Foreign Buyer Guide Singapore 2026: Eligibility, ABSD, Sentosa Cove & Financing

Buying property in Singapore as a foreigner is far from straightforward. The Republic runs one of the world’s tightest foreign-buyer regimes — a combination of the Residential Property Act, a 60% Additional Buyer’s Stamp Duty (ABSD), restrictive bank lending, and outright bans on most landed land and HDB flats. Yet thousands of foreigners do still buy here every year, drawn by Singapore’s rule of law, currency stability, and long-term capital story. This guide explains exactly what is allowed, what it costs, and how to plan the purchase without expensive surprises.

Throughout we use UK/Singapore English. All figures reflect rules in force as of April 2026 and the cooling-measures regime introduced on 27 April 2023. For the latest position, always cross-check the Singapore Land Authority Residential Property Act page, the IRAS stamp-duty page, and your appointed Singapore lawyer.

Quick Answer — foreign buyer guide at a glance

- Foreigners can buy condominiums, approved strata-landed units and apartments in Singapore.

- Foreigners cannot buy HDB flats or new Executive Condominiums (ECs) under the EC scheme.

- Mainland landed property requires Singapore Land Authority approval — very rarely granted.

- Sentosa Cove is the only landed enclave foreigners may own, and only for owner-occupation.

- ABSD: 60% on any residential purchase — first or fifth.

- Buyer’s Stamp Duty (BSD): progressive 1–6% on top of ABSD.

- Bank financing is typically capped at 50% LTV for foreign buyers, with shorter tenures and a higher rate spread.

- FTA nationals (US citizens; citizens and PRs of Iceland, Liechtenstein, Norway and Switzerland) get Singapore-Citizen ABSD treatment.

- Singapore CPF cannot be used — the entire down payment and stamp duty must come from offshore cash or banked-in funds.

Who counts as a “foreign buyer” in Singapore?

A “foreigner” for property purposes is any individual who is not a Singapore Citizen and not a Singapore Permanent Resident. Foreigners may be on long-term passes (Employment Pass, S Pass, EntrePass, Dependant’s Pass, Long-Term Visit Pass), Tech.Pass / ONE Pass holders, or simply non-residents. Pass-holder status is irrelevant to property law — what matters is whether you hold a Singapore IC as a Citizen or PR.

Companies and trusts are treated separately. A Singapore-incorporated entity buying residential property is still subject to ABSD at 65% (5% non-remittable for licensed housing developers, the remainder remittable in limited circumstances). A foreign-incorporated entity is treated as foreign throughout. Buying through a company structure, in 2026, generally costs more ABSD than buying personally — not less. We discuss this in the section on entity purchases below.

