Singapore Property Cooling Measures 2026: Complete Guide to ABSD, TDSR, LTV and SSD

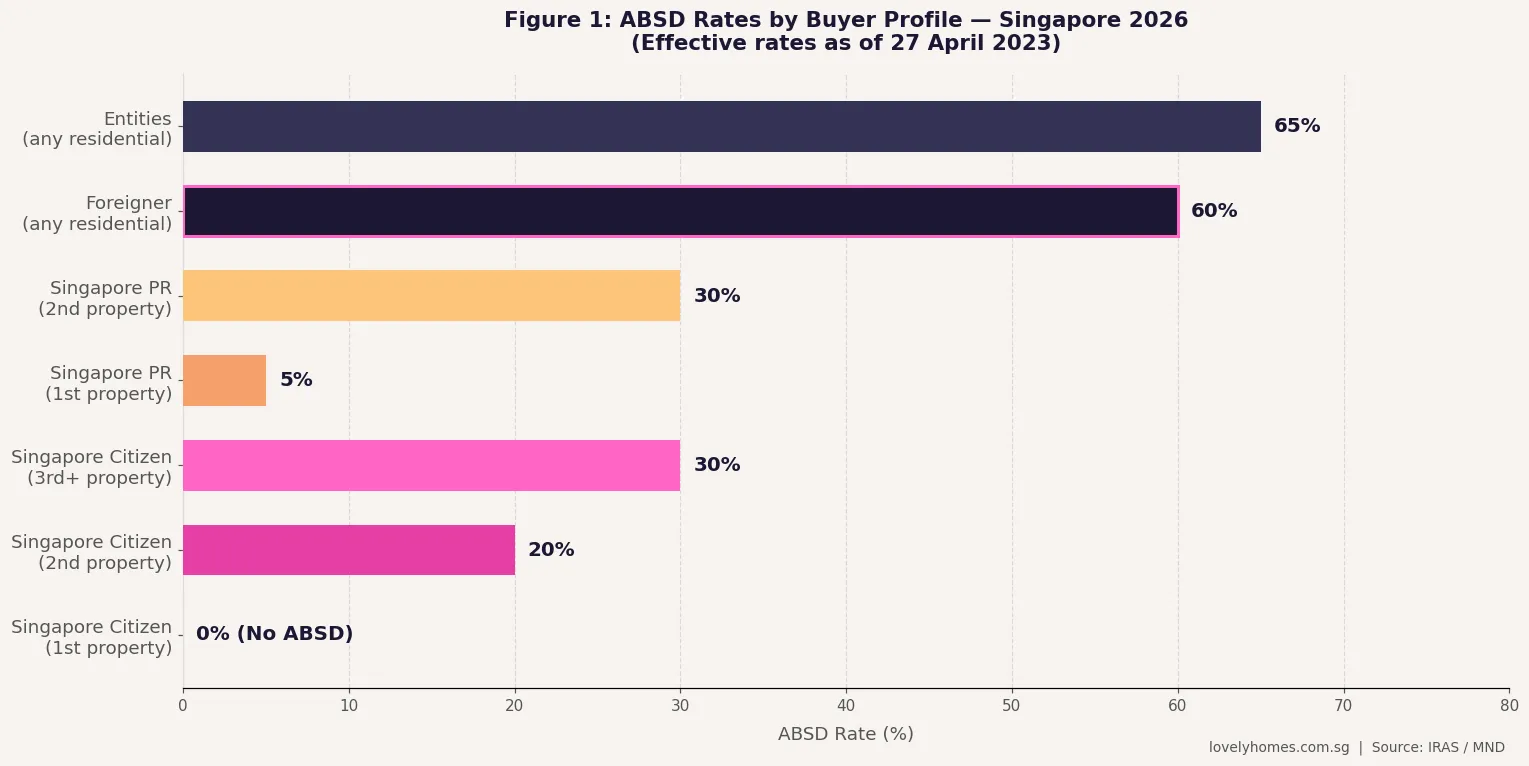

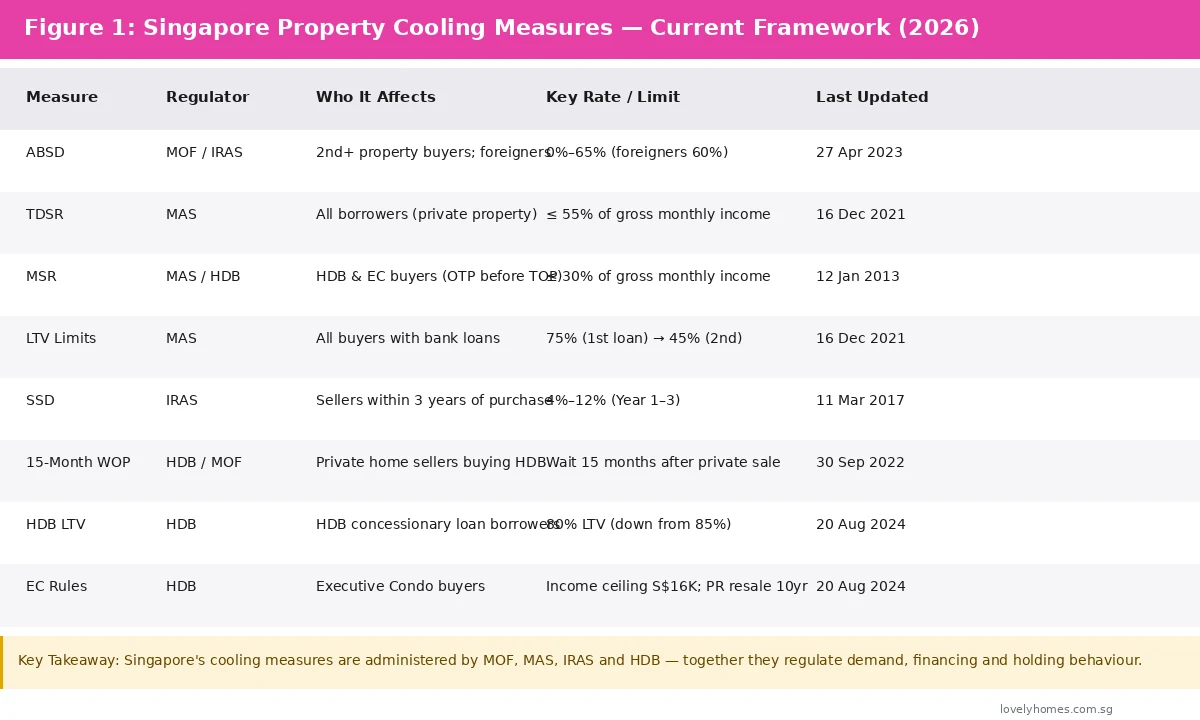

- ABSD — Additional Buyer’s Stamp Duty applies to 2nd+ residential properties; foreigners pay 60%; entities pay 65%.

- TDSR — Total Debt Servicing Ratio capped at 55% of gross monthly income for all bank property loans.

- MSR — Mortgage Servicing Ratio capped at 30% for HDB and Executive Condo loans before TOP.

- LTV — Loan-to-Value limit is 75% for a first bank loan, 45% for a second, and 35% for a third and beyond.

- SSD — Seller’s Stamp Duty of 4%–12% applies if a residential property is sold within 3 years of purchase.

- 15-Month Wait-Out Period — Private residential property owners must wait 15 months after disposal before buying an HDB resale flat.

- Administering bodies: Ministry of Finance (MOF), Monetary Authority of Singapore (MAS), IRAS, and the Housing & Development Board (HDB).

- Singapore has implemented 10 rounds of cooling since 2009; the most recent was 27 April 2023, which raised ABSD sharply.

What Are Property Cooling Measures?

Singapore’s property cooling measures are a suite of demand-management and financing regulations designed to keep the residential property market stable, affordable, and free from speculative excess. They are not merely bureaucratic obstacles — they are the primary tool through which the Singapore Government actively steers the balance between home ownership aspirations and financial prudence.

The measures are administered jointly by four bodies: the Ministry of Finance (MOF), which sets and reviews stamp duty policy; the Monetary Authority of Singapore (MAS), which governs loan limits and debt servicing ratios; IRAS, which collects and assesses stamp duties; and the Housing & Development Board (HDB), which administers HDB-specific rules on eligibility, pricing and resale conditions. Together, they form a layered framework that operates on both the demand side (who can buy, how much ABSD they pay) and the supply side (loan limits, holding periods).

As of 3 July 2026, the core cooling measures in force were established by the major rounds of 2021, 2022, and — most significantly — 27 April 2023. This guide consolidates all current measures into a single reference, explains why each exists, and shows you exactly how they affect your purchasing decision.

Additional Buyer’s Stamp Duty (ABSD)

The Additional Buyer’s Stamp Duty, first introduced on 8 December 2011 and most recently revised on 27 April 2023, is the most visible and financially significant of Singapore’s cooling tools. It is collected by IRAS and applies in addition to the ordinary Buyer’s Stamp Duty (BSD) on every residential property purchase that falls within its scope.

