Property Inheritance & Estate Planning Singapore 2026: Wills, CPF Nominations, Intestacy and What Happens to Your Home

Quick Answer — Property Inheritance in Singapore at a Glance

- Singapore abolished estate duty (a tax on assets passed on death) in February 2008. There is currently no estate duty in Singapore.

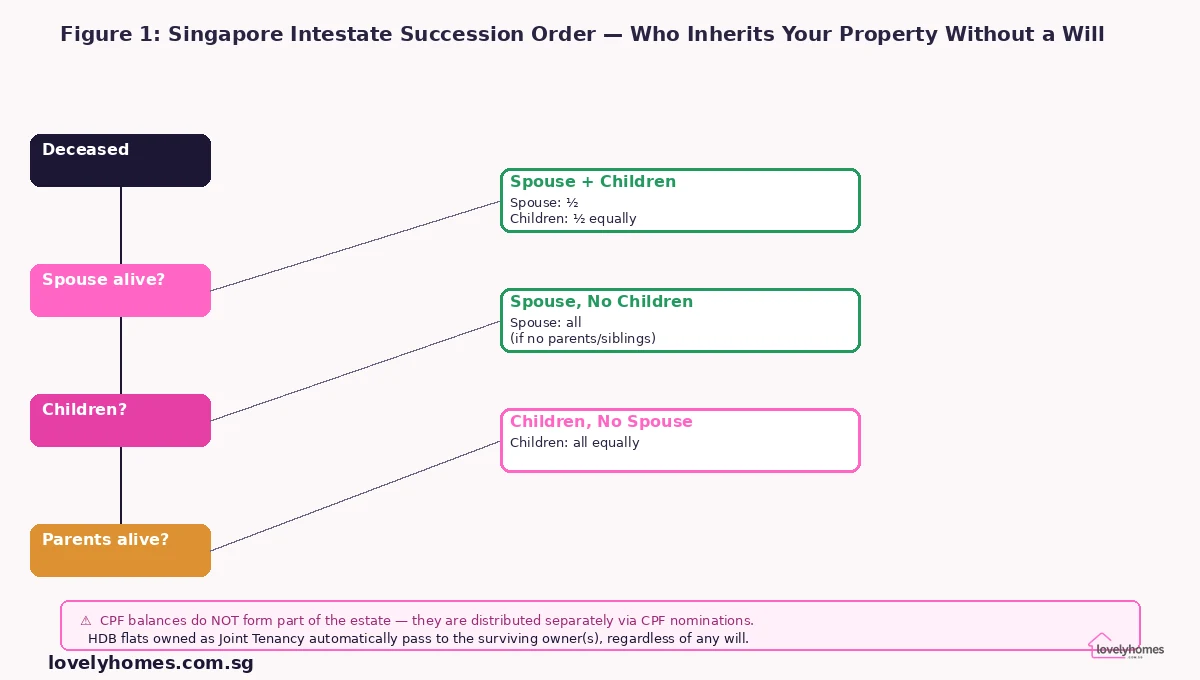

- Without a valid will, your property passes according to the Intestate Succession Act (Cap. 146) — the statutory order is spouse → children → parents → siblings → other kin.

- Muslims in Singapore follow a different framework: the Administration of Muslim Law Act (AMLA) and Faraid (Islamic inheritance law).

- CPF balances are not part of your estate and do not follow your will — they are distributed according to your CPF nomination, or to the Public Trustee if no nomination exists.

- HDB flats held under Joint Tenancy automatically pass to the surviving owner via the Right of Survivorship — bypassing both the will and intestacy rules.

- A valid will, a CPF nomination, and a Lasting Power of Attorney (LPA) are three separate documents — each serves a different purpose and all three are recommended.

- Property inheritance is administered primarily through the Public Trustee’s Office, the Family Justice Courts, and the CPF Board.

Singapore’s Estate Duty — Abolished in 2008

Before we discuss what happens to your property when you pass away, it is worth addressing one of the most persistent misconceptions in Singapore estate planning: estate duty. Singapore’s estate duty — a tax levied on the total value of assets passing on death — was abolished with effect from 15 February 2008. Estates of persons who died on or after that date are not subject to estate duty, regardless of the value of assets involved.

This is a significant advantage of Singapore as a domicile for wealth and property. Unlike jurisdictions such as the United Kingdom (where inheritance tax applies at 40% above a threshold) or the United States (which imposes federal estate tax on larger estates), Singapore imposes no tax at all on the transfer of assets upon death. The value of your property — whether a S$500,000 HDB flat or a S$5 million bungalow — passes to your beneficiaries without any estate-level deduction.

