Singapore Property Market Mid-Year Review 2026: H1 Results, Price Trends and 2H Outlook

Quick Answer: Singapore Property Market Mid-Year Review 2026

- Private prices up 0.9% QoQ in Q1 2026 — the sixth consecutive quarter of growth; Outside Central Region (OCR) leads at +2.2% QoQ.

- HDB resale dips −0.1% QoQ to RPI 203.4 — the first quarterly decline since Q2 2019, though still +1.2% year-on-year.

- Record 412 million-dollar HDB flats changed hands in Q1 2026, a new quarterly high despite the headline price softening.

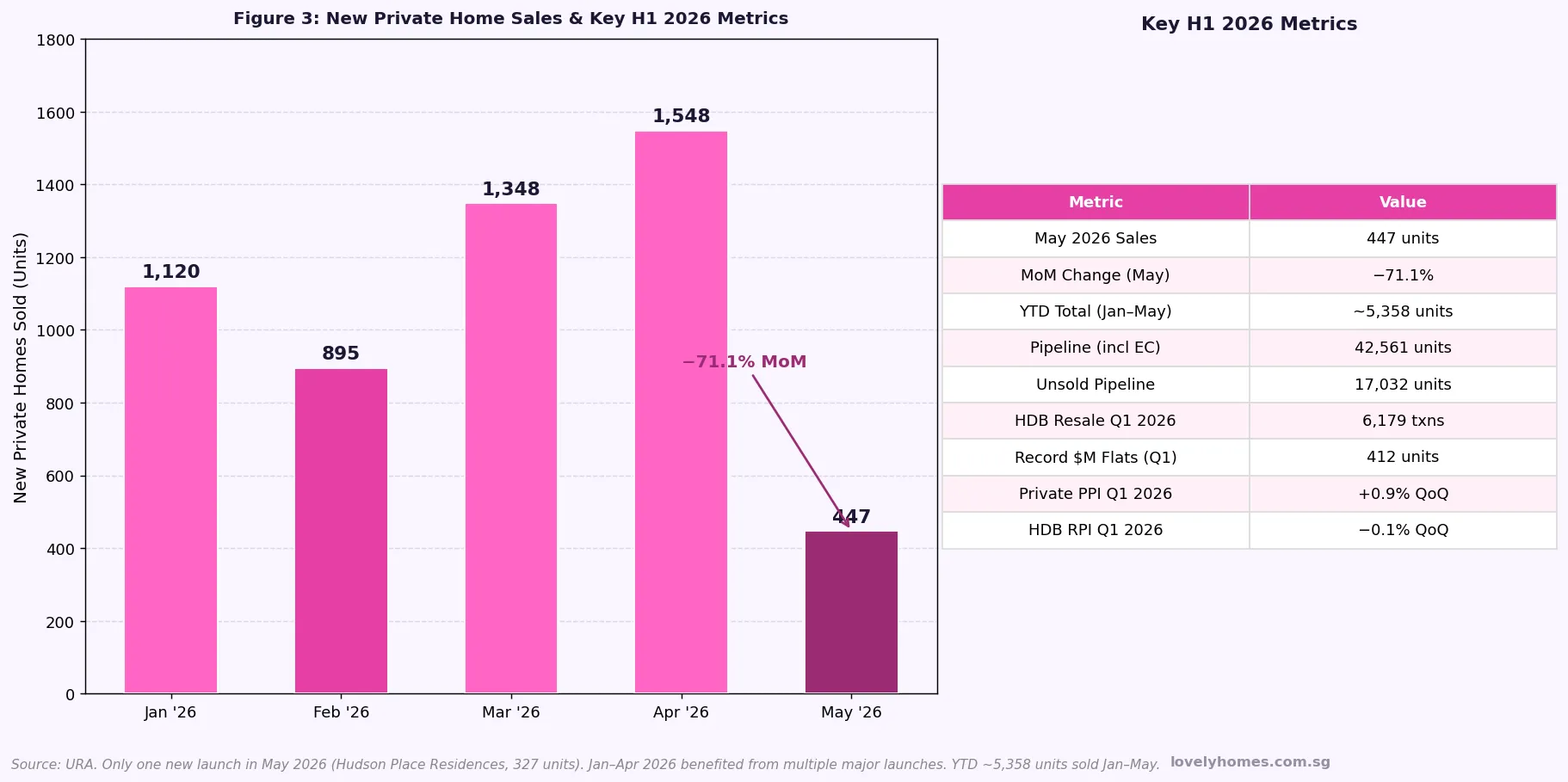

- Developer sales collapsed 71.1% MoM in May 2026 (447 units), reflecting a thin launch pipeline — only one project launched that month.

- 42,561 units in the pipeline (including ECs) with 17,032 unsold — providing a supply buffer that moderates price surges.

- Private rental softened −1.2% QoQ in Q1 2026; vacancy edged to 6.2%, though OCR bucked the trend with a modest +1.0% rental gain.