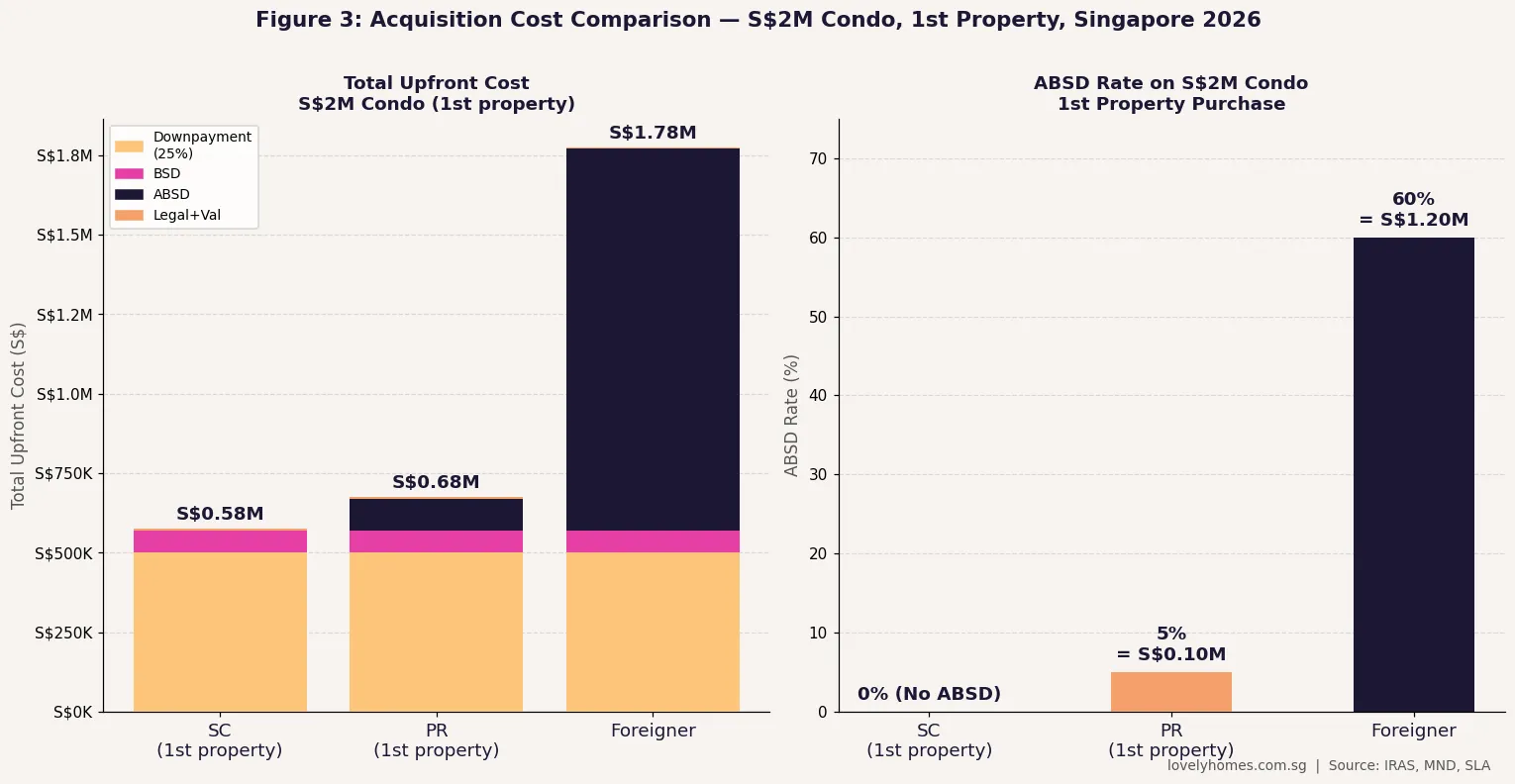

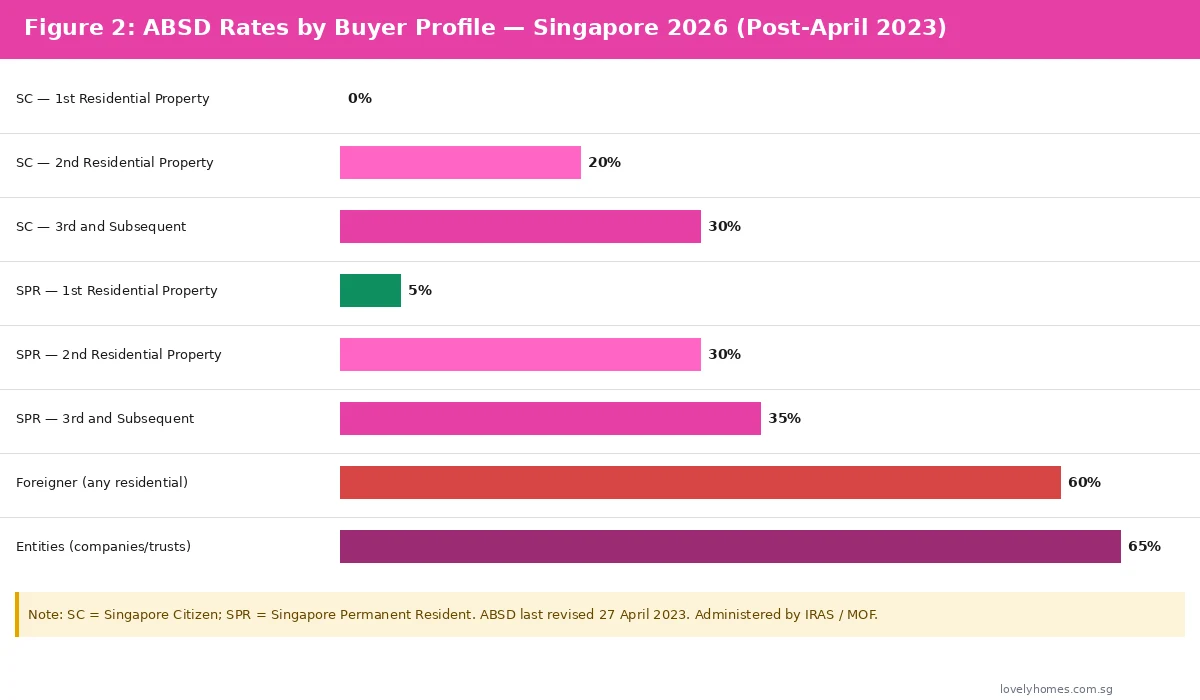

ABSD is calibrated by two factors: the buyer’s citizenship or residency status, and the count of residential properties already owned (or being purchased simultaneously). Singapore Citizens purchasing their first and only residential property are exempt from ABSD entirely. However, a Singapore Citizen buying a second property immediately incurs ABSD at 20% of the purchase price or valuation, whichever is higher. Foreigners — regardless of how many properties they own — pay 60%, a rate that was doubled from 30% in the April 2023 round specifically to reduce the proportion of foreign purchasers in the private residential segment. Corporate entities and trusts pay an even higher rate of 65%.

| Buyer Profile | 1st Property | 2nd Property | 3rd and Beyond |

|---|---|---|---|

| Singapore Citizen (SC) | 0% | 20% | 30% |

| Singapore Permanent Resident (SPR) | 5% | 30% | 35% |

| Foreigner (any nationality) | 60% (all purchases) | ||

| Entity (company / trust) | 65% (all purchases) + 5% additional for housing developers | ||

