June 2026 BTO Results: Berlayar Rise and Lakeview Cascadia Dominate With 4.5-4.7 Times Oversubscription

The June 2026 Build-To-Order (BTO) sales exercise closed on 24 June 2026 after five days of applications, confirming a pattern that has defined Singapore’s public housing market all year: Prime-classified projects in central and mature estates are dramatically oversubscribed, while Standard projects in the north and north-east attract softer demand — in some cases failing to reach full first-timer subscription. Here is the complete picture.

Quick Answer — June 2026 BTO Results at a Glance

- 6,952 flats launched across 7 projects in Ang Mo Kio, Bishan, Bukit Merah, Sembawang, and Woodlands.

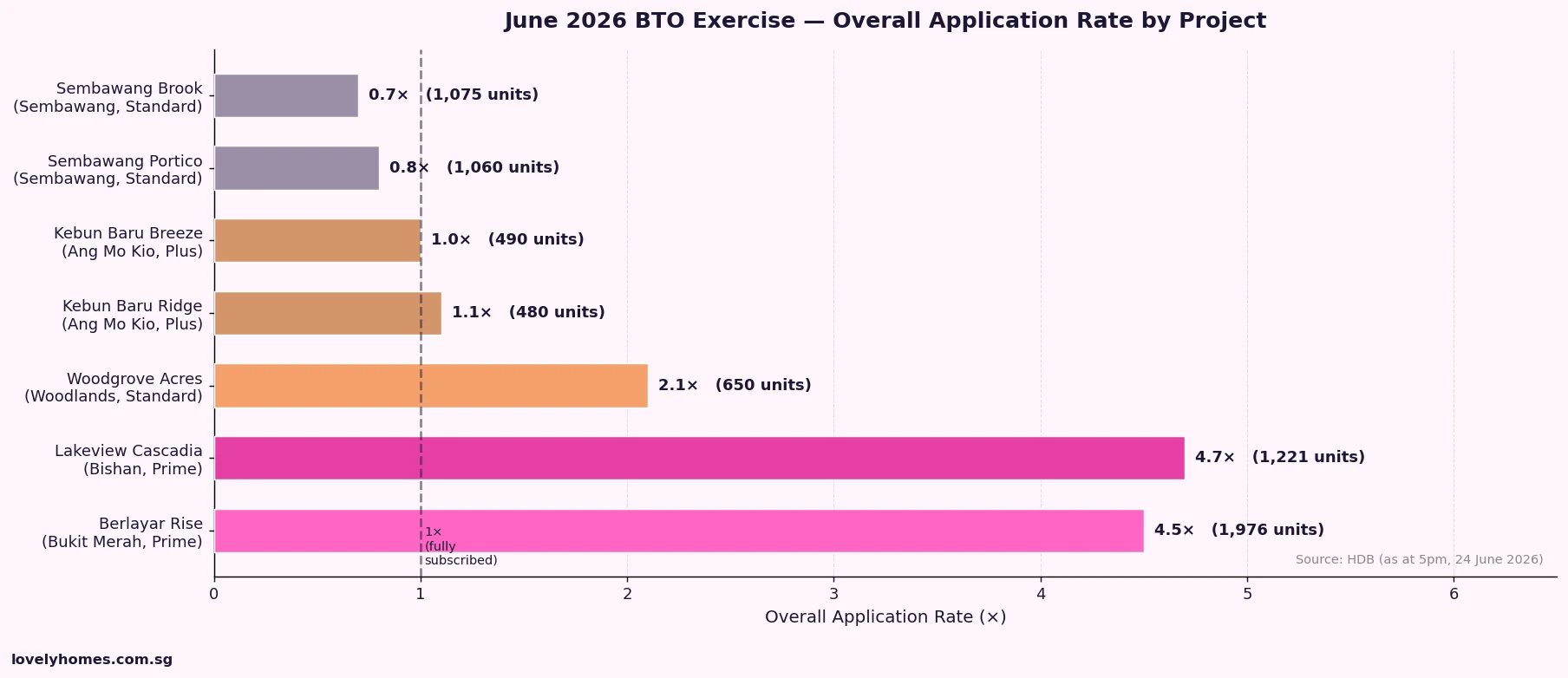

- Total applications: 22,634 — overall subscription rate of 3.3 times (as at 5pm, 24 June 2026).