- 2H2026 GLS programme launched 9 confirmed sites (4,745 units), including the Jurong Lake District white site and Orchard Boulevard.

- River Valley Green Parcel C set a new CCR GLS benchmark at S$1,730 psf ppr (June 2026), signalling continued developer confidence in prime addresses.

- BTO June 2026 released 6,952 flats across 7 projects, including the first new HDB in Bishan in 40 years — absorbing first-timer demand from the resale market.

- Full-year 2026 private price growth forecast at ~3%; URA Q2 2026 flash estimates expected in the first week of July — watch for confirmation of the trend.

Introduction: Where Singapore Property Stands at Mid-Year 2026

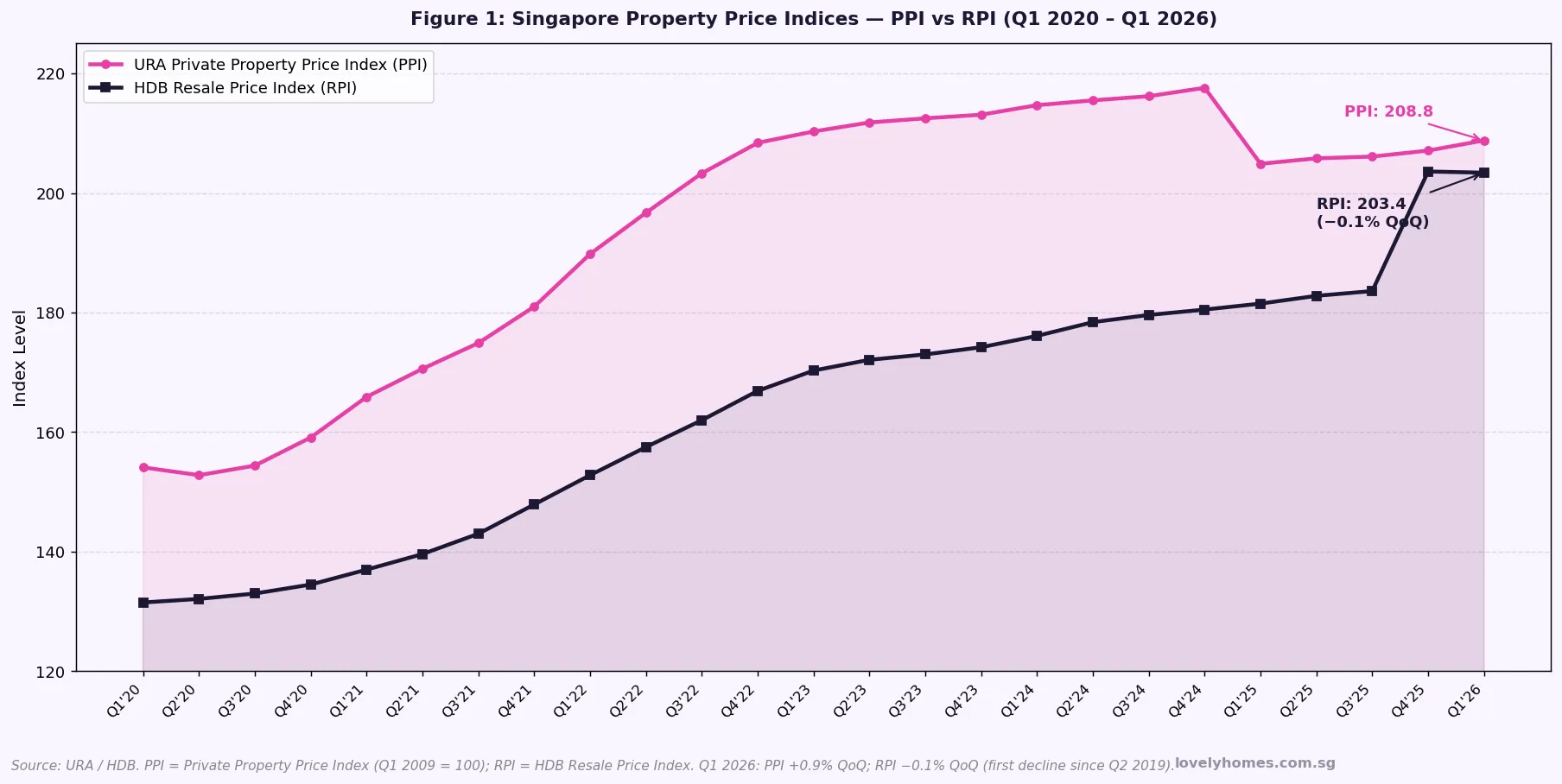

Six months into 2026, Singapore’s property market has delivered a split verdict. The private residential sector continues its steady upward march — the URA Private Property Price Index (PPI) rose 0.9% in Q1 2026, its sixth consecutive quarterly gain. At the same time, the HDB resale market recorded a rare 0.1% quarterly dip for the first time in nearly seven years, a signal that affordability constraints are beginning to bite in the public housing segment even as million-dollar flat transactions set new records.

