whole flat at any time. This rule has been in place since January 2003 and reflects the policy intent that SPRs should personally occupy their subsidised flat. SPRs may, however, rent out individual bedrooms after the MOP — provided the SPR owner continues to reside in the flat. The Non-Citizen Quota does not apply to bedroom rental (see below).

MOP: The First Gatekeeper

The Minimum Occupation Period is the most fundamental restriction. For Standard and Plus flats, the MOP is 5 years from the date of key collection (not from application date or booking date). For Prime flats (under the PLH Model, including flats in Bishan, Bukit Merah, Toa Payoh, and other central locations), the MOP is 10 years. During the MOP, neither whole-flat subletting nor room rental is permitted. Owners who violate this rule face the possibility of compulsory flat acquisition at below-market value.

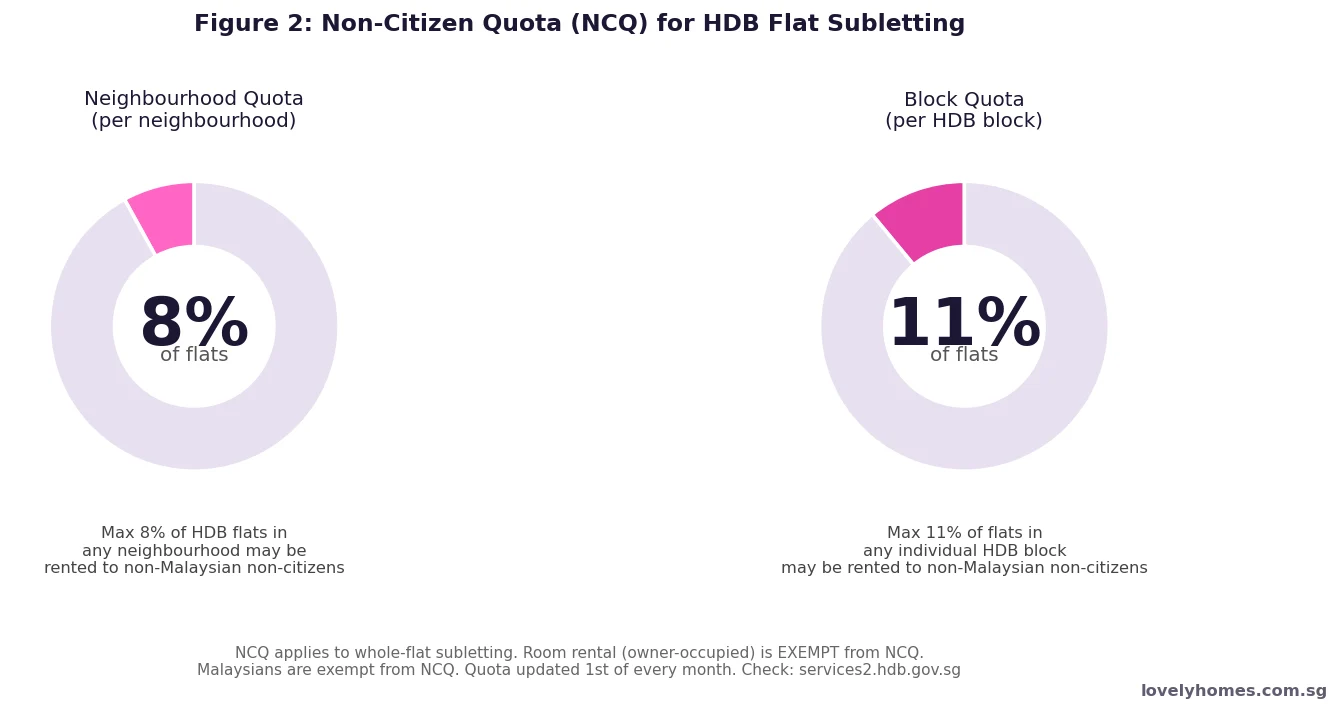

The Non-Citizen Quota (NCQ)

Introduced on 16 January 2014 to prevent the formation of foreigner enclaves in HDB estates, the NCQ applies whenever a SC owner sublets the whole flat to one or more non-Malaysian non-citizen tenants.

Figure 2: NCQ limits — 8% of flats in any neighbourhood and 11% in any HDB block may be rented to non-Malaysian non-citizens. Room rental (owner-occupied) is exempt. Click to enlarge.

How the NCQ Works

The Non-Citizen Quota operates at two levels. At the neighbourhood level, no more than 8% of HDB flats may be sublet (whole flat) to non-Malaysian non-citizen tenants. At the block level, the cap is 11%. HDB updates the quota availability on the first day of every month. If your block or neighbourhood has already reached the cap, you can still sublet — but only to Singapore Citizens, SPRs, or Malaysians.

Who is Exempt from NCQ?

Malaysian nationals are explicitly exempt from the NCQ, reflecting Singapore’s historical and social ties with Malaysia. Room rental (where the owner continues to reside in the flat) is also exempt regardless of the tenant’s nationality — the rationale being that the owner’s continued presence moderates the risk of foreigner concentration. The NCQ does not apply to private residential property.

Checking Your NCQ Status

Before committing to a non-Malaysian non-citizen tenant, check the NCQ status at services2.hdb.gov.sg/webapp/BR12AWNCQuota/. Enter your block and street name. If the quota is exhausted at either neighbourhood or block level, you cannot proceed with a non-Malaysian non-citizen tenant until the quota resets (typically when another flat in the quota pool transitions back to a citizen household).

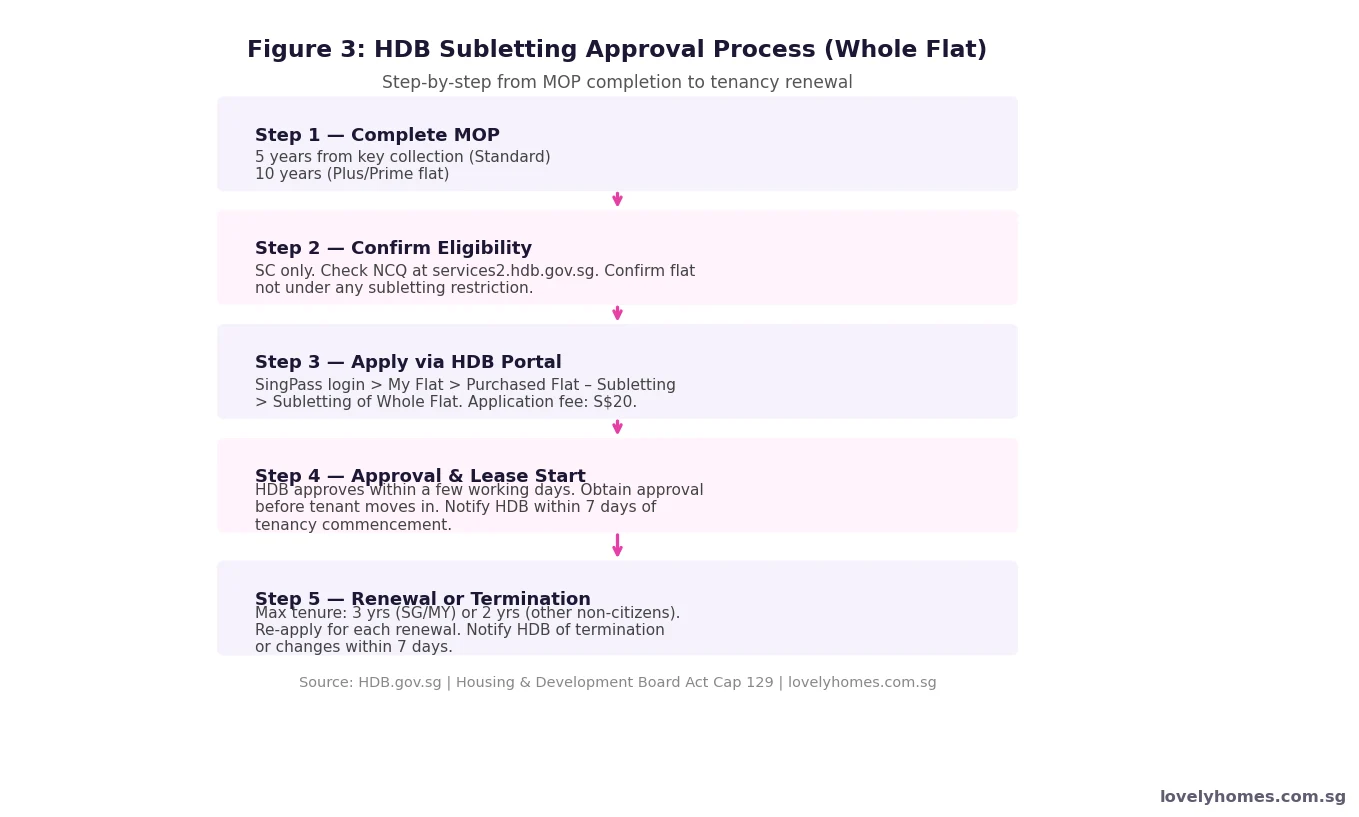

The HDB Subletting Approval Process

The approval process for whole-flat subletting is fully digital and administered through HDB’s e-Services portal. Bedroom rental operates under a lighter-touch notification regime.

Figure 3: HDB Whole-Flat Subletting — Step-by-Step Approval Process (2026). Five stages from MOP completion to renewal. Click to enlarge.

Whole-Flat Subletting: Step-by-Step

After completing the MOP and confirming NCQ eligibility, the owner logs in to the HDB portal via SingPass and navigates to My Flat > Purchased Flat – Subletting > Subletting of Whole Flat. The application requires the proposed tenant’s particulars (NRIC/FIN), intended tenancy start and end dates, and rental amount. The application fee is S$20, payable online. HDB typically approves within a few working days. The tenant must not move in before approval is received. Once approved, the owner must notify HDB within 7 days of the tenancy commencement date.

Bedroom Rental: Notification Only

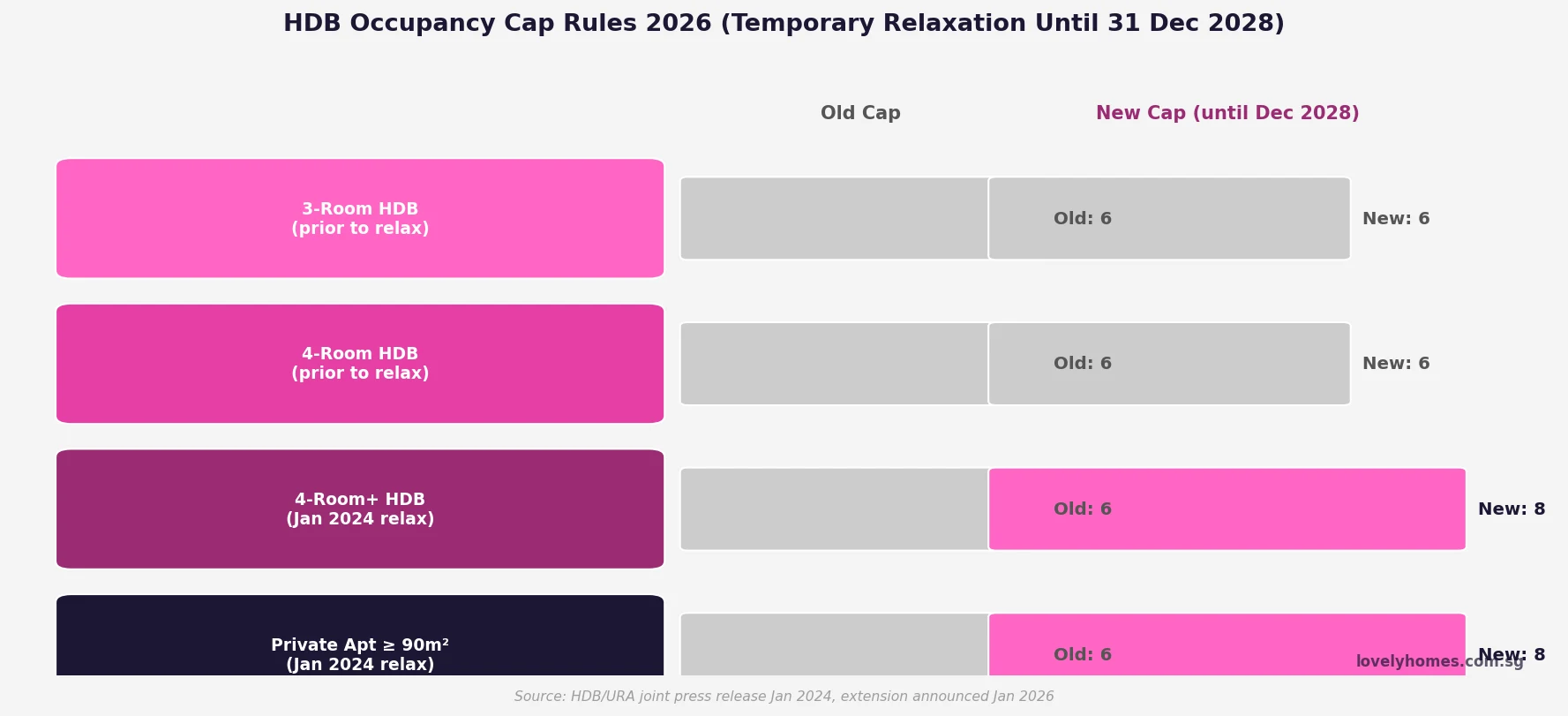

Renting out individual bedrooms — where the owner continues to reside in the flat — does not require prior HDB approval. However, the owner must still register the tenant with HDB via the portal and is responsible for ensuring the flat’s total occupancy does not exceed the permitted cap. As at 2026, the occupancy cap is relaxed to 8 persons per flat (extended until 31 December 2026 under a temporary government measure; previously 6 persons).