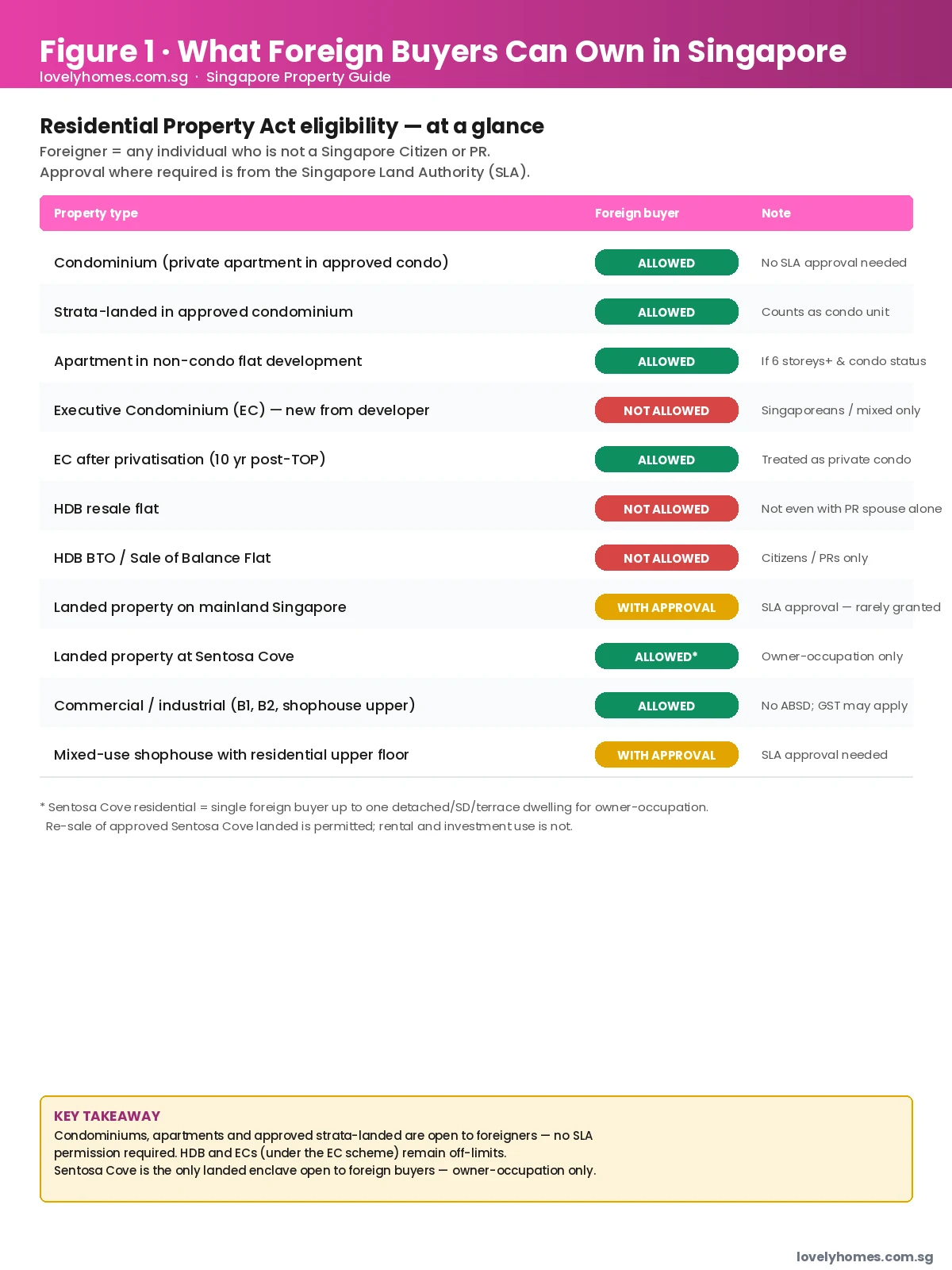

What foreigners can and cannot own — Residential Property Act in plain English

The Residential Property Act 1976 (RPA), administered by the Singapore Land Authority (SLA), is the single most important law for any foreign buyer. It distinguishes between “non-restricted residential property” (which foreigners may buy freely) and “restricted residential property” (which they generally may not). The matrix below sets out where each common Singapore property type sits.

To translate the matrix into practical advice:

- Condominiums — the dominant foreign-buyer asset class in Singapore. Any apartment in a condominium that has been gazetted as “non-restricted residential property” is open to foreign buyers without SLA approval. Almost every modern private condominium qualifies.

- Apartments in non-condo flat buildings — legal for foreigners only where the building is at least 6 storeys and has been classified as a condominium development by URA. Older walk-up apartments and converted houses often do not qualify.

- Executive Condominiums (ECs) — a hybrid public-private housing form. Under the EC scheme (the first 10 years from TOP) ECs are off-limits to foreigners entirely. Once an EC is fully privatised (10 years post-TOP), it trades as a private condominium and foreign buyers are welcome.

- HDB flats — both BTO and resale. Foreigners cannot buy HDB flats under any circumstance. A foreigner married to a Singapore Citizen may live in an HDB flat owned by the SC spouse, but cannot be on title.

- Landed property on the mainland — bungalows, semi-detacheds, terraces, town-houses, and cluster landed are all “restricted property”. A foreigner needs SLA approval, granted rarely and only on substantial economic-contribution grounds. Most applications are refused.

- Sentosa Cove — the one landed exception. Under a long-standing concession, a foreigner may own one detached, semi-detached or terrace dwelling at Sentosa Cove for owner-occupation. Investment letting and holiday-rental use are not permitted; SLA can act on covenant breaches.