While estate duty is gone, the process of distributing a deceased’s assets still requires legal administration: obtaining a Grant of Probate (if there is a will) or Letters of Administration (if there is no will), settling debts and liabilities, and transferring property into beneficiaries’ names. These processes take time and incur legal costs even without any estate tax.

Intestate Succession — What Happens Without a Will

If a Singapore resident (non-Muslim) dies without a valid will, their estate — including any real property held in their sole name or as a Tenant-in-Common — is distributed according to the Intestate Succession Act (Cap. 146). This Act sets out a fixed statutory order of priority:

Under the ISA, if the deceased is survived by both a spouse and children, the spouse receives one half of the estate and the children share the remaining half equally. If there is a spouse but no children (and no surviving parents), the spouse inherits everything. If there are children but no spouse, the children share the estate equally. If neither a spouse nor children survive, the estate passes to the deceased’s parents, and so on down the family tree.

The crucial point is that the ISA does not allow the deceased to direct who receives what. An elderly parent may have intended to leave a private condo to one particular child — perhaps the one who cared for them — but without a will, the ISA mandates equal distribution among all children. This is one of the strongest practical arguments for drafting a will, even for individuals with relatively modest assets.

Making a Valid Will in Singapore

A will in Singapore is governed by the Wills Act (Cap. 352). To be valid, a will must be:

Written (in any language), signed by the testator (the person making the will) at the foot or end of the will in the presence of two or more witnesses who are present at the same time, and attested and subscribed by those witnesses in the presence of the testator. A witness to the will — and their spouse — cannot be a beneficiary under that same will. A beneficiary who witnesses the will loses their entitlement under it, though the will itself remains valid.

The testator must be at least 21 years of age and must be of sound mind (testamentary capacity). Wills made before marriage are automatically revoked by the subsequent marriage unless made in contemplation of that specific marriage. A divorce does not revoke a will, but a divorced spouse is treated as having predeceased the testator for the purpose of any gift to them in the will.

There is no requirement to register a will with any government agency in Singapore, though some solicitors recommend depositing a copy with the Singapore Academy of Law’s Wills Registry for a small fee, to make it easier for family members to locate the will after death.

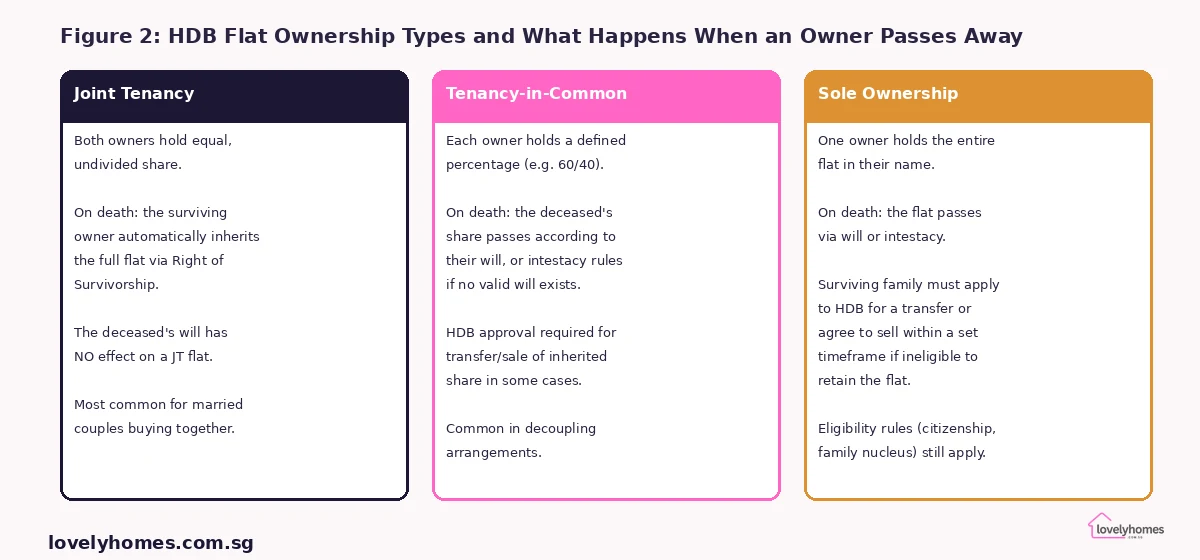

HDB Flat Inheritance — Ownership Type is Everything

For most Singaporean families, the HDB flat is the most valuable asset in the estate. How it passes on death depends critically on the type of ownership under which it is held.

