HDB Minimum Occupation Period (MOP) Singapore 2026: Standard, Plus and Prime Rules Explained

Quick Answer

- The HDB Minimum Occupation Period (MOP) is the mandatory period you must physically occupy your HDB flat before you can sell it on the open market, rent out the entire flat, or purchase a second private residential property without incurring the full ABSD burden. MOP is administered by HDB (Housing and Development Board).

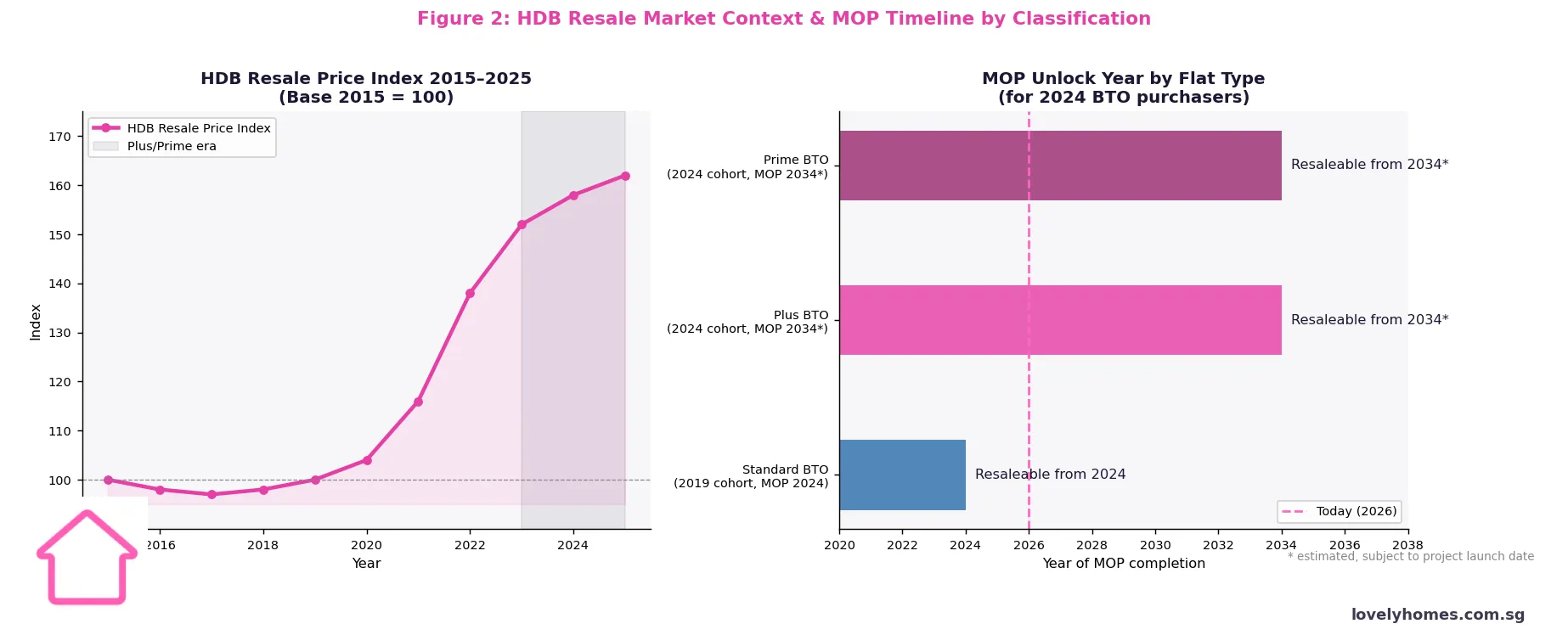

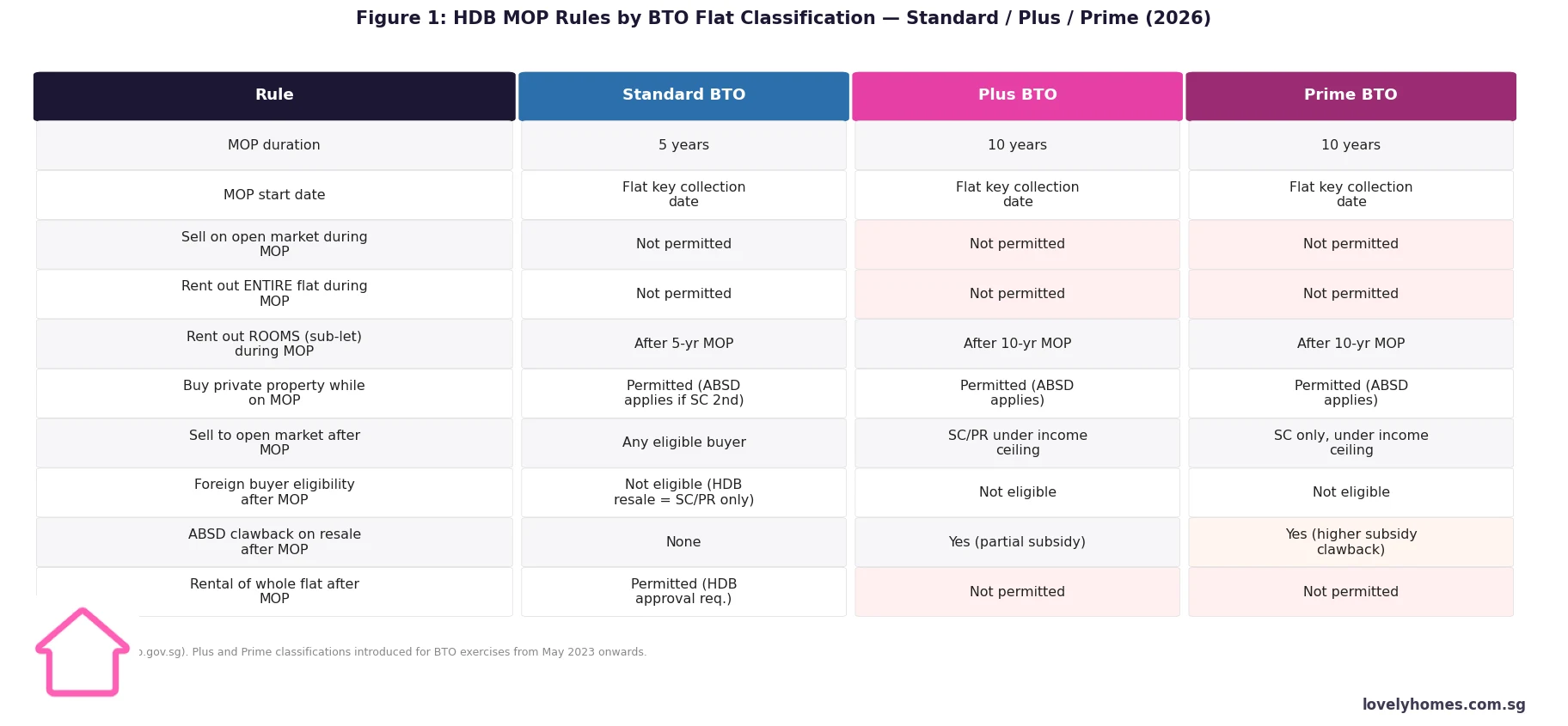

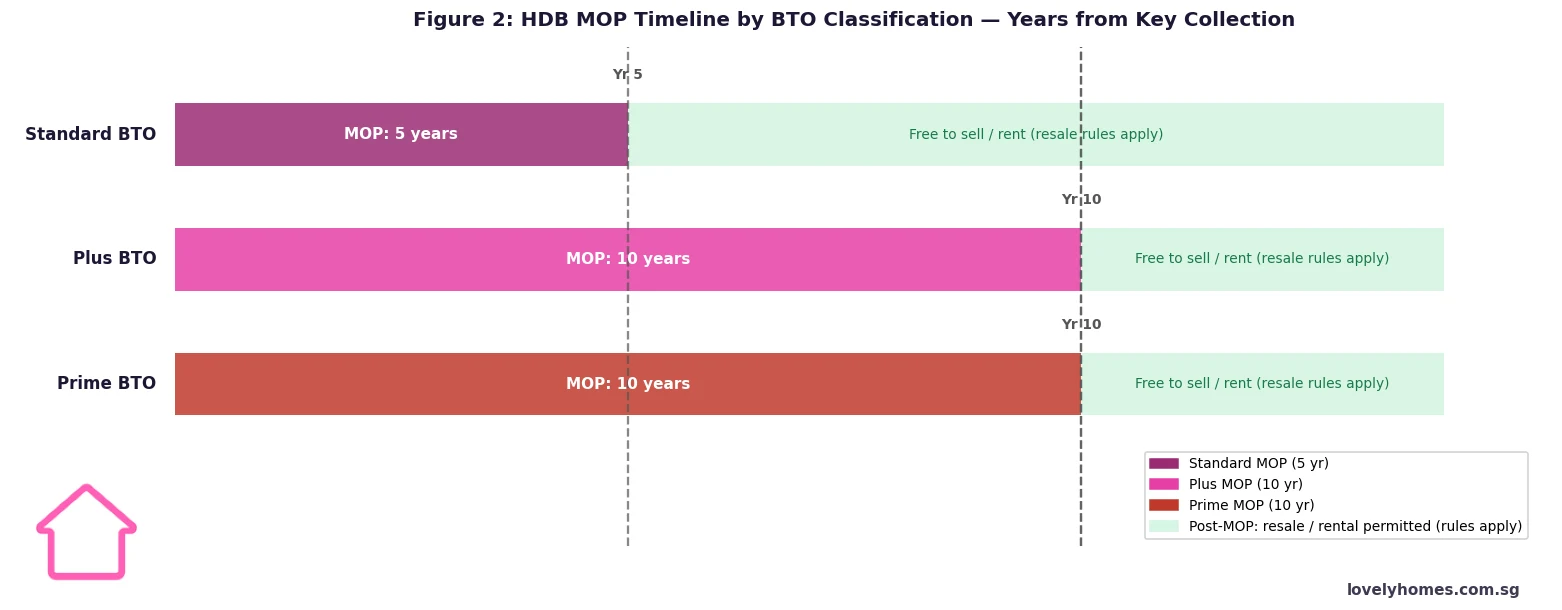

- For Standard BTO flats, the MOP is 5 years from the date of key collection. For Plus and Prime BTO flats (introduced for BTO exercises from May 2023), the MOP is 10 years.