This mid-year review consolidates the key price, transaction, supply, and rental data published by the Urban Redevelopment Authority (URA) and the Housing & Development Board (HDB) through Q1 2026, and frames the outlook for the second half of the year. Whether you are a first-time buyer weighing an HDB flat, an upgrader eyeing a new launch condominium, or an investor managing a rental property portfolio, understanding the H1 2026 data is essential context for decisions made in the months ahead.

Private Residential Market: Sixth Consecutive Quarter of Growth

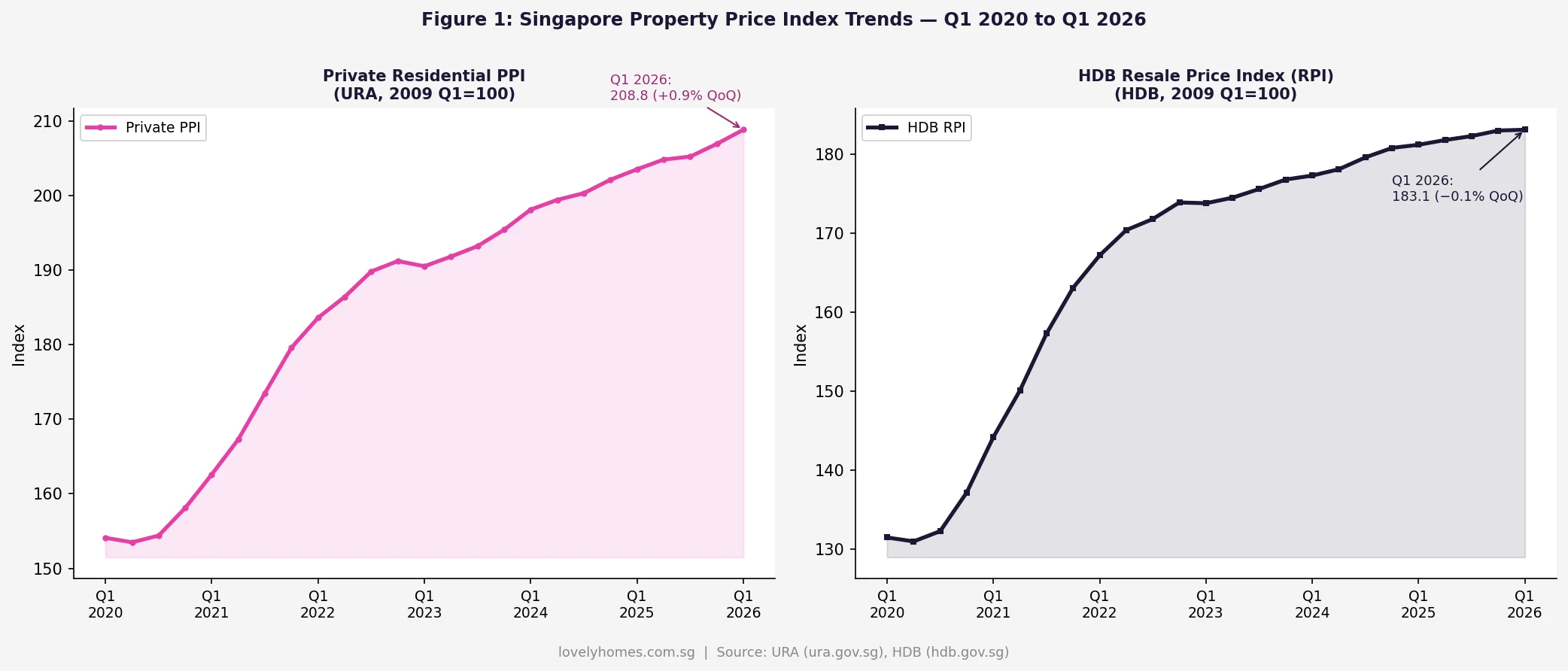

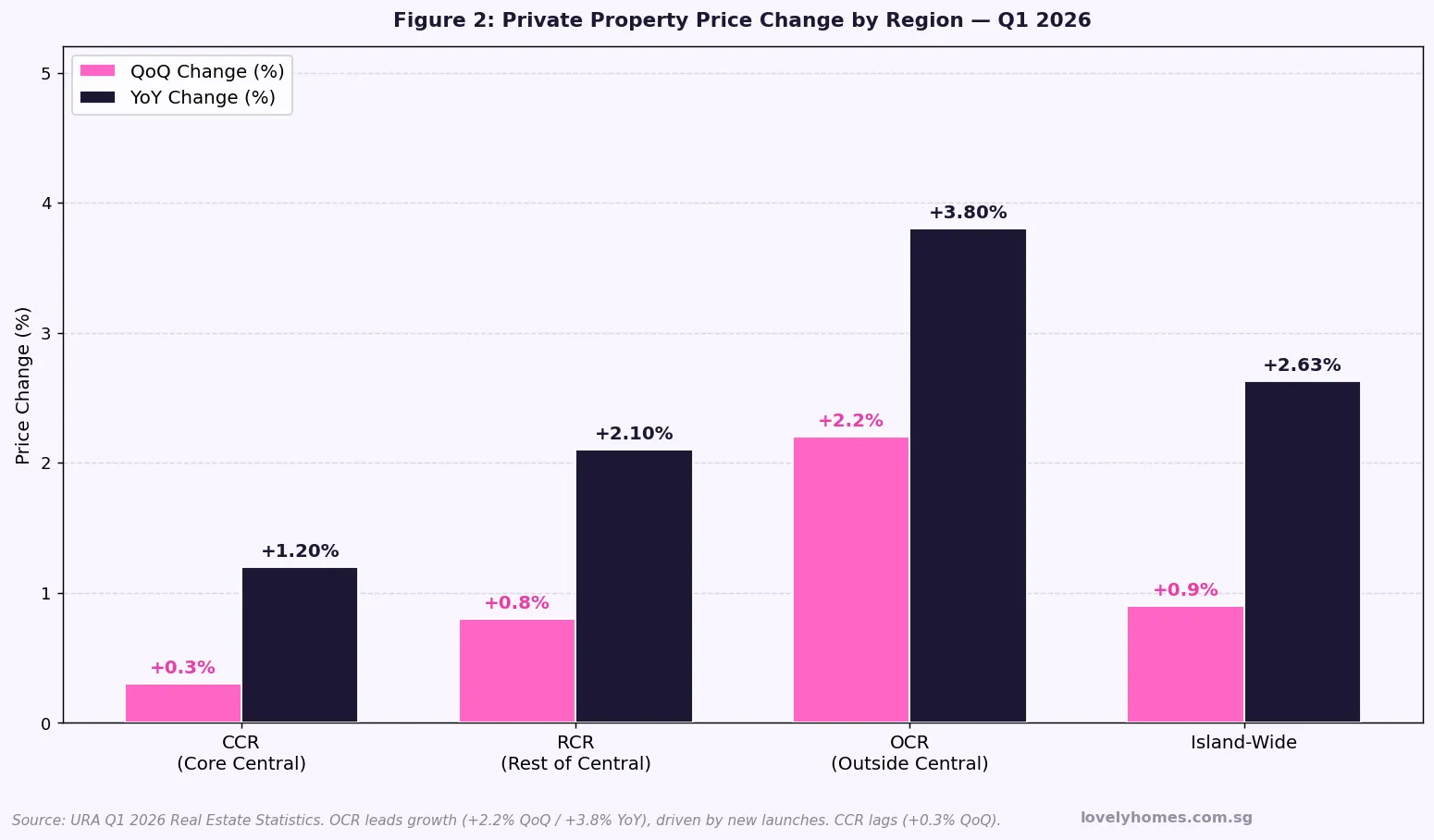

The URA’s Q1 2026 Real Estate Statistics confirmed a 0.9% quarter-on-quarter increase in the private residential PPI, bringing the index to 208.8. This builds on gains posted in every quarter since Q3 2024, and represents a 2.63% year-on-year improvement from Q1 2025.