Under Joint Tenancy — the most common arrangement for married couples — the Right of Survivorship means the flat automatically vests in the surviving owner(s) on the death of any one owner. No probate or letters of administration are needed for the flat itself. The surviving spouse merely needs to apply to HDB to update the ownership records with the appropriate death certificate. This is administratively simple and avoids the delays of estate administration entirely.

Under Tenancy-in-Common, each owner holds a defined percentage of the flat. This arrangement is common in decoupling scenarios (where spouses split ownership to allow one to buy a second property as a “first-time” buyer) or where unmarried co-owners hold property together. On the death of one owner, their defined share passes according to their will or intestacy rules — it does not automatically go to the surviving co-owner. HDB requires the transfer of the deceased’s share to be processed within a prescribed timeframe, and the incoming beneficiary must meet HDB eligibility criteria (citizenship, family nucleus) to retain the flat.

Where a beneficiary is ineligible to inherit a Tenancy-in-Common share (for example, a foreigner who cannot hold an HDB flat), HDB may require that the flat be sold on the open market and the proceeds distributed among beneficiaries.

CPF Balances — Separate from Your Estate

CPF savings — including the Ordinary Account, Special Account, MediSave Account, and Retirement Account — do not form part of your estate. They are not subject to your will. Instead, they are distributed according to your CPF nomination.

A CPF nomination directs the CPF Board to pay your balances to your nominated persons in the proportions you specify. Nominations are made via the CPF Online Services portal and can be updated at any time. It is important to review your nomination after major life events — marriage, divorce, the birth of children, and the death of a nominee.

If you die without a valid CPF nomination, your CPF savings are transferred to the Public Trustee’s Office, which distributes them in accordance with the Intestate Succession Act (for non-Muslims). This may delay distribution significantly — the Public Trustee process can take considerably longer than a direct CPF nomination. The administrative fee charged by the Public Trustee is also borne by the estate.

One frequently misunderstood point: the Home Protection Scheme (HPS) — the mortgage-reducing insurance tied to HDB flats — is also administered by CPF and is separate from general CPF balances. On the death of an insured HDB owner, the HPS pays out the outstanding loan directly to HDB, ensuring the flat is fully paid up. This is separate from the CPF nomination proceeds.

Private Property Inheritance and the Grant of Probate

For private property held in a deceased’s sole name or as Tenancy-in-Common, the estate must obtain a Grant of Probate (if there is a valid will) or Letters of Administration (if there is no will) before the property can be transferred to beneficiaries or sold. These are court orders issued by the Family Justice Courts that authorise the executor or administrator to deal with the estate.

The process typically involves filing a petition with the court, advertising for creditors, paying off the deceased’s debts and liabilities, and then transferring or selling the property. For a straightforward estate, this can take three to six months; for complex estates with disputes, multiple properties, or overseas assets, it can take considerably longer.

A key consideration for inherited private property is the Additional Buyer’s Stamp Duty (ABSD) position of the beneficiary. A property acquired by way of inheritance is not a “purchase” under the ABSD rules — the transfer of an inherited property does not attract ABSD on that transfer itself. However, the inherited property does count toward the beneficiary’s property count for future purchases. A Singapore Citizen who inherits a private condo and already owns their own home is considered to own two residential properties — any subsequent purchase would be at the SC second-property ABSD rate of 20%.

Worked Example — The Lim Family Estate

Mr Lim, aged 68, passes away in May 2026 without a valid will. He owned the following assets:

| Asset | Type / Notes | Estimated Value |

|---|---|---|

| Bishan 5-room HDB flat | Joint Tenancy with wife, Mrs Lim | S$900,000 |

| District 15 private condo unit | Tenancy-in-Common: Mr Lim 60%, son David 40% | S$1,200,000 (total) |

| CPF balances (OA + SA + MA) | CPF nomination: 100% to Mrs Lim | S$220,000 |

| Bank savings / cash | Sole name | S$150,000 |

Survivors: wife Mrs Lim (Singapore Citizen) and son David (Singapore Citizen, 40 years old).

What happens under intestacy:

The Bishan HDB flat passes automatically to Mrs Lim via the Right of Survivorship (Joint Tenancy). Mrs Lim applies to HDB to update ownership records. No probate needed for this asset.

The District 15 condo: Mr Lim’s 60% share (worth S$720,000) forms part of his estate. Under the ISA, with a surviving spouse and one child, Mrs Lim receives 1/2 = S$360,000 worth of the 60% share, and David receives the other 1/2 = S$360,000 worth. Added to David’s existing 40% share (worth S$480,000), David would hold an effective 70% economic interest (S$840,000) and Mrs Lim 30% (S$360,000). However, as a Tenancy-in-Common arrangement, the exact legal process involves the family obtaining Letters of Administration and then lodging a transfer of the 60% share in the proportions dictated by ISA. Both Mrs Lim and David will need to meet ABSD and property ownership rules in respect of this acquisition.