- Commercial and industrial property — shophouse upper floors zoned commercial, B1/B2 industrial, retail and office strata units are not “residential” and therefore not within the RPA. Foreigners may buy freely. ABSD does not apply, although GST and other taxes do.

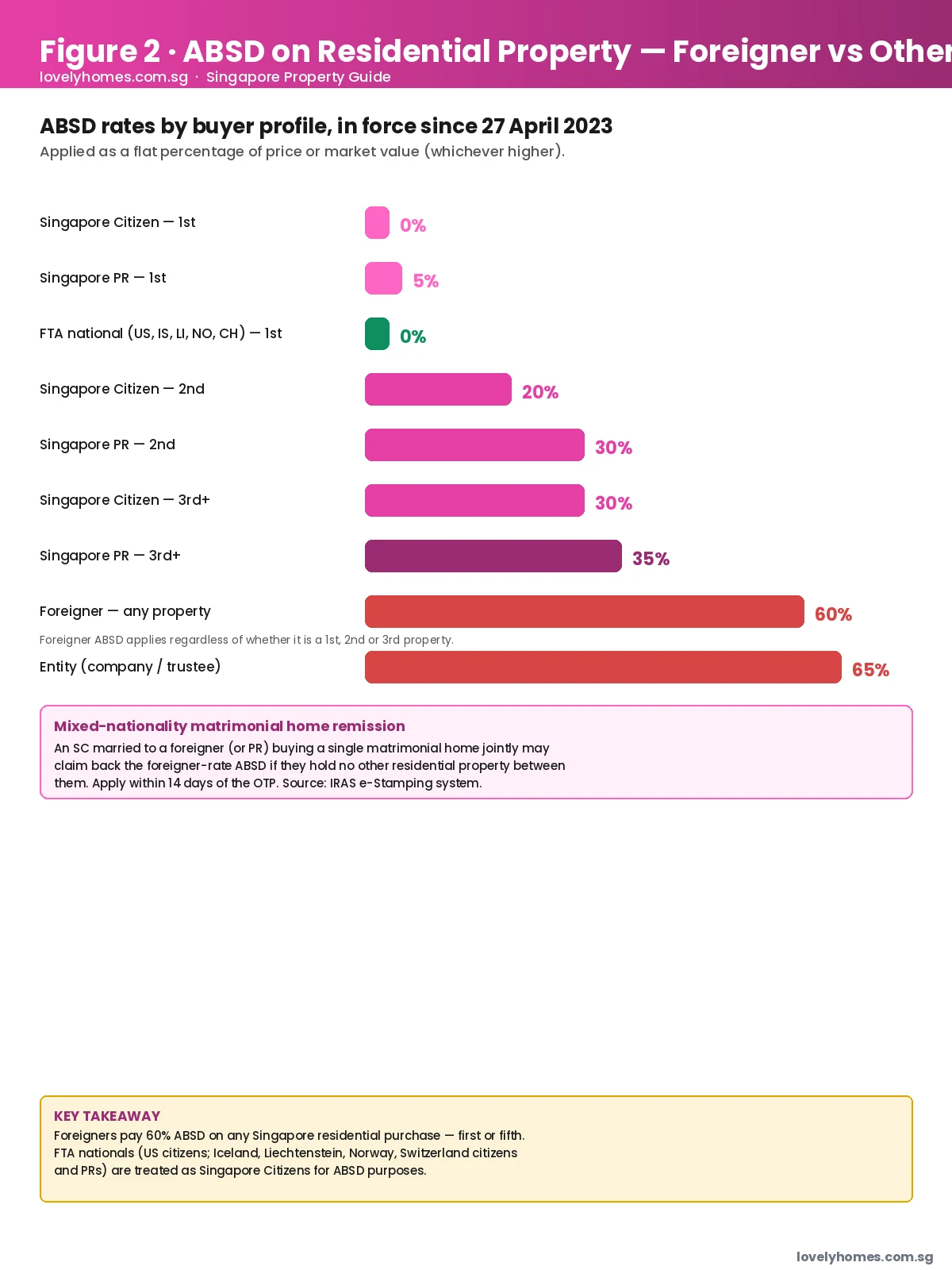

Free Trade Agreement (FTA) nationals — the citizenship “shortcut”

Singapore’s FTA framework with five countries treats those nationals (and in some cases their permanent residents) as Singapore Citizens for ABSD purposes:

- Citizens of the United States of America;

- Citizens and PRs of Iceland, Liechtenstein, Norway and Switzerland.