- During the MOP, you cannot sell the flat, rent out the entire unit, or transfer ownership. You can, however, rent out individual rooms with HDB approval, and you may purchase private property (subject to ABSD).

- After the MOP, Standard flat owners may sell to any eligible HDB buyer (SC or SPR). Plus flat owners must sell to SC or SPR buyers whose household income is within the prevailing income ceiling. Prime flat owners may only sell to Singapore Citizens whose household income is within the income ceiling.

- Whole-flat rental after MOP is permitted for Standard flats (subject to HDB approval). It is not permitted at any time for Plus or Prime flats.

- A subsidy clawback applies when Plus and Prime flats are sold on the open market — HDB recovers a portion of the housing grant and pricing subsidy. The clawback amount is higher for Prime flats.

- The MOP clock starts from the date of key collection — not the date of BTO application, booking fee payment, or Temporary Occupation Permit (TOP). A flat collected in June 2024 has its Standard MOP expiry in June 2029.

What Is the MOP and Who Administers It?

The Minimum Occupation Period (MOP) is a statutory requirement under the Housing and Development Act, administered by the Housing and Development Board (HDB). It requires owners of HDB flats to physically occupy their flat for a minimum period before certain rights become available — primarily the right to sell on the open market, rent out the entire unit, or purchase a second private residential property.

The MOP exists for two complementary policy reasons. First, it ensures that subsidised HDB flats are used as genuine owner-occupied homes rather than short-term investment instruments. Second, it moderates the supply of resale HDB flats that enter the market at any one time, which helps to stabilise resale prices. The requirement has been part of Singapore’s public housing policy for decades, and HDB enforces it through its ownership records, which are cross-referenced against the buyer’s NRIC address for SC/SPR buyers.