- Star project: Berlayar Rise (Bukit Merah, Prime) — 8,824 applications, 4.5× oversubscribed. Nearly 40% of all applications in the exercise.

- Runner-up: Lakeview Cascadia (Bishan, Prime) — 5,799 applications, 4.7× for certain flat types.

- Weakest demand: Sembawang Portico and Sembawang Brook — first-timer family rates fell below 1× for all 3-room and larger flat types.

- Singles demand surge: Woodgrove Acres (Woodlands) 2-bedroom flexi units hit 17.8× for first-timer singles.

- More than 2,500 flats offered have wait times of three years or less under HDB’s expedited build programme.

The Full Project-by-Project Breakdown

| Project | Town | Classification | Units | Applications | Overall Rate |

|---|---|---|---|---|---|

| Berlayar Rise | Bukit Merah | Prime | 1,976 | 8,824 | 4.5× |

| Lakeview Cascadia | Bishan | Prime | 1,221 | 5,799 | 4.7× |

| Woodgrove Acres | Woodlands | Standard | ~650 | — | ~2× (singles 17.8×) |

| Kebun Baru Ridge | Ang Mo Kio | Plus | ~480 | — | ~1.1× (3-room 2T: 22.9×) |

| Kebun Baru Breeze | Ang Mo Kio | Plus | ~490 | — | ~1.0× |

| Sembawang Portico | Sembawang | Standard | ~1,060 | — | <1× (families) |

| Sembawang Brook | Sembawang | Standard | ~1,075 | — | <1× (families) |

Source: HDB. Application rates as at 5pm, 24 June 2026. Woodgrove Acres, Kebun Baru, and Sembawang project unit counts are approximate; official HDB breakdown shows total 6,952 units across all 7 projects.

Berlayar Rise: The Greater Southern Waterfront Magnet

Berlayar Rise in Bukit Merah accounted for nearly 40% of all applications in the June exercise — a remarkable concentration of demand in a single project. The draw is straightforward: this is a Prime-classified development integrated with Telok Blangah MRT station on the Circle Line, positioned squarely within the Greater Southern Waterfront (GSW) transformation precinct. Prices for 4-room flats are estimated to start from around S$580,000 — a figure that, while elevated for public housing, represents a meaningful discount to what an equivalent private resale unit in the Telok Blangah/Bukit Merah corridor would cost (typically S$1.2–1.6 million for a comparable size).

The Prime designation means buyers are subject to the standard Prime location conditions: a 10-year Minimum Occupation Period (MOP), an income ceiling of S$14,000 for families, and subsidy clawback on resale (estimated at approximately 14%, based on the precedent set by the nearby Berlayar Residences project). For buyers who can meet those conditions and want a foothold in the GSW story, Berlayar Rise offers compelling long-term value. The development sits near the future Telok Blangah market and hawker centre, and the broader GSW transformation — connecting Keppel, Harbourfront, and Pasir Panjang — is a generational urban-planning project that will unfold over the next 15–20 years.