An eligible US citizen buying their first Singapore residential property therefore pays 0% ABSD, not 60%. This is a documentary entitlement — you must declare it on the e-stamping portal and produce the supporting passport/identification at stamping. The FTA exemption does not remove the Residential Property Act restrictions on landed property: an American buyer still cannot purchase a mainland bungalow without SLA approval.

The 60% ABSD — the single biggest cost

The Additional Buyer’s Stamp Duty (ABSD) is a flat-rate transaction tax on residential property purchases. For a foreign buyer in 2026, it is 60% of the purchase price or market value, whichever is higher. There is no “first property” discount — the rate applies whether it is the buyer’s first or twentieth Singapore property.

For full mechanics on ABSD — remissions, calculation rules, payment deadlines — see our complete ABSD Singapore guide. Two foreign-buyer-specific points are worth highlighting here.

Mixed-nationality matrimonial home remission

An SC married to a foreigner who buys a single matrimonial home jointly may apply for ABSD remission, paying ABSD at SC rates instead of foreigner rates. The conditions are strict:

- The couple must be legally married before the OTP is granted.

- The property must be held jointly as their only residential property between the two of them.

- Application must be made within 14 days of the document attracting duty (usually the OTP).

- If either spouse already owns another residential property, that property must be sold within six months.

The remission is one of the most powerful planning tools available to mixed-nationality couples. It can change a S$2 million purchase from S$1.2 million ABSD to zero, but the conditions must be observed precisely — an OTP signed in one party’s sole name disqualifies the remission, even if the title is later joint.

Decoupling and structuring

“Decoupling” — restructuring an existing co-owned property into a single-owner property so the freed spouse may buy a second residence at first-property rates — is a separate, intricate strategy primarily relevant to Singapore Citizen and PR couples, not foreigners. Where one spouse is foreign, the freed-up purchase still attracts the 60% rate and decoupling rarely helps. See our decoupling guide for the full mechanics.

Buyer’s Stamp Duty — on top of ABSD

Every property buyer in Singapore pays Buyer’s Stamp Duty (BSD), a progressive duty that ranges from 1% to 6% on residential purchases:

| Price band | BSD rate (residential) |

|---|---|

| First S$180,000 | 1% |

| Next S$180,000 | 2% |

| Next S$640,000 | 3% |

| Next S$500,000 | 4% |

| Next S$1,500,000 | 5% |

| Above S$3,000,000 | 6% |

BSD is calculated on the full purchase price; ABSD is then added on top. Both must be paid within 14 days of signing the OTP/Sale & Purchase Agreement. Late payment attracts penalties at IRAS’s stated rate. For a fuller worked example, see our Buyer’s Stamp Duty Singapore 2026 guide.