ABSD must be paid in cash within 14 days of the date of the document effecting the sale (or, for uncompleted properties, within 14 days of the date of the Sale & Purchase Agreement). It cannot be funded from CPF Ordinary Account savings. For a Singapore Citizen couple where one spouse is a foreigner, the higher of the two applicable ABSD rates will apply unless the foreign spouse is decoupled from the title and the property is purchased in the SC’s sole name alone — in which case ABSD is based solely on the SC’s property count.

The one significant ABSD remission pathway for Singapore Citizens is the 99-to-1 arrangement elimination and the simultaneous disposal rule: a married SC couple upgrading from an existing private property to a new private property may apply for ABSD remission on the replacement property if the first property is sold within six months of the purchase (or within six months of TOP for uncompleted properties). This remission is limited to one replacement property and is handled by IRAS on application.

Financing Limits: TDSR, MSR, and Loan-to-Value

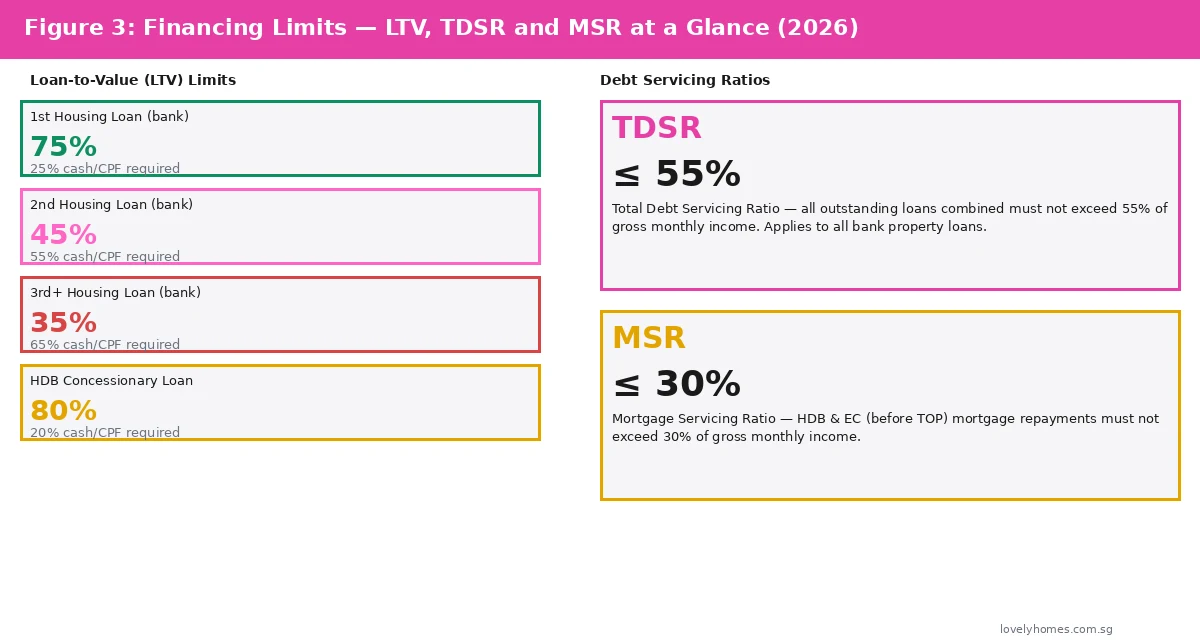

MAS administers the loan framework that constrains how much any buyer can borrow against any residential property. The three pillars are the Total Debt Servicing Ratio, the Mortgage Servicing Ratio, and the Loan-to-Value limit.