Standard, Plus and Prime: The Three BTO Classifications

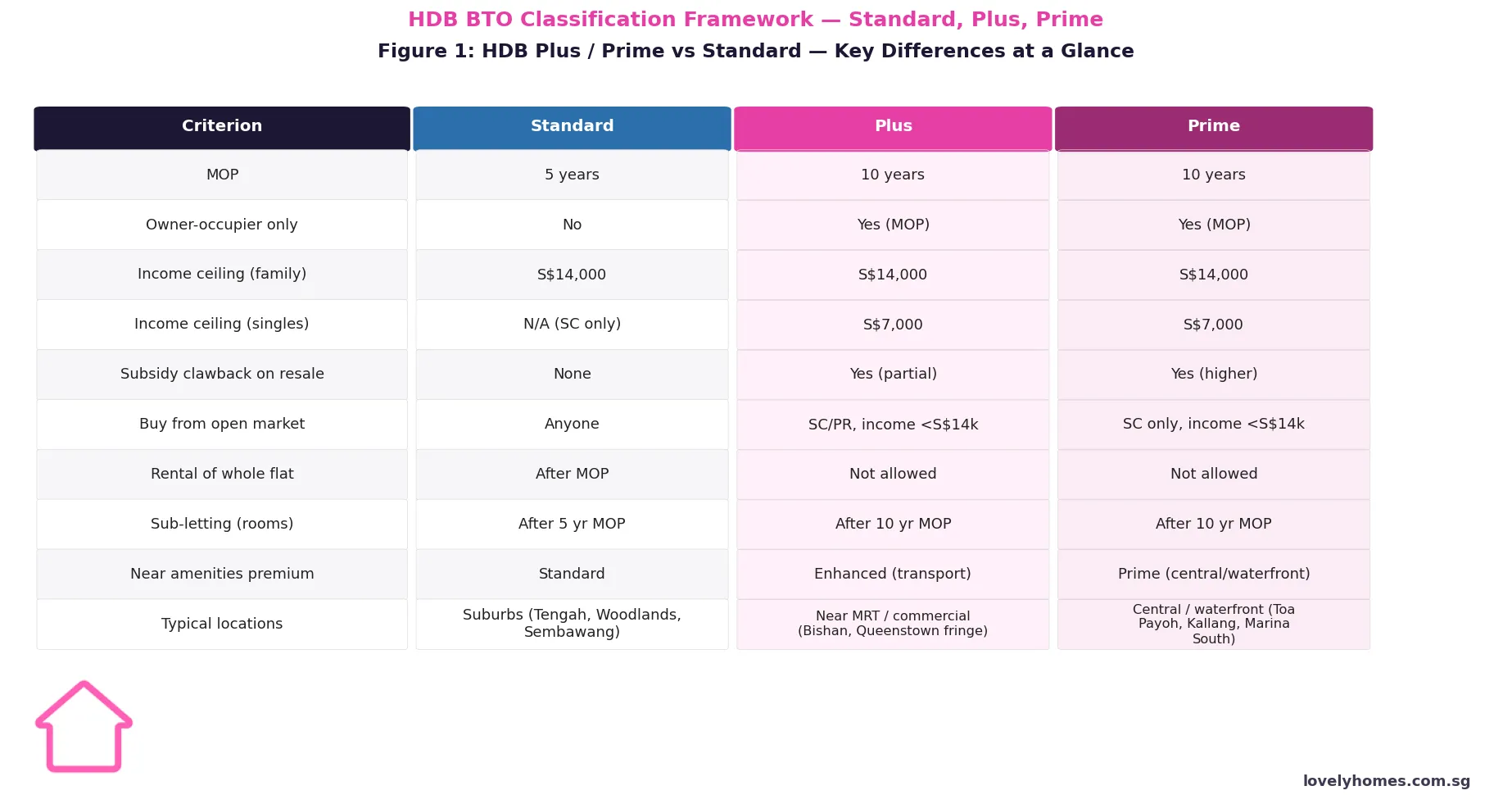

From the May 2023 BTO exercise onwards, HDB classifies all new BTO flats into one of three tiers based on location and subsidy level. This classification directly determines MOP length, post-MOP resale eligibility, rental rights, and subsidy clawback:

- Standard flats are located in non-central, typically suburban estates (such as Tengah, Woodlands, Sembawang, and Punggol). They carry the lowest subsidies relative to market value and have the most permissive rules: 5-year MOP, resale to any eligible SC/SPR buyer, and whole-flat rental allowed after MOP with HDB approval.

- Plus flats are located near transport nodes or commercial hubs, in estates that would otherwise be too pricey for first-timer buyers without additional subsidy. They come with a 10-year MOP, resale restricted to SC/SPR buyers within the prevailing income ceiling, and no whole-flat rental at any time.

- Prime flats are located in the choicest sites — city-fringe, waterfront, or mature central estates like Kallang, Toa Payoh, and Marina South — where HDB provides the heaviest subsidies. They carry a 10-year MOP, SC-only resale (SPR buyers are ineligible), income ceiling restrictions, no whole-flat rental at any time, and the highest clawback rate.

Buyers are told which classification a flat falls under at the time of BTO application. The classification is permanently attached to the flat and does not change over time, even after resale. A Prime flat remains a Prime flat in every subsequent transaction.

What You Can and Cannot Do During the MOP

The MOP does not mean you are locked away from all activity — it specifically restricts disposal and whole-unit rental. The table below summarises key permitted and prohibited actions:

| Activity | During MOP | After MOP (Standard) | After MOP (Plus/Prime) |

|---|---|---|---|

| Sell flat on open market | Not permitted | Permitted (SC/SPR buyers) | SC/PR (Plus); SC only (Prime); income ceiling applies |

| Rent out entire flat | Not permitted | Permitted (HDB approval) | Not permitted (ever) |

| Rent out rooms (sub-let) | Not permitted during MOP | Permitted (HDB approval) | Permitted (HDB approval) |

| Buy private property | Permitted (ABSD applies if SC 2nd property: 20%) | Permitted | Permitted |

| Transfer ownership (gift / divorce / death) | HDB approval case-by-case | Yes | Yes (subject to Plus/Prime resale rules) |

| Renovate / alter the flat | Permitted (HDB renovation permit) | Permitted | Permitted |

Buying Private Property During the MOP

One of the most common questions from HDB flat owners is whether they can buy a private condominium before their MOP is up. The answer is yes — you are allowed to purchase private residential property in Singapore while your MOP is running. However, there are important financial consequences to consider.