Subletting Duration and Renewal

Approval for whole-flat subletting is granted for a fixed term, capped at:

Tenant Nationality

Maximum Approved Term

Renewal

Singapore Citizens

3 years per term

Re-apply at end of each term

Malaysian nationals

3 years per term

Re-apply at end of each term

Other SPRs

2 years per term (subject to NCQ)

Re-apply; NCQ checked at renewal

Non-resident foreigners (Work Pass, EP, etc.)

2 years per term (subject to NCQ)

Re-apply; NCQ checked at renewal

Tourism/Short-Stay visitors

NOT PERMITTED (min 6 months)

N/A — illegal under URA rules

There is no limit on the number of consecutive renewals, provided eligibility requirements (MOP, NCQ, owner criteria) are met at the time of each renewal application. Owners must also notify HDB within 7 days of any early termination, change of tenant, or change in the number of occupants.

Income Tax on Rental Income

All rental income from HDB subletting is subject to Singapore income tax under the Income Tax Act (Cap 134). Rental income must be declared in your annual income tax return. The net rent (gross rent minus allowable deductions) is added to your total assessable income and taxed at the applicable progressive personal income tax rate.

Allowable Deductions Against Rental Income

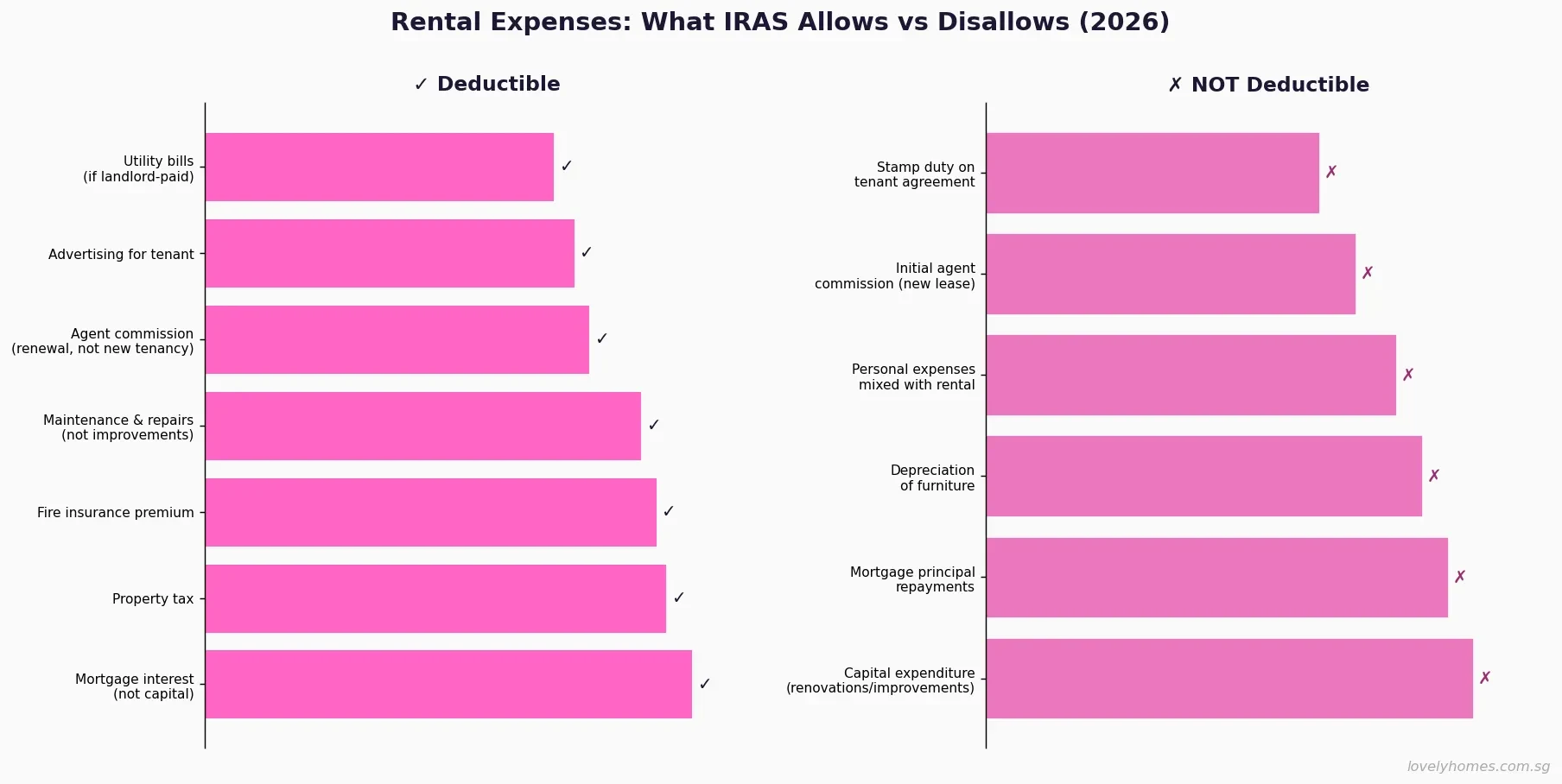

IRAS permits the following as deductible expenses against HDB rental income: mortgage interest (the interest component only, not principal repayment); property tax (the annual property tax liability, not stamp duty); maintenance and conservancy charges (S&CC/management fees paid to HDB); cost of repairs and maintenance directly related to the rental; insurance premiums for the property; and the HDB S$20 subletting application fee. Furniture and fittings are not deductible as capital expenditure, though rental of furnished rooms may allow partial deduction under IRAS practice guidelines. Pre-letting expenses (advertising, agent fees) are generally deductible if the property is subsequently let.

Item

Deductible?

Notes

Mortgage interest

Yes

Interest component only; principal is not deductible

Property tax

Yes

Annual property tax, not BSD/ABSD

S&CC (conservancy charges)

Yes

Monthly HDB town council charges

Repairs and maintenance

Yes

Must be directly related to rental unit

HDB subletting application fee

Yes

S$20 per application

Property agent commission

Yes

Where incurred to secure rental

Furniture / fittings

Generally No

Capital expenditure; check IRAS guidelines

Mortgage principal

No

Capital repayment, not an expense

Worked Example: Calculating Net Rental Income

Mr and Mrs Tan are SC joint owners of a 4-room HDB flat in Tampines. They collected keys in April 2019, completing their 5-year MOP in April 2024. In January 2025, they moved to their new condo and applied to sublet the whole HDB flat. In February 2025, they secured a Malaysian couple as tenants at S$3,200 per month on a 2-year lease.

Gross rental income (12 months): S$3,200 × 12 = S$38,400 Less deductions:

Mortgage interest component (~S$4,800 p.a.): −S$4,800

Property tax (owner-occupier rate does not apply once sublet; AV ~S$18,000, 10% = S$1,800): −S$1,800

S&CC town council charges (~S$70/mth × 12): −S$840

HDB subletting application fee: −S$20

Agent commission (half month): −S$1,600 Net assessable rental income: S$38,400 − S$9,060 = S$29,340

This is added to their other income for YA 2026 tax assessment. At the 7% personal income tax rate (income band), the additional tax payable is approximately S$2,054 per joint owner — a manageable cost relative to the gross S$38,400 rental earned.

Note: As Malaysians, the tenants are exempt from NCQ, so the block and neighbourhood quota check was not a constraint for this tenancy.

Violations: Penalties and Enforcement

HDB takes unauthorised subletting seriously. The Housing and Development Act empowers HDB to take action against flat owners who violate subletting rules. The penalty regime in 2026 is as follows.

For subletting without HDB approval, or subletting to ineligible occupants, owners face a fine of up to S$5,000 per offence. For repeat or serious violations — particularly renting to short-stay tourists, platforms such as Airbnb (which facilitates short-term stays of less than 3 months, prohibited under URA rules), or falsifying tenant particulars — HDB may proceed to compulsorily acquire the flat at below-market value. The owner loses all equity above the acquisition price and is barred from purchasing another HDB flat for a period. As at 2026, IRAS has also announced enhanced data-sharing with HDB to identify undeclared rental income.

Why This Matters: Subletting as a Financial Strategy

For HDB owners who have completed the MOP and moved to private property, subletting transforms a public housing asset into a yield-bearing investment. As at Q1 2026, HDB median rental yields sit at approximately 5.1–5.9% gross across flat types (see our Singapore Rental Market Guide 2026). At S$3,000–S$3,500 per month for a typical 4-room flat, the gross annual return of S$36,000–S$42,000 on a flat worth S$450,000–S$550,000 is materially better than most other asset classes available to retail investors in Singapore.

However, the regulatory framework means that subletting is only accessible to SC owners after MOP. SPRs are permanently limited to room rental — a significant constraint that affects SPRs’ ability to monetise their HDB assets. This distinction underlies much of the debate about SPR property rights in Singapore.

What Might Come Next

Based on policy trends and parliamentary discussions in 2025–2026, a few developments are worth watching. First, the temporary 8-person occupancy cap relaxation (extended to 31 December 2026) may be made permanent if government data shows no adverse outcomes. Second, HDB has indicated ongoing review of whether the Plus flat MOP of 10 years is calibrated correctly — earlier parliamentary questions have probed whether the 10-year rule unduly restricts owners’ flexibility. Third, with IRAS cross-referencing rental data more actively, there may be more enforcement actions on undeclared HDB rental income in YA 2027 tax filings. Flat owners who have been subletting informally should consider voluntary disclosure before enforcement activity increases.

Frequently Asked Questions

Can I start renting out my HDB flat before the MOP ends if I get a job overseas?

No. The MOP is an absolute bar on whole-flat subletting, regardless of your reason for not occupying the flat. HDB does not grant hardship exemptions for overseas deployment. If you are posted overseas, your options are to leave the flat occupied by a family member who is listed as an occupier, apply to HDB under the Temporary Absence Scheme (which covers eligible work, study, or national service postings), or sell the flat if you meet the resale conditions. Any subletting before the MOP is complete constitutes a violation under the Housing and Development Act and can result in compulsory acquisition.

I am an SPR — can I ever sublet my whole HDB flat?

No. SPRs are not permitted to sublet the whole flat at any time, regardless of how long they have owned the flat. This policy has been in place since January 2003. SPRs may rent out individual bedrooms after the MOP is completed, provided the SPR continues to reside in the flat. If an SPR subsequently renounces PR status and obtains Singapore Citizenship, they are thereafter entitled to apply for whole-flat subletting approval after the MOP — but the MOP clock does not restart on citizenship acquisition.

What happens if my block has reached the NCQ limit — can I still rent to a non-citizen?

If either the neighbourhood or block NCQ has been reached, you may only sublet to Singapore Citizens, SPRs (who are counted differently), or Malaysian nationals (who are exempt from NCQ). You can check the current quota at the HDB Non-Citizen Quota enquiry service. The quota is updated on the first of every month. If a flat in your block that was previously rented to a non-Malaysian non-citizen reverts to owner-occupancy or is rented to a Singapore Citizen, the quota frees up and your flat may become eligible again. There is no waiting list — availability is on a first-come, first-served basis each month.

I rented out my HDB flat but did not declare the income on my tax return. What should I do?

You should make a voluntary disclosure to IRAS as soon as possible. IRAS’s Voluntary Disclosure Programme provides significantly reduced penalties for taxpayers who come forward before IRAS initiates an audit or investigation. Penalties for non-disclosure can be as high as 200% of the underpaid tax under the Income Tax Act. The fact that HDB has your subletting approval on record means IRAS can cross-reference subletting approvals against tax filings. Voluntary disclosure typically results in penalties of 5–10% of underpaid tax rather than the full quantum. You should engage a tax adviser or the IRAS Taxpayer Services Centre before making the disclosure.