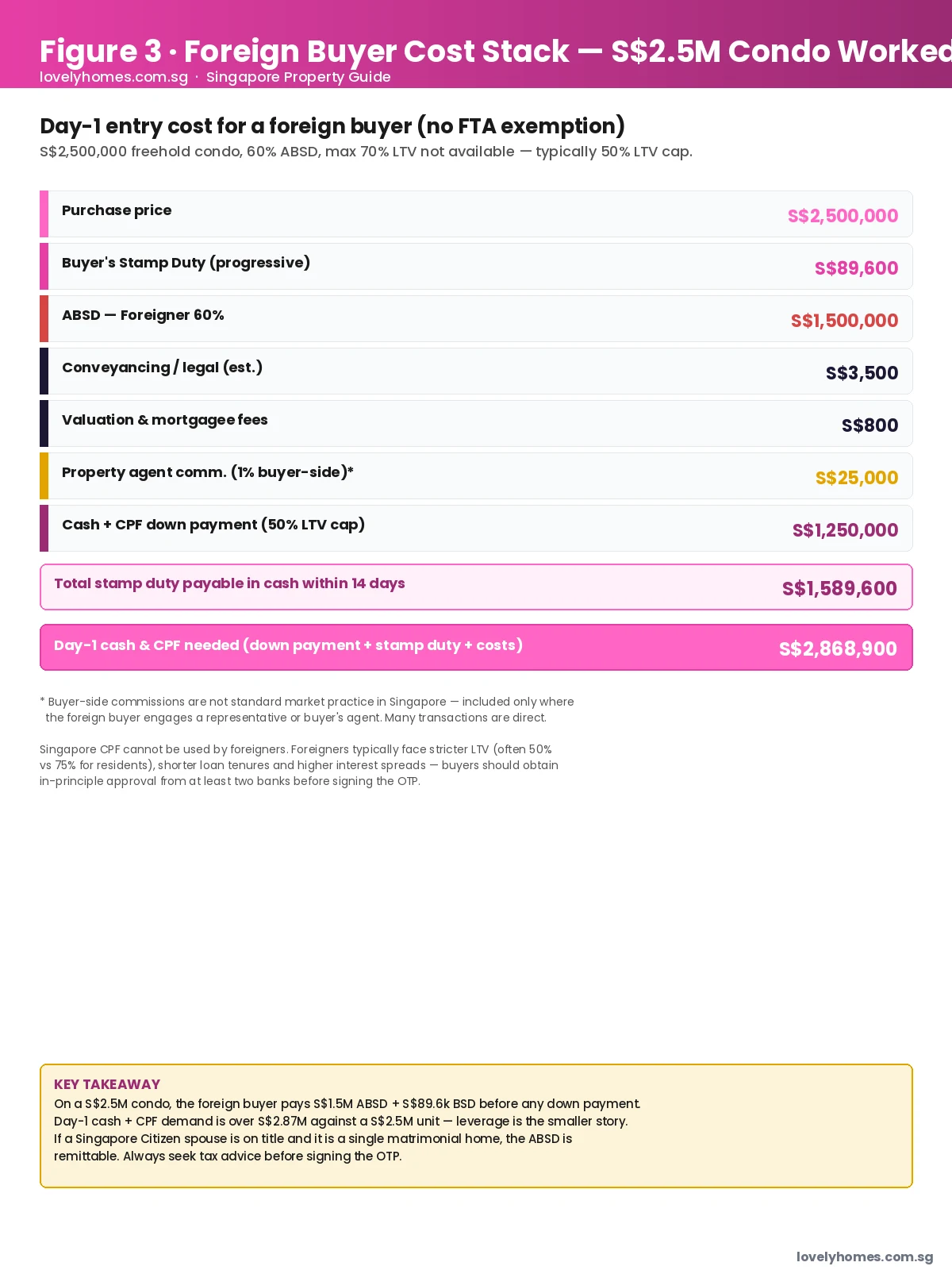

Worked example — S$2,500,000 freehold condo, foreign buyer

Take a freehold two-bedroom condominium in District 9 priced at S$2,500,000. The buyer is a foreign professional with no Singapore Citizen or FTA-eligible spouse. The full day-1 stack looks like this:

The mathematics is brutal but unambiguous. On a S$2.5 million purchase, the foreign buyer faces:

- Down payment at 50% LTV (foreigner cap): S$1,250,000;

- BSD on S$2.5 million: S$89,600;

- ABSD at 60%: S$1,500,000;

- Conveyancing legal fees, valuation report, mortgagee fees: S$4,000–5,000;

- Buyer-side commissions (where engaged): typically S$25,000.

Total day-1 cash and CPF (CPF being unavailable to foreigners, this is all cash): approximately S$2.87 million for a S$2.5 million unit. Singaporean buyers see roughly 35–38% upfront cost on a comparable purchase; foreign buyers see 115%. Plan accordingly.

Financing as a foreign buyer

Three financing realities sit on top of the stamp-duty position:

- Loan-to-Value (LTV) caps are tighter. Singaporean and PR borrowers can typically obtain up to 75% LTV on a first private property loan. Foreigner LTVs from local banks (DBS, OCBC, UOB) commonly cap at 50–55%, with some private-banking arrangements going higher subject to total relationship assets. Read our Singapore home loan guide 2026 for the LTV framework, MAS notice 632 caps and the broader picture.