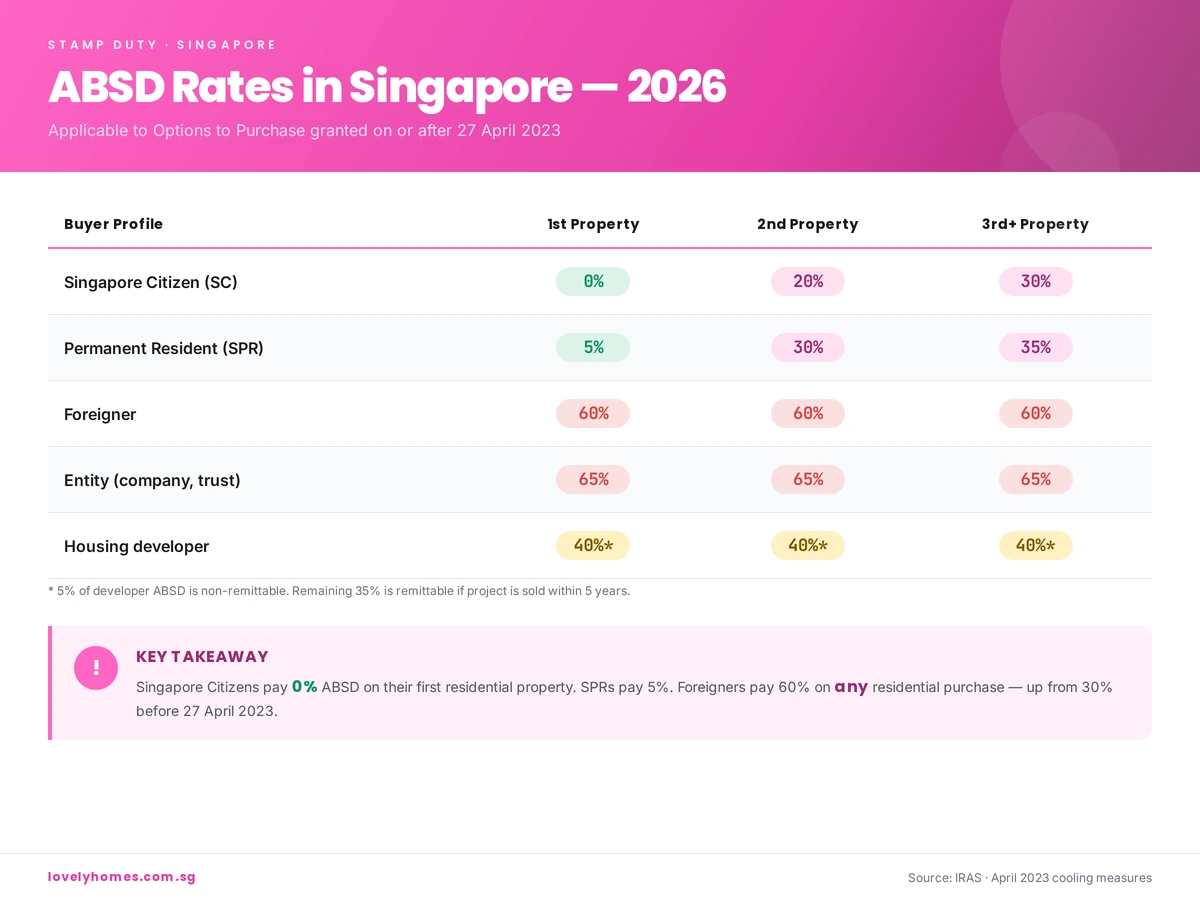

If you are a Singapore Citizen owning an HDB flat (which counts as your first residential property) and you buy a private condo during the MOP, you are buying a second property. This means you pay 20% ABSD on the private property purchase. If you are an SPR, your second-property ABSD is 30%. The HDB flat itself remains subject to the MOP and cannot be sold until the MOP expires.

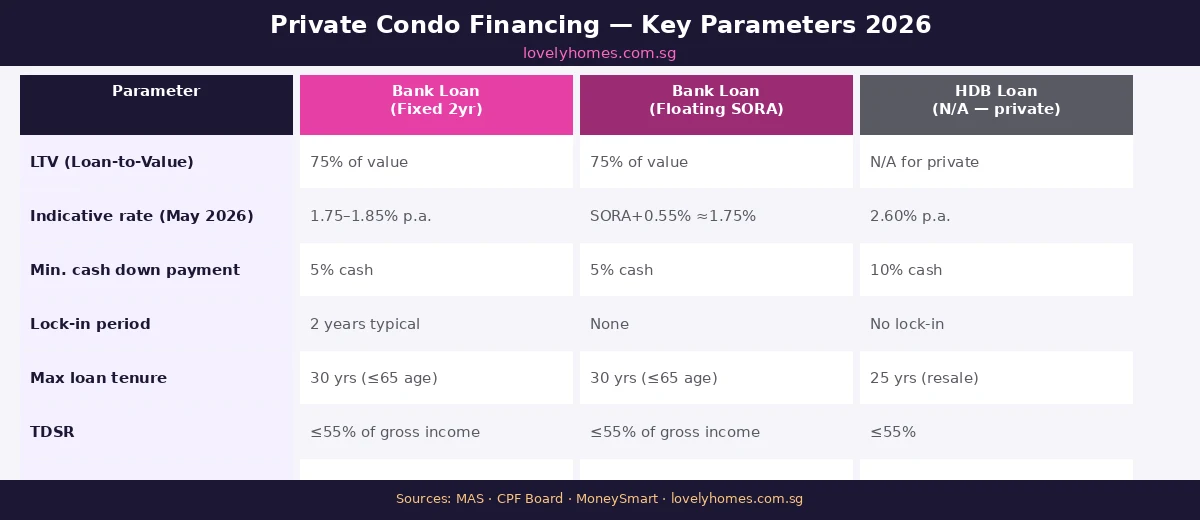

This means you will be servicing two housing loans simultaneously until the HDB can be sold — which requires careful TDSR planning. The TDSR cap of 55% applies across all outstanding loans. HDB loans (from HDB directly) and bank loans on HDB flats are both counted in TDSR. If the combined debt servicing ratio exceeds 55% when adding the private mortgage, financing for the private property may be declined.