Can I use Airbnb or short-term rental platforms to rent out my HDB flat?

No. Short-term rentals of residential property for periods of less than 3 consecutive months are prohibited under the Urban Redevelopment Authority (URA) regulations in Singapore. This prohibition applies to all residential property — HDB flats, condominiums, landed houses, and private apartments — and has been in force since 2017. Any listing on Airbnb, Booking.com, Agoda, or similar platforms that facilitates stays of fewer than 3 months constitutes a violation. Penalties include fines of up to S$200,000 for owners and up to S$20,000 for tenants. URA actively monitors short-term rental listings and has prosecuted multiple flat owners. The only exception is licensed hotels, serviced apartments, and other accommodation types that have explicit URA approval for short-stay use.

If my tenant damages the flat, is there any HDB recourse?

HDB does not arbitrate tenancy disputes between owners and tenants — this is a private civil matter. Your recourse is through the civil courts (Small Claims Tribunal for disputes up to S$20,000, or the Magistrate’s Court for larger claims). For this reason, collecting a security deposit equivalent to one month’s rent per year of lease (market convention in Singapore) is strongly advisable. You should also document the condition of the flat thoroughly before handover with time-stamped photographs and an inventory list signed by the tenant. If the damage is severe, you may also need to report it to HDB (e.g., structural damage, illegal modifications) as owners remain responsible for the physical condition of the flat under the terms of the HDB lease.

What is the minimum tenancy period for renting an HDB flat?

HDB requires a minimum tenancy of 6 months for the whole flat and a minimum of 6 months for individual bedrooms. HDB does not permit month-to-month tenancies or shorter leases. The URA’s 3-month minimum rule for short-stay is a separate, lower bar — HDB’s own minimum is 6 months and takes precedence. Market convention in Singapore is for 1-year or 2-year leases, which offer landlords stability and tenants cost certainty. Leases shorter than 12 months attract stamp duty at 0.4% of the total rent for the lease period (payable within 14 days of signing), which the parties may apportion by agreement.

Related Articles

Further Reading: HDB Rules and Rental in Singapore

Disclaimer: This article provides general information about HDB subletting rules as at June 2026 based on publicly available information from the Housing & Development Board (HDB.gov.sg), the Inland Revenue Authority of Singapore (IRAS.gov.sg), the Urban Redevelopment Authority (URA.gov.sg), and the Housing and Development Act (Cap 129). Rules, quotas, and penalty provisions may be amended by the relevant authorities at any time. This article is not legal or tax advice. Readers should verify current requirements with HDB directly, and consult a licensed property agent, qualified lawyer, or tax professional before taking any action.

Quick Answer: Renting Out Your HDB Flat 2026 — Key Facts

Who can sublet the whole flat? Singapore Citizens (SC) only. Permanent Residents (PR) may only rent out individual bedrooms — not the entire flat.

Minimum Occupation Period (MOP): 5 years from the date of key collection before subletting is permitted. Older flats purchased before 30 August 2010 without a grant have a 3-year MOP.

Minimum lease term: 6 months per tenancy agreement for whole-flat rental. No minimum for bedroom rental.

Non-Citizen Quota: 8% at neighbourhood level and 11% at block level. Applies when any tenant renting the whole flat is a non-Malaysian non-citizen.

Occupancy cap (temporarily relaxed): Up to 8 unrelated persons in a 4-room or larger HDB flat (relaxed from 6 until 31 December 2026).

HDB approval required: Flat owners must register the subletting with HDB online before tenants move in. Failure is a serious offence.

Rental yields: Approximately 5–7% gross depending on flat type and estate.

Can You Rent Out Your HDB Flat?

HDB flats in Singapore can be rented out, but the rules are considerably more prescriptive than for private residential property. The framework is administered by HDB under the Housing and Development Act (Cap 129), and non-compliance can result in severe penalties including compulsory acquisition of the flat. The rules distinguish sharply between who can rent (citizenship status), what can be rented (whole flat versus individual bedrooms), who the tenants can be (nationality quotas), and for how long (minimum tenancy periods).

Before considering subletting, flat owners should also understand how rental income interacts with their CPF, ABSD obligations, and income tax position — particularly if they have moved out to live elsewhere. This guide covers the complete picture for Singapore Citizens and Permanent Residents who own an HDB flat and wish to generate rental income from it.

Who is Eligible to Sublet?

The eligibility rules operate at two levels: (1) who can sublet the entire flat, and (2) who can rent out individual bedrooms.

Singapore Citizens (SC) may sublet their entire flat or individual bedrooms, subject to completing the MOP and receiving HDB’s approval for each subletting period. The flat owner does not need to live in the flat during the subletting period — they may reside elsewhere, including in private property, for the duration.

Permanent Residents (PR) may rent out individual bedrooms in their HDB flat, but may NOT sublet the entire flat. If a PR owns an HDB flat, the PR (or at least one listed owner) must continue to reside in the flat at all times while bedrooms are being rented out. PRs who wish to vacate entirely and rent out the whole flat must either sell the flat or apply for an SC-sponsored transfer — there is no exception.

Both SC and PR flat owners must have completed the applicable MOP before any subletting (whole flat or bedroom) is permitted.

Minimum Occupation Period (MOP) Before Subletting

The MOP is the most fundamental gating requirement for HDB subletting. It runs from the date of key collection (not purchase date) and applies to all flats regardless of whether they were purchased directly from HDB (BTO/DBSS) or on the open resale market with a grant:

Standard MOP (most flats): 5 years from key collection. Applies to all BTO flats, DBSS, and resale flats purchased with a CPF housing grant.

Shortened MOP: 3 years for resale flats purchased before 30 August 2010 without any housing grant. Very few flats remain in this category.

Plus and Prime flats: 10-year MOP. These are flats in highly sought-after locations announced under the 2023 HDB classification framework. Subletting the whole flat is not permitted even after the 10-year MOP — only bedroom rental is allowed for Plus and Prime flat owners.

Note that any period during which the flat was unoccupied (e.g., the owner lived overseas for work) may be deducted from the MOP clock by HDB in certain circumstances — check with HDB directly if this situation applies to you.

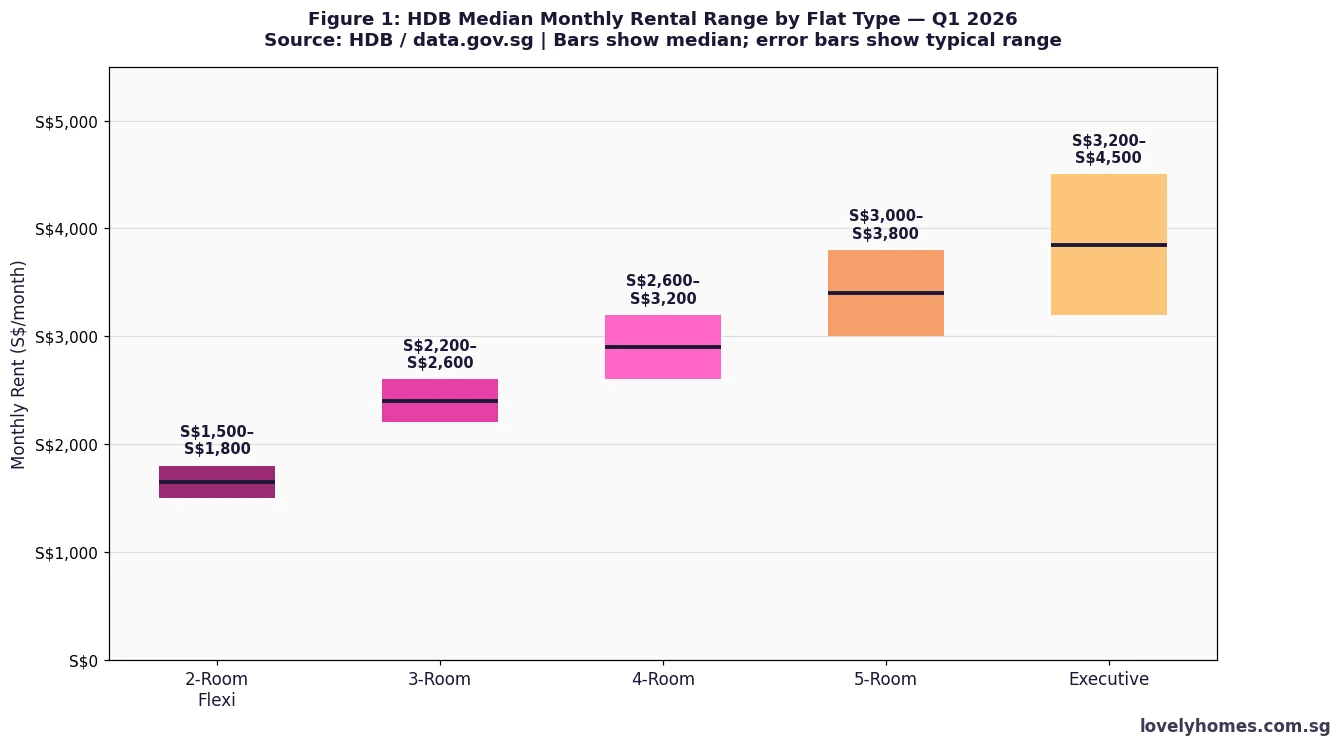

HDB Rental Rates in 2026

HDB rental rates have risen meaningfully since the pandemic-era demand surge, with median rents across all flat types up approximately 3.2% year-on-year as of Q1 2026. The chart below shows the typical monthly rental range by flat type across Singapore:

Figure 1: HDB Median Monthly Rental Range by Flat Type — Q1 2026 | Source: HDB / data.gov.sg | Bars show range; horizontal line shows median

These are Singapore-wide medians — estate location significantly affects achievable rents. Central estates (Toa Payoh, Bishan, Queenstown) typically command 15–25% premiums over the national median for the same flat type. Outer estates (Woodlands, Sembawang, Choa Chu Kang) trade at 5–15% discounts. The temporary relaxation of the occupancy cap to 8 unrelated persons (until 31 December 2026) has supported demand from shared accommodation arrangements, particularly in the co-living segment.

Non-Citizen Subletting Quota

To maintain the ethnic and community character of HDB estates, HDB imposes a Non-Citizen Quota (NCQ) on whole-flat subletting:

Level

Quota

What It Means

Neighbourhood

8%

No more than 8% of flats in the neighbourhood may be sublet to non-Malaysian non-citizen tenants

Block

11%

No more than 11% of flats in the block may be sublet to non-Malaysian non-citizen tenants

Source: HDB | Quota does not apply to bedroom rental — only whole-flat subletting.

Malaysian nationals are excluded from the NCQ calculation — a legacy of the historical close ties between Singapore and Malaysia. If the NCQ for your block or neighbourhood has been reached, you may only sublet your flat to Singaporean or Malaysian tenants. You can check the current NCQ status for any block through the HDB e-Services portal before entering into a tenancy agreement.

The NCQ is particularly relevant in popular expat neighbourhoods (Queenstown, Tiong Bahru, Toa Payoh) and around MRT hubs, where demand from foreign professionals is high. Landlords in these estates should monitor the NCQ status regularly — it changes as tenancy agreements expire and new ones begin.

Occupancy Cap — Temporarily Relaxed Until 31 December 2026

In January 2024, the Government temporarily relaxed the maximum number of unrelated occupants in larger HDB flats and private residential properties to address tight rental market conditions for foreign workers and students. As at 7 June 2026, this relaxation remains in effect:

Landlords of larger flats who wish to maximise occupancy for room-rental models should note that the occupancy cap reverts to 6 persons on 1 January 2027 unless HDB announces a further extension. Co-living operators using HDB flats as their supply base are particularly exposed to this change.

How to Apply — The Subletting Process

The subletting process involves HDB approval before tenants can move in. Here is the step-by-step workflow for a whole-flat subletting:

Confirm MOP has been satisfied: Check your key collection date and ensure 5 years have passed. Do not sign any tenancy agreement until the MOP is complete.

Confirm eligibility: Ensure you are an SC flat owner. Confirm all registered owners consent to the subletting.

Check NCQ status: Log in to HDB e-Services to confirm the NCQ for your block and neighbourhood is not fully utilised if you plan to rent to non-Malaysian non-citizens.

Negotiate and sign a tenancy agreement: The minimum tenancy period for a whole flat is 6 months. You may sublet for up to 3 years at a time, subject to renewal approval from HDB.

Register the subletting with HDB: Submit the subletting application online via HDB e-Services before the tenants move in. Provide tenants’ details (NRIC/FIN, nationality, employment pass type if applicable). This is a statutory requirement — failure to register before tenants move in is a breach of the Housing and Development Act.

Receive HDB approval: HDB will issue a confirmation letter (typically within a few working days for compliant applications). Retain this letter for your records.