- The TDSR still applies. The Total Debt Servicing Ratio caps total debt repayments at 55% of gross monthly income. Foreign buyers are stress-tested at the same 4% medium-term floor rate as residents, but lenders may apply income haircuts on overseas earnings (typically 30%). Our TDSR & MSR guide sets out the calculation in full.

- Loan tenures are typically shorter. Local banks frequently cap foreign-buyer tenures at 25 years (vs 30 for residents) and the loan must mature before age 65 in most cases. The combination of lower LTV and shorter tenure means the monthly instalment is materially higher than a comparable resident loan on the same unit.

We strongly recommend obtaining in-principle approval (IPA) from at least two banks before signing the OTP. The IPA is a written confirmation of the maximum loan you qualify for at current rates and is honoured for 30–60 days. Without an IPA, you may sign an OTP, fail bank approval, and forfeit the 1% option money.

Sentosa Cove — the one landed door open to foreigners

Sentosa Cove is a 117-hectare residential enclave on Sentosa Island, opened to foreign buyers in 2004 as a deliberate exception to the Residential Property Act. Around 2,000 detached, semi-detached and terrace homes plus a smaller number of condominiums sit on the cove, with private waterfront berths attached to many of the bungalows. The 99-year leases run from 2004 onwards, so most properties have 70–80 years of unexpired tenure as of 2026.

The conditions on foreign ownership at Sentosa Cove are restrictive:

- One foreign person/family may own one Sentosa Cove dwelling (additional Cove condos are bought through the standard condo route);

- The dwelling must be used for owner-occupation; renting out is not permitted under the RPA exemption;

- Re-sale to another foreign buyer is permitted, subject to the same one-dwelling rule;

- ABSD at 60% still applies on the purchase — the RPA exemption only relieves the foreign-ownership prohibition, not the duty.

Sentosa Cove prices in 2026 reflect the Cove’s small-supply / large-cheque-buyer dynamics: detached homes in the S$15–40 million range, semi-detached and terrace from around S$8 million. Most listings transact privately. Buyers should ensure their lawyer confirms the unit’s “non-restricted” status with SLA before signing the OTP.

Buying through a company or trust — usually a worse deal in 2026

Some foreign buyers ask whether a Singapore-incorporated company or family trust offers a better entry path. In 2026 the answer is generally no:

- Entity ABSD is 65% on residential purchases — 5 percentage points higher than the foreigner-individual rate;

- The 5-percentage-point “non-remittable” portion is paid even by licensed housing developers;

- Beneficial ownership of residential property by a foreign-controlled entity is monitored by SLA;

- Bank lending to a special-purpose vehicle is treated as foreigner financing for LTV purposes.

Entities continue to make sense for commercial and industrial portfolios, where ABSD does not apply. They make less sense for a single residential purchase in nearly every case. Always take Singapore tax and structuring advice before buying through any non-natural-person vehicle.

Summary table — foreign-buyer rule snapshot 2026

| Item | Position for a foreign individual buyer |

|---|---|

| Condo / approved apartment | Allowed; no SLA approval |

| HDB flat | Not allowed |

| EC under the EC scheme (first 10 years) | Not allowed |

| EC after privatisation | Allowed; treated as private condo |

| Mainland landed | SLA approval required — rare |

| Sentosa Cove landed | One dwelling, owner-occupation only |

| ABSD rate | 60% on every residential purchase |

| BSD rate | 1–6% progressive |

| CPF use | Not available |

| Typical bank LTV cap | 50–55% |

| FTA-national exception | US, IS, LI, NO, CH treated as SC for ABSD |

| Matrimonial home remission | Available where SC spouse is on title |

Why this matters — how Singapore compares

A 60% buyer-side stamp duty is one of the highest punitive rates on foreign property buying anywhere in the world. For comparison: Hong Kong’s Buyer’s Stamp Duty (BSD) for non-permanent residents is currently 7.5%; Australia’s federal foreign-purchaser surcharge plus state foreign-investor stamp duties run to 7–15% combined; the United Kingdom’s non-resident SDLT surcharge tops out at 17% on residential property; Canada has imposed a two-year moratorium on most foreign residential purchases altogether. None of those regimes approach Singapore’s 60% ABSD plus 6% BSD.