What Happens When You Sell After the MOP

Once the MOP is fulfilled, the key restrictions are lifted — but resale rules still apply, especially for Plus and Prime flats:

- Standard flats: May be sold to any eligible HDB resale buyer — SC or SPR, subject to standard HDB eligibility criteria (Ethnic Integration Policy quotas, family nucleus requirements, etc.). No income ceiling on the buyer.

- Plus flats: May only be sold to buyers whose household income does not exceed the prevailing income ceiling (currently S$14,000/month for families, S$7,000 for singles). SPR buyers are eligible. A subsidy clawback is deducted from the sale proceeds on the first open-market resale.

- Prime flats: May only be sold to Singapore Citizen buyers (SPR buyers are not eligible) whose household income does not exceed the income ceiling. The subsidy clawback rate is higher than for Plus flats and is also deducted from the first open-market resale proceeds.

The subsidy clawback is calculated as a percentage of the resale price (or market value, whichever is higher) and is paid to HDB at the point of resale. HDB has not publicly released a fixed clawback percentage table; the exact rate is determined and communicated at the time of application. This is intended to recover some of the subsidy advantage enjoyed by Plus/Prime buyers while still allowing them a fair profit on genuine capital appreciation.

The MOP and CPF Accrued Interest

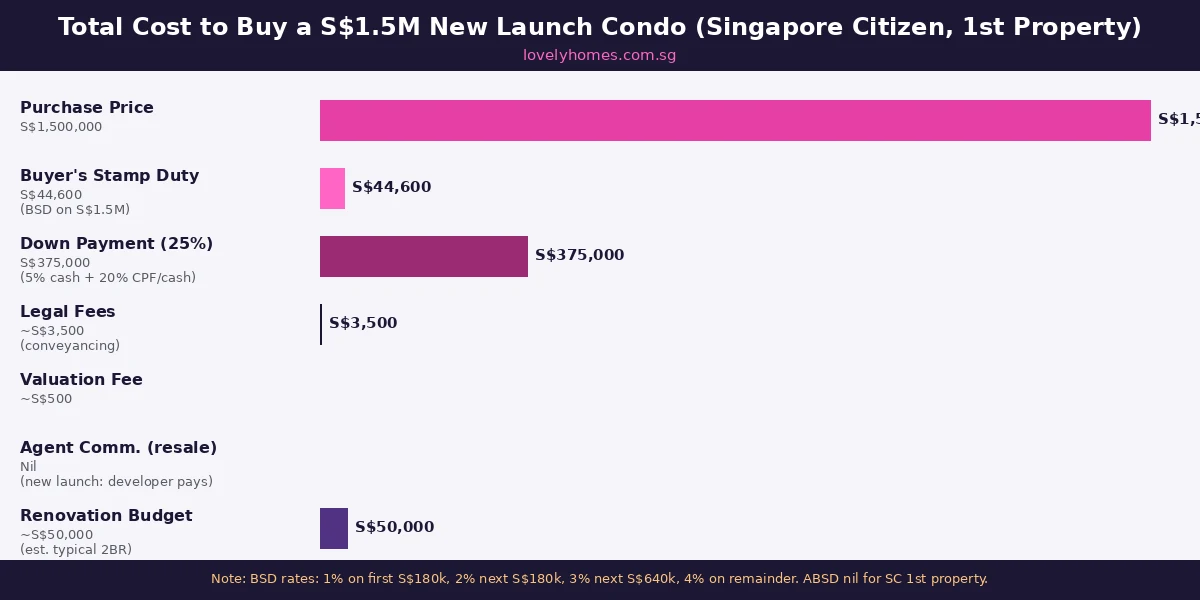

When you sell an HDB flat after the MOP, any CPF funds used to purchase the flat (including the option fee, downpayment, and monthly mortgage instalments paid from your CPF Ordinary Account) must be refunded to your CPF accounts — along with accrued interest at the CPF OA interest rate (currently 2.5% per annum). This accrued interest represents what your CPF savings would have earned had they not been used for housing. On a long MOP (10 years), accrued interest can be substantial and reduces the net cash proceeds from the sale.