The CPF balances of S$220,000 are paid directly to Mrs Lim by the CPF Board, pursuant to Mr Lim’s existing nomination. These funds do not enter the estate at all.

The bank savings of S$150,000 form part of the estate. Under ISA, Mrs Lim receives S$75,000 and David receives S$75,000.

The key lesson: if Mr Lim had made a will directing the condo 60% share entirely to Mrs Lim (to simplify ownership and avoid David’s ABSD exposure on the inherited share), or directing specific cash amounts to his son, the distribution would have been far more tax-efficient and administratively simpler. Without a will, the family must engage a lawyer to obtain Letters of Administration, pay the Public Trustee fees (since no administrator was named), and deal with the complexity of a Tenancy-in-Common estate transfer under the ISA proportions.

Lasting Power of Attorney — Planning for Incapacity

A will takes effect only on death. A Lasting Power of Attorney (LPA) takes effect while you are still alive but have lost mental capacity. The LPA is a legal document made under the Mental Capacity Act (Cap. 177A) that appoints a donee (or donees) to make decisions on your behalf regarding personal welfare and/or property and affairs.

For property matters, an LPA with a property-and-affairs grant allows the donee to manage your bank accounts, collect rent from investment properties, sell or purchase property on your behalf, and manage your CPF affairs (to a limited extent). Without an LPA, if you lose mental capacity, your family would need to apply to the Family Justice Courts for a deputy to be appointed — a longer and more expensive process.

LPAs are registered with the Office of the Public Guardian (OPG) under the Ministry of Social and Family Development. Registration takes several weeks and requires a certificate issuer (a doctor or lawyer) to certify that you understood the document when signing it. There is a registration fee of S$75 for the standard form LPA.

Muslim Inheritance — A Different Framework

For Muslims in Singapore, property inheritance is governed by the Administration of Muslim Law Act (AMLA, Cap. 3) and Faraid — the Islamic system of inheritance. Under Faraid, the deceased’s assets are distributed to prescribed categories of heirs (such as spouse, children, parents, and siblings) in fixed shares determined by Islamic law, regardless of any contrary instructions in a will.

Muslim testators may not disinherit the heirs prescribed under Faraid, and cannot give more than one-third of their estate to non-heirs (including charities). Wills made by Muslim testators must comply with Faraid; a will that purports to override Faraid distribution is not enforceable to the extent of any excess. The Syariah Court handles inheritance matters for Muslims, including the issue of inheritance certificates (heirship certificates).

For HDB flats owned by Muslims under Joint Tenancy, the same Right of Survivorship applies — the flat passes to the surviving co-owner without going through Faraid. However, Muslim co-owners who are aware that their Faraid heirs may have an entitlement to the flat should take advice from a Muslim inheritance specialist or a lawyer with expertise in AMLA.

What Might Come Next — Policy Outlook

Singapore has not signalled any intention to reintroduce estate duty, and the Government’s consistent position has been that removing estate duty supports long-term capital accumulation and generational wealth transfer. However, several areas of estate and inheritance policy may evolve over the coming years.

The CPF nomination framework may be updated to allow more flexible or conditional nominations. Currently, CPF nominations are straightforward percentage allocations with no conditions attached. A “contingent nomination” structure — common in other jurisdictions — would allow members to specify alternative nominees if a primary nominee predeceases them. CPF Board has historically reviewed and modernised its member-facing tools periodically.

HDB’s policies on inherited flat eligibility — particularly for sole-name flats where beneficiaries may not meet the flat ownership eligibility criteria — are also periodically reviewed. As Singapore’s population ages and more HDB flats are transferred via inheritance, simplifications to the administrative process would be welcome.

Frequently Asked Questions

Can a foreigner inherit an HDB flat in Singapore?

No. HDB flats can only be owned by Singapore Citizens or Permanent Residents (and only under specific conditions for PRs, such as meeting the family nucleus requirement). If a foreigner inherits an HDB flat through a will or intestacy, they are not permitted to retain ownership of the flat. In such a situation, HDB will require the flat to be sold on the open market within a specified period and the proceeds distributed to the beneficiary. Similarly, if all remaining family members who inherit a Tenancy-in-Common HDB flat are ineligible to hold it, a sale is required. This is an important planning consideration: if you wish to leave your HDB flat to a non-citizen beneficiary, you should understand that the flat itself cannot be transferred — only the monetary value of its proceeds.

Does an inherited property attract ABSD for the beneficiary?