The Total Debt Servicing Ratio (TDSR), effective since 29 June 2013 and tightened on 16 December 2021 from 60% to 55%, requires that the borrower’s total monthly debt obligations — including the property loan being applied for — do not exceed 55% of gross monthly income. The TDSR applies to all bank property loans; it does not apply to HDB concessionary loans.

The Mortgage Servicing Ratio (MSR), capped at 30% of gross monthly income, applies specifically to loans for HDB flats and Executive Condos purchased before TOP. Unlike the TDSR, the MSR uses only the mortgage being applied for — not total outstanding debt — in its calculation. For couples, income is computed on a joint basis. This means that a household earning S$7,000 combined per month has a monthly MSR ceiling of S$2,100 for their HDB loan.

The Loan-to-Value (LTV) limits cap the maximum loan amount as a percentage of the property’s value (or price, whichever is lower). A buyer taking their first bank loan may borrow up to 75% LTV, meaning they must stump up at least 25% in cash and/or CPF savings. A buyer with an existing outstanding bank loan faces an LTV of 45% (55% downpayment required), and a buyer with two or more outstanding loans faces an LTV of just 35%. For HDB concessionary loans, the LTV was reduced from 85% to 80% on 20 August 2024 — meaning an HDB loan buyer must find at least 20% from CPF and/or cash.

| Outstanding Loans | Max LTV (Bank Loan) | Min Cash | Min Cash + CPF |

|---|---|---|---|

| 0 (first bank loan) | 75% | 5% | 25% |

| 1 outstanding | 45% | 25% | 55% |

| 2 or more outstanding | 35% | 25% | 65% |

| HDB Concessionary Loan | 80% | 0% | 20% (CPF/cash) |

Seller’s Stamp Duty (SSD)

The Seller’s Stamp Duty is a holding-period tax designed to discourage short-term flipping. Currently calibrated at 12% if a residential property is sold within the first year of purchase, 8% in Year 2, and 4% in Year 3, with no SSD payable from Year 4 onwards. The SSD applies to all private residential properties in Singapore; HDB flats are exempt. It is collected by IRAS based on the selling price or market value, whichever is higher, and must be paid in cash — like ABSD, it cannot be funded from CPF.

For a buyer who purchased a private condominium at S$1.5 million and sold it 18 months later at S$1.65 million, the SSD would be 8% × S$1.65 million = S$132,000 — wiping out most of the S$150,000 gross gain and rendering the transaction loss-making after legal fees and agent commissions.

15-Month Wait-Out Period for HDB Resale

Introduced on 30 September 2022, the 15-month wait-out period (WOP) requires that private residential property owners — and those who have previously owned private property — wait at least 15 months from the date of disposal (completion of sale) before they may purchase an HDB resale flat. This measure targets the segment of upgraders and en-bloc beneficiaries who were purchasing HDB resale flats immediately after selling private property, pushing up resale prices.

There are limited exceptions: buyers aged 55 and above purchasing a 4-room or smaller HDB flat, and those in urgent housing need under specific circumstances, may apply for an exemption from the Ministry of National Development. Importantly, the WOP does not apply to Singapore Citizens purchasing HDB BTO flats — only to resale transactions.

Summary: All Current Cooling Measures at a Glance

| Measure | Regulator | Scope | Key Threshold | Effective Date |

|---|---|---|---|---|

| ABSD | MOF / IRAS | Residential property purchases | 0%–65% by buyer profile | 27 Apr 2023 |

| BSD | IRAS | All property (residential & non-res.) | 1%–6% on purchase price | Feb 2023 |

| TDSR | MAS | All bank property loans | ≤ 55% gross income | 16 Dec 2021 |

| MSR | MAS / HDB | HDB & EC (pre-TOP) | ≤ 30% gross income | 12 Jan 2013 |

| LTV (bank) | MAS | Bank loans for property | 75%→45%→35% | 16 Dec 2021 |

| LTV (HDB loan) | HDB | HDB concessionary loan | 80% | 20 Aug 2024 |

| SSD | IRAS | Private residential disposals | 12%/8%/4% (Yr 1/2/3) | 11 Mar 2017 |

| 15-Mth WOP | HDB / MND | Private owners buying HDB resale | 15 months from disposal | 30 Sep 2022 |

| EC Rules | HDB | EC buyers | Income ceil. S$16K; PR resale 10yr | 20 Aug 2024 |

Worked Example: How Cooling Measures Affect a Real Purchase Decision

Consider the Lee family. Mr Lee is a Singapore Citizen who owns a 4-room HDB flat in Tampines purchased in 2018. Mrs Lee is a Singapore Permanent Resident. They wish to upgrade to a private condominium in the Outside Central Region (OCR) priced at S$1.4 million while retaining the HDB flat as a rental investment.