Collect rent and manage the tenancy: Issue a proper tenancy agreement. Collect a security deposit (typically 1–2 months rent). Stamp the tenancy agreement via IRAS e-Stamping (stamp duty on rental: 0.4% of total rent for leases exceeding one year).

Renewal: Notify HDB and apply for renewal before each renewal period. HDB re-checks eligibility and NCQ at each renewal.

Rental Yield Analysis — Is Renting Out Worth It?

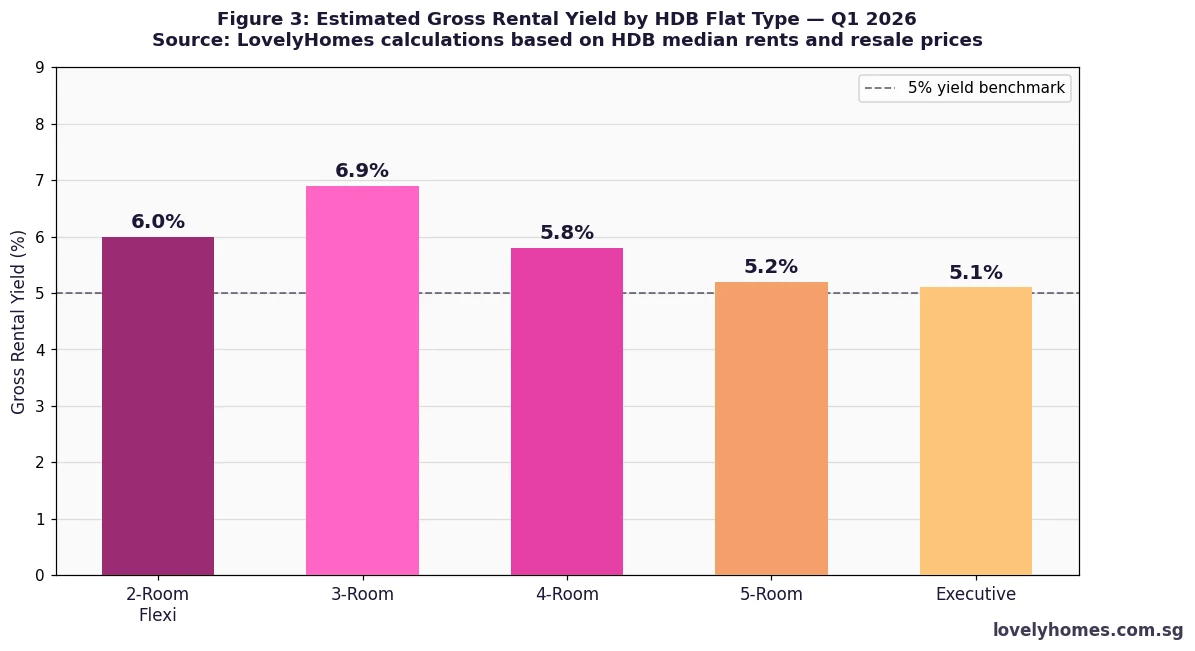

Figure 3: Estimated Gross Rental Yield by HDB Flat Type — Q1 2026 | Source: LovelyHomes calculations based on HDB median rents and resale prices

Gross rental yields on HDB flats are among the highest of any property class in Singapore, ranging from approximately 5.1% to 6.9% depending on flat type. Smaller flats (2-room, 3-room) generate higher yields relative to their resale values because rents have not declined proportionately with the relatively lower price points. Larger flats (5-room, Executive) generate lower percentage yields but higher absolute monthly income.

Net yields — after property tax, maintenance fees, and occasional void periods — are typically 0.5–1.0 percentage points lower than gross. At 5–6% net yield, HDB flats compare favourably to private condo yields (typically 3–4% net) and offer a meaningful income return for SC flat owners who have upgraded to private property and retained their HDB flat — a common wealth-building strategy for Singapore families, subject to ABSD on the second property.

Summary Table: HDB Whole-Flat vs Bedroom Rental — Key Differences

Rule

Whole-Flat Rental

Bedroom Rental

Who can sublet

Singapore Citizens only

SC and PR flat owners

Owner must reside in flat

No — owner may live elsewhere

Yes — PR owner must remain in flat

Minimum lease

6 months

No statutory minimum

Maximum subletting period

3 years (renewable)

No statutory maximum per term

Non-Citizen Quota

Yes — 8%/11% (neighbourhood/block)

Not applicable

HDB approval required

Yes — before tenants move in

Yes — must register bedroom tenants

Tenancy stamp duty

0.4% of total rent (IRAS)

0.4% of total rent (IRAS)

Income tax on rental income

Yes — reportable to IRAS

Yes — reportable to IRAS

Source: HDB / IRAS | As at 7 June 2026.

Worked Example: Mr and Mrs Tan Rent Out Their Toa Payoh HDB Flat

Mr and Mrs Tan, both Singapore Citizens, purchased a 4-room HDB flat in Toa Payoh in June 2018 and collected keys in September 2021. They completed their 5-year MOP in September 2026. Having upgraded to a private condominium in Bishan in April 2026 (paying ABSD as a second property purchase), they wish to sublet their HDB flat for rental income to help service the new mortgage.

Rental market check: A 4-room HDB in Toa Payoh commands S$2,800–S$3,200/mth. They aim for S$3,000/mth.

NCQ check: Their block in Toa Payoh Lorong 2 has NCQ utilisation at 6% (neighbourhood) and 9% (block) — both below the 8%/11% thresholds. They can rent to non-Malaysian non-citizens.

Process: They sign a 12-month tenancy agreement at S$3,000/mth with an expatriate family. Security deposit: S$6,000 (2 months). Tenancy stamp duty: 0.4% x S$3,000 x 12 months = S$144, payable to IRAS. They register the subletting with HDB before the tenants move in.

Financials:

Annual rental income: S$36,000

Property tax on rented-out flat (annual value ~S$20,400 x 12% owner-occupier rate — no, since it is now non-owner-occupied, higher rates apply: 10–20% on AV): approximately S$2,040–S$4,080/year

Maintenance fee: approximately S$70–S$80/mth = S$840–S$960/year

Net yield (after property tax and maintenance): approximately 3.7–4.0%

Annual net rental income (approx.): S$29,000–S$31,000

Mr and Mrs Tan must also declare the rental income in their annual personal income tax returns filed with IRAS. They may deduct allowable expenses (property tax, maintenance fees, mortgage interest if the loan relates to the rented property, insurance, agent fees) from the rental income before tax. There is no Capital Gains Tax in Singapore, so future sale proceeds are not taxed.

Why HDB Rental Income Matters — and What It Means for Flat Owners

For Singapore Citizens who have upgraded to private housing and retained their HDB flat, rental income from the HDB flat is one of Singapore’s most tax-efficient income streams. At yields of 5–7% gross and no CGT, a S$600,000 HDB flat generating S$30,000 per year in net rental income represents a meaningful supplement to household income. The key constraint is that such a strategy requires paying ABSD on the private property (currently 20% for SC second property — see our ABSD guide for full rates), which takes years of rental income to recover. The maths works best for SC couples who are certain they want to hold both properties long term.

For SC flat owners who do not own other property — for example, those who travel frequently for work — the ability to rent out the whole flat while living elsewhere provides genuine flexibility. The 6-month minimum tenancy ensures landlords are not trapped in indefinitely short arrangements, while the 3-year maximum subletting period (renewable) provides medium-term income stability.

What Might Change for HDB Rental Rules

This section reflects editorial analysis and is speculative in nature.

The temporary occupancy cap relaxation (from 6 to 8 unrelated persons in larger flats) is set to expire on 31 December 2026. HDB will assess whether rental market conditions continue to justify the relaxation. If the rental market tightens further — driven by continued foreign workforce growth and an undersupply of completed units — the relaxation may be extended. If the private rental market stabilises, it is more likely to revert to 6 persons. Landlords operating shared-accommodation models should not assume the relaxation will continue beyond year-end without official confirmation.

More broadly, the HDB Plus and Prime classification framework (announced in 2023) will progressively bring more units with 10-year MOPs and whole-flat subletting restrictions into the resale pool as these projects complete. Over the next decade, the supply of freely-sublettable HDB flats (i.e., non-Plus, non-Prime flats with completed MOPs) will remain substantial but may not grow as rapidly as the overall HDB stock.

Frequently Asked Questions

I am a PR and want to rent out my whole HDB flat — is this allowed?

No. Permanent Residents are not permitted to sublet the entire HDB flat. PRs may only rent out individual bedrooms in the flat, and must continue to reside in the flat at all times while bedroom tenants are present. If you are a PR and wish to vacate the flat entirely, you must sell the flat on the open market. There is no exception for this rule. If you become a Singapore Citizen after purchasing your flat, you immediately become eligible to sublet the whole flat (subject to MOP completion) — another advantage of SC status for property owners.

Can a foreigner rent an HDB flat in Singapore?

Yes, foreigners may rent HDB flats as tenants. However, the Non-Citizen Quota (8% neighbourhood / 11% block) limits how many HDB flats in any given area can be rented to non-Malaysian non-citizens. If the quota for a block is reached, only Singaporean or Malaysian tenants are permitted. Foreigners should check with potential landlords whether the quota has been reached before committing to a lease. The quota does not apply to bedroom rental — foreigners may always rent individual bedrooms in HDB flats regardless of quota status.

What happens if I rent out my flat without HDB approval?

Subletting without HDB approval is a serious breach of the Housing and Development Act. Penalties include a fine of up to S$5,000 for first offences, and compulsory acquisition of the flat (forced sale at market value with no premium) for repeat or serious offences. HDB conducts periodic estate checks and receives tip-offs from neighbours, so non-compliant landlords are regularly caught. The financial cost of compulsory acquisition — losing the flat at market value with no recourse to negotiate — far outweighs any short-term rental income gained from operating without approval.

Do I need to pay tax on rental income from my HDB flat?

Yes. Rental income from an HDB flat is taxable income in Singapore and must be declared in your annual Income Tax Return filed with IRAS. The income is taxed at your marginal personal income tax rate (ranging from 0% to 24% for residents). You may deduct allowable expenses from the rental income: mortgage interest (if the loan relates to the rented property), property tax, fire insurance, maintenance fees, and agent commission. Wear and tear (depreciation) is not a deductible expense under Singapore tax rules. You are also entitled to a deemed deduction of 15% of the gross rent in lieu of actual expenses if that is simpler. Speak to a tax adviser if your rental income is material. See the IRAS website for the specific guidelines.

Can I rent out my HDB flat on Airbnb or other short-term platforms?

No. Short-term rentals of HDB flats — defined as any rental period of less than 6 months — are strictly prohibited under HDB rules and the Hotels Licensing Act. Platforms like Airbnb, Booking.com, and similar services facilitate short-term stays that would violate the minimum 6-month tenancy requirement for whole-flat subletting. HDB has prosecuted flat owners for Airbnb violations and the consequences are the same as for any unlicensed subletting: fines and potential compulsory acquisition. This prohibition applies to HDB flats; private residential property is governed by separate URA rules (which also generally prohibit short-term lets of under 3 months for most private properties).

What is the stamp duty on a rental agreement for an HDB flat?

Rental agreements for HDB flats (and private residential property) must be stamped via the IRAS e-Stamping Portal within 14 days of signing. The stamp duty rate is 0.4% of the total rent for leases exceeding one year, and 0.2% of the total rent for leases of one year or less. For a typical 12-month lease at S$2,800/mth, the stamp duty is 0.4% x S$33,600 = S$134.40. The duty is conventionally paid by the tenant (as the party receiving the tenancy document), though landlord and tenant may agree otherwise in the tenancy agreement.

My HDB MOP will be completed in 3 months. Can I start looking for tenants now?

You may market the flat and negotiate tenancy terms before the MOP is completed, but you cannot sign a tenancy agreement or submit the HDB subletting application until the MOP date has passed. In practice, the market is aware of this constraint and tenants are generally willing to allow for a short lead time between signing and move-in. A common approach is to agree on the lease terms and execute the tenancy agreement on the day of (or shortly after) MOP completion, with tenants moving in a week or two later — giving time for HDB approval to be received (typically 3–5 working days for compliant applications).

This article is for general informational purposes only and does not constitute legal, tax, or financial advice. HDB policies, occupancy cap rules, and rental regulations can change. Always verify current eligibility conditions, quotas, and approval requirements directly with HDB and consult a qualified Singapore property lawyer or tax adviser before making rental decisions. Rental rates, yields, and government policy cited are based on information available as at 7 June 2026.

Singapore’s residential rental market entered 2026 after two years of adjustment. The extraordinary rental surge of 2022–2023 — when median rents rose by 30–40% driven by returning expatriates, supply disruptions, and a flood of en-bloc proceeds — has given way to a more measured environment. Vacancy rates across private residential properties averaged 7.6% at end-2025 (URA), reflecting a significant influx of completed units from the 2021–2023 pipeline.