Prime vs Plus vs Standard: A Market Verdict

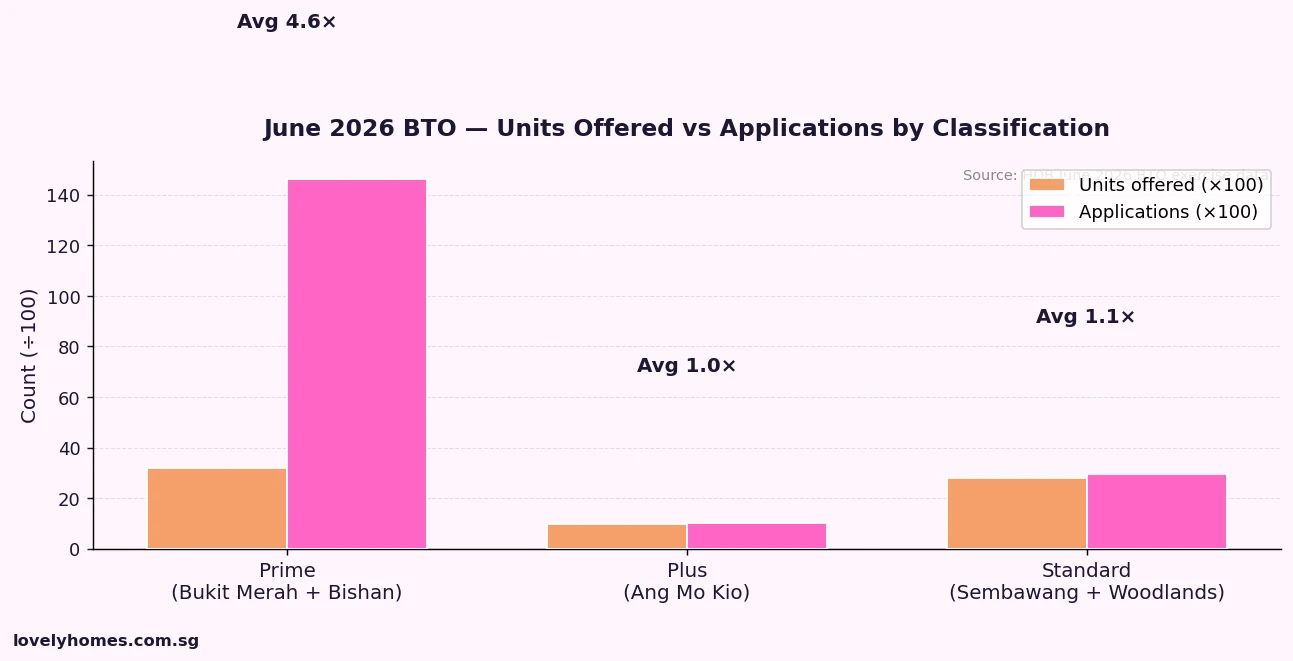

The June 2026 results are the clearest data point yet that Singapore’s three-tier BTO classification system (Prime, Plus, Standard) is functioning broadly as intended — but with some unintended consequences at the Standard end.

Prime projects (Berlayar Rise and Lakeview Cascadia) together offered 3,197 units but attracted approximately 14,623 applications — an average rate of 4.6 times. This is precisely the outcome the Government anticipated when it introduced the classification: demand for centrally located, well-connected projects is intense, and the subsidy recovery and MOP conditions are not deterring buyers who value location above all else.

Plus projects (Kebun Baru Breeze and Ridge in Ang Mo Kio) sat at approximately 1× overall subscription for first-timer families — marginally fully subscribed, which means successful ballots are likely but not certain for this cohort. The Plus designation was designed to sit between Prime and Standard in both location quality and subsidy level, and the Ang Mo Kio projects are genuinely well-located (D20, established mature estate, near Yio Chu Kang and Ang Mo Kio MRT). The lukewarm response may reflect the Plus conditions — 6-year MOP and clawback provisions — deterring the upgrader segment that has traditionally been the main buyer of Ang Mo Kio BTO flats.

Standard projects in Sembawang fell below full subscription for families. This is consistent with the market’s verdict on northern Singapore’s accessibility: despite the upcoming Cross Island Line (CRL) timeline, Sembawang remains a long commute for most CBD workers. The two projects together offered over 2,100 units — the largest supply block in the exercise — but attracted insufficient family demand to be oversubscribed. Unsuccessful ballot applicants from more competitive projects will likely be allocated here under HDB’s concession scheme.

The Singles Story: Woodlands Breaks Records

The most striking single data point in the June exercise was Woodgrove Acres in Woodlands: 2-bedroom flexi flats — the designated flat type for first-timer singles — were 17.8 times oversubscribed. This is an extraordinary figure that reflects both the shortage of BTO supply for singles (who are restricted to 2-bedroom flexi flats) and the growing demographic weight of single-person households in Singapore. The government has been incrementally expanding singles’ eligibility for BTO housing, but the 17.8× rate suggests the supply pipeline for singles remains severely constrained relative to demand.