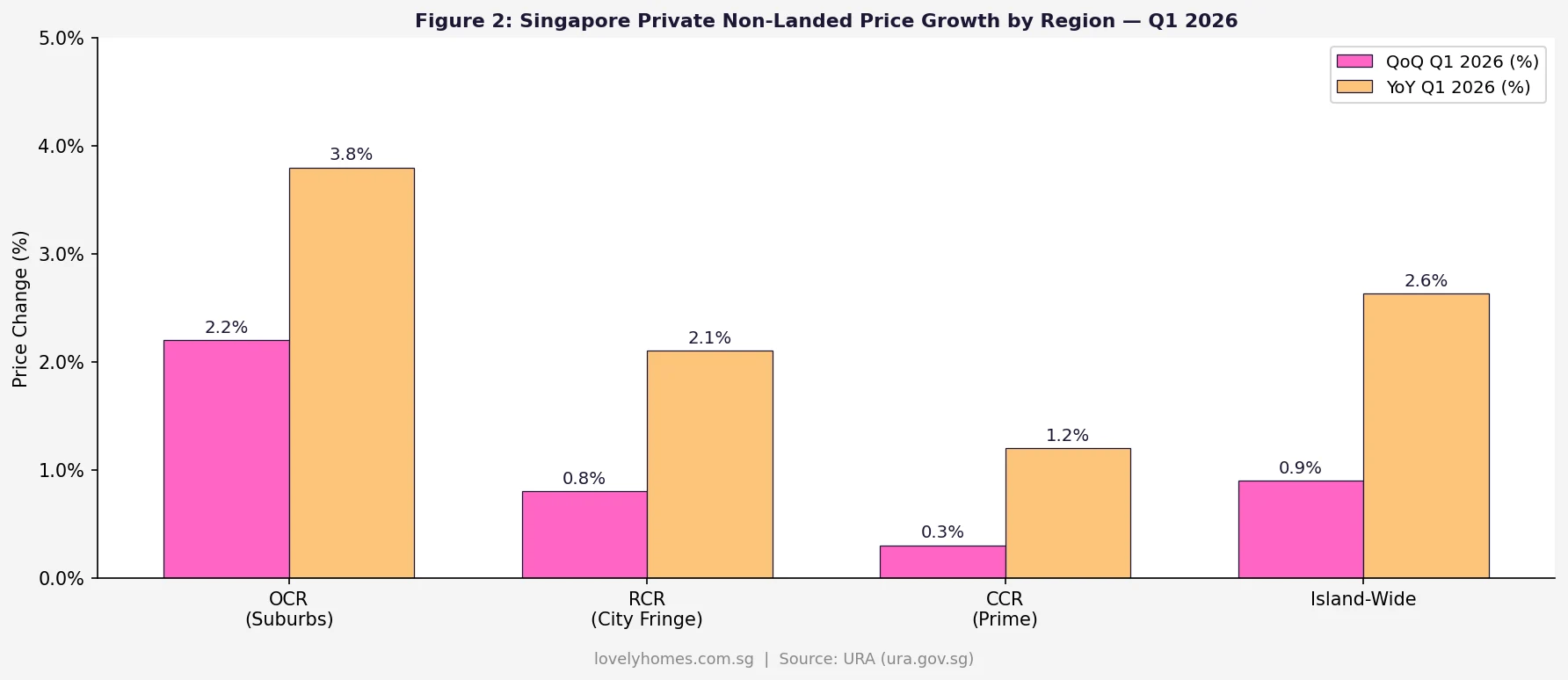

The growth, however, is not uniform across regions. The Outside Central Region (OCR) — Singapore’s mass-market suburban segment — leads with a 2.2% QoQ gain and 3.8% year-on-year increase, driven primarily by newly launched projects in areas such as Tampines, Tengah, and Bukit Batok. The Rest of Central Region (RCR) came in second at +0.8% QoQ, while the Core Central Region (CCR) advanced only 0.3% QoQ — reflecting the combined drag of high absolute prices, the 60% Additional Buyer’s Stamp Duty (ABSD) on foreign purchasers, and a thinner pipeline of new launches in the prime districts.

HDB Resale Market: First Price Dip in Seven Years

The HDB Resale Price Index (RPI) fell 0.1% in Q1 2026 to 203.4, the first quarterly decline since Q2 2019. While modest in numerical terms, the reversal ends a run of 26 consecutive quarters of price growth in the public resale market. On a year-on-year basis, the index remains 1.2% higher than Q1 2025, indicating that the longer-term trajectory of HDB prices is intact — this is a pause rather than a correction.

Transaction volumes, by contrast, accelerated sharply. HDB registered 6,179 resale transactions in Q1 2026, a 17.6% increase over Q4 2025’s 5,256 cases. This combination of higher volume alongside a slightly lower index is consistent with composition effects: more buyers are transacting in less mature estates or in smaller flat types, which pulls the index down even as demand itself remains solid.

Most strikingly, Q1 2026 saw a record 412 HDB resale flats change hands at S$1 million or above — surpassing the previous record. Executive flats and 5-room units in mature estates such as Queenstown, Bishan, and Toa Payoh account for the majority of these million-dollar transactions. The persistence of such transactions at elevated price points signals that a subset of buyers remains willing to pay premium prices for location, remaining lease, and flat condition.

New Launch and Developer Sales: Volatile Monthly Figures, Steady Fundamentals

Developer sales in Singapore fluctuate dramatically month to month, largely as a function of which projects happen to launch in any given period. May 2026 illustrated this vividly: only 447 new private homes were sold — a 71.1% month-on-month collapse from April 2026’s 1,548 units. This decline was not a market failure; it simply reflected the absence of major new launches, with only Hudson Place Residences (327 units in Balestier, 201 sold at an average S$2,458 psf) entering the market that month.

Year-to-date through May 2026, approximately 5,358 new private homes had been transacted — a healthy pace relative to 2025, which was itself a recovery year. The River Valley Green Parcel C Government Land Sales (GLS) tender, which closed on 18 June 2026, attracted four bids with the top offer of S$750.6 million (S$1,730 psf per plot ratio) from a Sunway-MCL-CSC Land joint venture. That result — a 22% premium over the adjacent Parcel B tender two years earlier — signals that developers remain confident in the absorption of prime CCR product, notwithstanding the 60% ABSD on foreign buyers.