ABSD impact: Mr Lee already owns one residential property (the HDB flat), so the condo is his second purchase. ABSD rate: 20% × S$1.4 million = S$280,000 — payable in cash within 14 days of the S&P Agreement. Mrs Lee, as an SPR with one existing property, would face ABSD of 30% × S$1.4 million = S$420,000. To minimise ABSD, the condo should be purchased in Mr Lee’s sole name only, incurring S$280,000.

Financing impact: Mr Lee’s gross monthly income is S$9,500. TDSR limit: S$9,500 × 55% = S$5,225. His existing HDB mortgage: S$1,350/month. Remaining TDSR room for condo loan: S$5,225 − S$1,350 = S$3,875/month. At 3.5% for 25 years, this supports a loan of approximately S$756,000. LTV limit on second bank loan: 45% × S$1.4 million = S$630,000. TDSR permits up to S$756,000 but LTV caps at S$630,000 — LTV is the binding constraint. Downpayment required: 55% × S$1.4 million = S$770,000 (of which at least 25% = S$350,000 must be in cash). Total upfront cash: BSD S$37,600 + ABSD S$280,000 + 25% cash downpayment S$350,000 + legal S$3,500 ≈ S$671,100 cash plus CPF of S$420,000 for the remaining downpayment.

Why Singapore’s Cooling Measures Are Structurally Unique

Singapore is often studied internationally as a model for demand-side property regulation. Unlike pure price controls — which distort supply incentives — or interest rate manipulation — which carries systemic financial risk — Singapore’s measures target specific buyer segments with calibrated stamp duties. The result is a market that has historically avoided the speculative boom-bust cycles seen in Hong Kong, Sydney, and Vancouver, while still delivering significant long-term capital appreciation to home owners.

The 60% ABSD for foreigners, introduced in April 2023, is the highest of any Asian gateway city and effectively prices out most foreign investors from the residential segment. This is a deliberate policy choice: Singapore wants foreigners to participate in the economy as workers and entrepreneurs — not as speculative property buyers. The corresponding result is that the Singapore residential market is predominantly owner-occupied, with the private speculative segment limited in scale.

What Might Come Next: Outlook for 2026–2027

The following section contains analytical speculation and is not a statement of government policy.