Yet demand remains structurally healthy. Singapore’s open-economy model, its position as a regional headquarters hub, and a steady pipeline of work-permit and employment-pass holders keep rental absorption strong in the OCR and mature HDB heartland districts. For first-time landlords considering a buy-to-let strategy, and for tenants navigating a complex regulatory framework, understanding the rules administered by the Housing & Development Board (HDB), the Urban Redevelopment Authority (URA), and the Inland Revenue Authority of Singapore (IRAS) is essential.

HDB Flat Subletting Rules: What Every Landlord and Tenant Must Know

HDB flats are subsidised public housing built for owner-occupation, not investment. Subletting an entire HDB flat — or even individual rooms — is subject to a strict ruleset administered by the HDB under the Housing and Development Act.

Minimum Occupation Period (MOP)

Before a flat owner may sublet the entire flat, the property must have completed its 5-year Minimum Occupation Period (MOP) from the date of key collection. For flats purchased under the Prime Location Public Housing (PLH) or Plus classification introduced under HDB’s new classification system (effective BTO exercises from October 2023), the MOP is 10 years.

Room Rental (Subletting a bedroom)

Room-only subletting — where the owner continues to reside in the flat — is permitted before MOP, subject to occupancy cap rules. From 22 January 2026, the HDB and URA implemented a temporary relaxation of the occupancy cap to allow up to 8 unrelated persons in a flat or private residential property (up from the standard 6), applicable until 22 January 2028.

Key HDB subletting rules at a glance

Minimum tenancy term: 6 consecutive months per subletting period

Maximum subletting term: 3 years per application (renewable)

HDB subletting application must be made online at hdb.gov.sg before the subletting commences

Subtenants must be Singapore Citizens, Permanent Residents, or foreigners with a valid long-term pass (Employment Pass, S Pass, Dependent Pass, Long-Term Visit Pass)

Non-citizen (NR) subletting quota: no more than 8% of the HDB block may be sublet to non-Malaysian foreigners

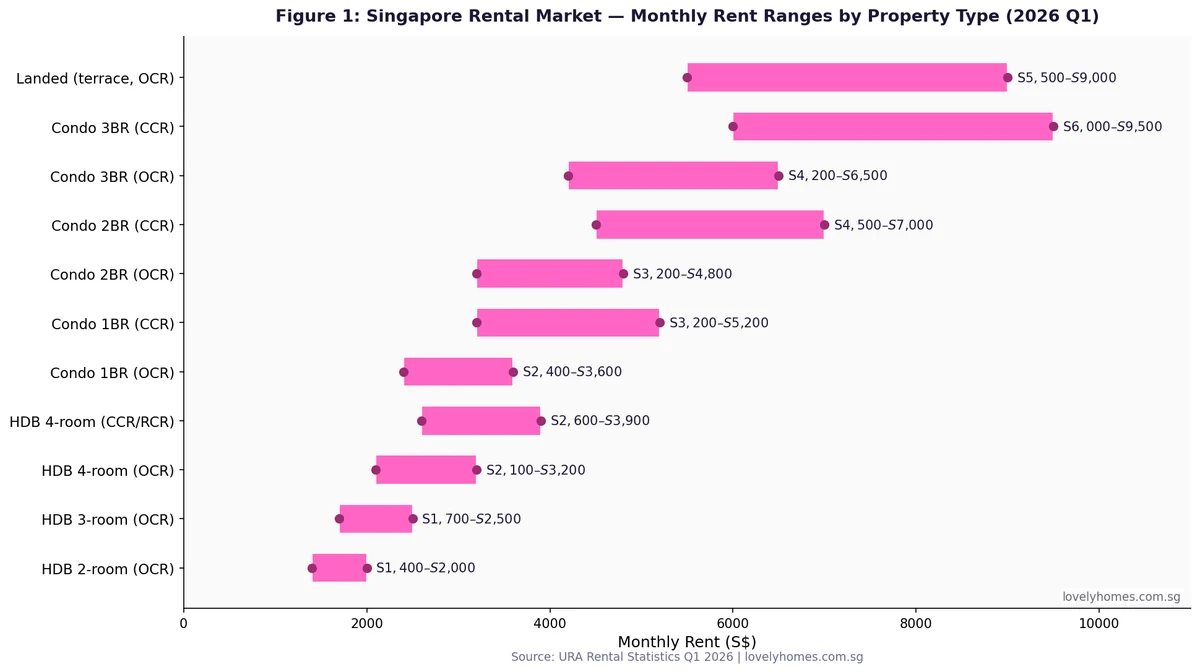

Figure 1: Singapore rental market — monthly rent ranges by property type and location, Q1 2026. Source: URA Rental Statistics.

Private Condo and Landed Property Rental Rules

Private residential properties — condominiums, apartments, and landed houses — are not subject to MOP restrictions. An investor who purchases a newly-launched private condo may sublet the entire unit immediately upon receiving the Temporary Occupation Permit (TOP), subject to two key rules administered by URA:

Minimum tenancy term: 3 consecutive months for private residential properties (compared to 6 months for HDB)

Occupancy cap: The standard cap is 6 unrelated persons per dwelling unit; the temporary relaxation to 8 persons applies through January 2028

Short-term rental prohibition: Platforms such as Airbnb and similar short-stay apps are prohibited for private residential properties in Singapore. Rental terms below 3 months are illegal and carry fines of up to S$5,000

Landed properties — terraced houses, semi-detached, and bungalows — follow private property rules (3-month minimum, no MOP). Foreign ownership of landed property is restricted under the Residential Property Act 1976, but foreigners may rent any landed home freely.

Rental Rates in 2026: What to Budget as a Tenant

Singapore’s rental market is priced according to property type, location (CCR/RCR/OCR), floor level, condition, and proximity to MRT stations. The data below reflects URA and HDB Rental Statistics for Q1 2026. All figures are monthly rents in Singapore dollars.

Property Type

Location

Typical Monthly Rent

Indicative PSF

HDB 2-room

OCR

S$1,400–S$2,000

S$3.0–S$4.2

HDB 3-room

OCR

S$1,700–S$2,500

S$2.8–S$3.8

HDB 4-room

OCR (mature)

S$2,100–S$3,200

S$2.6–S$3.5

HDB 4-room

CCR/RCR (Bishan, Toa Payoh)

S$2,600–S$3,900

S$3.2–S$4.2

Condo 1BR

OCR

S$2,400–S$3,600

S$4.2–S$5.5

Condo 1BR

CCR

S$3,200–S$5,200

S$5.5–S$8.0

Condo 2BR

OCR

S$3,200–S$4,800

S$3.8–S$5.2

Condo 2BR

CCR

S$4,500–S$7,000

S$5.8–S$8.5

Condo 3BR

OCR

S$4,200–S$6,500

S$3.5–S$5.0

Landed terrace

OCR

S$5,500–S$9,000

S$2.8–S$4.5

Stamp Duty on Tenancy Agreements

In Singapore, the tenant bears the cost of stamping the Tenancy Agreement (TA) via IRAS e-Stamp within 14 days of signing. The stamp duty rate is:

For leases of 4 years or less: S$4 for every S$250 (or part thereof) of the total rent payable over the term

For leases exceeding 4 years (or indefinite term): calculated on the higher of total rent or 4× annual rent, at the same rate

Example: A 2-year tenancy at S$3,500/month = S$84,000 total rent. Stamp duty = S$84,000 ÷ S$250 × S$4 = S$1,344. This must be paid via the IRAS e-Stamping portal at iras.gov.sg.

Rental Yield and Investment Performance

For property investors, gross rental yield is calculated as annual rent divided by purchase price. Singapore’s rental yields have compressed over the past decade as capital values outpaced rent growth, yet certain property types and locations still offer respectable returns — particularly HDB-adjacent OCR condos near MRT nodes and mature-town HDB resale flats after MOP.

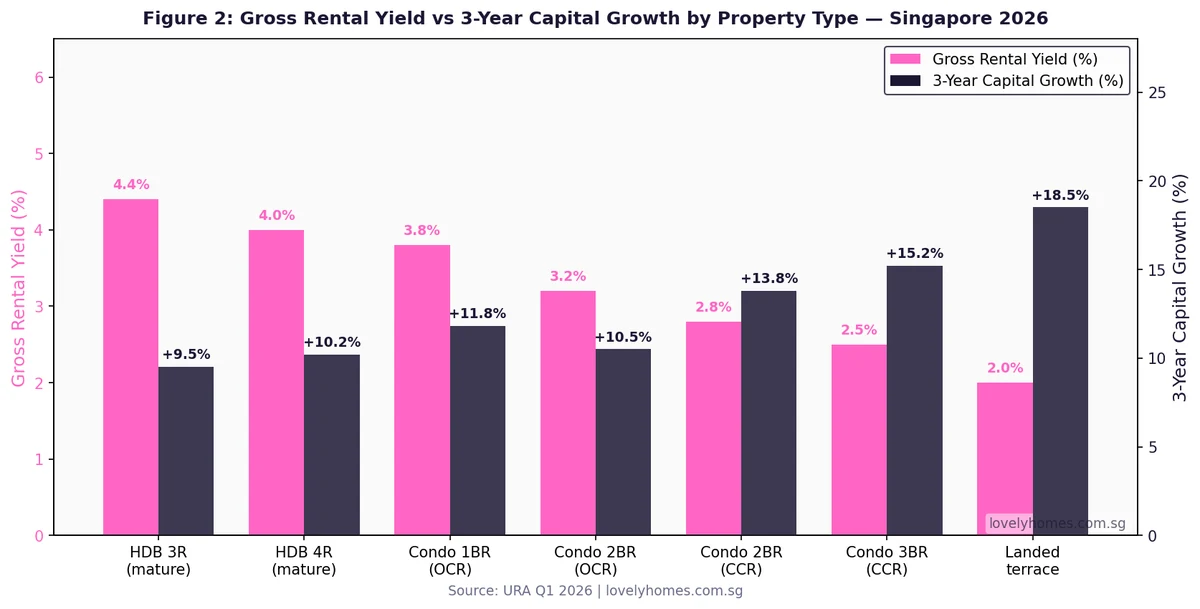

Figure 2: Gross rental yield vs 3-year capital growth by property type — Singapore Q1 2026. Source: URA / lovelyhomes.com.sg research.

HDB resale flats offer the highest gross rental yields (4.0–4.4%) among mainstream property types, owing to relatively affordable purchase prices and sustained heartlander demand. Private condo yields are lower (2.5–3.8%), but the CCR segment benefits from stronger long-term capital growth — up to +15.2% over three years for CCR 3-bedroom units — driven by the irreplaceable land scarcity in Districts 9–11. Landed property yields are modest (2.0%) but capital growth is exceptional (+18.5%), reflecting the structural restriction on new landed supply in Singapore.

PSF Benchmarks and Vacancy Rates Across the Market

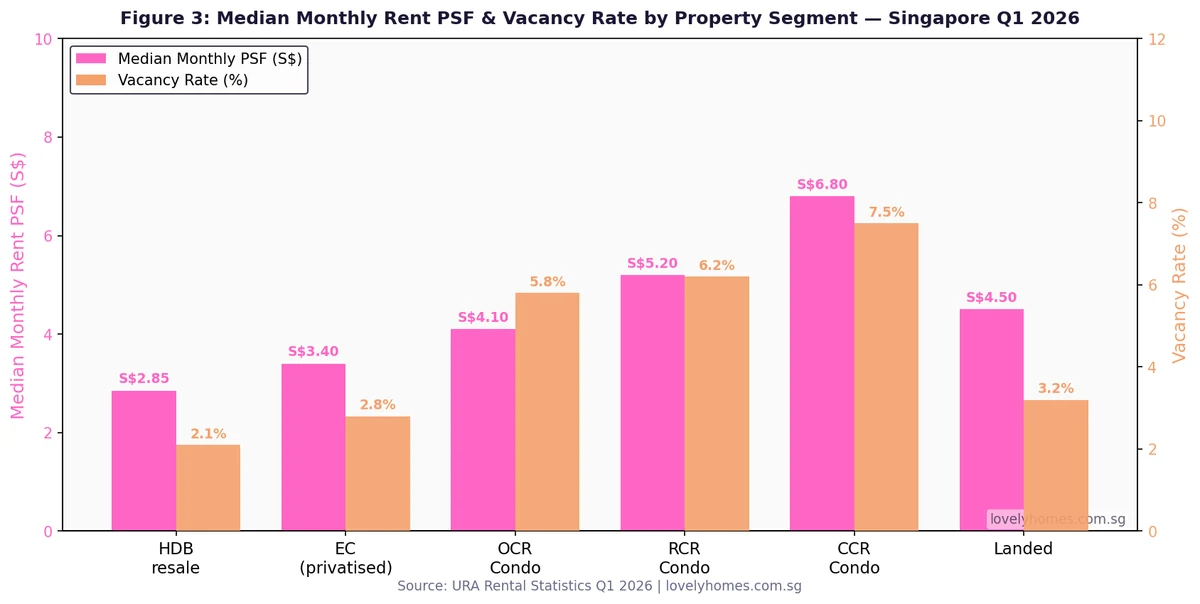

Analysing median monthly rent on a per-square-foot (PSF) basis allows meaningful comparison across property types of different sizes. URA’s Q1 2026 Rental Statistics show that CCR condos command the highest PSF (~S$6.80/sqft/month) but also carry the highest vacancy rates (~7.5%), reflecting the elevated supply completions in the prime districts. OCR condos are priced more keenly (~S$4.10 PSF) with lower vacancy (~5.8%).