Rental Market: Supply Headwinds Keep Rents Soft

Singapore’s private residential rental index declined 1.2% in Q1 2026, continuing the softening trend that began after the 2023 peak. Vacancy rates edged up from 6.0% in Q4 2025 to 6.2% in Q1 2026, reflecting the cumulative effect of completions from the elevated 2023–2025 GLS award cycle reaching the market simultaneously. Median condominium rents in Q1 2026 were approximately S$3,600 per month for a 2-bedroom unit in the OCR and S$5,200 per month for a 3-bedroom unit.

The OCR rental sub-market was an exception to the softening, posting a +1.0% QoQ gain, supported by demand from foreign professionals holding Employment Passes and from local upgraders seeking interim accommodation while awaiting new home completions. The CCR, where per-square-foot rents at S$6.20 are highest, saw the sharpest decline (−0.5% QoQ) as tenant options widened. HDB rental remained more resilient, supported by tighter eligibility controls and a smaller rental pool relative to demand.

Landlords pricing competitively — particularly in the RCR, where PSF rents fell 1.2% QoQ to S$5.40 — are finding that well-maintained, well-located units continue to attract tenants quickly. Those with outdated furnishings or aggressive asking rents are facing extended vacancy periods of 30 to 60 days in some cases.

Supply Pipeline and the 2H2026 GLS Programme

As at Q1 2026, 42,561 units (including executive condominiums) held planning approval, with 17,032 remaining unsold. This supply overhang provides a structural moderating force on private residential prices — a concern acknowledged by analysts who forecast full-year 2026 private price growth in the 2% to 4% range, with consensus estimates clustering around 3%.

The Government announced the 2H2026 GLS Confirmed List on 3 June 2026, comprising nine sites with a combined yield of approximately 4,745 units. Key sites include: the Jurong Lake District (JLD) white site (mixed use, yielding approximately 1,760 residential units), Orchard Boulevard (approximately 485 units in the CCR), Lentor Gardens Parcels A and B, Bayshore Road (mixed use), and the Jurong East executive condominium site. These awards, once tendered and developed over the 2027–2030 horizon, will continue the government’s policy of maintaining adequate supply to prevent speculative price surges.

On the HDB side, the June 2026 BTO exercise launched 6,952 flats across seven projects in Ang Mo Kio, Bishan, Bukit Merah, Sembawang, and Woodlands. Notably, the Bishan Lakeview and Bishan Shunfu projects mark the first new HDB flats in the Bishan estate in over four decades — a significant milestone that generated substantial first-timer interest. With approximately 50% of the June 2026 BTO units classified as Plus or Prime (carrying enhanced restrictions including a 10-year Minimum Occupation Period and tighter rental and resale conditions), the absorption of first-timer demand from the resale market may ease more gradually than prior exercises.

Key H1 2026 Metrics at a Glance

| Metric | Value / Change | Source / Notes |

|---|---|---|

| URA Private Property PPI (Q1 2026) | 208.8 (+0.9% QoQ, +2.63% YoY) | URA Q1 2026 Real Estate Statistics |

| HDB Resale Price Index (Q1 2026) | 203.4 (−0.1% QoQ, +1.2% YoY) | HDB Q1 2026 — first decline since Q2 2019 |

| OCR Price Change (Q1 2026) | +2.2% QoQ / +3.8% YoY | URA — leads all regions |

| CCR Price Change (Q1 2026) | +0.3% QoQ / +1.2% YoY | URA — moderated by ABSD impact on foreign buyers |

| New Private Homes Sold (May 2026) | 447 units (−71.1% MoM) | URA — thin launch month; one project launched |

| YTD Developer Sales (Jan–May 2026) | ~5,358 units | URA — healthy pace vs 2025 |

| HDB Resale Transactions (Q1 2026) | 6,179 (+17.6% QoQ) | HDB — strong demand rebound |

| Million-Dollar HDB Flats (Q1 2026) | 412 (new quarterly record) | HDB — 5-room / exec flats in mature estates |

| Private Pipeline (incl ECs) | 42,561 units; 17,032 unsold | URA Q1 2026 |

| Private Rental Index (Q1 2026) | −1.2% QoQ; vacancy 6.2% | URA — supply pressure from recent completions |

| River Valley Green Parcel C GLS | S$1,730 psf ppr (top bid) | URA tender closed 18 June 2026 |

| 2H2026 Confirmed GLS Supply | 9 sites / ~4,745 units | URA / MND — announced 3 June 2026 |

Worked Example: The Lim Family — Deciding Whether to Buy in H2 2026

Mr and Mrs Lim are a Singapore Citizen couple with a combined gross monthly income of S$14,000. Their HDB flat in Tampines (5-room, purchased 2019) completed its 5-year Minimum Occupation Period (MOP) in 2024. They wish to upgrade to a condominium in the OCR — specifically, they are considering a 3-bedroom unit at an upcoming Tampines new launch priced at S$1.65 million.