The policy intent is explicit: the Government uses ABSD as a deliberate brake on foreign capital in private residential property, prioritising owner-occupier affordability for Singaporeans. Industry figures show that foreign-buyer share of private home transactions has fallen from roughly 7% in 2020 to under 2% since the 27 April 2023 increase — the market has adjusted, and the floor has held. For the broader cooling-measures context see our cooling-measures timeline.

What might come next

The 60% rate has been in force since April 2023 with no public signal of relaxation. Two scenarios are conceivable in 2026–2028 but speculative:

- Targeted relaxation for high-end inventory. If unsold high-end CCR stock continues to overhang the market, the Government could cut the foreigner rate selectively (for example through an enhanced FTA list or a top-tier-residency property programme). Industry submissions during the 2025–2026 budget cycle have raised this. There is no policy commitment.

- Tighter screening of trust and corporate structures. Conversely, if hidden beneficial-ownership cases attract attention (the recent S$3 billion money-laundering case is widely cited), the Government could tighten reporting on non-natural-person buyers and family-trust transfers.

For active updates as policy moves see our Laws, Regulations & Policies and Property News sections.

Frequently Asked Questions

As an Employment Pass holder, am I a “foreigner” for property purposes?

Yes. Pass status is not relevant; only Singapore Citizenship or PR moves you out of the foreign-buyer category. EP, S Pass, EntrePass, Tech.Pass, ONE Pass and Dependant’s Pass holders all pay 60% ABSD on residential purchases.

Can I buy a Singapore property remotely without coming on-shore?

Yes, although it is harder. The OTP and Sale & Purchase Agreement can be signed via Power of Attorney (POA) to a Singapore lawyer, but most banks will require a physical signing of the loan documents and original passport sighting at the branch. KYC requirements at the lawyer’s end have also tightened — expect to provide certified copies of passport, address proof, and source-of-funds documentation.

If I become a Singapore PR after I sign the OTP, can I claim a refund of the foreigner ABSD?

No. The buyer profile at the date the document attracts duty (usually the OTP date) is what determines ABSD. Becoming a PR or SC subsequently does not unlock a remission. If your PR application is in advanced stages, time the OTP carefully — in edge cases waiting six to twelve weeks can change the rate by 30–55 percentage points.

Can I buy a Sentosa Cove property as an investment to rent out?

No. The Residential Property Act exemption that opens Sentosa Cove to foreign owners is conditional on owner-occupation. Letting out a Sentosa Cove dwelling acquired under the foreign-buyer concession breaches the covenant and SLA can act, including unwinding the transaction.

What is the difference between a “non-restricted” and “restricted” residential property?

“Non-restricted” residential property is condominiums, approved apartments, and strata-landed in approved condominium developments. Foreigners may buy these without SLA approval. “Restricted” residential property is mainland landed (detached, semi-detached, terrace, town-house, cluster), as well as some HDB flats and apartments in non-condo flat buildings. Foreigners need SLA approval, granted rarely. The Sentosa Cove concession is the main exception.

Will I be liable for Singapore property tax and rental income tax?

Yes. Property tax is owed by the owner regardless of citizenship and runs at owner-occupier or non-owner-occupier rates depending on use. Rental income from a Singapore property is Singapore-source income and is taxable in Singapore at non-resident rates (currently 24% on net rental income for non-residents, after deductible expenses). See our Singapore property tax guide for the full rate ladder.