What This Means for BTO Applicants

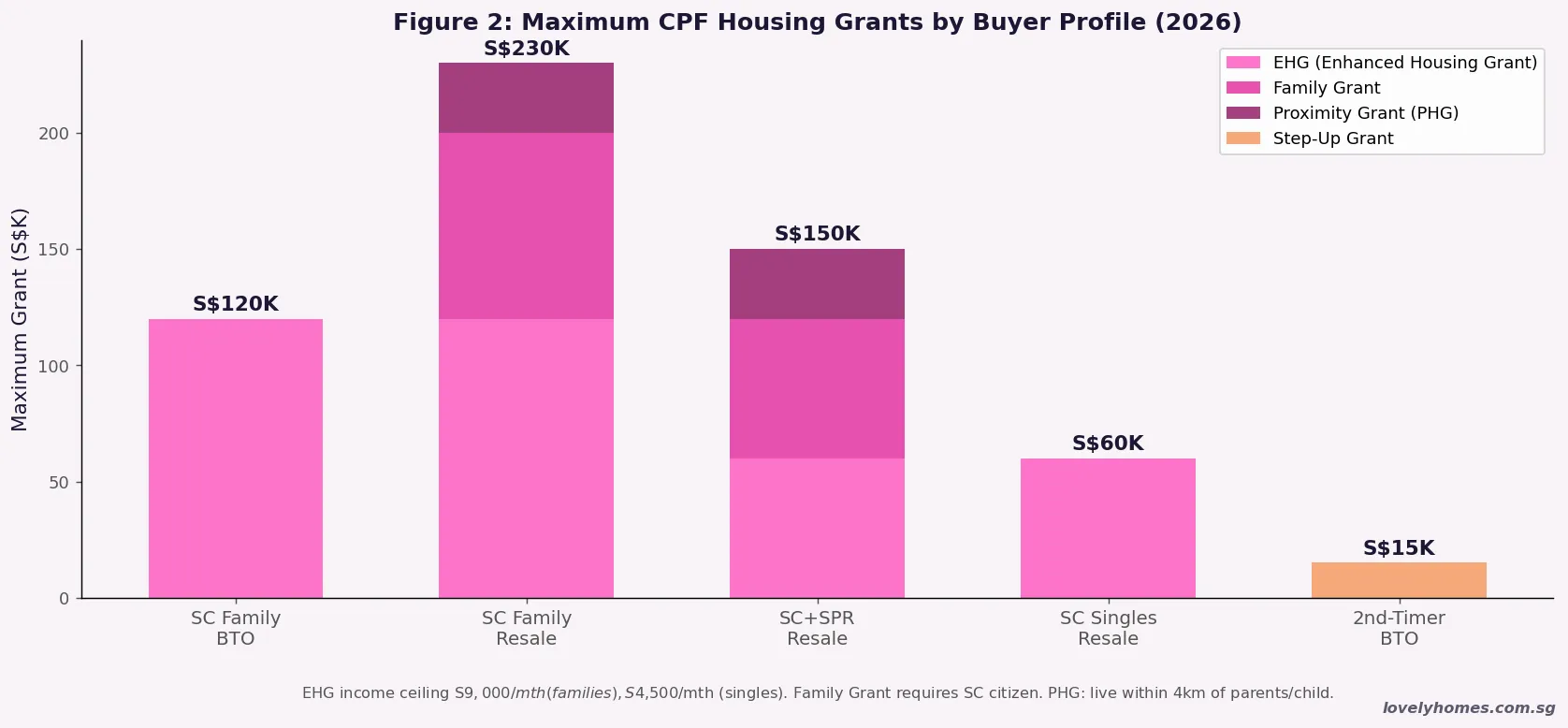

For applicants who were unsuccessful in the Berlayar Rise and Lakeview Cascadia ballots, the practical options are to re-apply in the October 2026 BTO exercise (details not yet announced), consider the concession flat allocation scheme which may direct them to Sembawang, or explore the HDB resale market where wait times are zero. Resale prices in mature estates have risen, but the Enhanced CPF Housing Grant (EHG) is available for resale purchases and can offset up to S$120,000 of the purchase price for eligible first-timers.

For families considering Sembawang, the below-1× first-timer rate means that applicants in this tranche are virtually guaranteed a flat if they apply — a rare situation in the BTO context. The trade-off is location and commute time, but Sembawang does offer genuine value: 4-room BTO flats in Standard Sembawang projects are typically priced in the S$330,000–S$430,000 range, representing the lowest entry point into new public housing available anywhere in the exercise.