As first-time private property purchasers (they currently own only the HDB flat), the ABSD position is as follows: under the SC Couple ABSD Remission Scheme, they may purchase the condo and pay 20% ABSD (S$330,000 in cash), then sell their HDB within 6 months of the condominium’s completion to qualify for a full ABSD refund. Alternatively, if they sell their HDB first, they become first-time private buyers and pay zero ABSD — but they would need interim rental accommodation, adding approximately S$3,200 to S$3,600 per month in rent costs. The BSD on S$1.65 million is S$47,600 (payable from CPF).

On the mortgage, with S$14,000 gross income and no other credit obligations, the maximum TDSR-55% exposure is S$7,700 per month. A 75% LTV loan of S$1,237,500 at 3.2% over 30 years costs approximately S$5,338 per month — representing a TDSR of 38.1%, comfortably within the limit. Their HDB CPF Ordinary Account balance of S$280,000 can fully cover the BSD and contribute toward the cash down payment. With H1 2026 data showing OCR prices rising fastest (+2.2% QoQ), waiting beyond 2026 carries the risk of further price appreciation — the Lim family’s analysis suggests buying now, with the ABSD remission strategy, offers the most cost-effective path.

Why H1 2026 Data Matters for Buyers, Sellers and Investors

The divergence between private and HDB price trends in Q1 2026 has meaningful implications across buyer segments. For HDB upgraders, the slight moderation in HDB resale prices — combined with continued OCR private price growth — may marginally compress the equity gain from a resale flat sale. However, the record pace of million-dollar HDB transactions indicates that well-located mature-estate flats continue to attract premium valuations, providing upgraders with strong exit equity.

For investors, the rental market data warrants careful attention. A 1.2% QoQ decline in private rental coupled with rising vacancy rates suggests that the yield compression of 2024–2025 is continuing into 2026. Gross yields in the CCR have compressed to approximately 2.6% — below the prevailing bank fixed deposit rate — prompting a reassessment of the investment case for prime rental properties. OCR yields remain more attractive at approximately 4.0% to 4.5%, supported by domestic upgrader demand for rentals.

For sellers, the RPI dip is a reminder that the HDB resale market is not a one-way escalator. The combination of a large June 2026 BTO exercise absorbing first-timer demand, a growing pool of alternative supply from Plus and Prime flats reaching resale eligibility in future years, and affordability constraints on younger buyers, suggests that HDB resale price growth in H2 2026 will remain modest.

What Might Come Next in H2 2026

Several events and data releases will shape Singapore’s property market in the second half of 2026. The URA Q2 2026 flash estimates — expected in the first week of July 2026 — will provide the first indication of whether the private market maintained its growth trajectory or softened in the April-to-June period. Analysts will be particularly focused on whether the OCR can sustain its outsized QoQ gains given that multiple new launches — including projects in Tengah and Bukit Timah — were scheduled for the quarter.

On the supply side, the Lorong Puntong GLS tender (0.43 ha, approximately 140 units, near Bright Hill MRT) was scheduled for launch in late June 2026, with results expected in Q3 2026. The Sembawang Drive executive condominium GLS site — the first EC in the north of Singapore to be tendered under the new 10-year MOP rules — will also attract close attention for its pricing implications on the EC market. Should these tenders attract aggressive bids — as River Valley Green Parcel C did — it would signal continued developer confidence despite rising completion volumes.

ABSD policy is, for the time being, unchanged. The current rates — 20% for Singapore Citizens purchasing a second property, 60% for foreigners — remain in place as structural cooling measures. Any adjustment would likely require a material deterioration in market fundamentals or a significant policy signal from the Ministry of National Development. For H2 2026, the base case among analysts is steady rates, steady growth of roughly 2% to 3%, and continued healthy transaction volumes in both HDB resale and new launches.

Frequently Asked Questions

What does the PPI +0.9% in Q1 2026 mean for buyers?

The 0.9% quarterly gain in the URA Private Property Price Index (PPI) reflects the weighted average price movement across all private residential transactions in Q1 2026. For a buyer purchasing a S$1.5 million condominium, a 0.9% QoQ increase would translate to approximately S$13,500 of price appreciation in a single quarter — though individual property price movements vary significantly by location, project age, and unit attributes. The PPI is most useful as a market-wide temperature gauge rather than a predictor of any specific property’s trajectory. Buyers should note that OCR prices (+2.2% QoQ) rose substantially faster than the island-wide average, suggesting stronger near-term price momentum in suburban new launches.

Why did HDB resale prices dip in Q1 2026 despite record million-dollar transactions?