Worked Example: The Wong Family and the MOP Decision

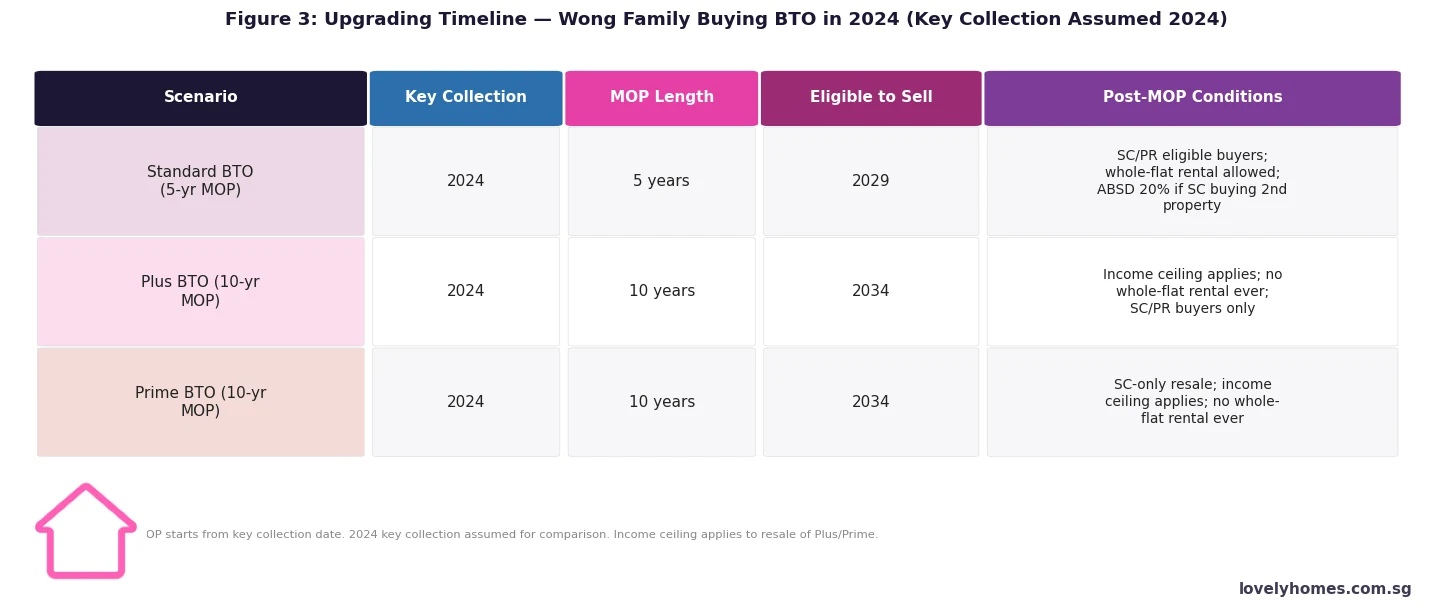

Mr and Mrs Wong, both Singapore Citizens, purchase a 4-room BTO flat in Bishan (classified as a Plus flat) in June 2024. Key collection is in June 2024. Their household income is S$9,000/month. The purchase price is S$550,000.

| Scenario | Event | Year | Notes |

|---|---|---|---|

| Plus BTO — Bishan | Key collection | 2024 | MOP clock starts |

| Buy private condo (2nd property, if desired) | Any time | 20% ABSD applies; TDSR must clear; HDB MOP still running | |

| MOP expires — eligible to sell HDB | 2034 | 10-year MOP; income ceiling on buyer (S$14k); clawback on sale proceeds | |

| Can rent out rooms (sub-let) | From 2034 | HDB approval required; cannot rent entire flat (ever) |

Over the 10-year MOP, if the flat appreciates from S$550,000 to S$800,000 (a not unreasonable assumption for a Plus-classified Bishan flat), the Wongs would make a nominal gross gain of S$250,000. From this, HDB deducts the clawback (amount TBD at point of sale), plus CPF refund with accrued interest. On a S$550,000 purchase with 25% CPF downpayment (S$137,500) at 2.5% CPF OA rate over 10 years, accrued interest alone would be approximately S$38,700 — reducing net cash-in-hand from the sale. This is still a solid return, but buyers should model it carefully before factoring in the Plus flat subsidy as pure profit.

What This Means for HDB Buyers in 2026

The 10-year MOP for Plus and Prime flats is a significant commitment. A buyer collecting keys in 2026 cannot sell their Plus or Prime flat until 2036 at the earliest. Over that decade, Singapore’s property market will go through multiple cycles, interest rate shifts, and policy changes. Buyers who select Plus or Prime flats primarily because of the lower purchase price — and not because they genuinely intend to occupy the flat for 10 years — may find themselves in a difficult position if circumstances change (job relocation overseas, family expansion, divorce).

For those who do plan to stay, the Plus and Prime schemes deliver real value. A Prime flat in a central location at a subsidised price, occupied for 10 years with a no-rental restriction, is likely to appreciate meaningfully in absolute terms even after clawback. The restriction is the price of the subsidy.

What Might Come Next

The May 2023 introduction of Plus and Prime classifications represented a significant shift from the old Mature/Non-Mature estate binary. The April 2023 announcement also removed the ability of EC buyers to use the Deferred Payment Scheme from May 2026 — suggesting the government continues to tighten across all public and quasi-public housing tiers. Any further changes to MOP duration are unlikely in the near term given that the 10-year Plus/Prime MOP is relatively new and the government will want to assess its impact before adjusting. The resale income ceiling may, however, be revised upwards over time to track median income growth in Singapore.