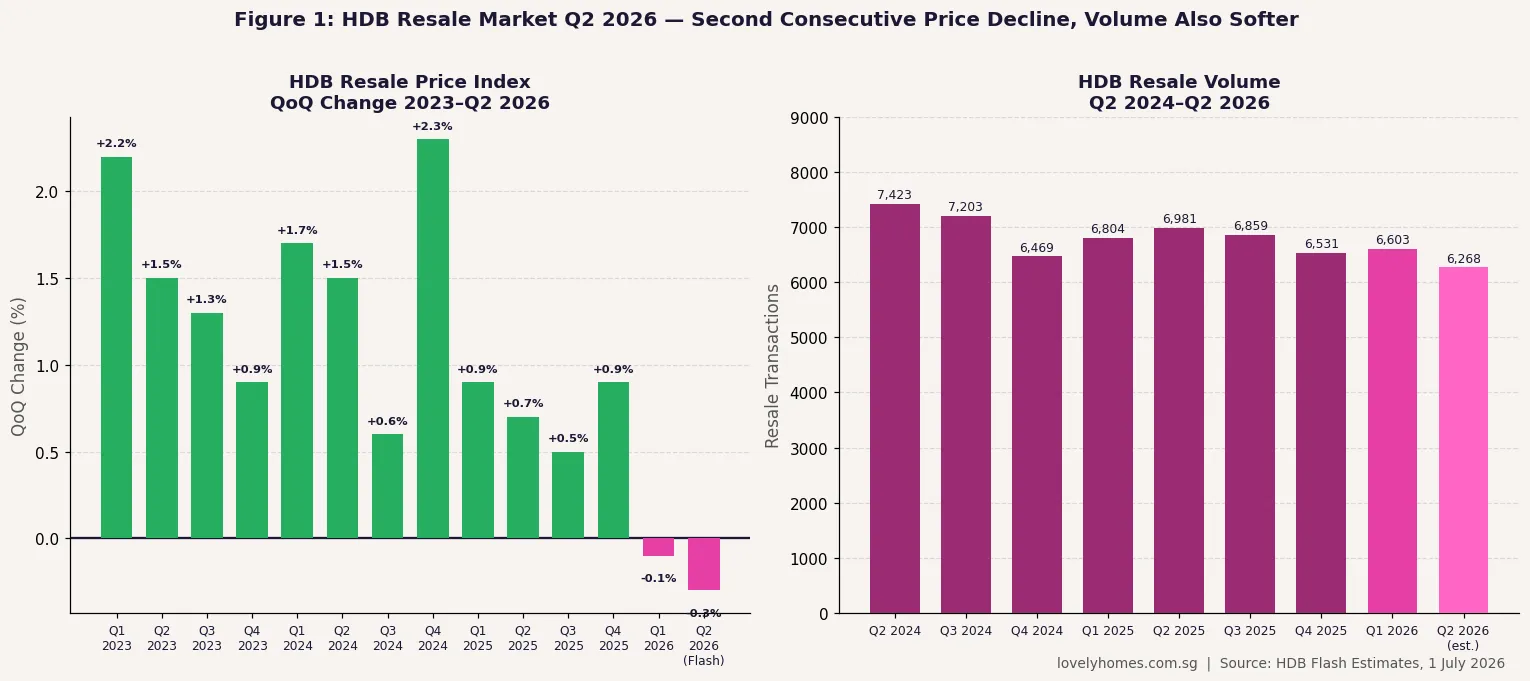

The Q2 2026 URA flash estimates showed private residential prices rising just +0.5% — a marked deceleration from Q1’s +0.9% and well below the 2021–2022 era acceleration. HDB resale prices fell for a second consecutive quarter (−0.3% in Q2 2026). Both indicators suggest the current measures are broadly achieving their goal: a cooling but not crashing market. Industry observers believe the probability of a further tightening round in 2026–2027 is low given these moderating trends. A partial relaxation — such as a modest reduction in the ABSD surcharge for SPR first-time buyers, or raising EC income ceilings to S$18,000 — is more plausible as a next move, particularly if HDB resale prices continue their downward drift. However, any relaxation for foreigners is considered highly unlikely given the political sensitivity and the Government’s stated commitment to keeping Singapore homes primarily for Singaporeans.

Frequently Asked Questions

Can I use CPF to pay ABSD?

No. ABSD must be paid entirely in cash. Unlike Buyer’s Stamp Duty (BSD), which can be funded from CPF Ordinary Account savings for the purchase of an HDB flat or private residential property, ABSD cannot be funded from CPF under any circumstances. This is an important cash-flow consideration: on a S$1.4 million condo with 20% ABSD, the buyer must have S$280,000 in liquid cash available at contract signing.

Does the TDSR apply to HDB loans?

No. The TDSR, which is governed by MAS Notice 632 and Notice MAS-655, applies only to bank and finance company property loans. HDB concessionary loans are not subject to TDSR. Instead, HDB loan applicants are subject to the MSR (≤ 30% of gross monthly income) and income ceiling eligibility criteria. However, if a buyer later refinances an HDB loan with a bank, the bank loan becomes subject to TDSR from that point forward.

My spouse is a foreigner — which ABSD rate applies?

If the property is purchased in both names (Singapore Citizen and foreign spouse), IRAS applies the higher of the two applicable ABSD rates. For a first property, the SC pays 0% and the foreigner pays 60% — so the transaction would be assessed at 60% on the full purchase price. To avoid this, the SC spouse may purchase in their sole name only, in which case ABSD is assessed solely based on the SC’s property count — potentially 0% for a first purchase. However, purchasing in sole name removes the foreign spouse from the title and has implications for CPF usage, estate planning, and stamp duty remission on future disposals. Legal advice is strongly recommended.