These two data points are not contradictory. The HDB Resale Price Index (RPI) uses a regression model that controls for flat type, floor area, remaining lease, and town — it measures the like-for-like price movement, stripping out changes in the composition of what transacted. In Q1 2026, a higher share of transactions occurred in non-mature estates and in smaller flat types, which mathematically pulled the index down even as premium flats in mature estates continued to transact at record prices. The 412 million-dollar transactions reflect demand for a specific niche of the HDB market — larger, well-located flats with long remaining leases — rather than the broad-based market captured by the RPI.

Should I wait for Q2 2026 data before making a buying decision?

Timing the market based on quarterly index releases is rarely a reliable strategy. By the time URA publishes Q2 2026 flash estimates (expected first week of July 2026), property prices will reflect conditions from April to June — data that is already two to three months old. More importantly, the index captures market-wide trends, not the specific property you intend to purchase. If a target property fits your financial capacity (TDSR and MSR within limits), your housing needs, and your long-term plans, waiting for one additional data point is unlikely to materially improve the outcome. The more useful discipline is ensuring your ABSD position is optimised and your mortgage is competitively priced before signing the Option to Purchase.

Is the private rental market going to keep falling in H2 2026?

The primary driver of private rental softening — elevated completions from the 2023–2025 construction cycle — will continue to exert downward pressure through at least mid-2027, as the bulk of the pipeline reaches the market. However, rental declines are unlikely to be severe because demand from foreign professionals (Employment Pass and S Pass holders) and domestic upgraders awaiting new home completion provides a floor. The OCR rental market, which already posted a positive 1.0% QoQ gain in Q1 2026, is likely to prove the most resilient. Landlords in the CCR should price realistically and invest in renovation quality to stand out in a market where tenants have expanding choices.

What is the significance of the River Valley Green Parcel C S$1,730 psf ppr bid?

The S$1,730 psf per plot ratio (psf ppr) top bid on River Valley Green Parcel C — submitted by a Sunway MCL and CSC Land joint venture — represents the highest CCR GLS land rate in Singapore’s history for that precinct. The psf ppr metric reflects the price paid per square foot of the site’s plot ratio (i.e., the total allowable gross floor area). When developers pay S$1,730 psf ppr, they typically need to sell the resulting apartments at approximately S$2,800 to S$3,200 psf to achieve acceptable returns after construction costs, professional fees, financing costs, and developer profit. This benchmarks what buyers can expect the eventual River Valley Green project — likely marketed in 2027 or 2028 — to be priced at upon launch.

How does the 2H2026 GLS programme affect buyers of new launches?

The nine confirmed list sites in the 2H2026 GLS programme — comprising approximately 4,745 units including the Jurong Lake District white site and Orchard Boulevard — will take two to four years to develop and launch. GLS awards made in 2H2026 will therefore result in new projects entering the market approximately in 2028 to 2030. For buyers considering new launches in 2026 or 2027, the GLS pipeline primarily affects expectations about the medium-term supply environment rather than the immediate availability of units. It also provides comfort that the government is managing supply actively — a signal that extreme price surges, as seen in 2021 to 2023, are unlikely to recur in this cycle.

Can Singapore Citizens pay ABSD in CPF?

No. ABSD — including the 20% levied on Singapore Citizens purchasing a second property — must be paid entirely in cash. Only Buyer’s Stamp Duty (BSD) may be paid from the CPF Ordinary Account (for properties purchased for occupation, not purely for investment). For a second property purchase at S$1.65 million, the ABSD of S$330,000 must be funded from cash savings. If the buyer is a Singapore Citizen couple who currently own one HDB flat and are purchasing a private property with intent to sell the HDB within 6 months of the new property’s completion, they may qualify for a full ABSD remission under the SC Couple Remission Scheme — in which case the S$330,000 is paid upfront and later refunded by the Inland Revenue Authority of Singapore (IRAS).

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Cooling Measures Guide 2026: ABSD, TDSR, LTV and SSD Explained

- Singapore Property Market Mid-Year Outlook 2026

- Singapore 2H2026 GLS Programme Guide: 9 Sites, 4,745 Units

- Singapore HDB Flat Eligibility Guide 2026: HFE Check, Income Ceilings and Qualifications

- Singapore Property Mortgage Guide 2026: SORA, Fixed vs Floating, LTV and Refinancing

- Singapore First-Time Buyer Guide 2026: HDB, Resale or New Launch?

Disclaimer

This article is for general informational purposes only and does not constitute financial, legal, or property investment advice. All property price data is sourced from official releases by the Urban Redevelopment Authority (URA) and the Housing & Development Board (HDB). ABSD rates, BSD rates, CPF rules, LTV limits, and TDSR thresholds are correct as at June 2026 and are subject to change without notice. Readers should verify current rates at ura.gov.sg, hdb.gov.sg, iras.gov.sg, and mas.gov.sg before making any property transaction. All worked examples use illustrative figures; individual circumstances vary. Consult a licensed mortgage broker, conveyancing solicitor, and CEA-registered property agent for advice specific to your situation.

Click anywhere or press Esc to close