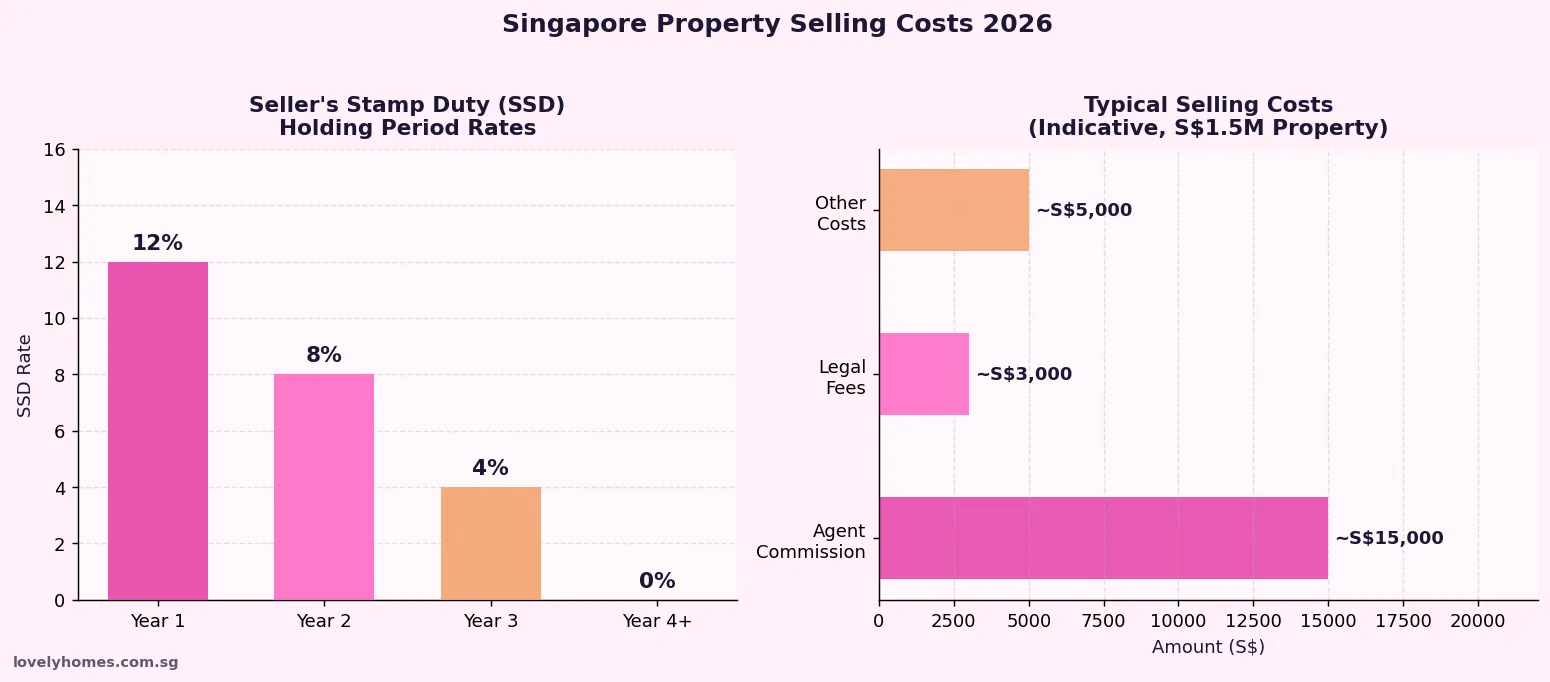

If I sell within three years, do I pay Seller’s Stamp Duty?

Yes, on the same basis as Singaporean sellers. SSD is 12% / 8% / 4% on the holding-period bands in years 1, 2, and 3, dropping to 0% from year 4. See our Seller’s Stamp Duty Singapore 2026 guide for worked examples and remission rules.

Related reading on LovelyHomes

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty Singapore 2026: Rates, Worked Examples & How to Calculate

- Property Conveyancing Guide Singapore 2026: OTP, S&P, Legal Fees & Timelines

- Singapore Home Loan Guide 2026: LTV, TDSR, Fixed vs SORA

- TDSR and MSR Singapore 2026: The Complete Borrowing Limits Guide

- Singapore Property Tax 2026: Owner-Occupier vs Investor Rates

- Seller’s Stamp Duty Singapore 2026

- Singapore Property Cooling Measures: Complete Timeline (2009–2026)

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. Eligibility under the Residential Property Act, ABSD remissions and bank-lending caps are fact-specific and change over time. Always verify the current position with the Singapore Land Authority, the IRAS Stamp Duty page, the Monetary Authority of Singapore and a licensed Singapore conveyancing lawyer before signing any OTP or Sale & Purchase Agreement.