No — the transfer of an inherited residential property to a beneficiary does not attract ABSD on that specific transfer. ABSD applies to purchases; an inheritance is not a purchase. However, the inherited property counts toward the beneficiary’s residential property count for any future purchases. A Singapore Citizen who inherits a private condo and already owns their HDB flat would be considered a two-property owner. If they subsequently purchase another residential property, it would be subject to the 20% SC second-property ABSD (or 30% if they already own two) on the purchase price. This ABSD implication of inherited properties is frequently overlooked in estate planning discussions and can significantly affect the beneficiary’s property strategy going forward.

How long does the probate process take in Singapore for a property estate?

For a straightforward estate — a single will, no disputes, assets held only in Singapore — the Grant of Probate typically takes three to five months from the date of filing the petition with the Family Justice Courts. Where there is no will (Letters of Administration required), the process can take four to six months or more, due to the additional step of advertising for creditors and the Public Trustee’s involvement if needed. For contested estates — where family members dispute the will or the appointment of the administrator — proceedings can extend for years. The Singapore Law Society maintains a directory of probate lawyers; it is worth engaging a specialist early if the estate includes property, CPF assets, or any overseas elements, as these add complexity to the administration.

What happens to the mortgage on an inherited property?

The outstanding mortgage on a property does not disappear when the owner dies — it becomes a liability of the estate. For HDB flats covered by the Home Protection Scheme (HPS), the outstanding HDB loan balance is paid off by HPS upon the insured owner’s death, leaving the flat free of debt. For private properties with bank mortgages, the estate is liable for the outstanding loan. If the beneficiaries wish to retain the property, they must either settle the loan from estate funds, refinance the loan in their own names (subject to TDSR and lender approval), or sell the property and use the proceeds to repay the loan before distributing the balance to beneficiaries. Where the estate does not have sufficient liquid funds to service the mortgage during the probate period, the executor must arrange interim financing or seek a quick sale to prevent default.

Is a CPF nomination the same as a will?

No — a CPF nomination and a will are entirely separate legal instruments. A will governs your estate assets — property, bank accounts, investments, personal belongings — that pass on death. A CPF nomination governs only your CPF balances, which are excluded from your estate by statute. The two documents can name different beneficiaries or different proportions without conflict. Many Singaporeans make the mistake of assuming that a will automatically covers their CPF savings — it does not. If you have both a will and a CPF nomination, both are valid and operate independently. You should ensure that together they reflect a coherent overall plan: for example, that the beneficiaries of your CPF nomination are consistent with the overall distribution you intend, and that the proportion of CPF versus estate assets going to each beneficiary aligns with your wishes.

Can I change my will or CPF nomination after making them?

Yes — both can be changed at any time while you have legal capacity. A new will typically revokes the prior will if it contains a standard revocation clause; alternatively, you can execute a codicil (a supplementary document amending the existing will). A CPF nomination is changed by submitting a new nomination through the CPF Online Services portal or at a CPF Service Centre — the new nomination automatically supersedes any prior nomination. There is no limit to the number of times you may change either document. It is advisable to review both after any major life event — marriage, divorce, death of a beneficiary, birth of a child, or significant change in your asset base — to ensure they still reflect your wishes and that the named beneficiaries are still the right people.

Related Articles

- CPF Accrued Interest and Property Sales Singapore 2026: How Your Retirement Savings Affect Your Cash Proceeds

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Stamp Duty Remissions Singapore 2026: ABSD Married Couple Refund, Developer Clawback and BSD Exemptions Explained

- Strata Title & MCST Singapore 2026: Share Values, Management Funds and By-Laws Explained

- Upgrading from HDB to Private Property Singapore 2026: Step-by-Step Guide, Costs and Timing

- HDB Resale Flat Eligibility Singapore 2026: Who Can Buy, Citizenship Rules and How to Qualify

- Minimum Occupation Period (MOP) Singapore 2026: HDB, EC and Private Property Rules Explained

Disclaimer: This article is for general information only and does not constitute legal, tax, estate-planning, or financial advice. Singapore’s laws governing wills, intestacy, CPF, and HDB property ownership are subject to change. The worked example is a simplified illustration; actual outcomes will vary depending on individual circumstances, court discretion, and the specific facts of the estate. Always consult a licensed solicitor, an accredited estate planner, or the relevant government body (CPF Board, HDB, Public Trustee’s Office) before making any decisions about estate planning, property transfer, or inheritance. For Muslim inheritance queries, consult a practitioner with expertise in AMLA and Faraid. Official sources: Intestate Succession Act; CPF Nomination; HDB Transfer of Flat Ownership.