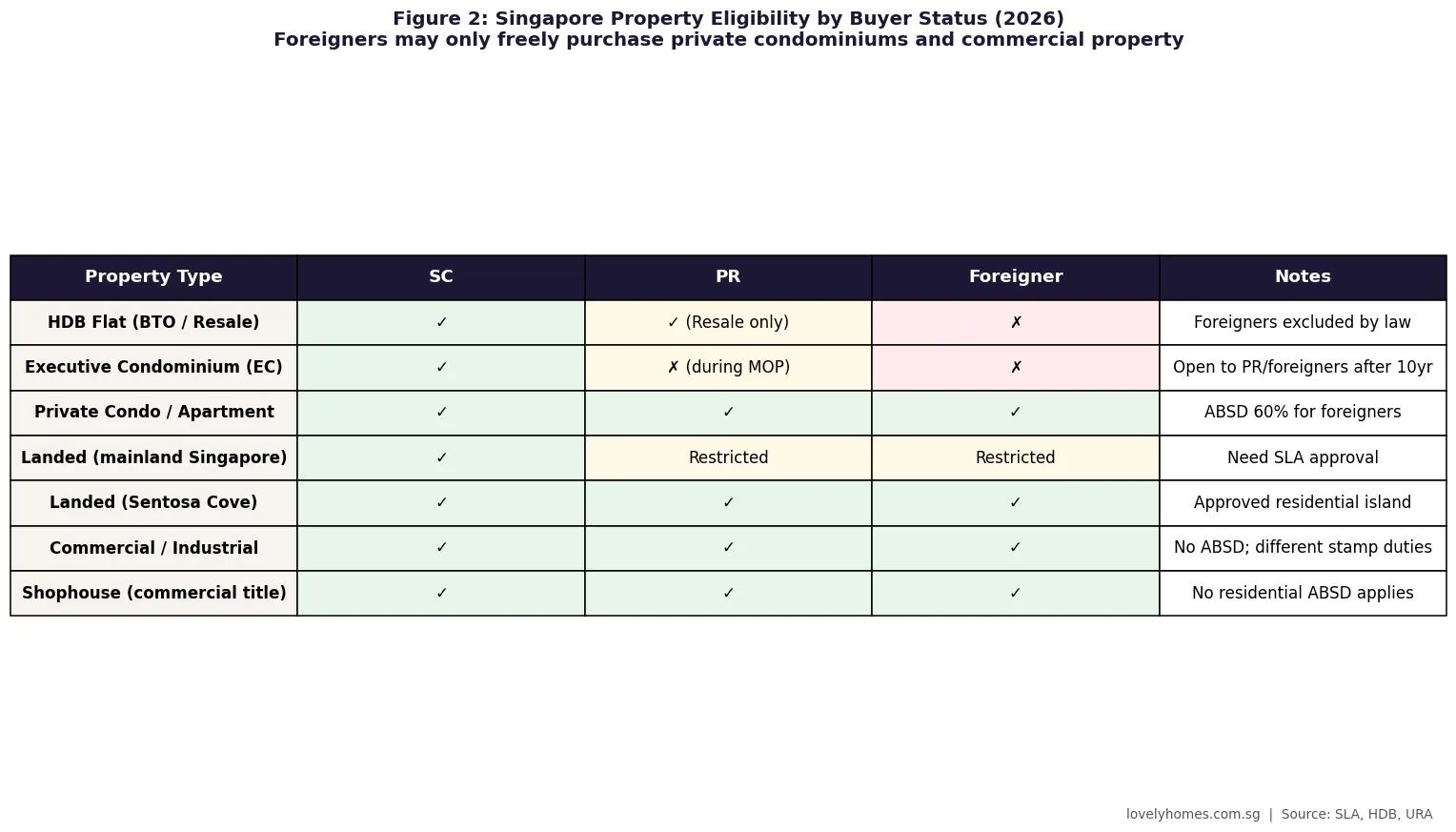

Do cooling measures apply to commercial properties?

ABSD and MSR apply only to residential properties. Commercial and industrial properties — shophouses, offices, factories, and retail units — are not subject to ABSD, and buyers of commercial property are not constrained by MSR. However, commercial property purchases are still subject to standard BSD, and the TDSR (which applies to all property loans from banks) may still constrain the loan amount available. The LTV limits for non-residential properties also differ from residential: typically 55%–80% depending on property type and loan count.

Will cooling measures ever be removed entirely?

The Singapore Government has consistently maintained that cooling measures are calibrated to market conditions and are not permanent fixtures, but their track record suggests they are structurally embedded in the regulatory landscape. Since 2009, every relaxation has eventually been followed by a tightening. The more realistic expectation is that individual components — such as specific ABSD rates for narrow buyer profiles — may be adjusted incrementally, but the framework itself (ABSD, TDSR, LTV) is likely to remain. Government spokespeople have explicitly stated that a stable, sustainable property market is a long-term national objective, and the measures are the mechanism for achieving it.

What is the property count for ABSD — does an inherited property count?

Yes. For ABSD purposes, an inherited residential property is counted as part of the buyer’s existing property count if the estate has been distributed and the property vested in the heir. This means a Singapore Citizen who inherits a private apartment and then purchases a new property is subject to ABSD at the rate applicable to their second property (20% as at 2026). The count also includes overseas residential properties for Singapore Citizens, although assessing overseas holdings is practically more complex. IRAS assesses property count at the time of the purchase being assessed.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Seller’s Stamp Duty (SSD) Guide 2026: Rates, Calculations and When It Applies

- Singapore Stamp Duty Calculator 2026: BSD and ABSD Explained

- Foreigner Buying Property in Singapore 2026: Complete Guide

- Singapore Property Cooling Measures Timeline: 2009–2026

- Singapore HDB Minimum Occupation Period (MOP) 2026: Complete Guide

Disclaimer

This article is published for general informational and educational purposes and does not constitute legal, financial, tax, or professional advice. Stamp duty rates, loan limits, and regulatory rules are subject to change by the relevant Singapore government authorities at any time; all figures cited are accurate as at 3 July 2026. Readers should verify current rates directly with IRAS (iras.gov.sg), MAS (mas.gov.sg), HDB (hdb.gov.sg), and MOF (mof.gov.sg) before making any property purchase or investment decision. LovelyHomes is not a licensed property agent, financial adviser, or legal practitioner. Always consult a qualified professional for advice specific to your circumstances.