Figure 3: Median monthly rent PSF and vacancy rate by property segment — Singapore Q1 2026. Source: URA Rental Statistics.

Rental Income Tax for Landlords

Rental income is taxable in Singapore under the Income Tax Act. Landlords must declare gross rental receipts in their annual tax returns (Year of Assessment for the preceding calendar year). Allowable deductions reduce the taxable rental income:

Mortgage interest (for the period the property was rented out; capital repayments are not deductible)

Property tax paid on the rented property

Fire insurance premiums

Maintenance and repair costs (not capital improvements)

Agent commission (for securing the tenancy)

For individual landlords, the net rental income is added to total chargeable income and taxed at progressive rates (0–22% for residents in YA 2026). Non-resident landlords face a flat 24% withholding tax on gross rental income unless a lower treaty rate applies. IRAS cross-checks rental declarations against the HDB/URA subletting register, so non-disclosure carries significant risk.

Tenant Rights and Responsibilities in Singapore

Singapore does not have a dedicated Tenants’ Rights Act. Tenancy agreements are governed by general contract law and the Distress Act (Cap 84). However, several protections and obligations apply by convention and statute:

Security deposit: typically 1 month per year of tenancy (2 months for a 2-year lease). The landlord must return the deposit within 14 days of lease expiry, less documented deductions for damage beyond fair wear and tear

Good Faith Principle (HDB): HDB subletting landlords may not impose conditions on how subtenants use common areas of the flat

Quiet enjoyment: A tenant in possession cannot be evicted without court order once a TA is duly executed and stamped

Utilities: Tenants are solely responsible for utilities (SP Services) unless expressly stated in the TA

Dispute resolution: Landlord-tenant disputes may be referred to the Community Disputes Resolution Tribunals (CDRT) or Small Claims Tribunals (SCT) for claims under S$20,000

Worked Example: The Nguyens Rent and Invest in Singapore

Mr & Mrs Nguyen, Vietnamese nationals on Employment Passes, arrive in Singapore in June 2026. They have a monthly EP allowance of S$12,000 combined and wish to rent a 3-bedroom condo in the east (D15/D16 Marine Parade/Bedok corridor) for a 2-year lease.

Agent commission: Typically 1 month (half/half split with landlord) = S$2,600, usually borne by landlord for a 2-year lease from month 13 onwards per industry convention

Total upfront cash outlay by tenant: S$10,400 + S$5,200 + S$1,997 = S$17,597

Annual rental budget: S$5,200 × 12 = S$62,400 (51.7% of annual EP income — in the higher range, but Singapore’s 55% TDSR is a credit metric, not an expense-to-income rule for tenants)

Simultaneously, Mr & Mrs Nguyen consider whether to invest in a D16 OCR condo unit at S$1.65M. As foreigners, they would pay BSD S$51,800 + ABSD S$1,072,500 (65% of S$1.65M) = S$1,124,300 total stamp duty — effectively a 68% surcharge on the purchase price. ABSD for foreigners at 65% makes direct property investment by foreigners financially prohibitive in most cases; rental remains the rational choice for non-PR residents.

Why the Rental Market Matters for Property Investors

Singapore’s rental market is not a peripheral consideration — it directly influences property valuations, lending decisions, and investment returns. The MAS Total Debt Servicing Ratio (TDSR) framework allows a landlord to include up to 70% of verified rental income from existing investment properties when computing their debt-servicing capacity for new loan applications. This means a property generating S$4,000/month in verifiable rental income effectively allows the landlord to carry an additional S$2,800/month in debt obligations under TDSR calculations — a meaningful lever for portfolio expansion.

For owner-occupiers considering upgrading, rental yield is also an opportunity cost metric: if your HDB flat could generate S$3,000/month post-MOP but you remain in it rent-free, that S$3,000 is the implicit value of owner-occupation compared against renting out and renting elsewhere. The condo vs HDB upgrader analysis is informed significantly by this rental yield comparison.

What Might Come Next for Singapore Rentals

The near-term rental outlook points to continued moderation. The completion of large private condo projects in the OCR and RCR pipeline — particularly the Tengah, Bukit Timah, and Greater Southern Waterfront corridors — will keep vacancy elevated through 2026–2027. However, several countervailing forces support long-term demand: Singapore’s push to attract global business headquarters, the expanding one-north and JTC LaunchPad ecosystem, and the steady pace of permanent residence approvals all support rental absorption. If URA’s Q2 2026 data (expected July 2026) shows vacancy stabilising below 8%, that will be a positive signal for landlords. The HDB subletting market is likely to tighten further as the 2019–2021 BTO cohort approaches MOP in 2024–2026, releasing a new wave of HDB supply into the rental pool at precisely the moment private vacancy is also elevated. Tenants may benefit from negotiating power in this window.

Frequently Asked Questions

Can I rent out my HDB flat before completing the MOP?

You cannot sublet the entire HDB flat before completing the 5-year MOP (or 10-year MOP for PLH/Plus flats). However, you may sublet individual rooms — provided you continue to reside in the flat yourself. Room subletting does not require HDB approval, but the occupancy cap still applies (maximum 6 unrelated persons, or 8 during the temporary relaxation period through January 2028). Subletting the entire flat pre-MOP is a breach of the HDB terms and conditions and may result in compulsory acquisition of the flat by HDB.

What is the minimum tenancy period for a private condo in Singapore?

The minimum tenancy for a private residential property (including condominiums, apartments, and landed houses) in Singapore is 3 consecutive months, as set by URA regulations. Any lease shorter than 3 months is classified as short-term rental and is prohibited. For HDB flats, the minimum is 6 consecutive months. Short-stay platform listings (Airbnb-style) are illegal for all residential properties in Singapore and can result in fines of up to S$5,000 per offence.

Do I need to pay income tax on rental income in Singapore?

Yes. Rental income received by individuals is subject to income tax under the Income Tax Act (Cap 134). You must declare gross rental receipts in your annual income tax return. Allowable deductions include mortgage interest (not capital repayment), property tax, fire insurance premiums, maintenance and repair costs, and agent commission. The taxable net rental income is added to your other chargeable income and taxed at progressive rates (0–22% for residents in YA 2026; 24% flat for non-residents). IRAS cross-references HDB and URA subletting records, so undeclared rental income carries significant audit risk. You may file via myTax Portal at iras.gov.sg.

Who pays stamp duty on a Tenancy Agreement — landlord or tenant?

By convention and IRAS practice, the tenant bears the stamp duty on the Tenancy Agreement, unless the TA expressly states otherwise. The rate is S$4 per S$250 (or part thereof) of the total rent payable over the term (for leases up to 4 years). Stamp duty must be paid via IRAS e-Stamping within 14 days of signing the TA if signed in Singapore, or within 30 days if signed overseas. An unstamped TA is inadmissible in court as evidence, which is a significant risk if a landlord-tenant dispute later arises.

Can a foreigner rent a private condo or HDB flat in Singapore?

Foreigners may rent private residential properties (condominiums, apartments, landed houses) without restriction. However, foreigners may only rent HDB flats if they hold a valid long-term pass — specifically an Employment Pass, S Pass, Dependent Pass, or Long-Term Visit Pass. Tourist visa holders (SVP/STP) and short-term pass holders cannot legally rent an HDB flat. The HDB maintains a non-citizen (non-Malaysian foreigner) quota of 8% per HDB block — once that quota is reached, additional non-Malaysian foreigners cannot rent any flat in that block regardless of their pass type.

What security deposit is standard in Singapore rental agreements?

Singapore’s rental market follows the convention of 1 month’s deposit per year of tenancy — so a 1-year lease carries a 1-month deposit and a 2-year lease carries a 2-month deposit. This is not enshrined in statute but is industry standard enforced by the IRAS stamp-duty framework (which uses “gross rent” inclusive of any deposit payments). The landlord must return the full deposit within 14 days after the lease end date, less documented deductions for damage beyond normal fair wear and tear. Disputes over deposit deductions may be brought before the Small Claims Tribunal (SCT) for claims under S$20,000.

What happens if my landlord refuses to return my security deposit?

If a landlord unlawfully withholds a security deposit, the tenant may file a claim with the Small Claims Tribunal (SCT) for disputes involving sums up to S$20,000, or with the Community Disputes Resolution Tribunal (CDRT) if the dispute also involves neighbourly conduct. A stamped Tenancy Agreement is the primary piece of evidence; ensure you retain a signed copy and document the flat’s condition with photographs at both the start and end of the tenancy. The Consumer Association of Singapore (CASE) also provides mediation for tenancy disputes. Singapore’s courts have consistently upheld tenants’ rights to deposit recovery where the landlord cannot produce evidence of actual damage.

Disclaimer: The information in this guide is for general educational purposes only and does not constitute legal, tax, or financial advice. Rental rules, stamp duty rates, and HDB policies are subject to change by the relevant authorities — HDB, URA, IRAS, CPF Board, and MAS. Always verify current rules at the official government portals (hdb.gov.sg, ura.gov.sg, iras.gov.sg) and consult a licensed property agent or solicitor before entering into any tenancy or purchase transaction. LovelyHomes is an independent editorial platform and is not affiliated with any property agency.

If you own a property in Singapore and rent it out — whether an HDB flat, a private condominium, or a landed house — the rental income you receive is taxable. The Inland Revenue Authority of Singapore (IRAS) treats rental income as part of your total chargeable income for that Year of Assessment (YA), taxed at the prevailing personal income tax rates. Knowing how the system works, which expenses you may deduct, and when to file are not merely compliance obligations — they directly affect your net return on any investment property you hold.

This guide covers every aspect of rental income tax in Singapore for YA 2026 (income earned in 2025): what counts as rental income, allowable deductions, the tax rate schedule, filing deadlines, worked examples, and the most common landlord mistakes that trigger IRAS scrutiny.

Quick Answer — Key Takeaways

Rental income from Singapore properties is taxable; you must declare it in your annual income tax return.

Net rental income = gross rent minus allowable deductions (mortgage interest, property tax, maintenance, insurance, agent fees for renewals).

Personal income tax rates for YA 2026 range from 0% (first S$20,000) to 22% (above S$320,000 chargeable income).

Capital expenditure — renovations, improvements, furniture purchases — is not deductible; only revenue expenses qualify.

IRAS filing deadline: 18 April 2026 (paper) / 18 April 2026 (e-filing via myTax Portal); penalties of up to 200% of unpaid tax may apply for non-declaration.

Mortgage principal repayments are not deductible; only the interest component qualifies.

Foreign rental income remitted to Singapore by tax residents is also taxable (with credit for foreign taxes paid).

A property rented partially for personal use requires apportionment of expenses.

What Counts as Rental Income in Singapore

IRAS defines rental income broadly. It includes all amounts received or receivable from letting out a property in Singapore: monthly or annual rent, advance rent, premiums received for granting a lease, and service or facility charges included in the rental arrangement. If your tenant pays utilities as part of a gross rental arrangement and reimburses you, that reimbursement is also rental income.

What does not count: genuine security deposits that you hold in trust and will refund are not income. However, if a deposit is forfeited (e.g., the tenant breaks the lease), the forfeited amount becomes income in the year it is forfeited.

Rental income is assessed on a received basis for individuals — meaning you declare what you actually received (or were entitled to receive) during the calendar year 2025 for YA 2026, regardless of when the tenancy period technically falls.