What Might Come Next

The October 2026 BTO exercise is expected to launch in mid-October. HDB has indicated it will continue offering at least one Prime project per exercise to maintain supply at the most competitive tier. Industry observers expect the next Prime project to be in the Queenstown or Geylang/Kallang corridor, given the land parcels currently under preparation. For the Sembawang and Woodlands Standard supply overhang, HDB may consider adjusting pricing or flat-type mix in future launches to better match demand.

Frequently Asked Questions

What happens if a BTO project is undersubscribed?

If a BTO project does not receive sufficient applications to fill all available units within a flat type during the initial application period, HDB opens unsold flats for Sale of Balance Flats (SBF) exercises or re-offers them in subsequent BTO exercises. For the Sembawang Standard projects in June 2026, HDB’s concession flat scheme may direct unsuccessful applicants from oversubscribed projects to take up these units, often with a priority queue position. Buyers who accept concession flats in less popular projects lose the right to re-ballot in the same exercise but gain a guaranteed flat allocation.

What is the subsidy clawback for Berlayar Rise (Prime)?

The exact clawback percentage for Berlayar Rise has not yet been officially confirmed by HDB, but based on the precedent of the nearby Berlayar Residences (a Prime project from the October 2025 exercise), the clawback is estimated at approximately 14% of the resale price on first resale after the 10-year MOP. This means that if you sell a Berlayar Rise flat in 2036+ at, say, S$900,000, approximately S$126,000 would be clawed back by HDB before you receive your net sale proceeds. The clawback is intended to recover some of the Prime location subsidy from sellers who benefit from the price appreciation in the GSW area. Always check the specific clawback terms in your sales agreement.

Can first-timer singles apply for Berlayar Rise or Lakeview Cascadia?

First-timer singles (aged 35 and above) may apply for 2-bedroom flexi flats in Prime and Plus projects, subject to the same income ceiling (S$7,000 per month for singles) and the additional MOP/clawback conditions. However, the quota for singles in Prime projects is limited, and competition for 2-bedroom flexi units in Prime projects is historically intense. The June 2026 exercise did not publicly disclose the singles-specific application rate for Berlayar Rise or Lakeview Cascadia, but based on past exercises, 2-bedroom flexi units in Prime projects typically see subscription rates well above 5×.

What is the Minimum Occupation Period for these projects?

The MOP varies by classification: Prime projects (Berlayar Rise, Lakeview Cascadia) have a 10-year MOP. Plus projects (Kebun Baru Breeze and Ridge in Ang Mo Kio) have a 6-year MOP. Standard projects (Woodgrove Acres, Sembawang Portico, Sembawang Brook) have the standard 5-year MOP. During the MOP, owners cannot sell the flat on the open market or rent out the entire flat. Partial renting of individual rooms is permitted after an owner has fulfilled occupation requirements. The longer MOP for Prime and Plus projects is part of the policy design to moderate speculative demand and ensure these subsidised flats serve genuine owner-occupiers over the medium term.

When will the October 2026 BTO exercise launch?

HDB typically announces each BTO exercise approximately one month before applications open. Based on the 2025–2026 schedule, the October 2026 exercise is likely to open for applications in mid-to-late October 2026, with flat details announced in mid-September 2026. LovelyHomes will cover the October 2026 BTO launch as soon as HDB releases official details. You can subscribe to HDB’s e-alerts at homes.hdb.gov.sg to be notified when new launches are announced.

Related Articles

- HDB CPF Housing Grant Guide 2026: EHG, Family Grant, Step-Up, PHG and Singles Grant Explained

- Singapore HDB Resale Guide 2026: How to Buy, Price, and Negotiate

- HDB Ethnic Integration Policy Singapore 2026: Quotas, Eligibility and What Buyers Must Know

- HDB Resale Levy Singapore 2026: Complete Guide for Second-Timer Buyers

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer: Application rates and project details are sourced from HDB Singapore (as at 5pm, 24 June 2026) and industry reporting. Figures are subject to change as HDB publishes final ballot results. Subsidy clawback estimates are indicative based on comparable projects and are not official HDB figures for Berlayar Rise. Always refer to HDB’s official flat listings and consult a licensed property agent or HDB directly before making any application or purchase decision. LovelyHomes is not affiliated with HDB or any property agency.