Related Articles

- HDB Plus and Prime Flats Singapore 2026: What the BTO Classification Means for Buyers

- HDB BTO Application and Ballot System Singapore 2026: Priority Schemes and Ballot Odds

- Enhanced Housing Grant (EHG) Singapore 2026: Who Qualifies, How Much and How to Apply

- Upgrading from HDB to Private Property Singapore 2026: Cost, ABSD and Timing Guide

- CPF Accrued Interest and Property Sales Singapore 2026: How It Affects Your Cash Proceeds

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- HDB Resale Flat Eligibility Singapore 2026: Who Can Buy and How to Qualify

Frequently Asked Questions

When does the MOP start — from key collection or from BTO ballot application?

The MOP starts from the date of key collection — not the date of BTO application, not the ballot exercise date, and not the date you pay the option fee or sign the lease agreement. The key collection date is when you physically receive the keys to your flat and formally take possession. This date is recorded by HDB and serves as the MOP commencement date. For a Standard flat collected in July 2024, the MOP expires in July 2029. For a Plus or Prime flat collected in the same month, it expires in July 2034.

Can I rent out rooms in my HDB flat while the MOP is running?

No. During the MOP, you may not rent out any part of your flat — neither the entire unit nor individual rooms. Room rental (sub-letting) is only permitted after the MOP has been fulfilled and only with HDB’s prior written approval. After the MOP, Standard flat owners may rent out rooms or the entire flat (with HDB approval); Plus and Prime flat owners may rent out rooms after the MOP but may never rent out the entire flat under any circumstances.

What happens if I need to move overseas for work during the MOP?

If you need to work overseas temporarily, you must continue to maintain your HDB flat as your Singapore residence — meaning a family member must continue to reside in the flat, and you must return periodically. You cannot rent out the flat during the MOP even if you are overseas. If your overseas stint is long-term and the flat will genuinely be unoccupied, you should consult HDB directly. Abandoning the occupancy requirement during the MOP can result in HDB compulsorily acquiring the flat at a below-market price under the Housing and Development Act — a severe consequence that buyers should be aware of.

Can I buy a private condo while my HDB MOP is still running?

Yes. Purchasing a private residential property while your HDB MOP is outstanding is permitted. However, since your HDB flat counts as your first residential property, the private condo purchase is classified as a second property for ABSD purposes. A SC pays 20% ABSD on the private condo. An SPR pays 30%. You must also have the financial capacity to service both housing loans simultaneously and remain within the 55% TDSR cap. Many HDB owners choose to exercise this option a year or two before their MOP expires, so the HDB can be sold shortly after the MOP milestone — reducing the period of dual-loan exposure.

What is the subsidy clawback for Plus and Prime flats, and when is it paid?

The subsidy clawback for Plus and Prime flats is paid to HDB at the point of the first open-market resale (i.e., the first resale transaction after the MOP). It is deducted from the sale proceeds before any balance is paid to the seller. The clawback is calculated as a percentage of the resale price or market valuation (whichever is higher). HDB has not published a fixed percentage table publicly; the exact rate is communicated in the flat purchase document at the time of BTO booking and is specific to the flat’s classification and location. The clawback only applies to the first open-market resale — subsequent owners of a Plus or Prime flat do not face an additional clawback when they eventually sell.

Do MOP rules apply to HDB flats purchased on the open resale market?

Yes. When you purchase an HDB resale flat — whether Standard, Plus, or Prime — the MOP requirement applies afresh from the date you collect the keys. A Standard resale flat has a 5-year MOP from your key collection date; a Plus resale flat has a 10-year MOP; and a Prime resale flat has a 10-year MOP. The classification (Standard, Plus, Prime) of the flat follows it through all transactions. You cannot shorten the MOP on a resale flat because the previous owner already fulfilled their MOP.

Can an SPR buyer purchase a Plus or Prime HDB flat on the open resale market?

For Plus flats: yes, subject to the income ceiling (S$14,000/month household income) and standard SPR eligibility criteria. For Prime flats: no — Prime flats may only be resold to Singapore Citizens (not SPR). This restriction applies to every resale of a Prime flat in perpetuity, not just the first resale. SPR buyers wishing to purchase Plus flats must also form an eligible family nucleus (e.g., SC/SPR family or SPR household of two or more) to qualify under HDB’s resale eligibility framework.

Disclaimer: This article is for general information only and does not constitute legal or financial advice. HDB rules, MOP durations, clawback rates, and eligibility criteria are subject to change by HDB and the Ministry of National Development. Always verify the latest requirements at hdb.gov.sg and consult HDB directly or a licensed HDB resale agent for guidance specific to your situation. All figures and scenarios are illustrative and based on publicly available data as at 16 May 2026.