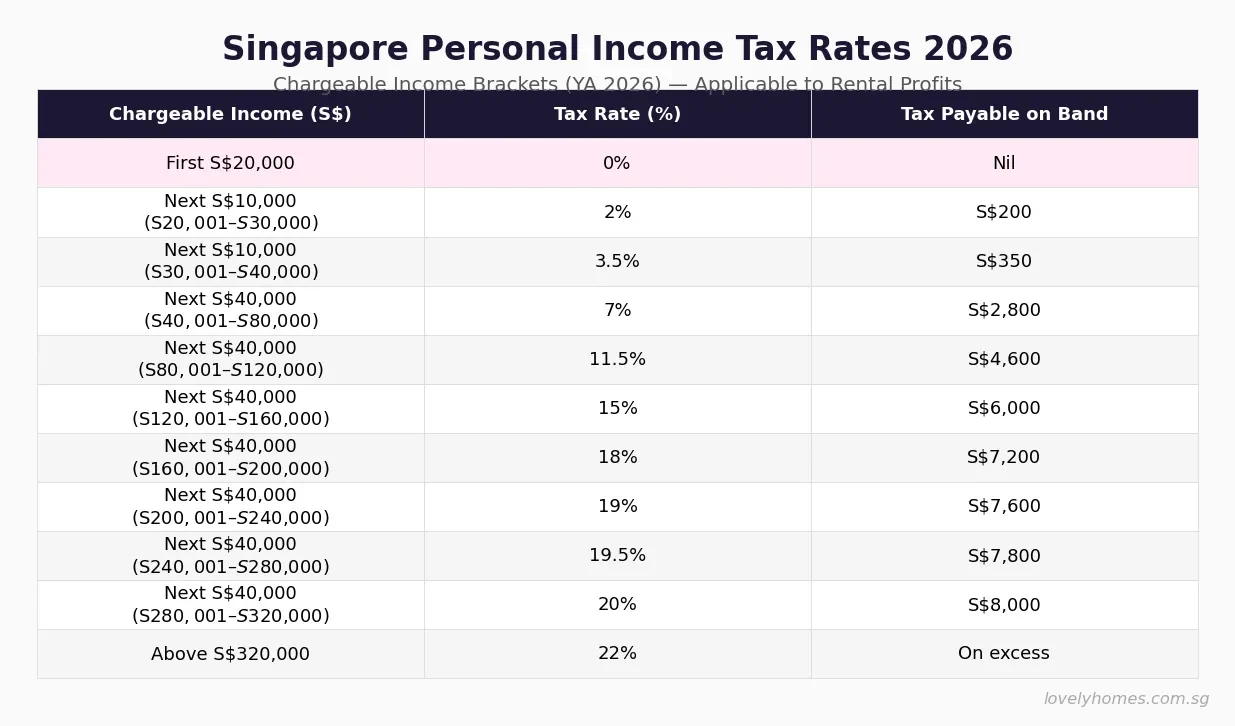

Figure 1: Singapore personal income tax rate schedule for YA 2026. Rental profits are added to all other income sources to determine which bracket applies. Source: IRAS.

The tax rates above are progressive and cumulative. A landlord whose only income is rental income of S$60,000 net does not pay 7% on the full S$60,000. Instead, the first S$20,000 attracts 0%, the next S$10,000 attracts 2% (S$200), the next S$10,000 attracts 3.5% (S$350), and the remaining S$20,000 attracts 7% (S$1,400) — a total tax of S$1,950, an effective rate of 3.25%.

Allowable Deductions: What You Can Claim Against Rental Income

IRAS applies the revenue versus capital test to every expense. Revenue expenses — those incurred to earn rental income on an ongoing basis — are deductible. Capital expenses — those that create or improve a long-term asset — are not. The distinction sometimes requires careful analysis, especially for renovation and repair costs.

Expense Category

Deductible?

Notes

Mortgage interest

✓ Yes

Interest portion only; not principal repayment. Proportionate if property partly owner-occupied.

Property tax (annual)

✓ Yes

The property tax bill from IRAS itself is deductible as a landlord expense.

Fire / home insurance premium

✓ Yes

Premiums for insurance on the rented property are allowable.

Maintenance and repairs

✓ Yes

Restoring to original condition (e.g., repainting, plumbing repairs) — revenue in nature.

Agent commission (renewal)

✓ Yes

Renewal commissions are revenue expenses. First-time lease commissions may be disallowed.

Advertising costs

✓ Yes

Costs of finding a tenant (online listings, print ads).

Furniture rental

✓ Yes

Monthly rental of furniture provided to tenant is deductible; purchase of furniture is not.

Renovation and improvements

✗ No

Capital in nature — creates new value. Not deductible regardless of amount.

Mortgage principal repayment

✗ No

Capital repayment only reduces liability; does not generate income.

Furniture purchase

✗ No

Capital expenditure; no depreciation allowance available to individuals.

Initial agent commission (new lease)

✗ No

IRAS typically treats this as capital to secure the tenancy; not ongoing revenue.

Personal expenses

✗ No

Any expenses not wholly and exclusively incurred to produce rental income.

Figure 2: Deductible versus non-deductible rental expenses for Singapore landlords (YA 2026). Source: IRAS e-Tax Guide on Taxation of Property Owners.

Repairs vs Improvements — The Critical Distinction

The boundary between a deductible repair and a disallowed improvement is one of the most contested areas in rental tax practice. IRAS looks at whether the work restores an asset to its original working condition (deductible) or improves it beyond its original state (capital, not deductible). Replacing a broken tile with an identical tile: deductible. Replacing worn carpet with hardwood flooring: capital. Repainting walls in the same colour: deductible. Knocking down a wall to open plan the kitchen: capital. When in doubt, document the original condition and the work scope, and retain quotes and invoices.

Mortgage Interest — Most Valuable Deduction for Leveraged Landlords

For landlords who financed their investment property with a bank loan, the interest component of each monthly mortgage instalment is deductible. You must obtain a mortgage statement from your bank showing the split between principal and interest for the year — this is typically included in your annual statement or available via the bank’s portal.

If you live in the property for part of the year and rent it out for the remainder, you must apportion the interest on a time basis. For example, if you rented the property for nine out of twelve months, only 9/12ths of the annual interest is deductible.

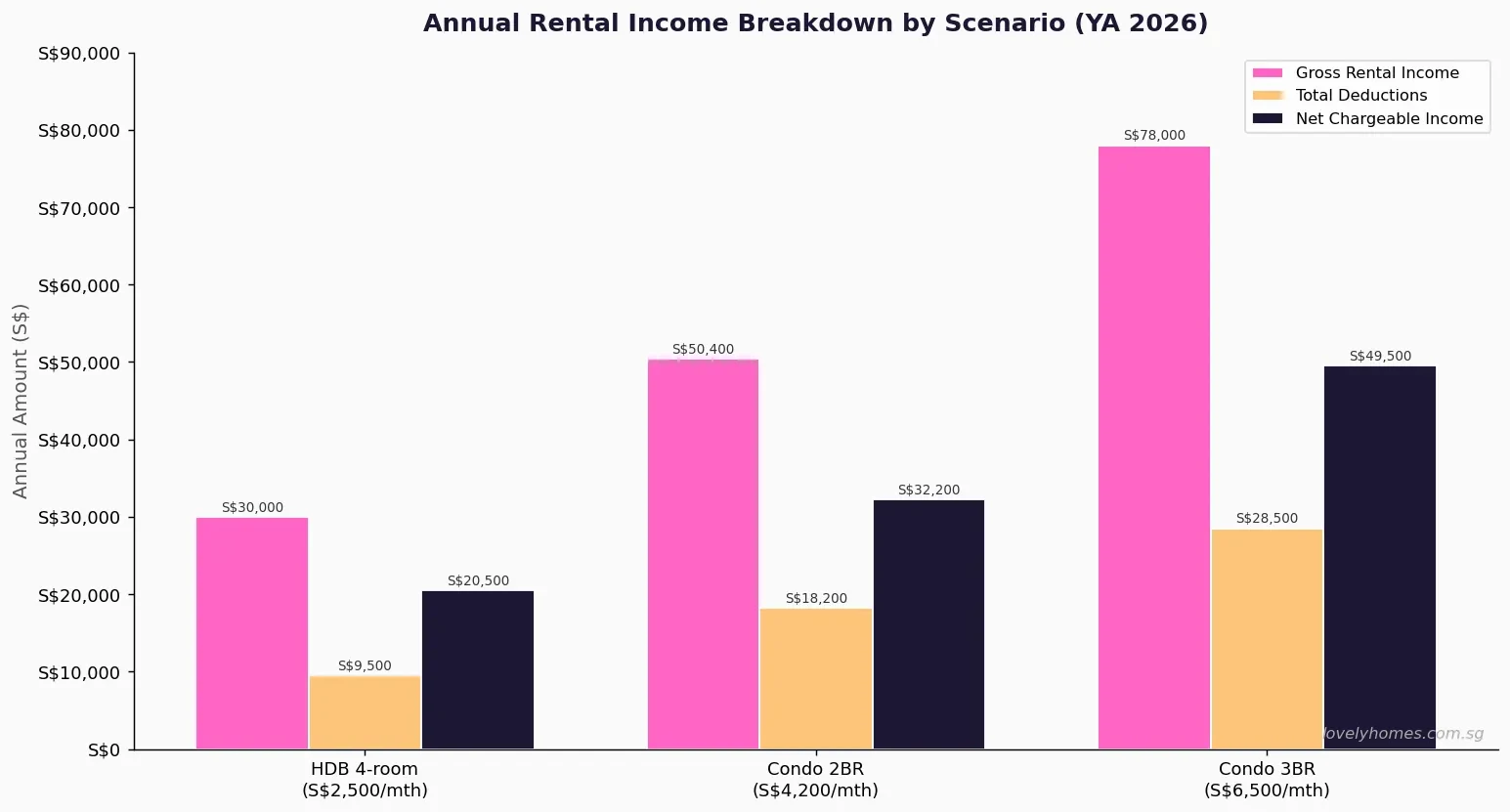

How Net Rental Income Is Calculated: Three Scenarios

Figure 3: Annual rental income breakdown — gross rent, total deductions, and net chargeable income — across three common Singapore landlord scenarios (YA 2026). Figures are illustrative.

The three scenarios above reflect a spectrum of Singapore rental situations. A modest HDB 4-room flat in a mature estate rented at S$2,500 per month (S$30,000 gross per year) might yield deductions of approximately S$9,500 (mortgage interest S$6,500, property tax S$1,800, fire insurance S$400, maintenance S$800), leaving net chargeable rental income of roughly S$20,500. A city-fringe condo 2-bedroom at S$4,200 per month carries higher deductions (larger mortgage, higher property tax) and nets approximately S$32,200. A 3-bedroom at S$6,500 per month nets roughly S$49,500 after all allowable deductions.

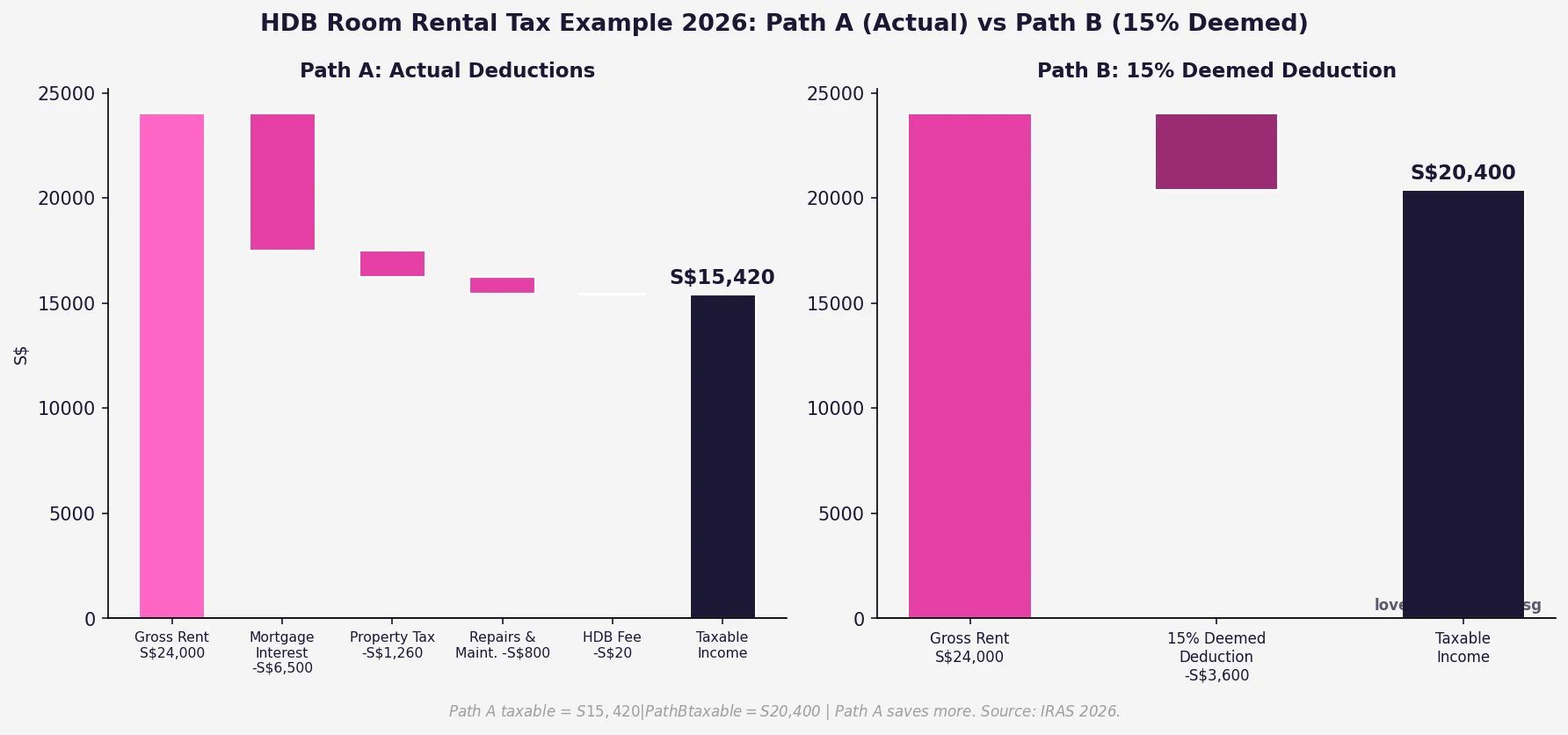

Worked Example: Mr Tan’s Investment Condo, YA 2026

Property: 2-bedroom condominium in Tampines, purchased March 2023 for S$1.2 million. Bank loan of S$840,000 at 3.0% p.a. fixed (2-year lock-in, now on floating SORA+0.9% ≈ 3.25% p.a.). Rented at S$3,800 per month for the full 12 months of 2025.

Step 4 — Tax on Rental Income: Mr Tan also earns an employment income of S$120,000. His total chargeable income is S$120,000 + S$12,724 = S$132,724 (assuming standard personal reliefs of, say, S$20,000 apply, reducing to S$112,724 chargeable). Applying the YA 2026 brackets, his incremental tax on the S$12,724 rental profit (falling in the 11.5–15% marginal bands) is approximately S$1,850.

Key insight: Mortgage interest is the single largest deduction — without it, net rental income would have been S$38,724, and the incremental tax nearly four times higher. Landlords with high-interest-rate loans in 2025 (SORA-linked packages averaging 3.0–3.5%) benefit the most from the interest deduction.

Filing Obligations: How and When to Declare Rental Income

Rental income is declared in your annual income tax return via myTax Portal (IRAS). The filing deadline is 18 April each year for both paper and e-filing; for YA 2026 (income earned in calendar year 2025), you should have filed by 18 April 2026. If you missed the deadline, file immediately to minimise late penalties.

On your return, you will see a section titled Rental Income where you enter: the address of each rented property, gross rent received, and itemised deductions. IRAS may request supporting documents — keep mortgage statements, tenancy agreements, property tax bills, invoices for maintenance, and insurance schedules for at least five years.

Obligation

Detail

Consequence of Non-Compliance

Declare rental income

Gross rent from all Singapore and foreign rental properties

Penalty up to 200% of unpaid tax; prosecution for wilful non-declaration

e-File via myTax Portal

Deadline: 18 April each YA

Late filing penalty; estimated assessment by IRAS if returns not filed

Retain records

5 years from relevant YA

IRAS may disallow deductions if supporting documents unavailable

Notify IRAS of change in rental status

If property was previously owner-occupied

Incorrect owner-occupier property tax rates may trigger recovery

Property Tax on Rented Properties — A Related but Separate Obligation

Property tax (administered by IRAS separately from income tax) applies to all Singapore properties. Owner-occupiers receive a concessionary progressive rate; landlords renting out their properties pay the higher non-owner-occupier rate on the Annual Value (AV) of the property. The non-owner-occupier residential property tax rates for 2026 range from 12% (first S$30,000 AV) to 36% (AV above S$90,000), reflecting the government’s ongoing property cooling stance.

Critically, the property tax bill itself is a deductible expense against your rental income for income tax purposes — effectively giving you a partial recovery of the property tax cost at your marginal income tax rate. For a landlord in the 15% income tax bracket, a S$5,000 property tax bill reduces rental income tax by S$750.

HDB Flat Rental — Additional Considerations

HDB flat owners who sublet their flat (or individual rooms) must first obtain HDB approval before renting. Once approval is granted, all rental income rules above apply equally — declare gross rent, claim allowable deductions, pay income tax on the net profit. The mortgage interest deduction is particularly significant for HDB owners who carry an outstanding HDB concessionary loan (2.60% p.a. as at May 2026), as the interest on that loan is deductible.

Note that HDB owner-occupier property tax rates apply to HDB flats irrespective of whether you sublet individual rooms (as opposed to the whole flat). If you rent out the entire flat, HDB requires you to rent a replacement home, and the non-owner property tax rate applies.

Foreign Rental Income for Singapore Tax Residents

If you are a Singapore tax resident and receive rental income from overseas properties (Malaysia, Thailand, Australia, the United Kingdom, and so on), that income is generally taxable in Singapore when it is remitted or deemed remitted to Singapore. Singapore does not tax foreign income that is kept offshore. However, once transferred to a Singapore bank account — even briefly — it is treated as remitted. You may claim a credit for foreign taxes paid on that income, subject to the double tax agreements Singapore maintains with over 80 countries.

What This Means for Singapore Landlords in 2026

Singapore’s rental income tax framework is moderate by global standards — the progressive rate structure, generous mortgage interest deduction, and property tax deductibility all reduce the effective tax burden for most landlords. However, three factors are squeezing margins in 2026: elevated mortgage rates (SORA-linked packages remain near 3.0–3.5%), higher non-owner-occupier property tax rates following the 2024–2025 AV revision cycle, and increased ABSD costs that raise the entry price for new investment purchases.

Net rental yields across Singapore private residential properties averaged 3.0–3.6% in Q1 2026 (industry data), down from the 4.0–4.5% range prevalent in 2022. For a leveraged landlord on a 75% LTV mortgage at 3.25% interest, the after-tax net yield may narrow to 1.5–2.5% depending on location and property type — compelling careful cash-flow modelling before any new acquisition.

What Might Come Next: Rental Tax Policy Outlook

This section is speculative and should not be relied upon for financial decisions. Singapore’s tax authorities have signalled no imminent changes to the personal income tax treatment of rental income. However, three developments are worth monitoring: (1) further property tax AV revisions for 2026–2027, which IRAS reviews annually and which directly affect the size of the deductible property tax bill; (2) any shifts in SORA-linked benchmark rates as the global monetary cycle evolves, affecting deductible mortgage interest; and (3) potential tightening of the regime for short-term rental platforms (Airbnb, Booking.com), which IRAS may subject to different rules if legislative changes follow proposed government reviews.

Frequently Asked Questions

Do I need to declare rental income if I only rent out one room?

Yes. IRAS requires you to declare all rental income, including income from subletting a single bedroom in your HDB flat or private property. The gross rent received for the room, less allowable deductions (apportioned based on the rented room’s floor area as a proportion of total floor area), must be reported in your annual income tax return. The apportionment approach applies to expenses like mortgage interest, property tax, and maintenance that cover the whole property.

Can I deduct renovation costs incurred before the tenant moved in?

Generally, no. IRAS treats renovation expenditure as capital expenditure, even if done to attract a tenant. The only exception is expenditure that constitutes genuine repair — restoring the property to its existing condition — rather than improvement. A fresh coat of paint before a new tenancy commences is typically allowable; a full kitchen overhaul or new bathroom suite is not. Retain full documentation of the pre- and post-renovation condition and all invoices.

My property was vacant for three months — can I still deduct mortgage interest for those months?

IRAS’s position is that you may deduct mortgage interest for vacant periods only if the vacancy arises because you are actively seeking a tenant (for example, the existing tenant has moved out and you are marketing the unit). If the property is vacant because you are occupying it for personal use or have no intention of renting during that period, the interest for those months is not deductible. Keep records of your rental marketing efforts (listing screenshots, agent correspondence) during any vacancy period.

How does IRAS know I have rental income if I do not declare it?

IRAS has multiple data-matching sources: HDB approval records for flat subletting, URA rental contract submissions (required for private properties since 2021), tenancy agreements registered with SLA, and property transaction data. IRAS also receives bank interest income information and can cross-reference rental deposits with landlord declarations. Undeclared rental income has led to IRAS audits resulting in penalties of up to 200% of underpaid tax. The risk of non-declaration significantly outweighs any short-term saving.

Can joint owners of an investment property both claim deductions?

Yes. Where a property is jointly owned, both owners must declare their respective share of the rental income and may each claim their proportionate share of the allowable deductions. If the property is held as tenants-in-common with unequal shares (for example, 60/40), each owner declares income and deductions in those proportions. Joint tenants (equal shares by default) split 50/50. Each owner files a separate income tax return.

Is rental income from Airbnb and short-term lets treated the same way?

For income tax purposes, yes — all rental income, whether from long-term tenancies or short-term platform bookings, is taxable. However, short-term rentals of private residential properties (less than three consecutive months per guest) are illegal in Singapore under URA regulations unless the property has a specific hotel or serviced apartment licence. HDB flats require a minimum rental period of six months per tenant. Accordingly, most Airbnb-style activity in Singapore private homes is legally prohibited. IRAS’s income tax rules would apply to any such income, but the underlying activity also exposes the owner to URA enforcement.

What if my rental income creates a loss (deductions exceed rent received)?

If your allowable deductions exceed your gross rental income for a year (producing a rental loss), IRAS generally does not allow that loss to be offset against other income sources such as employment income. Rental losses may in some circumstances be carried forward to offset future rental income from the same property. The rules on loss relief are complex and depend on whether the rental activity constitutes a trade — for most individual landlords, losses are quarantined within the rental income category. Consult a registered tax professional if you anticipate a rental loss position.

This article is intended for general informational purposes only and does not constitute tax, legal, or financial advice. Tax rules are subject to change; always verify current rates, thresholds, and filing requirements directly with the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg and the Monetary Authority of Singapore (MAS). Readers with specific tax questions regarding their rental properties should consult a qualified Singapore tax professional or a licensed financial adviser. Figures and examples used are illustrative and may not reflect your individual circumstances.

Singapore Citizens (SC) can sublet the whole flat or individual bedrooms after meeting the 5-year Minimum Occupation Period (MOP), with HDB approval.

Permanent Residents (PR) can only rent out spare bedrooms — not the entire flat — and must continue living in the flat.

You must physically occupy the flat for at least 5 years from key collection before subletting; overseas postings do not pause the clock.

Minimum rental period: 6 months per tenancy. Short-term lettings (Airbnb-style) are strictly prohibited and can result in flat acquisition.

The occupancy cap has been temporarily raised: 4-room flats and larger may now accommodate 8 unrelated persons (up from 6) until 31 December 2028, under a joint HDB/URA directive.

All rental income must be declared to IRAS annually. You may deduct actual allowable expenses or elect the 15% deemed deduction — actual expenses typically save more.

Penalties for subletting without HDB approval: fine up to S$5,000 for a first offence; compulsory flat acquisition for repeat or serious offences.

Always register the tenancy with HDB within 7 days of the start of the lease.

What Is HDB Subletting?

Subletting — or renting out — your HDB flat or its spare bedrooms is permitted under the Housing and Development Act (Cap. 129) and is administered by the Housing and Development Board (HDB). It allows eligible flat owners to generate rental income while providing accommodation to tenants who cannot or prefer not to buy their own home. As at Q1 2026, approximately 58,600 HDB flats are being rented out in Singapore’s private rental market, with HDB subletting constituting an important segment of the broader rental ecosystem. HDB rental data is monitored by URA and published quarterly as part of Singapore’s official rental market statistics.

Figure 1: HDB subletting eligibility matrix 2026 — who can sublet what, MOP requirement, and approval pathway. Source: HDB.

Eligibility: Who Can Sublet and What

HDB’s subletting rules distinguish sharply between Singapore Citizens and Permanent Residents, and between subletting a whole flat versus individual bedrooms.

Whole Flat Subletting — Singapore Citizens Only

Only SC flat owners may sublet the entire flat (i.e., move out and rent the property to tenants). The owner and his/her household members are not required to remain in the flat during the subletting period. Conditions:

MOP met: 5 years of physical occupation from the date of key collection, calculated on the basis of the flat’s registration period at HDB. Importantly, if the owner relocates overseas for work, the overseas period does not count towards the MOP — the clock pauses.

Only 3-room flats or larger may be sublet. 1-room and 2-room Flexi flats cannot be sublet as whole units.

Owner must not own other residential property in Singapore concurrently, unless HDB grants prior approval (typically for medical or employment reasons).

Tenants must be eligible: Singapore Citizens, PRs, and certain non-citizen pass holders (Employment Pass, S-Pass, Dependent Pass, Long-Term Visit Pass) are accepted. Tourists are not.

Bedroom Subletting — SC and PR Owners